Our Marketing Team at PopaDex

Master Your Finances with the 20 30 50 Rule

The 20 30 50 rule is a simple but powerful budgeting strategy that puts your savings first. The idea is to split your after-tax income into just three buckets: 20% for Savings and Debt, 30% for Wants, and 50% for Needs. By dedicating a slice of your income to your financial future before anything else, it makes saving an intentional, non-negotiable part of your monthly routine.

What Is the 20 30 50 Budgeting Rule?

Imagine getting your paycheck and immediately paying your future self—before you even think about rent, groceries, or that morning coffee. That’s the core idea behind the 20 30 50 rule. It’s a budgeting framework that flips the script by prioritizing your financial goals instead of treating them as an afterthought.

Most people pay their bills, cover their expenses, and then try to save whatever is left over, if anything. This rule does the opposite. It forces you to set aside the most important “ingredient”—your savings—right from the start.

This approach ensures you’re always making progress. Whether your goal is to build a solid emergency fund, start investing for retirement, or aggressively pay down high-interest debt, this method carves out the money to make it happen.

Understanding the Categories

The beauty of this framework is its simplicity. You don’t need a complicated spreadsheet with dozens of line items. All your spending just falls into one of three buckets.

Here’s a quick overview of how your after-tax income gets divided.

The 20 30 50 Rule at a Glance

| Percentage | Category | Description and Examples |

|---|---|---|

| 20% | Savings & Debt Repayment | This is your “pay yourself first” money. It covers retirement contributions, investments, emergency fund savings, and extra payments on credit cards or student loans. |

| 30% | Wants | Your lifestyle fund. This is for all the non-essentials that make life more enjoyable, like dining out, hobbies, streaming services, concert tickets, and vacations. |

| 50% | Needs | These are your essential, must-pay expenses. Think rent or mortgage, groceries, utilities, transportation to work, and insurance premiums. |

This clear structure gives you a balanced way to manage your money without getting bogged down in the details.

If you’ve heard of other percentage-based budgets, this might sound familiar. It’s actually a spin on a more common framework. We break down its popular cousin in our guide to the 50/30/20 budget. The only real difference is which financial goal you decide to tackle first.

Why Prioritizing Savings Changes Everything

On the surface, the 20 30 50 rule seems like a simple reshuffling of its more famous cousin, the 50/30/20 rule. The percentages are identical, but flipping the order completely changes the game. It’s the difference between saving what’s left over versus spending what’s left over.

And that small tweak makes all the difference.

By putting 20% toward savings and debt repayment first, you turn wealth-building into a non-negotiable part of your budget, not an afterthought. This “pay yourself first” approach isn’t just a catchy phrase; it’s a powerful commitment you make to your future. You stop hoping there’s money left at the end of the month and start ensuring your goals are funded from day one.

This proactive mindset fundamentally re-engineers your relationship with money. It creates a guardrail for anyone prone to impulse buys and puts disciplined savers on the fast track to automating their success.

A Mindset Shift from Reactive to Proactive

When you cover your needs and wants first, saving often takes a backseat. It’s way too easy for “lifestyle creep” to quietly eat up your income, leaving little—or nothing—for your long-term goals. The 20 30 50 rule flips the script. It forces you to make conscious spending decisions based on what remains after you’ve secured your savings.

This simple change reframes your entire budget. You stop asking, “How much can I afford to save?” and start asking, “How can I live on the money I have left after saving?”

Of course, when you prioritize savings, the first order of business is building a safety net. Learning how to build an emergency fund ensures you have a cash cushion for life’s surprises without derailing your progress. Once that foundation is solid, your 20% can go full-throttle into investing, retirement accounts, and knocking out high-interest debt.

To really see the difference in action, let’s put the two philosophies head-to-head.

Comparing Budgeting Philosophies 20 30 50 vs 50 30 20

A side-by-side comparison of the two budgeting rules reveals just how much a simple change in priority can impact your financial habits and outcomes.

| Aspect | 20 30 50 Rule (Savings-First) | 50 30 20 Rule (Expenses-First) |

|---|---|---|

| Core Philosophy | Pay yourself first to guarantee progress toward financial goals. | Cover essentials first, then allocate remaining funds to wants and savings. |

| Psychological Impact | Builds discipline and treats saving as a fixed, essential expense. | Can make savings feel like an optional leftover if spending exceeds projections. |

| Typical Outcome | Leads to consistent and automated wealth building. Financial goals are met more reliably. | Savings can be inconsistent, especially in months with unexpected expenses. |

| Best For | Individuals who want to aggressively build wealth and ensure they always hit savings targets. | Beginners who are just starting to track expenses and need a simple framework. |

At the end of the day, choosing the 20 30 50 rule is about making a deliberate choice for your future. It’s an active strategy, not a passive hope, that ensures you’re consistently building a secure financial foundation, one paycheck at a time.

Putting the 20 30 50 Rule into Practice

Alright, let’s move this from theory to reality. Turning the 20 30 50 rule into a working budget is actually pretty straightforward once you get the hang of it.

The most critical first step? Starting with the right number. We’re not talking about your gross salary; we’re talking about your actual take-home pay. This is the money that hits your bank account after all the deductions—taxes, healthcare, retirement contributions—have been taken out.

This after-tax figure is the true foundation of your budget. Getting it right is everything, because it keeps your plan grounded in reality, not wishful thinking. For a detailed breakdown, check out our guide on how to calculate disposable income to make sure your starting line is accurate.

Once you’ve got that magic number, the rest is just simple multiplication.

Calculating Your Budget Buckets

Let’s walk through it with a quick example. Say your monthly take-home pay is $4,000.

- Calculate Your Savings (20%): Multiply your income by 0.20. So, $4,000 x 0.20 = $800. This is your monthly target for savings, investments, or blasting away at extra debt payments.

- Calculate Your Wants (30%): Next, multiply by 0.30. In this case, $4,000 x 0.30 = $1,200. This is your fun money—the flexible cash for dining out, hobbies, and streaming subscriptions.

- Calculate Your Needs (50%): Finally, multiply by 0.50, which gives you $4,000 x 0.50 = $2,000. This bucket is reserved for all your absolute essentials, like rent, utilities, and groceries.

Just like that, you have clear spending targets. The game from here on out is to track where your money goes and see how it lines up with these amounts.

Categorizing Your Common Expenses

Now for the fun part: figuring out where your money is actually going. Grab your recent bank and credit card statements and start sorting every expense into one of the three buckets.

Some things are no-brainers. Rent is a Need. That concert ticket is a Want. But some expenses live in a gray area. That daily latte might feel like a need to get your day started, but it’s really a want. A gym membership could be a want if it’s for leisure, but a need if it’s essential for managing a health condition.

The key is to be brutally honest with yourself. What’s truly necessary for survival versus what just makes life more enjoyable?

This simple hierarchy is what the 20 30 50 rule is all about.

As you can see, Savings sits at the top—securing your future is priority one. Wants come next, representing your lifestyle choices. And Needs form the essential foundation of your entire financial plan.

How This Budget Works in the Real World

Theory is one thing, but a budget’s real test is how it holds up against the chaos of actual life. The 20 30 50 rule isn’t meant to be a rigid cage; think of it more as a flexible guide that can bend and adapt to your financial reality, whether that means a sky-high cost of living, a wildly unpredictable income, or finances spread across the globe.

Let’s see how this adaptability plays out by looking at three totally different, real-world scenarios. We’ll follow a young professional navigating an expensive city, a freelancer with a fluctuating paycheck, and an expat juggling multiple currencies. Each story uses real numbers to show how this simple framework brings clarity and control, no matter what life throws at you.

The Urban Professional in a High-Cost City

First up, meet Alex, a marketing specialist living in a big, expensive city. After taxes, Alex’s take-home pay is $5,000 a month. Applying the 20 30 50 rule, the targets look like this:

- Savings (20%): $1,000

- Wants (30%): $1,500

- Needs (50%): $2,500

Right away, there’s a problem. Alex’s rent alone is a hefty $2,200. Throw in utilities and groceries, and the “Needs” category balloons to $3,000—that’s 60% of take-home pay. This isn’t unusual; countless urbanites find their essential costs easily blowing past that 50% guideline.

Instead of scrapping the whole budget, Alex makes an adjustment. That $500 overage in Needs has to be balanced out, so it comes from the “Wants” category, shrinking it from $1,500 down to $1,000. The most important part? The 20% savings goal of $1,000 stays untouched. This tweak ensures that even in a pricey city, long-term financial goals don’t get sacrificed.

The Freelancer with Irregular Income

Now let’s look at Maya, a freelance graphic designer. Her income is all over the place, but it averages out to around £4,000 a month after she puts money aside for taxes. A fluctuating income can make budgeting feel like trying to nail Jell-O to a wall, but this rule can bring some much-needed order.

Maya’s main challenge is consistency. One month she might pull in £6,000, but the next could be a lean £2,500. To handle this, she bases her budget on her average income, not her best month. When she has a great month and earns an extra £2,000, that money goes straight into a buffer fund. That fund is her safety net, covering expenses—and her savings goals—when work is slow.

This strategy is absolutely vital for gig workers. For example, a freelancer in London might find that housing and other essentials devour their budget. Studies have found that 55% of people in major cities see their needs climb above the 50% mark, mostly because of housing. By cutting back on discretionary spending like daily coffee runs and extra subscriptions, they can protect their savings discipline. For a deeper dive, you can find expert insights on how the 50/30/20 budget works in different scenarios. Building a buffer and being flexible with “wants” is exactly how freelancers can consistently hit that 20% savings target, even when their income is a rollercoaster.

The Expat Juggling Multiple Currencies

Finally, let’s meet Ben. He’s an expat working in Germany but still has financial ties back in the United States. He earns in Euros, pays a student loan in U.S. dollars, and has savings goals in both currencies. This is where a simple percentage-based rule really proves its worth.

The beauty of the 20 30 50 rule is that it’s currency-agnostic. Ben simply applies the percentages to his total after-tax income, converting it all to a single currency just for his planning. This gives him a clear, unified snapshot of his global financial health.

For expats, a unified tracking tool isn’t a luxury—it’s essential. It turns a complex web of international accounts and exchange rates into a simple, actionable financial plan.

By using a platform that can handle multi-currency aggregation, Ben can see exactly how his spending in Euros and dollars stacks up against his budget. He can make sure his 20% savings are correctly split between his German investment account and his U.S. retirement fund, all while keeping his 30% wants and 50% needs in check. It’s a perfect example of how the rule can bring simplicity to even the most complicated financial lives.

Accelerate Your Long-Term Financial Goals

The 20 30 50 rule isn’t just a way to manage your monthly bills; it’s a powerful engine for building serious, long-term wealth. When you consistently set aside 20% of your income for savings and investments, you tap into one of the most incredible forces in finance: compound interest. This is the magic moment where your money starts working for you, earning returns that then go on to earn their own returns.

Think of it like rolling a small snowball down a long, snowy hill. It starts small and grows slowly. But give it enough time, and it starts picking up snow exponentially, eventually becoming an unstoppable force. Your 20% savings bucket is that snowball.

This simple, repeatable habit lays the groundwork for hitting major life goals that go way beyond just retirement. That steady 20% can be put to work in a few different ways:

- Building Home Equity: A chunk can go toward a down payment fund, getting your foot in the property market door much faster.

- Wiping Out Debt: Making extra payments on high-interest debt like credit cards or student loans can save you thousands in interest over the years.

- Investing for the Future: Funneling money into accounts like a 401(k) or IRA puts your cash to work in the market.

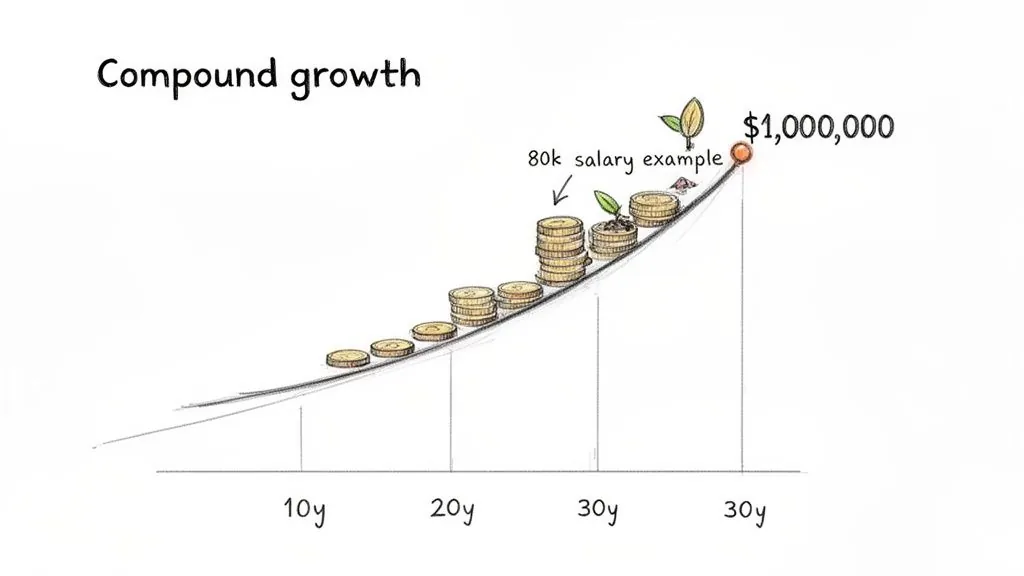

From Consistent Savings to a Million-Dollar Nest Egg

Let’s put some real numbers to this. Imagine someone earning $80,000 a year. After taxes, their monthly take-home pay is about $6,667. Following the 20% rule, their savings goal is $1,334 every single month.

If they consistently invest that amount and earn a pretty average annual return of 7%, they could have over $1.2 million in 30 years. This shows how the disciplined approach of the 20 30 50 rule can turn a regular salary into a massive nest egg. It’s proof that small, steady actions really do lead to incredible long-term results.

Of course, a big part of this is knowing your target. It’s crucial to understand how much you need for retirement so you can set clear goals for what you’re building toward.

The real magic of this rule isn’t just about the percentages. It’s about the consistency and automation it forces you to build. By making saving a non-negotiable first step, you create a wealth-generating habit that works tirelessly for you in the background, locking in your financial future.

Choosing the Right Tools to Track Your Budget

A great financial plan like the 20 30 50 rule is only as good as your ability to stick with it. Let’s be honest, nobody wants to spend hours manually punching numbers into a clunky spreadsheet. That’s where the right tools come in, turning a smart budgeting framework into an easy, automated habit.

The first step is simply seeing where your money is actually going. Guesswork and manual tracking are recipes for frustration and failure. A dedicated platform cuts through the noise and gives you a clear picture of your entire financial world in one place.

See Your Full Financial Picture

To really make the 20 30 50 rule work for you, you need a tool that does more than just list transactions. You’re looking for features that automate the heavy lifting and make staying on track feel effortless.

Here’s what really matters:

- Automated Bank Integrations: Securely link your accounts so your spending and income update in real-time. This is non-negotiable—it kills manual entry and keeps your budget honest.

- Interactive Dashboards: Good tools use charts and visuals to show you exactly where your money is going. You can see instantly if you’re hitting your 20%, 30%, and 50% targets.

- Multi-Currency Support: This is an absolute game-changer for expats and anyone earning or spending in different currencies. It’s the only way to maintain one unified budget.

From Plan to Progress

The right tech takes your budget from an abstract idea and makes it real. The data backs this up: people who follow a structured budget save a lot more than those who don’t. Research shows that Americans using these methods can boost their annual savings by 15-20%, with median savings rates jumping from just 5% to 18%.

This is especially true for expats. Imagine tracking a salary paid in London while managing rent in Berlin—a tool like PopaDex handles that seamlessly in a single dashboard. Smart alerts and clear insights turn abstract percentages into actual progress toward your goals. You can find more details on how budgeting rules can increase your savings on johnhancock.com.

Ultimately, a good tool gives you the clarity and motivation you need to make your budget last. To help you find the right fit, we’ve put together a guide on the best free budgeting apps out there today.

Common Questions About the 20 30 50 Rule

Whenever you try a new budgeting framework, questions are bound to pop up. The 20 30 50 rule is no different. Let’s dig into a few common sticking points people run into when they first put this savings-first method to the test.

What if My Needs Exceed 50 Percent?

This is probably the most common hurdle, especially if you live in a city with a sky-high cost of living. If you find your rent, utilities, and groceries are consistently eating up more than half your income, don’t throw in the towel. The key is to adapt, not abandon.

Your first priority has to be protecting that 20% savings goal. To make the numbers work, you’ll need to borrow from your 30% Wants category. That might mean cutting back on a few dinners out or hitting pause on a streaming service you barely use, but it keeps your financial future front and center.

The goal isn’t to be perfectly rigid; it’s about making conscious trade-offs. The real magic of this rule is its flexibility—it bends to fit your life while keeping your long-term goals locked in.

How Do I Budget for Irregular Income?

Life as a freelancer or gig worker means your income can look like a rollercoaster. The best way to handle this is to build a budget based on your average monthly earnings.

When a great month rolls in, take that extra cash and sweep it into a separate “buffer” or “income stabilization” account. During the leaner months, you can pull from that fund to cover your essentials and—most importantly—still hit your 20% savings target. It’s a simple trick that turns unpredictable income into a steady, reliable flow.

Can I Use This Rule to Pay Off Debt?

Absolutely. In fact, tackling high-interest debt is one of the smartest ways to use your 20% savings bucket. Think about it: paying off a credit card with an 18% APR is like getting an 18% return on your money. You can’t beat that.

Just make sure your minimum payments are covered under your Needs category first. Then, you can funnel the rest (or all) of that 20% toward making extra debt payments. This approach transforms the 20 30 50 rule into a powerful machine for getting you to debt-free status faster.

Ready to stop guessing and start tracking? With PopaDex, you can see your entire financial world in one place, making it easy to implement the 20 30 50 rule and watch your net worth grow. Get your complete financial picture at https://popadex.com.