Our Marketing Team at PopaDex

What Is the Average IRA Balance by Age and Where Do You Stand?

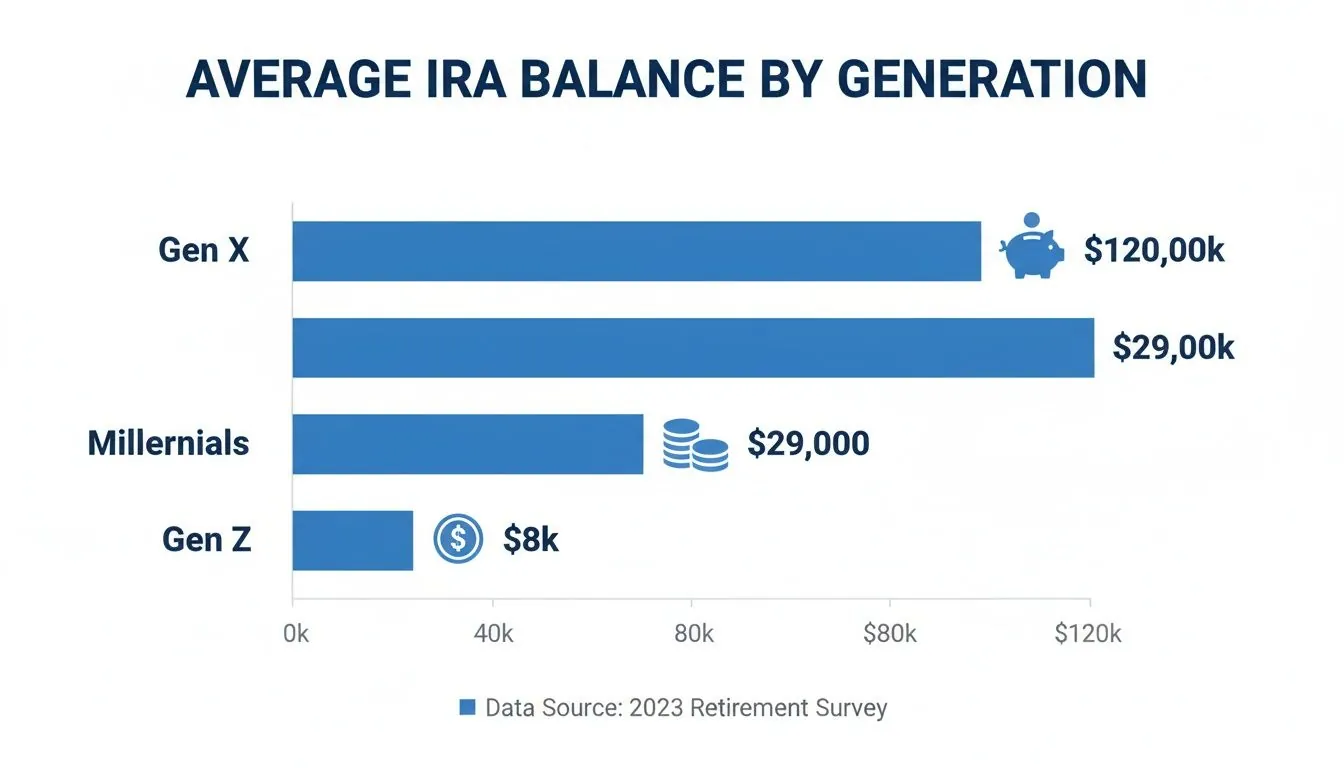

Ever wonder how your IRA stacks up against others your age? It’s a natural question. Recent data shows Millennials (ages 29-44) have an average IRA balance of about $29,410, while Gen X (ages 45-60) is sitting on an average of $120,273. These numbers really drive home the power of long-term, consistent investing.

A Quick Look at Average IRA Balances by Age

Knowing where you are is the first step to getting where you want to go, and your retirement journey is no different. Comparing your Individual Retirement Account (IRA) balance to the national averages gives you a useful reference point. It’s a simple way to see if your saving habits are on track, a little behind, or maybe even ahead of the curve.

Think of these numbers as landmarks on a map. They show you where you are relative to others, but they don’t dictate your final destination. Your personal retirement goals, your income, and the lifestyle you want will ultimately chart your unique course. Still, having a baseline is crucial for setting realistic and motivating savings targets.

Benchmarking Your Savings Against Your Generation

To give you a clearer picture, let’s break down the average IRA balances by generation. These figures are a snapshot in time and can shift based on market performance, economic trends, and even the unique saving habits of each generation.

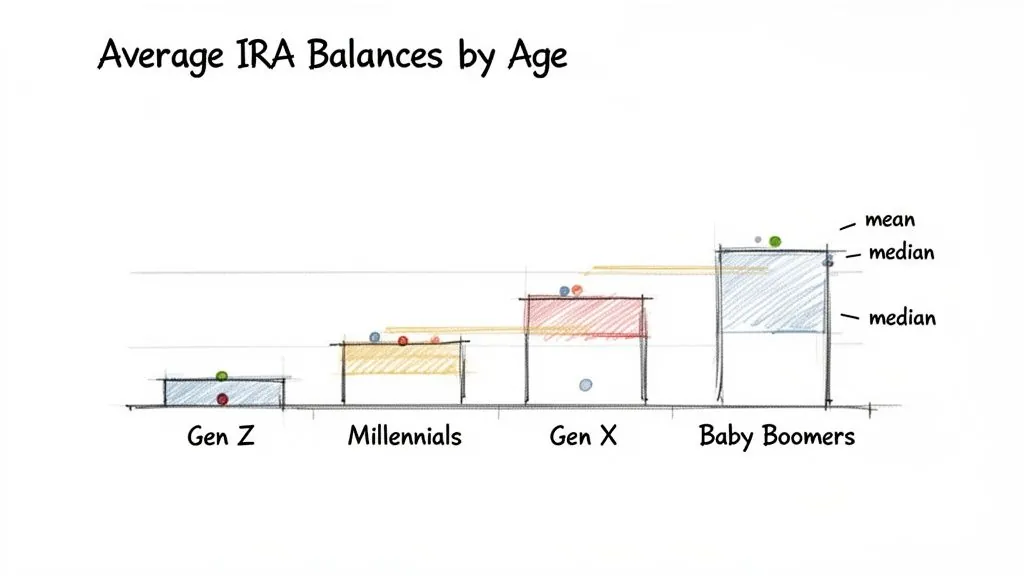

Here’s a quick summary of both the mean (the mathematical average) and the median (the middle value) IRA balances for major age groups. The median is often a more realistic benchmark because it isn’t skewed by a small number of accounts with extremely high balances.

Average IRA Balance by Generation

This table offers a snapshot of where different generations stand with their IRA savings, highlighting the key financial pressures influencing their progress.

| Generation (Age Range) | Average (Mean) IRA Balance | Median IRA Balance | Primary Savings Influences |

|---|---|---|---|

| Gen Z (13-28) | $8,019 | $3,100 | Just starting careers, prioritizing short-term goals and debt. |

| Millennials (29-44) | $29,410 | $14,933 | Balancing student loans, homeownership, and family costs. |

| Gen X (45-60) | $120,273 | $60,763 | Reaching peak earning years, leveraging catch-up contributions. |

| Baby Boomers (61-79) | $287,640 | $87,571 | Shifting focus to wealth preservation and withdrawal strategies. |

As you can see, the gap between the mean and median grows wider with age, which tells us that a smaller group of high-earners tends to pull the average up significantly.

This visual really highlights the dramatic jump in savings between younger generations and those in their prime earning years, showcasing the incredible effect of decades of compounding growth.

Remember, your IRA is just one piece of your retirement puzzle. It’s crucial to consider all your accounts, including any 401(k)s, for a complete financial picture.

While an IRA is a fantastic savings tool, it often works in tandem with an employer-sponsored plan. To get the full story on retirement benchmarks, you might find our guide on the average 401(k) balance by age helpful. Looking at both helps you build a much stronger, more complete strategy for your future.

Why Averages Alone Can Be Deceiving

Looking at the average IRA balance by age can be a bit like checking the average temperature of a hospital—it tells you almost nothing about the health of any single patient. One person could be running a high fever while another is perfectly fine, yet the average might look completely normal. That’s why you have to dig a little deeper for a realistic financial check-up.

When you see the word “average,” it almost always means the mean. This is the simple calculation where you add up all the account balances and divide by the number of accounts. It’s straightforward, but it has one massive weakness, especially when you’re talking about money.

A small handful of extremely high balances—think of the accounts held by “super-savers” or the ultra-wealthy—can drag the mean way, way up. This creates a skewed picture that doesn’t reflect what a typical person actually has saved.

The Billionaire in the Room Analogy

Let’s make this crystal clear with an analogy. Imagine ten people are in a room talking about their retirement savings. Nine of them have a respectable $50,000 tucked away in their IRA. The tenth person? A billionaire with $1 billion in their account.

If we calculate the mean savings for this group, the result is over $100 million per person. That number is technically correct, but is it a fair representation of the nine people with $50,000? Not even close. It’s completely misleading.

This is exactly why another type of average, the median, is so much more useful.

Why the Median Is Your More Realistic Benchmark

The median is simply the middle number in a data set. If you were to line up every single IRA balance from the smallest to the largest, the median is the value that sits smack-dab in the middle. Half the accounts will have more than this amount, and half will have less.

Let’s go back to our room of ten savers. If we arrange their balances in order, the middle value (the median) is $50,000. Now that number provides a far more accurate and relatable benchmark for the typical person in the room. It isn’t thrown off by the billionaire outlier.

By focusing on the median IRA balance, you get a much clearer sense of the central tendency—or what is ‘typical’—for your age group, helping you set more attainable and meaningful goals.

When you’re looking at financial data, the median almost always tells a more honest story. If you ever need to find the middle value in a skewed dataset, a median calculator can give you a more robust measure.

Shifting Your Focus Beyond a Single Number

At the end of the day, both the mean and the median are just reference points. They give you some context, but they don’t define your personal financial journey. Obsessing over a national average can be discouraging if you feel like you’re behind or, worse, create a false sense of security if you’re ahead.

The goal isn’t just to beat an average. The real objective is to build a retirement plan that will actually support the life you want to live. Instead of getting bogged down by a single statistic, it’s far more productive to focus on the things you can actually control.

These are the metrics that truly matter for your long-term success:

- Your Personal Savings Rate: What percentage of your income are you consistently putting away for the future?

- Your Investment Strategy: Are your investments aligned with your age, how much risk you’re comfortable with, and your long-term goals?

- Your Progress Over Time: Is your net worth actually growing year after year? Are you moving in the right direction?

Focusing on these personal metrics shifts your mindset from comparison to progress. It’s all about building strong financial habits and making smart decisions over and over again. That’s the most reliable path to a secure retirement, no matter what the national averages say.

A Generational Guide to Retirement Savings

Knowing the national averages for IRA balances is a good starting point, but the numbers really click when you see them through the lens of your own generation. Every age group has its own financial landscape to navigate—from landing that first job to figuring out wealth distribution in your later years.

Your age doesn’t just dictate how much you should have saved; it shapes your entire investment philosophy. A 25-year-old and a 65-year-old are playing completely different games when it comes to risk, growth, and time. Let’s break down what the numbers mean for you, wherever you are on your financial journey.

Gen Z (Ages 13-28) Your Superpower is Time

For Gen Z, your single greatest financial asset isn’t a six-figure salary or a family inheritance—it’s time. With decades stretching out before retirement, every dollar you invest has an incredible runway to grow thanks to the magic of compound interest.

Think of it like this: a small sapling planted today will grow into a massive oak tree over 50 years. It will tower over a much larger tree planted just 10 years from now. That’s why starting early, even with tiny amounts, is a financial superpower.

The goal for this generation isn’t to have a huge balance right now. It’s all about building the habit of consistent saving and letting time do the heavy lifting.

- Primary Goal: Build a consistent savings habit and give your money as much time as possible to compound.

- Key Challenge: Juggling lower starting salaries with the desire to get ahead.

- Best Strategy: Automate small, regular contributions to a Roth IRA. This locks in tax-free growth for decades. Even $50 a month can snowball into a serious nest egg over a long career.

Millennials (Ages 29-44) The Great Balancing Act

Millennials are often right in the middle of the most financially complicated years of their lives. Many are juggling student loan debt, the crushing cost of a down payment, and the ever-rising expenses of raising a family. With all these competing priorities, saving for retirement can feel like just another thing on an overwhelming to-do list.

This is the generation where the average IRA balance by age starts to climb, but it’s often a hard-fought battle. The key is to stop long-term goals from getting completely shoved aside by short-term pressures.

For Millennials, progress is far more important than perfection. Finding a savings rate that actually works with your budget—and bumping it up little by little—is the most realistic path to success.

A recent analysis confirms these generational patterns. In the third quarter of 2025, the average IRA balance across all savers was $137,900. The breakdown showed Gen Z with an average of $8,019, while Millennials held $29,410—a perfect illustration of the slow but steady accumulation phase they’re in. You can explore more about these retirement savings trends to see how that consistency pays off.

Gen X (Ages 45-60) Time to Hit the Accelerator

Generation X is typically cruising through its peak earning years, which opens up a golden opportunity for retirement savings. With bigger paychecks and potentially fewer kid-related expenses, now is the time to supercharge your contributions.

For many in this age group, retirement is no longer some abstract idea—it’s a fast-approaching reality. That sense of urgency often sparks a renewed focus on making up for lost time or simply taking full advantage of a higher salary.

This is also the first generation that gets to use a powerful tool designed just for them.

Making the Most of Catch-Up Contributions Once you turn 50, the IRS gives you a special perk: the ability to contribute extra money to your IRA each year. These are called catch-up contributions, and they’re designed to help you accelerate your savings as you get closer to the finish line.

- For 2024: The standard IRA contribution limit is $7,000.

- Catch-Up Amount: Savers aged 50 and over can tack on an extra $1,000.

- Total Potential: That brings your total possible contribution to $8,000 a year.

Taking advantage of these extra contributions can add tens of thousands of dollars to your nest egg in that final decade before retirement.

Baby Boomers (Ages 61-79) The Shift to Preservation

For Baby Boomers, the financial game changes completely. The focus shifts from accumulation to preservation and distribution. Your primary goal is no longer about growing wealth as fast as possible, but about making sure the wealth you’ve built lasts for the rest of your life.

The conversation turns from “How much can I save?” to “How do I create a reliable income stream?” This means making critical decisions about when to claim Social Security, how to manage required minimum distributions (RMDs), and how to dial back risk in your investment portfolio.

The priority now is protecting your principal while generating enough income to live comfortably. This often means shifting away from growth-focused stocks and toward more stable, income-producing assets like bonds and dividend stocks. It’s all about securing the financial future you worked so hard to build.

Actionable Strategies to Boost Your IRA Balance

Seeing the average IRA balance for your age group can be a real eye-opener, but turning that awareness into action is what actually builds wealth. Let’s get into your playbook for growth—practical, straightforward strategies you can put in motion today to start seeing your own numbers climb.

This isn’t about fancy financial footwork or trying to time the market. It’s all about creating simple, consistent habits that pay off big time down the road. Every massive retirement account you see was built on a foundation of small, steady actions.

Put Your Contributions on Autopilot

The single most powerful thing you can do to grow your IRA is to automate your contributions. Set up an automatic transfer from your checking account to your IRA, and you instantly remove willpower and emotion from the savings game. It just becomes another bill you pay—this one to your future self.

Think of it as the “set it and forget it” method. Whether you start with $50 a paycheck or $500 a month, consistency is what really moves the needle. This approach, known as dollar-cost averaging, ensures you’re buying into the market on a regular basis, smoothing out the highs and lows over time.

Maximize Free Money First

Before you send a single dollar to your IRA, make sure you aren’t leaving free money on the table at work. If your employer offers a 401(k) with a matching contribution, your top priority should be contributing enough to snag that full match.

An employer match is an immediate, guaranteed return on your investment—often 50% or 100%. You won’t find another investment that offers that kind of instant, risk-free gain anywhere else.

Once you’ve secured the full 401(k) match, then you can shift your focus to funding your IRA. This one-two punch ensures you’re making the most of every retirement savings tool available to you.

Choose the Right IRA for Your Tax Situation

The choice between a Traditional IRA and a Roth IRA has huge tax implications down the line. The right fit depends on your income now versus what you think your income (and tax bracket) will look like when you retire.

- Traditional IRA: Your contributions might be tax-deductible today, which lowers your current taxable income. The trade-off? You’ll pay income tax on your withdrawals in retirement. This can be a smart move if you expect to be in a lower tax bracket when you retire.

- Roth IRA: You contribute with after-tax dollars, so there’s no upfront tax break. But the payoff is massive: all your qualified withdrawals in retirement are 100% tax-free. This is a fantastic option if you think you’ll be in a higher tax bracket later in life.

For most younger savers with decades of career growth ahead, the Roth IRA is often the clear winner because it locks in that tax-free growth for the long haul.

Perform an Annual Financial Check-Up

Your financial life isn’t set in stone, so your retirement strategy shouldn’t be either. Make a habit of setting aside time once a year to review your progress and make any necessary tweaks. This simple check-up is a game-changer.

During your review, ask yourself a few questions:

- Can I bump up my contribution? Even a 1% increase can make a shocking difference over a few decades.

- Is my investment mix still right for me? Your comfort with risk might change as you get closer to retirement.

- Am I on track to hit my goals? If not, what small adjustments can I make to get back on course?

This yearly ritual keeps you in the driver’s seat of your financial future. If you feel like you’ve fallen behind, take a look at our guide on how to catch up on retirement savings for some more targeted ideas.

Avoid Common and Costly Mistakes

Building a healthy IRA balance is just as much about dodging mistakes as it is about making smart moves. Two of the biggest blunders are being too conservative with your investments and pulling money out prematurely. A solid grasp of how to invest money for beginners is critical to steering clear of these pitfalls.

Younger investors, especially, need to embrace a growth-focused strategy. With decades ahead of you to recover from any market dips, playing it too safe means missing out on the compounding power that truly fuels long-term growth. Those impressive six-figure IRA balances weren’t built by sticking to safe, low-return investments for 40 years.

How to Track Your Progress and Stay on Course

Knowing the average IRA balance for your age is like having a map of the entire country. It’s useful, for sure, but it doesn’t tell you where you are on that map. All the benchmarks and savings strategies in the world are just theory until you have a way to measure your own journey.

This is where you make the leap from knowing the numbers to actually managing them. It’s how you turn a vague retirement goal into a reality you can see taking shape. The secret is to shift from abstract goals to concrete, visible progress, day by day.

Your Financial Co-Pilot

Think of a dedicated net worth tracker as your financial co-pilot. It gives you a single dashboard for your entire financial life—a place where your IRA, 401(k), brokerage accounts, and other investments all come together. No more logging into five different websites to piece together your progress.

This holistic view is absolutely critical. Your IRA is a big piece of the puzzle, but it’s still just one piece. A powerful tracking tool helps you answer the questions that really drive growth:

- How are my contributions actually moving the needle on my total net worth?

- Is my investment strategy working across all my accounts, or just one?

- Where are my biggest opportunities to save more or knock down debt?

See Your Entire Financial World in One Place

Let’s be honest, modern financial lives are messy. You might have an IRA with one company, an old 401(k) somewhere else, a little bit of crypto, and maybe even investments in different currencies. A tool like PopaDex is built for exactly this kind of complexity. It brings everything into a single, clean view.

This screenshot shows how PopaDex pulls your whole portfolio into one simple, easy-to-read dashboard.

It gives you an instant snapshot of your net worth, breaking it down so you can see where your wealth is and how it’s performing.

This isn’t just about watching numbers go up. It’s about building confidence. When you can actually see your progress visualized, it becomes a powerful motivator. It encourages you to stick with your savings plan, even when the market gets shaky or life throws a few expensive curveballs your way. For a deeper dive into setting targets, our retirement savings calculator by age can help you dial in specific goals to track.

By pulling all your financial data into one place, you move past the guesswork. You can finally make decisions based on a complete and accurate picture of your finances, making sure every dollar is working as hard as it can for your future.

Designed for the Modern Investor

Today’s investor looks a lot different than the last generation. Freelance gigs with irregular income, managing assets in multiple currencies, and tracking alternative investments are all part of the new normal. Older, more traditional tools just weren’t built for this.

PopaDex tackles these modern challenges head-on:

- Multi-Currency Support: Essential if you’re an expat, remote worker, or have international investments. It automatically converts and tracks everything in your home currency.

- Irregular Income Tracking: A game-changer for gig workers and business owners. It provides a realistic view of your financial health when your income isn’t a steady paycheck.

- Comprehensive Asset Integration: From your bank accounts and stocks to real estate and crypto, you get a full accounting of your entire net worth.

In the end, tracking your progress is what makes a retirement plan feel real. It transforms abstract savings goals into a tangible, measurable journey. When you can clearly see the results of your discipline, you build the momentum you need to stay the course and reach the future you’ve been working for.

Common Questions About IRA Balances

After digging into all the data on IRA balances, it’s totally normal for a few more questions to pop up. Seeing the numbers is one thing, but figuring out how they apply to your financial life is what really matters.

Let’s tackle some of the most common questions head-on to clear up any confusion and help you move forward with a solid plan.

What Is a Good IRA Balance for My Age?

Instead of getting hung up on a single national average, a much better target is a multiple of your annual salary. This approach tethers your savings goals directly to your income and the lifestyle you actually want to maintain down the road.

Many financial experts point to these general benchmarks for your total retirement savings:

- By age 30: Aim for 1x your annual salary.

- By age 40: You should have about 3x your annual salary saved.

- By age 50: Work toward having 6x your annual salary.

- By retirement: The goal is 8-10x your annual salary.

Remember, your IRA is just one piece of this puzzle. You need to factor in your 401(k), brokerage accounts, and any other retirement funds to get the full picture of where you stand.

Should I Choose a Roth or Traditional IRA?

The choice between a Roth and a Traditional IRA really boils down to one simple question: Do you expect to pay more in taxes now or in retirement?

A Roth IRA is fantastic if you think you’ll be in a higher tax bracket later in life. You contribute with after-tax dollars, so you don’t get a tax break today. The huge payoff? All of your qualified withdrawals in retirement are completely tax-free.

On the flip side, a Traditional IRA can be a better fit if you need a tax deduction now or believe you’ll be in a lower tax bracket when you retire. Your contributions might be tax-deductible, which lowers your taxable income today, but you’ll pay income taxes on your withdrawals later.

Think of it this way: With a Traditional IRA, you pay taxes later. With a Roth IRA, you pay them now. For most young professionals with decades of income growth ahead, the Roth IRA often ends up being the more powerful long-term tool.

What if My Balance Is Way Below the Average?

First thing’s first: don’t panic. Comparing yourself to a national statistic can feel defeating, and it’s not a productive way to think about your own journey. The most powerful move you can make is to simply start from where you are today.

Focus on your own progress, not on where someone else might be. Every massive IRA balance out there began with a small, consistent first step. Here are a few things you can do right now to start closing the gap:

- Create a Simple Budget: Get a real handle on where your money is going. This almost always uncovers opportunities to redirect cash toward your savings goals.

- Automate Your Contributions: Set up a recurring transfer to your IRA, even if it’s a small amount to start. This builds the habit and makes sure you’re consistently investing without even thinking about it.

- Use Catch-Up Contributions: If you’re age 50 or older, you can contribute an extra $1,000 to your IRA each year. It’s a fantastic tool designed specifically to help you accelerate your savings.

Ultimately, it’s all about momentum. Tracking your personal growth with a dashboard can be incredibly motivating and helps you celebrate your own wins—big or small—along the way.

Ready to stop guessing and start seeing your real financial picture? With PopaDex, you can track your IRA, 401(k), and your entire net worth in one simple, clear dashboard. Gain the clarity you need to build the future you want by signing up for free at https://popadex.com.