Our Marketing Team at PopaDex

10 Actionable 401k Investment Strategies to Build Wealth in 2026

Your 401(k) is a powerful wealth-building engine for your future. However, simply contributing is not enough to secure the retirement you envision. The difference between a comfortable financial future and just getting by often lies in the specific 401k investment strategies you implement. Many investors fall into one of two traps: they either ‘set and forget’ their contributions into default funds without a clear plan, or they make reactive, emotional decisions based on short-term market noise. Both approaches can significantly hinder long-term growth and undermine your retirement goals.

This guide moves beyond generic advice to provide a curated roundup of 10 distinct, actionable strategies. Each one is designed for different financial goals, risk tolerances, and desired levels of hands-on involvement. Whether you are a hands-off investor seeking the elegant simplicity of a Target-Date Fund or a seasoned DIYer looking for advanced tax optimization through a Roth Conversion Ladder, you will find a practical, step-by-step framework here.

We will explore each strategy in detail, covering its core principles, the ideal investor it suits, and concrete implementation steps. You will also find sample portfolio allocations and learn how to monitor your progress effectively using modern financial tools like the PopaDex net worth tracker. It is time to transform your 401(k) from a passive account into an actively managed asset that works intelligently to build the retirement you deserve.

1. Target-Date Funds (Lifecycle Investing)

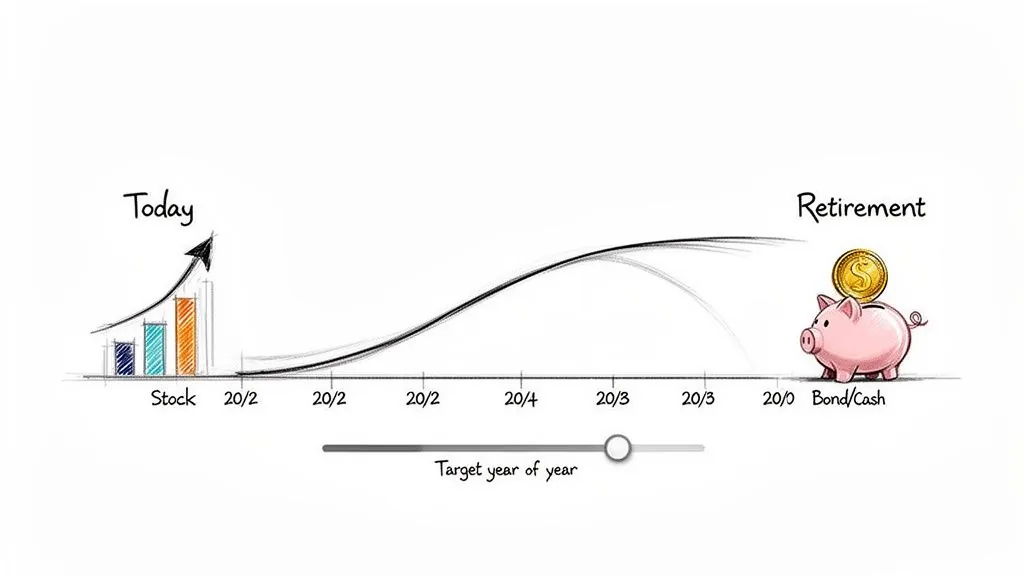

Among the most popular 401k investment strategies, target-date funds (TDFs) offer a simplified, hands-off approach to long-term saving. These funds, also known as lifecycle funds, are essentially a diversified portfolio-in-a-box designed to automatically adjust their asset allocation over time. When you are far from retirement, the fund holds a higher percentage of stocks for aggressive growth. As your target retirement year approaches, it gradually and automatically shifts toward more conservative assets like bonds and cash equivalents to preserve capital.

This automated rebalancing, or “glide path,” is the key benefit. It removes the need for you to manually buy and sell assets to maintain a desired risk level, making it an excellent choice for investors who prefer a “set it and forget it” strategy.

Who It’s For

This strategy is ideal for investors who:

- Want a simple, all-in-one investment solution.

- Are uncomfortable making complex asset allocation decisions.

- Lack the time or desire to actively manage their 401k portfolio.

How to Implement This Strategy

- Identify Your Target Year: Locate the fund in your 401k plan options with the year closest to when you plan to retire (e.g., “Target 2055 Fund” if you expect to retire around 2055).

- Allocate 100%: For this strategy to work as designed, you should typically allocate 100% of your 401k contributions to a single target-date fund. Owning multiple TDFs or mixing one with other funds can disrupt its intended asset allocation.

- Review Periodically: While the fund manages itself, check in every few years to ensure the fund’s risk profile still aligns with your goals.

- Track Your Progress: Use a tool like the PopaDex net worth tracker to monitor how your 401k balance contributes to your overall financial picture. This gives you a holistic view beyond just the single fund’s performance.

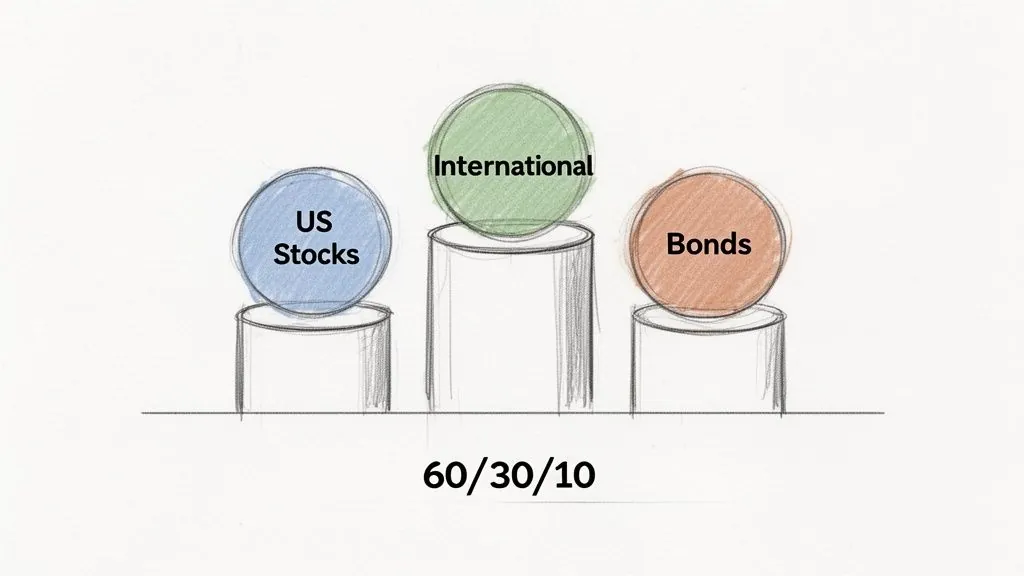

2. Three-Fund Portfolio Strategy

Popularized by the Bogleheads investment philosophy, the three-fund portfolio is one of the most elegant and effective 401k investment strategies available. It simplifies diversification by using just three low-cost, broad-market index funds: a total U.S. stock market fund, a total international stock market fund, and a total U.S. bond market fund. This approach provides comprehensive global market exposure while minimizing the complexity and high fees often associated with actively managed funds.

The core principle is to capture the returns of the entire market, rather than trying to beat it. By holding a mix of U.S. stocks, international stocks, and bonds, you create a balanced portfolio that can weather various economic conditions. It’s a disciplined, low-maintenance strategy that gives you more control than a target-date fund but remains incredibly straightforward.

Who It’s For

This strategy is ideal for investors who:

- Are cost-conscious and want to minimize investment fees.

- Prefer a hands-on approach that is still simple to manage.

- Believe in passive, index-based investing over active stock picking.

How to Implement This Strategy

- Select Your Funds: Identify three broad-market index funds in your 401k plan. Look for options like a “Total Stock Market Index,” “Total International Stock Index,” and a “U.S. Aggregate Bond Index.”

- Determine Your Allocation: A common starting point for a moderate-risk investor is a 60% U.S. stock, 30% international stock, and 10% bond allocation. You can adjust this mix based on your age and risk tolerance, increasing your bond percentage as you near retirement.

- Rebalance Periodically: Once a year, or when your allocations drift more than 5% from their targets, sell portions of the overperforming assets and buy more of the underperforming ones to return to your desired mix.

- Track Your Portfolio: Use the PopaDex net worth tracker to monitor your 401k balance and see how your three-fund portfolio fits within your total financial picture. This helps you maintain your target asset allocation across all your accounts, not just your 401k.

3. Dollar-Cost Averaging (DCA)

Dollar-cost averaging is less of a fund choice and more of a disciplined, automatic investing habit. This powerful 401k investment strategy involves contributing a fixed dollar amount to your account at regular intervals, typically with each paycheck. By investing consistently regardless of market fluctuations, you automatically buy more shares when prices are low and fewer shares when prices are high, which can lower your average cost per share over time.

This systematic approach removes emotion from the investment process. Instead of trying to time the market, a notoriously difficult feat, you commit to a long-term plan. This consistency is the cornerstone of building substantial retirement wealth through your 401k.

Who It’s For

This strategy is fundamental for nearly every 401k participant, especially those who:

- Are building their retirement savings over a long period.

- Want to mitigate the risks of market volatility.

- Prefer an automated, disciplined approach to investing.

- Are prone to making emotional decisions based on market news.

How to Implement This Strategy

- Set Up Automatic Contributions: The easiest way to implement DCA is through your employer’s payroll deductions. Determine the percentage or dollar amount you want to contribute each pay period and set it up with your HR or benefits department.

- Maximize Your Employer Match: Ensure your contribution rate is high enough to receive the full employer match. This is free money and one of the best returns you can get on your investment.

- Stay Consistent: The key to DCA is consistency. Resist the urge to pause your contributions during a market downturn; these are the times your fixed dollar amount buys more shares, potentially leading to greater long-term gains.

- Monitor and Increase: Use a tool like the PopaDex disposable income calculator to find your optimal contribution rate. Track your contributions and overall investment growth within the platform. Make it a habit to increase your contribution percentage each time you get a raise to accelerate your savings.

4. Risk-Based Asset Allocation

Moving beyond age-based formulas, a risk-based asset allocation strategy tailors your 401k portfolio directly to your personal risk tolerance, financial situation, and long-term goals. This approach acknowledges that two investors of the same age can have vastly different comfort levels with market volatility and different capacities for financial risk. Instead of relying on a pre-set glide path, you build a custom mix of stocks, bonds, and other assets that aligns with your unique profile.

For example, a conservative 35-year-old with low job security might choose a 50% stock and 50% bond portfolio. In contrast, an aggressive 55-year-old with a large nest egg and high-risk tolerance might opt for an 85% stock allocation to maximize growth. This personalized method is a cornerstone of modern 401k investment strategies, empowering you to take control based on what you can emotionally and financially handle.

Who It’s For

This strategy is ideal for investors who:

- Have a clear understanding of their personal risk tolerance.

- Want more control over their portfolio than a target-date fund offers.

- Are willing to periodically review and rebalance their investments.

How to Implement This Strategy

- Assess Your Risk Profile: Honestly complete a risk tolerance questionnaire, often provided by your 401k administrator. Consider factors like your job stability, other assets, and how you would react to a significant market downturn.

- Build Your Allocation: Based on your assessment (e.g., conservative, moderate, aggressive), select a mix of stock and bond index funds to match your target percentages. For instance, a moderate portfolio might be 70% in a total stock market index fund and 30% in a total bond market index fund.

- Review and Rebalance Annually: At least once a year, or after major life events like a promotion or change in family status, review your allocation. Sell assets that have grown disproportionately and buy those that have shrunk to return to your original target percentages.

- Gain a Holistic View: Use the PopaDex net worth tracker to see how your 401k’s risk-based allocation fits within your entire financial picture, including savings, real estate, and other investments. This context is crucial for making informed allocation decisions.

5. Employer Match Maximization Strategy

Perhaps the most fundamental of all 401k investment strategies, maximizing your employer match is the closest thing to a “free lunch” in investing. This approach prioritizes contributing enough to your 401k to capture the full matching contribution from your employer. This match is an immediate, guaranteed return on your investment, often 50% or 100%, which is an unparalleled growth opportunity you won’t find anywhere else.

Failing to contribute enough to get the full match is like turning down a portion of your salary. For example, if your employer matches 100% of your contributions up to 4% of your salary, contributing that 4% instantly doubles your money. This powerful boost significantly accelerates your retirement savings, making it a non-negotiable first step before considering other investment avenues.

Who It’s For

This strategy is essential for every employee who:

- Has access to a 401k plan with an employer match.

- Wants to accelerate their retirement savings with guaranteed returns.

- Is building a foundational financial plan.

How to Implement This Strategy

- Understand Your Match Formula: Start by thoroughly evaluating your total compensation package to understand all benefits offered, specifically your 401k match. Common formulas include a 100% match up to 3% of your salary or a 50% match on contributions up to 6% of your salary.

- Calculate Your Contribution: Determine the exact percentage of your pre-tax salary you need to contribute per paycheck to receive the full match.

- Set Your Payroll Deduction: Log into your 401k provider’s portal or contact your HR department to set your contribution rate to at least the minimum required for the full match. Prioritize this before any other investment.

- Monitor Your Vesting Schedule: Be aware of your company’s vesting schedule, which dictates when you gain full ownership of the matched funds. Many companies use a “cliff” (e.g., 100% ownership after 3 years) or “graded” schedule (e.g., 20% ownership per year).

- Track Your Progress: Use a tool like the PopaDex dashboard to see how your consistent contributions and the employer match are accelerating your 401k balance and boosting your overall net worth. Understanding the pros and cons of a 401k is crucial, and the employer match is one of its biggest advantages.

6. Roth Conversion Ladder Strategy

The Roth Conversion Ladder is an advanced tax-planning technique used to access retirement funds early without penalty and create a source of tax-free income in retirement. It involves systematically converting pre-tax money from a traditional 401k or IRA into a Roth IRA over several years. You pay income tax on the converted amount in the year of the conversion, but after a five-year waiting period for each conversion, the principal and all its future earnings can be withdrawn tax-free.

This strategy is particularly powerful for those planning an early retirement or expecting to be in a higher tax bracket in the future. By strategically converting funds during low-income years, such as a sabbatical or the gap between retiring and taking Social Security, you can minimize the tax impact. For example, a mid-career professional might convert $20,000 annually, paying taxes at their current rate to build a future tax-free withdrawal pipeline.

Popularized within the Financial Independence, Retire Early (FIRE) community, this is one of the more complex 401k investment strategies that requires careful planning to execute effectively.

Who It’s For

This strategy is ideal for investors who:

- Plan to retire before age 59½ and need access to their funds.

- Expect their income tax rate to be higher in retirement.

- Have low-income years where they can convert funds at a lower tax rate.

- Have cash outside of their retirement accounts to pay the conversion taxes.

How to Implement This Strategy

- Initiate a Rollover: First, you typically need to roll over funds from your traditional 401k to a traditional IRA. This step gives you the flexibility to perform conversions.

- Convert in Chunks: Decide how much to convert to a Roth IRA each year. Spread conversions over multiple years to avoid being pushed into a higher tax bracket.

- Pay the Taxes: You must pay income tax on the converted amount for the year the conversion occurs. Use non-retirement funds for this to avoid penalties and taxes on the money used.

- Wait Five Years: Each conversion amount has its own five-year clock. After five years, that specific converted amount can be withdrawn tax-free and penalty-free, regardless of your age.

- Track Your Ladder: Use your PopaDex dashboard to monitor the growth of your Roth IRA and see how these tax-advantaged funds impact your total net worth. This helps visualize the long-term benefit of your conversion strategy.

- Consult a Professional: Given the complexity and tax implications, work with a financial advisor or tax professional to optimize your conversion amounts and timing. When evaluating strategies like this, it’s beneficial to understand how tax benefits in diverse investment scenarios can apply across different asset classes.

7. Dividend Growth and Income Strategy

The dividend growth and income strategy focuses on building a portfolio of stocks that not only pay dividends but consistently increase those payouts over time. Instead of relying solely on stock price appreciation, this approach generates a growing stream of cash flow that can be reinvested to fuel compounding or eventually supplement your retirement income. The core idea is that companies with a long history of raising dividends are often financially stable and well-managed.

This method shifts the focus from short-term market fluctuations to the long-term health and cash-generating power of the underlying businesses. By reinvesting dividends, you purchase more shares, which in turn generate more dividends, creating a powerful compounding effect that can significantly boost your 401k’s growth potential. It’s a conservative-growth strategy that emphasizes quality and sustainability.

Who It’s For

This strategy is a great fit for investors who:

- Are looking for both capital appreciation and a steady, growing income stream.

- Prefer investing in established, financially sound companies.

- Have a long-term horizon and can patiently let dividends compound.

- Want to build a portfolio that can provide reliable income in retirement.

How to Implement This Strategy

- Identify Dividend-Focused Funds: Look for mutual funds or ETFs in your 401k plan with names like “Dividend Growth,” “Dividend Appreciation,” or “Equity Income.” Examples include funds that track indices similar to the Vanguard Dividend Appreciation ETF (VIG) or the Schwab U.S. Dividend Equity ETF (SCHD).

- Allocate a Portion of Your Portfolio: You can dedicate a specific percentage of your 401k to this strategy, such as 20-40%, while balancing the rest with other growth or index funds. A full 100% allocation might be too conservative for younger investors.

- Ensure Dividends Are Reinvested: This is the most crucial step. Check your 401k plan settings to confirm that all dividends are automatically reinvested. This puts the power of compounding to work for you.

- Monitor Dividend Health: Use a tool like the PopaDex net worth tracker to monitor your 401k balance and, where possible, track the income generated. Periodically review your chosen funds to ensure their dividend growth remains consistent and their payout ratios are sustainable.

8. International Diversification Strategy

While U.S. markets are robust, limiting your investments solely to domestic companies creates “home-country bias,” potentially missing out on global growth opportunities. The International Diversification Strategy involves deliberately allocating a significant portion of your equity portfolio, typically 20-40%, to stocks outside the United States. This includes both developed markets (like Europe and Japan) and emerging markets (like China and Brazil), capturing a wider economic landscape.

This approach is rooted in modern portfolio theory, which suggests that holding assets with different return patterns can reduce overall portfolio volatility. Since international and U.S. markets don’t always move in perfect sync, one can provide a buffer when the other is underperforming. It’s a key component of many well-regarded 401k investment strategies, including the Bogleheads’ three-fund portfolio.

Who It’s For

This strategy is ideal for investors who:

- Believe that global economic growth will not be limited to the U.S. alone.

- Want to reduce portfolio volatility by avoiding over-concentration in a single country’s market.

- Have a long-term investment horizon and can tolerate the unique risks of international investing, including currency fluctuations.

How to Implement This Strategy

- Determine Your Allocation: Decide on a target percentage for international stocks. A common starting point is a 70% U.S. / 30% international split for your equity holdings. For example, if your total 401k is 90% stocks, you would aim for 63% U.S. stocks and 27% international stocks.

- Select Low-Cost Funds: Look for broad international index funds in your 401k plan, such as a “Total International Stock Index Fund” (similar to VTIAX) or a “Developed Markets Index Fund.” Aim for funds with low expense ratios, ideally below 0.25%.

- Consider Emerging Markets: For more aggressive growth potential, you could add a small, separate allocation (e.g., 5-10% of your total portfolio) to an emerging markets fund if one is available.

- Rebalance Annually: At least once a year, review your portfolio to ensure your international allocation hasn’t drifted too far from your target. Sell some of the outperforming asset and buy the underperformer to get back in line. Learn more about how to diversify an investment portfolio effectively.

- Monitor Your Global Picture: Use a tool like PopaDex to track your total portfolio’s asset allocation. This is especially useful for seeing how your international 401k holdings fit with any international investments you might have in other brokerage accounts.

9. Self-Directed Brokerage Account Strategy (SDBA)

For the investor seeking ultimate control and a universe of options beyond the standard 401k menu, the Self-Directed Brokerage Account (SDBA) offers an advanced path. Often called a “brokerage window,” an SDBA is a feature offered by some 401k plans that lets you open a brokerage account within your retirement plan. This unlocks access to a vast array of individual stocks, bonds, ETFs, and other securities not available through your plan’s core fund lineup.

This strategy essentially turns a portion of your 401k into a standard brokerage account, giving you the freedom to execute specific 401k investment strategies like buying individual dividend stocks or investing in niche sector ETFs. It provides maximum flexibility but also demands significant investment knowledge, research, and active management, as you become your own fund manager.

Who It’s For

This strategy is ideal for investors who:

- Are experienced, confident, and have a deep understanding of security analysis.

- Want to invest in specific companies or assets not offered in the main 401k plan.

- Are willing to dedicate significant time to researching and managing individual investments.

- Understand and accept the higher risks associated with individual stock picking.

How to Implement This Strategy

- Confirm Availability: First, check with your 401k plan administrator to see if an SDBA option is available. Not all plans offer this feature.

- Open the Account: Follow your plan’s procedures to open the SDBA. This usually involves completing an application and transferring a portion of your 401k funds into the new brokerage account.

- Define Your Allocation: Use the SDBA for a smaller, “satellite” portion of your portfolio (e.g., 5-15%). Keep the majority of your assets in a diversified core holding, like a target-date fund or broad-market index fund, to maintain a stable foundation.

- Research and Invest: Conduct thorough due diligence on any individual stock, bond, or ETF before purchasing. Avoid over-concentrating in a single company (especially your employer’s stock) or sector.

- Monitor and Manage: Track not only the performance but also the trading fees and any account maintenance costs, as these can impact your net returns. Use the PopaDex net worth tracker to get a granular view of your SDBA holdings alongside your core 401k funds, ensuring your overall asset allocation remains aligned with your retirement goals.

10. Catch-Up Contributions and Accelerated Savings Strategy

For investors over age 50, one of the most powerful 401k investment strategies involves leveraging IRS provisions for catch-up contributions. This strategy allows you to contribute significantly more to your 401k than the standard annual limit, providing a powerful, tax-advantaged method to accelerate your savings in the final years before retirement. It’s an essential tool for those who may have started saving late, experienced a career interruption, or simply want to supercharge their nest egg.

This approach isn’t just about saving more; it’s about making those final working years count disproportionately toward your retirement goals. For example, in 2024, an eligible individual could contribute the standard $23,000 plus an additional $7,500 catch-up contribution, for a total of $30,500. This dramatic increase can substantially boost your portfolio’s growth potential right before you need to start drawing from it.

Who It’s For

This strategy is ideal for investors who:

- Are age 50 or older and still working.

- Feel they are behind on their retirement savings goals.

- Have increased disposable income later in their careers (e.g., kids have moved out, mortgage is paid off).

- Want to maximize their tax-deferred or tax-free growth in their final working years.

How to Implement This Strategy

- Confirm Eligibility: You must be turning 50 or older during the calendar year to be eligible. Verify that your specific 401k plan permits catch-up contributions (most do).

- Calculate Your New Contribution: Determine the maximum amount you can afford to contribute. Work with your payroll or HR department to increase your deferral percentage to include the additional catch-up amount.

- Automate the Increase: Adjust your payroll deductions to reflect the higher contribution rate. The best approach is to “set it and forget it,” ensuring you consistently contribute the maximum you can.

- Model the Impact: Use the PopaDex net worth tracker to project how these accelerated savings will impact your retirement date and overall portfolio value. This helps you visualize the benefit and confirm if you are on track to close any retirement savings gap. You can learn more about how to catch up on retirement savings to refine your plan.

401(k) Investment Strategies: 10-Point Comparison

| Strategy | Implementation Complexity | Resource Requirements | Expected Effectiveness | Expected Outcomes | Best for / Key advantage |

|---|---|---|---|---|---|

| Target-Date Funds (Lifecycle Investing) | Very low — set‑and‑forget single fund | Minimal — one fund, low fees, no active management | — strong for typical retirement timelines | Gradual de‑risking, diversified returns, lower volatility near retirement | Hands‑off investors; automatic glidepath simplifies planning |

| Three‑Fund Portfolio Strategy | Low to moderate — needs initial allocation decision | Low — low‑cost index funds, annual rebalancing | — cost‑efficient broad market exposure | Market returns with high diversification and low fees | DIY, cost‑conscious savers seeking simple diversification |

| Dollar‑Cost Averaging (DCA) | Very low — automated contributions | Low — regular payroll deductions, discipline required | — good behavioral tool, not optimal for lump sums | Smoother purchase price, reduced timing risk, steady accumulation | Consistent savers and those avoiding market‑timing stress |

| Risk‑Based Asset Allocation | Moderate — requires risk assessment & periodic reviews | Moderate — questionnaires, possible advisor, rebalancing | — personalized fit improves adherence | Tailored risk/return profile; potentially better long‑term alignment | Investors with distinct risk preferences or complex finances |

| Employer Match Maximization Strategy | Very low — adjust contributions to capture match | Low income impact if planned; must meet contribution minimums | — immediate, guaranteed return (often best ROI) | Immediate boost to savings; accelerates retirement accumulation | All 401(k) participants; priority strategy for guaranteed return |

| Roth Conversion Ladder Strategy | High — multi‑year tax planning and coordination | High — liquidity to pay taxes, tax advisor recommended | — strong long‑term tax benefits if executed properly | Tax‑free growth/withdrawals, RMD avoidance, variable short‑term tax cost | High‑income, early retirees, those expecting higher future taxes |

| Dividend Growth and Income Strategy | Moderate — selection/monitoring of dividend payers | Moderate — research, dividend ETFs/stocks, reinvestment | — stable income focus, may limit growth potential | Growing income stream, lower volatility, possibly lower total returns | Pre‑retirees and income‑focused investors seeking stability |

| International Diversification Strategy | Low to moderate — decide allocation to foreign markets | Low — international funds/ETFs; consider currency/expense ratios | — improves diversification over long horizon | Reduced home‑country bias, potential for uncorrelated returns, added volatility | Globally‑minded investors wanting true market diversification |

| Self‑Directed Brokerage Account (SDBA) | High — active management and security selection | High — time, expertise, potentially higher fees | — potential for outperformance but higher risk | Greater control and concentrated returns or losses; higher monitoring | Experienced investors seeking control and bespoke strategies |

| Catch‑Up Contributions & Accelerated Savings | Low — increase payroll allocations; planning required | High — requires sufficient income and budget adjustments | — very effective at boosting final balance late‑career | Significant near‑term balance increase; tax‑advantaged growth | Age 50+, late starters, high earners wanting to close retirement gaps |

From Strategy to Action: Building Your Confident Financial Future

Navigating the landscape of 401(k) investment strategies can feel complex, but the journey to a secure retirement is built on a series of deliberate, informed decisions. Throughout this guide, we’ve dissected a diverse toolkit of approaches, moving from foundational concepts to advanced tactics. The central theme is clear: there is no one-size-fits-all solution, only the strategy that perfectly fits you.

The most sophisticated financial plan is useless until it is put into action. Your primary takeaway should be the empowerment that comes from understanding your options. Whether you’re setting up a simple and effective Three-Fund Portfolio or maximizing your employer match, the power lies in choosing a path and committing to it with discipline.

Recapping Your Strategic Options

We’ve explored a wide array of powerful 401k investment strategies, each designed for different goals, risk appetites, and life stages.

- For the Hands-Off Investor: Strategies like Target-Date Funds and the classic Three-Fund Portfolio offer simplicity, low costs, and built-in diversification, making them ideal for those who prefer a set-it-and-forget-it approach.

- For the Active Accumulator: Dollar-Cost Averaging provides a disciplined framework for investing consistently through market cycles, while Employer Match Maximization is the single most effective way to accelerate your savings with “free” money.

- For the Advanced Planner: Techniques like the Roth Conversion Ladder and leveraging a Self-Directed Brokerage Account (SDBA) offer greater control over your tax future and investment choices, suiting those who want to actively manage their financial destiny.

Remember, the goal isn’t to master every strategy at once. It’s about identifying the one or two that align most closely with your current financial situation and long-term vision.

From Plan to Progress: Your Actionable Next Steps

Knowledge is the starting point, but execution is what builds wealth. The difference between a comfortable retirement and a stressful one often comes down to consistent action and periodic review. Your 401(k) is not a static account; it’s a dynamic tool that requires your attention as your life evolves. A promotion, a new family member, or a change in your financial goals are all signals that it might be time to revisit your chosen strategy.

The most critical step you can take today is to transform passive learning into active management. Don’t let analysis paralysis stop you from making a decision. Choose the strategy that resonates most with you, log into your 401(k) provider’s portal, and implement the necessary changes. Adjust your contribution percentage, rebalance your portfolio, or explore the fund options available to you.

Key Insight: A good plan executed today is far better than a perfect plan implemented tomorrow. Your future self is counting on the decisive actions you take right now.

Ultimately, mastering your 401k investment strategies is about more than just numbers on a screen. It’s about building a life of financial freedom, security, and choice. It’s about having the resources to travel, pursue passions, and support loved ones without financial worry. By taking control of your 401(k), you are laying the foundation for that future, one contribution and one strategic decision at a time. This is your roadmap; the destination is a retirement lived on your own terms.

Ready to stop guessing and start seeing the complete picture of your financial health? PopaDex connects all your accounts, including your 401(k), to provide a real-time, holistic view of your net worth, helping you track your progress and make smarter investment decisions. Sign up for free at PopaDex and take confident control of your financial journey today.