Our Marketing Team at PopaDex

Actively Managed Funds vs Index Funds A Definitive Comparison

When it comes to investing, one of the first big questions you’ll face is whether to go with an actively managed fund or an index fund. The difference is pretty straightforward: active funds have a manager trying to beat the market, while index funds simply aim to match the market by tracking a benchmark like the S&P 500.

While the promise of a brilliant fund manager outsmarting everyone else sounds tempting, history tells a different story. For most people investing for the long haul, low-cost index funds have consistently come out on top.

The Core Investment Decision: Actively Managed vs. Index Funds

Deciding between an active or passive strategy is a huge fork in the road for any investor. This single choice will have a direct ripple effect on your long-term returns, the fees you pay every year, and how complicated your portfolio becomes. Getting a handle on how each one works is the first real step toward building a solid financial future.

Defining the Two Philosophies

At its core, this isn’t just about different products; it’s about two completely opposite beliefs about how the market works. One philosophy bets that skilled professionals can spot opportunities and inefficiencies to deliver above-average returns. The other argues that the market is mostly efficient, making it almost impossible to consistently outperform, especially after you factor in the higher fees active managers charge.

Let’s break down what that means in practice:

- Actively Managed Funds: Here, a fund manager—or a whole team of analysts—is making daily calls on what to buy, hold, or sell. Their entire job is to beat a specific benchmark, like the S&P 500. This approach leans heavily on deep research, economic forecasting, and expert judgment.

- Index (Passive) Funds: These funds are built to be simple copies. They just buy and hold all (or a representative slice) of the stocks or bonds in a specific market index. There are no gut calls or attempts to pick winners; the only goal is to mirror the index’s performance as closely as possible.

If you’re new to the world of passive investing, our guide on understanding index funds is a great place to start. It breaks down the fundamentals in a way that’s easy to digest.

An index fund basically guarantees you’ll get the market’s return. Matching the market is the easy part. Beating the market, on the other hand, is incredibly tough—and the data shows most who try ultimately fail, especially over longer time horizons.

The fallout from this choice is massive. It dictates everything from your annual fees and tax bill to how much time you’ll spend worrying about your portfolio. Using a tool like PopaDex to track your investments can make these differences crystal clear, showing you exactly how much fees and performance are impacting your net worth over time.

Active vs. Index Funds: Key Differences at a Glance

Before we dive deeper, this table gives you a quick snapshot of the core differences. It’s a handy reference for understanding the fundamental trade-offs you’re making with each choice.

| Characteristic | Actively Managed Funds | Index Funds |

|---|---|---|

| Goal | To beat a market benchmark (e.g., S&P 500) | To match a market benchmark’s performance |

| Management | Hands-on decisions by a portfolio manager | Automated, rules-based portfolio construction |

| Cost | Higher expense ratios (0.50% - 1.50%+) | Lower expense ratios (0.03% - 0.20%) |

| Turnover | High; frequent buying and selling of assets | Low; assets are only bought or sold when the index changes |

| Tax Efficiency | Generally less tax-efficient due to capital gains | Highly tax-efficient due to low turnover |

| Risk | Market risk plus “manager risk” (poor decisions) | Only systematic market risk |

As you can see, the higher costs and risks of active management are supposed to be justified by the potential for higher returns. But as we’ll explore, that potential rarely becomes a reality for most investors.

Historical Performance and The Challenge of Outperformance

When it comes to actively managed funds versus index funds, the whole debate really hangs on one question: Is paying a pro to manage your money actually worth it? For years, this was just talk. Now, we have decades of hard data, and the answer is surprisingly clear.

The big selling point for active funds is the promise of outperformance. The idea is that a smart manager can pick winning stocks, dodge market dips, and deliver returns that beat the market average, a concept known as “alpha.” It sounds great in theory. The data, however, tells a very different story.

The Verdict from SPIVA Scorecards

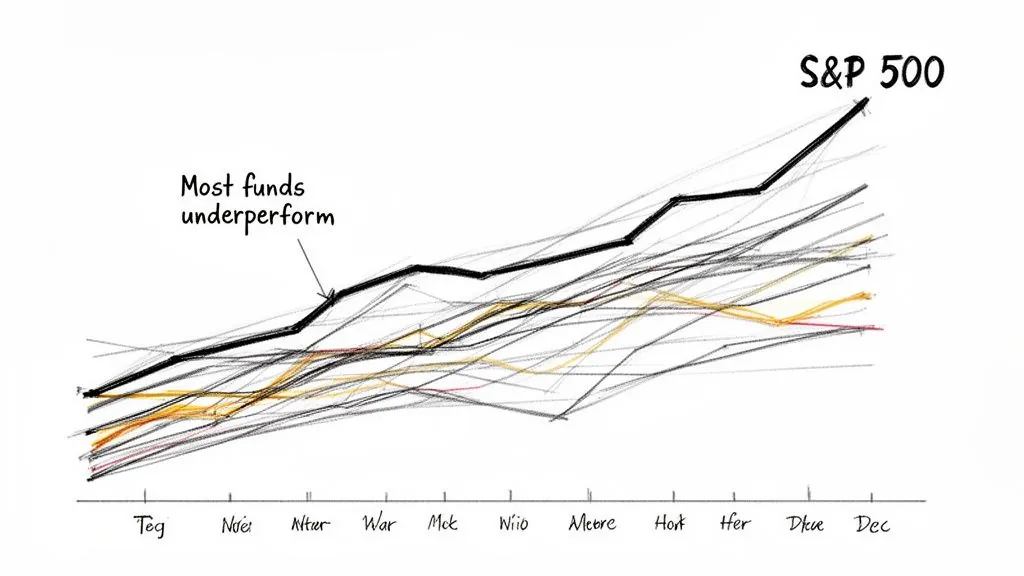

The most convincing proof comes from the S&P Dow Jones SPIVA (S&P Indices Versus Active) scorecards. Think of these reports as the official record-keeper in the active vs. passive fight for over 20 years. They don’t mess around, just straight-up performance comparisons.

Time and again, the SPIVA data shows that most active managers fail to beat their benchmarks over the long haul, especially after their fees are taken out. For instance, looking back over a 20-year period, a staggering 65% of all large-cap U.S. equity funds couldn’t keep up with their benchmarks. And the longer you look, the worse the numbers get for the active crowd.

This isn’t a new trend. Even when markets get wild—times you’d think a skilled stock-picker would shine—the results are the same. In one recent volatile year, about 65% of actively managed large-cap U.S. equity funds still trailed the S&P 500.

After 15 years, SPIVA found no major category where most active managers beat their index, whether in the U.S. or internationally. This is the crux of the issue—it’s incredibly tough to stay ahead of the market consistently, year after year.

This track record makes you question the entire premise of paying higher fees for active management. If the odds are stacked against you, choosing an active fund is essentially a bet that you can find the one manager who defies those odds. That’s a tall order, even for the pros.

Introducing Manager Risk

This brings up a hidden danger many investors miss: manager risk. This is the risk that the specific manager you’ve picked makes bad calls, underperforms other managers, or just decides to retire, leaving you scrambling to find the next supposed genius.

Manager risk adds a layer of unpredictability that simply doesn’t exist with index funds. An index fund is designed to eliminate that variable completely. You’re guaranteed to get the market’s return, minus a tiny fee. You’ll never beat the market, sure, but more importantly, you’ll never get crushed because of one person’s bad strategy.

For anyone investing for the long term, that reliability is huge. The goal for most of us isn’t to hit a home run; it’s to steadily grow our money over time. To get a better sense of what those returns look like, you can learn more about the average rate of return in the stock market in our guide.

Why Outperformance Is So Difficult

It turns out there are a few built-in reasons why it’s so hard for active managers to consistently win:

- Fees: Active funds charge more to cover salaries, research, and marketing. That fee creates a handicap from day one. The manager has to beat the market by at least the amount of their fee just to tie with a cheap index fund.

- Competition: Every fund manager is competing against millions of other brilliant, well-informed investors all trying to do the same thing. This collective brainpower makes markets very efficient, meaning it’s incredibly rare to find a stock that’s a true, undiscovered bargain.

- The Zero-Sum Game: Before you account for costs, active investing is a zero-sum game. For every winner, there has to be a loser. But once you factor in the higher fees, it becomes a loser’s game—the average dollar managed actively must underperform the average dollar managed passively.

If you’re using a tool like PopaDex to track your portfolio, the takeaway from all this data is crystal clear. By comparing your investments to their benchmarks, you can see for yourself if those extra fees are actually buying you better performance or just eating into your returns. The evidence strongly suggests that for most people, the simplest path—owning the whole market through a low-cost index fund—is the most reliable way to build wealth.

Analyzing The True Cost of Investment Fees

While performance charts tell one side of the story, the real engine behind the long-term success of index funds is something far less exciting but infinitely more powerful: fees. Investment costs are one of the few things you have complete control over, and their impact on your portfolio’s growth over time is staggering.

Even tiny fee differences act like a constant drag on your returns, compounding against you, year after year.

The cost gap between active and index funds isn’t a small detail—it’s baked into their DNA. Active funds have to charge more to cover their overhead: large research teams, portfolio manager salaries, and frequent trading commissions. Index funds, on the other hand, just mirror a benchmark, allowing them to run a lean operation with dramatically lower costs.

Deconstructing the Expense Ratio

The most obvious cost is the expense ratio, an annual fee that’s taken as a percentage of your investment. It might seem like just a fraction of a percent, but the difference between fund types is a chasm.

This is a huge reason for the performance gap in the actively managed funds vs index debate. Recent data shows the average expense ratio for U.S. index equity mutual funds is about 0.05%, while actively managed equity mutual funds average around 0.64%. That’s more than 10 times higher.

Many active funds still charge investors around 1% annually, while you can find passive options for well under 0.10%. You can dig into more industry fee data on MoneyGuy.com to see the full picture.

To really get a handle on these numbers, check out our guide on what the expense ratio is and how it affects your investments.

The Long-Term Erosion from High Fees

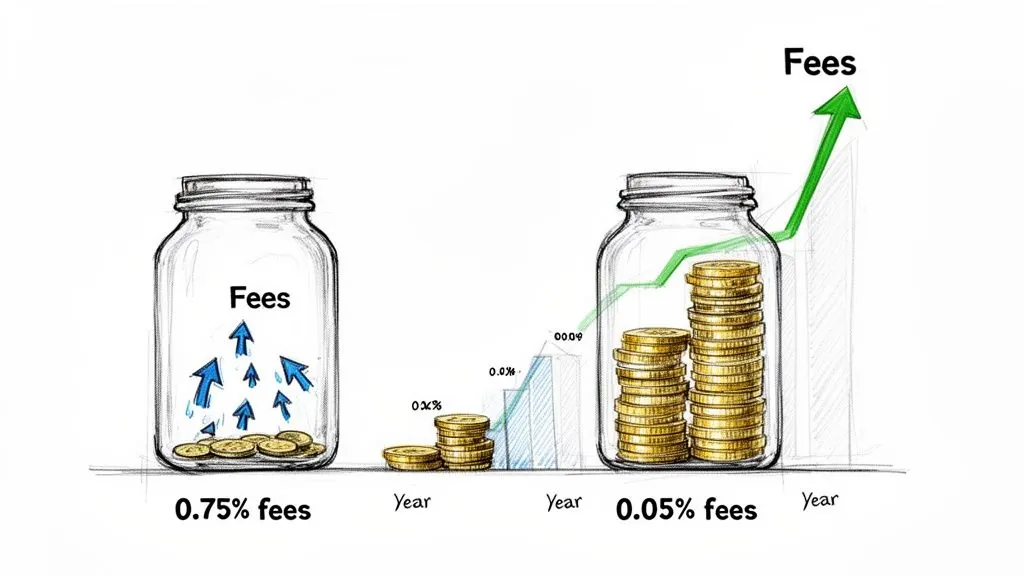

The corrosive power of high fees becomes undeniable over an investing lifetime. Let’s look at two investors, both starting with $100,000 and earning an average of 7% per year before fees over 30 years.

- Investor A (Index Fund): Pays a tiny 0.05% expense ratio. Their portfolio grows to about $750,295.

- Investor B (Active Fund): Pays a 0.75% expense ratio. Their portfolio only grows to around $611,617.

That seemingly small 0.70% difference in fees means Investor B ends up with nearly $139,000 less than Investor A after three decades. That extra money didn’t buy better performance; it just evaporated.

And this example only covers the expense ratio. The total cost of active management is often even higher once you account for the less obvious expenses.

Uncovering the Hidden Costs

Beyond the expense ratio, actively managed funds have other costs that quietly eat away at your returns. These “hidden” fees are a direct result of the high-turnover strategy that defines active management.

- Trading Costs: Active managers are constantly buying and selling. Every trade racks up costs like commissions and bid-ask spreads. These aren’t listed in the expense ratio, but they come directly out of the fund’s assets, reducing your return.

- Tax Inefficiency: All that buying and selling can trigger frequent capital gains distributions. If you hold these funds in a regular taxable brokerage account, you could be hit with a tax bill every year—something that rarely happens with low-turnover index funds.

When you connect all your accounts to a portfolio tracker like PopaDex, these fee differences become painfully clear. If a $200,000 portfolio is paying an extra 0.7% per year in active fund fees, that’s $1,400 annually that isn’t working for you. Seeing this drag across your entire financial picture makes one thing obvious: minimizing costs is one of the surest paths to maximizing wealth.

Risk, Turnover, and the Hidden Tax Bite

It’s easy to get lost in performance charts and expense ratios, but the real story of actively managed vs. index funds often lies deeper, in their internal mechanics. How these funds operate day-to-day creates massive differences in risk, portfolio turnover, and—most importantly—your tax bill. These factors can quietly drain your returns, making them a crucial part of your decision.

The core difference comes down to portfolio turnover. This is just a fancy way of saying how often a fund manager buys and sells investments. For active funds, high turnover is the name of the game; managers are constantly trading to find that next big winner. In sharp contrast, index funds are lazy by design. They only trade when the index they’re tracking changes, which means their turnover is incredibly low.

Why High Turnover Can Wreck Your Tax Bill

This single difference—turnover—has huge tax consequences, especially if you’re investing in a taxable brokerage account. Every time a fund manager sells an asset for a profit, it triggers a capital gain. That gain has to be passed on to you, the shareholder.

An actively managed fund with a turnover rate of 85% is basically a capital gains machine. It’s constantly buying and selling, which means you’re likely to get hit with a capital gains distribution every single year. This creates the bizarre and frustrating situation where you owe taxes on the fund’s activity, even if you never sold a single share yourself.

Index funds, with their minimal turnover (often around 4%), sidestep this problem almost entirely. They rarely generate significant capital gains, which makes them far more tax-efficient. This lets your money compound without the government taking a slice every year, a huge advantage for long-term growth.

The constant trading in active funds creates a “tax drag” that eats away at your returns. An active manager might beat the market before taxes, but once the annual tax bill from all that trading comes due, that advantage can vanish, leaving you with less than a simple index fund would have delivered.

Understanding the tax implications is non-negotiable for smart investing. For a closer look at the mechanics, you can learn more about how capital gains tax is calculated in Canada. This context really drives home why a low-turnover strategy is so powerful.

The Two Types of Risk You’re Taking On

When we talk about risk, it’s not just about the market going up or down. Both fund types expose you to market volatility, but they each add their own unique layer of risk you need to be aware of.

Active funds saddle you with “manager risk.” This is the risk that the star manager you picked makes a few bad calls, underperforms their peers, or just decides to retire. You aren’t just betting on the market; you’re betting on a specific person or team. While a brilliant manager could theoretically sidestep a crash, the data overwhelmingly shows this is a rare exception, not the rule.

Index funds completely eliminate manager risk. By tracking an index, its performance is as predictable as it gets—it will deliver the market’s return, minus a tiny fee. The flip side is you are buckled in for the entire ride. There’s no manager to soften the blow of a market crash; you get 100% of the market’s ups and downs.

This trade-off is at the heart of the actively managed funds vs index debate. Here’s a quick breakdown of how they stack up on risk and tax efficiency:

| Factor | Actively Managed Funds | Index Funds |

|---|---|---|

| Primary Risk | Market risk + Manager risk | Systematic market risk only |

| Turnover Rate | High (often 50-100%+) | Low (typically <10%) |

| Tax Efficiency | Generally low due to frequent capital gains | High due to infrequent trading |

| Predictability | Low; depends on the manager’s strategy | High; tracks a specific market benchmark |

Ultimately, choosing an index fund is a conscious decision to accept the market’s volatility in exchange for eliminating manager risk, slashing costs, and dramatically improving your tax situation. For the vast majority of long-term investors, this proves to be the most reliable path to building wealth.

Choosing Your Strategy: Scenarios and Use Cases

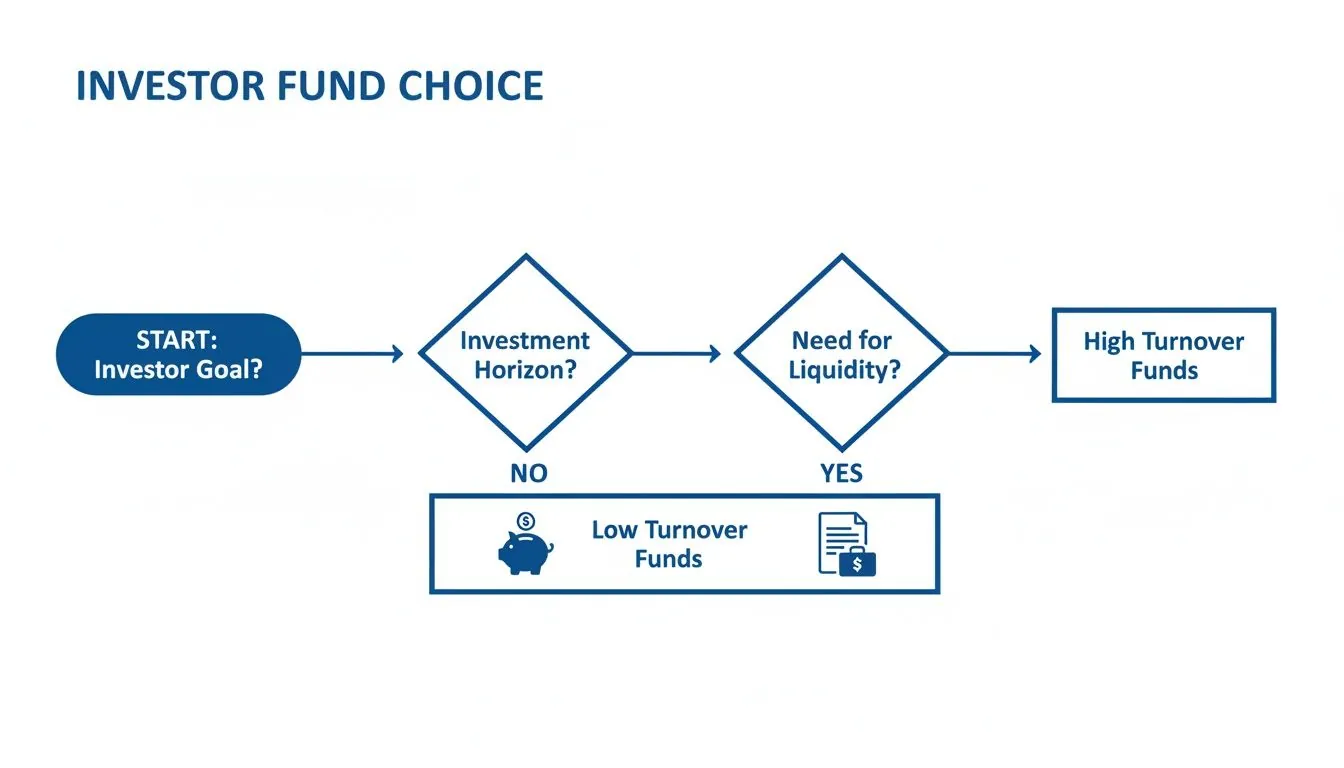

Knowing the data behind actively managed funds versus index funds is one thing, but applying it to your own life is a completely different ballgame. The best strategy isn’t a one-size-fits-all solution—it really comes down to your financial goals, your timeline, and even your personality. This section breaks down some practical scenarios to help you figure out which approach makes the most sense for your investment journey.

This decision tree can help you visualize the key factors that should influence your choice, especially when considering the turnover rates of different funds.

As the flowchart shows, investors playing the long game and aiming for tax-efficient wealth accumulation are almost always better served by the low-turnover nature of index funds.

When to Prioritize Index Funds

For the vast majority of us, especially anyone focused on long-term goals, index funds are the perfect foundation for a portfolio. They’re simple, cheap, and tax-efficient, making them an incredibly powerful tool for building wealth steadily over time.

Think of index funds as your go-to in these common situations:

- Building a Core Retirement Portfolio: If you’re saving for retirement decades down the road, index funds are pretty much unmatched. A straightforward mix of a total U.S. stock market fund, an international stock fund, and a bond fund gives you global diversification at a rock-bottom cost. This lets your money compound with minimal interference.

- You’re a New Investor: Getting started with investing can feel overwhelming. Index funds cut through the noise by eliminating the need to research individual stocks or vet fund managers. Dollar-cost averaging into a broad market index fund is one of the most effective and least stressful ways to begin.

- Adopting a “Set-and-Forget” Strategy: Life gets busy. If you’d rather not spend your weekends glued to market news, index investing is for you. You can automate your contributions, rebalance once a year, and rest easy knowing you’re capturing the market’s long-term growth.

- Investing in Taxable Accounts: As we’ve covered, the low turnover of index funds makes them far more tax-efficient. If you’re investing outside a tax-advantaged account like a 401(k) or IRA, using index funds can save you a bundle on capital gains taxes over the years.

Niche Scenarios for Active Funds

While the data shows index funds win out for most people in the long run, there are a few specific, nuanced situations where an actively managed fund might be worth a look. Just know that this path requires a lot more research and a clear-eyed view of the risks.

Active funds might be considered for a small, satellite slice of your portfolio if you are:

- Seeking Specific Downside Protection: Some active funds are built specifically to hedge against market downturns using complex strategies. For retirees or those who can’t stomach much risk, these “managed volatility” or “absolute return” funds might offer peace of mind. The trade-off? They often come with high fees and can seriously lag in bull markets.

- Targeting Inefficient Markets: The strongest case for active management is in markets where information isn’t as widespread, like emerging markets or small-cap stocks. A skilled manager with a research team on the ground might find opportunities that a broad index would miss. But even here, SPIVA data shows most managers still fall short.

- Investing in Specific Niche Sectors: Want to get very granular with an industry like telecommunications or data centers? An active manager specializing in that space might offer deeper expertise than a broad sector index. For example, recent data shows active managers overweighting telecom assets at 136% of their index share, signaling strong conviction in that area.

A key takeaway here is that even when you find a reason to use an active fund, it should almost always supplement, not replace, a core holding of low-cost index funds. This “core-satellite” approach lets you keep a reliable, diversified base while you make a few calculated bets on the side.

Ultimately, the choice boils down to aligning your strategy with your goals. For reliable, long-term wealth creation, the evidence overwhelmingly points toward a simple, low-cost index fund approach. If you decide to dip your toes into active management, do it with a clear purpose, a small allocation, and a healthy dose of skepticism.

How to Build and Monitor Your Ideal Portfolio

All the theory in the world doesn’t mean much until you put it into practice. This is where you actually start building wealth—by turning the insights from the actively managed funds vs index debate into a real portfolio.

The best first move? Keep it simple. Build a globally diversified portfolio that you can stick with for the long haul. For most of us, that means using low-cost index funds or ETFs as the bedrock. They give you broad exposure to the entire market without the hefty fees and guesswork that come with active funds.

A great starting point is a three-fund core: one for the total U.S. stock market, one for the total international stock market, and one for the total bond market. This straightforward setup ensures you’re not betting the farm on a single country or asset class. If you’d like a more detailed breakdown, our guide on how to diversify your investment portfolio walks you through the specifics.

Monitoring Your Portfolio Effectively

Once your portfolio is live, the work isn’t over. You need to keep an eye on it to make sure it’s tracking toward your goals. This is where a modern portfolio tracker like PopaDex comes in, taking you from anxious guessing to data-backed confidence.

Just connect your brokerage accounts, and PopaDex will pull in your data automatically. No more manual spreadsheets. You get a real-time, consolidated view of all your investments in one place.

You can also add other assets manually—like real estate or private equity—and track your liabilities to get a true picture of your net worth. It’s this holistic view that powers smart financial decisions.

Here’s a glimpse of what the PopaDex dashboard looks like, giving you a clear visual of your asset allocation and overall growth.

The dashboard instantly shows if your asset mix is aligned with your targets and helps you measure your progress toward your biggest financial milestones.

Using Data to Stay on Course

A good tracking tool does more than just show you numbers; it reveals the real-world impact of your investment choices. You can see exactly how much fees are costing you over time or how your investments in different currencies are performing.

This constant feedback loop is your best defense against making emotional, reactive moves when the market gets choppy. It helps you stay disciplined and focused on the long game.

The big picture is undeniable: investors are steadily moving toward passive strategies. The right tools make it incredibly easy to build an evidence-based portfolio and see for yourself why it works, keeping you aligned with your long-term vision.

Despite the mountain of evidence favoring index funds, the split between active and passive investing is still surprisingly close. But if you look at where the new money is going, the story becomes crystal clear.

Recently, total assets in U.S. actively managed funds and ETFs hit $17.46 trillion, while indexed funds and ETFs climbed to $19.12 trillion. In just one month, indexed funds pulled in more than double the new cash that active funds did. This isn’t a fluke; it’s a trend driven by years of data proving that, after fees, passive investing consistently comes out ahead.

Common Questions Answered

Even with all the data, it’s normal to have a few questions rolling around in your head. Let’s tackle some of the most common ones to help you nail down your investment strategy.

Can I Use Both Fund Types In My Portfolio?

You absolutely can. In fact, a popular and really effective strategy is known as “core-satellite.” It’s a great way to blend both approaches.

The idea is simple: You use low-cost, broadly diversified index funds as the stable “core” of your portfolio. This part is designed to reliably capture the market’s overall returns. Then, you can allocate a smaller slice of your capital to actively managed funds as “satellites” to target specific areas or chase unique strategies where you think a manager might have a real edge. This gives you a nice balance—the steady reliability of passive investing with a shot at outperformance from active management.

When Might Active Funds Actually Outperform?

It’s a fair question. While the long-term data for broad markets isn’t kind to active managers, the argument is that they have a better chance in less “efficient” markets. These are corners of the investment world where information isn’t as widely available, giving sharp managers a chance to spot undervalued gems before everyone else does.

A few examples that often come up include:

- Emerging markets, where on-the-ground local knowledge could be a game-changer.

- Small-cap stocks, which don’t get nearly as much attention from big-name analysts.

- Niche bond categories with complex credit risks that require deep expertise.

But—and this is a big but—it’s critical to remember that even in these areas, the data from scorecards like SPIVA often shows the majority of active managers still fail to beat their benchmarks over the long haul, especially once you factor in their higher fees.

How Do I Find The Best Low-Cost Index Funds?

Finding a great index fund is pretty straightforward once you know what to look for. First, decide which market you want to track—maybe the S&P 500 for big U.S. companies or the MSCI World for a global view.

From there, you’ll want to check out the ETFs and mutual funds from the major players like Vanguard, iShares (from BlackRock), Fidelity, and Charles Schwab.

The single most important number to look at is the expense ratio. For common, broad market indexes, you should be looking for funds with expense ratios well below 0.10%. Also, double-check for any trading commissions on your brokerage platform to keep your total costs as low as humanly possible.

Ready to see how your fund choices impact your net worth? Take control of your financial picture with PopaDex. Track all your accounts in one place, monitor fees, and watch your wealth grow. Start for free at popadex.com.