Our Marketing Team at PopaDex

How to Calculate Personal Net Worth From Scratch

At its core, calculating your personal net worth comes down to a simple, powerful formula: Assets (what you own) minus Liabilities (what you owe). This single number is the most important metric for understanding your true financial health at any given moment. It’s a clear, honest snapshot of where you stand.

Your Financial Snapshot: Understanding Net Worth

Before you start pulling up bank statements and digging through spreadsheets, it’s worth taking a moment to appreciate why this calculation actually matters. Your net worth isn’t some grade on your financial report card, and it’s certainly not a measure of your self-worth. It’s a practical tool.

Think of it as your financial GPS. It tells you your exact location, which is the first step in plotting a course to where you want to go—whether that’s a comfortable retirement, financial independence, or buying your first home. When you see it this way, a simple accounting exercise transforms into a strategic planning session. It reveals the progress you’re making over time, highlights your wins (like a growing investment portfolio), and shines a light on potential risks (like mounting credit card debt).

Why Tracking Your Net Worth Is Crucial

Honestly, if you’re not tracking your net worth, you’re flying blind. You’re making financial decisions based on guesswork, not data. Monitoring this number regularly puts you back in the driver’s seat. It empowers you to:

- Measure Real Progress: See if your wealth is actually growing, just treading water, or—worse—declining over months and years.

- Set Goals That Make Sense: Knowing your starting point makes it way easier to set achievable targets for saving, investing, and smashing debt.

- Make Smarter Decisions: A clear net worth picture helps you confidently decide if you can afford that major purchase or if you should focus on beefing up your savings instead.

Globally, personal wealth is on the rise. A recent report from UBS noted that global wealth surged by 4.6%, with adults in North America averaging $593,347. But that growth isn’t a given for everyone; over half of markets saw wealth declines in real terms, which just goes to show why a precise, personal calculation is so vital to stay ahead of the curve.

To help you get started, it’s useful to know exactly what counts as an asset versus a liability. Here’s a quick cheat sheet to get you organized.

Quick Guide to Assets and Liabilities

| Category | What It Is | Examples |

|---|---|---|

| Assets | Anything you own that has monetary value. | Cash, savings accounts, investments (stocks, bonds), retirement funds (401k, IRA), real estate, vehicles, valuable personal property. |

| Liabilities | Any debt or financial obligation you owe to someone else. | Mortgage, car loan, student loans, credit card balances, personal loans, medical debt. |

Think of this table as your starting point. As you gather your financial documents, you can start sorting everything into these two columns before you even touch a calculator.

The core idea is simple: what gets measured gets managed. When you consistently calculate your personal net worth, you gain a tangible benchmark for every financial choice you make. It helps you see the direct impact of saving an extra hundred dollars or paying down a high-interest loan. This isn’t about comparing yourself to others—it’s about competing with who you were yesterday.

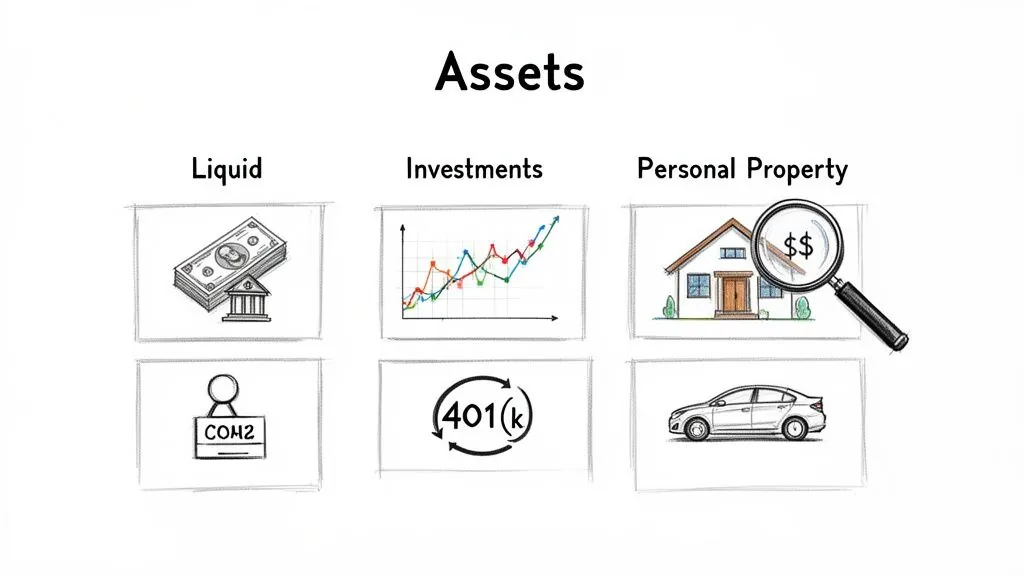

Identifying and Valuing Your Assets

Alright, with the basics covered, let’s get into the nitty-gritty and build the first half of your net worth equation. This is all about taking a detailed inventory of everything you own that has monetary value. The goal here is to be both thorough and realistic to paint an honest picture of your financial resources.

To keep this from feeling overwhelming, I always recommend breaking your assets down into categories. It makes the whole process smoother and, more importantly, gives you a clearer view of your financial structure. Are you cash-heavy? Investment-focused? Or is most of your wealth tied up in your home? Let’s find out.

Your Liquid Assets

We’ll start with the easy stuff: your liquid assets. These are the things that are either cash already or can be turned into cash in a snap. Think of this as your most accessible money.

Finding these values is straightforward. Just log into your online banking portals or grab your most recent statements. You’re looking for the exact balance on the day you’re doing this calculation.

- Checking Accounts: The total amount sitting in all your checking accounts.

- Savings Accounts: Pull the balances from any high-yield savings, standard savings, or money market accounts you have.

- Cash on Hand: Don’t laugh—that emergency stash of cash you keep at home counts! It might not be a game-changer, but every dollar adds to the accuracy.

- Certificates of Deposit (CDs): Jot down the current value of any CDs you hold.

Valuing Your Investment Portfolio

Next up are your investments. Since these values can change daily, it’s important to use the most recent figures you can get your hands on. A quick check of your latest brokerage or retirement account statement will give you the numbers you need.

For something like a 401(k) through your employer, you want to record the total vested balance. This is the amount you’d walk away with if you left your job today.

Common investments to list include:

- Retirement Accounts: This covers your 401(k), 403(b), IRA (both Roth and Traditional), and any pension funds.

- Brokerage Accounts: The current market value of your stocks, bonds, mutual funds, and ETFs held in taxable accounts.

- Health Savings Accounts (HSA): If you’re using your HSA as an investment tool (which is a great strategy), include its current balance.

Keeping all these figures organized is key. If you’re looking for a simple, effective way to track everything manually, you can grab a great net worth tracking spreadsheet to get started.

When you calculate personal net worth, precision is your friend. Avoid the temptation to guess. Taking a few extra minutes to log in to each account and pull the exact numbers builds a foundation of accuracy that makes the final result far more reliable and useful.

Assessing Your Personal Property

This is often the trickiest part because the value isn’t neatly listed on a monthly statement. Personal property covers your big-ticket physical possessions. The key here is to find a reasonable market value for each—what someone would actually pay for it today, not what you paid for it years ago.

For something like your home, getting professional house valuations offers the most precise figure. But for a quick-and-dirty estimate, real estate sites like Zillow or Redfin can give you a decent ballpark number.

Here’s a practical approach for valuing your most common personal assets:

- Real Estate: Use a recent appraisal if you have one, or check a trusted online home value estimator. My advice? Be conservative. Go with a realistic sale price, not an overly optimistic one.

- Vehicles: Jump on sites like Kelley Blue Book or Edmunds to find the current private-party sale value for your car, truck, or motorcycle. Be brutally honest about its condition.

- Valuable Collectibles: For things like fine art, high-end jewelry, or rare collectibles, a professional appraisal is really the only way to go. If that’s not an option, look at what similar items have recently sold for at auction.

It’s easy to get bogged down here, so focus on the big stuff. While your furniture and electronics technically have value, they depreciate fast and are a pain to price accurately. Unless you own specific pieces worth thousands, it’s often easiest to only include items worth $1,000 or more. This keeps your statement from getting cluttered with minor assets.

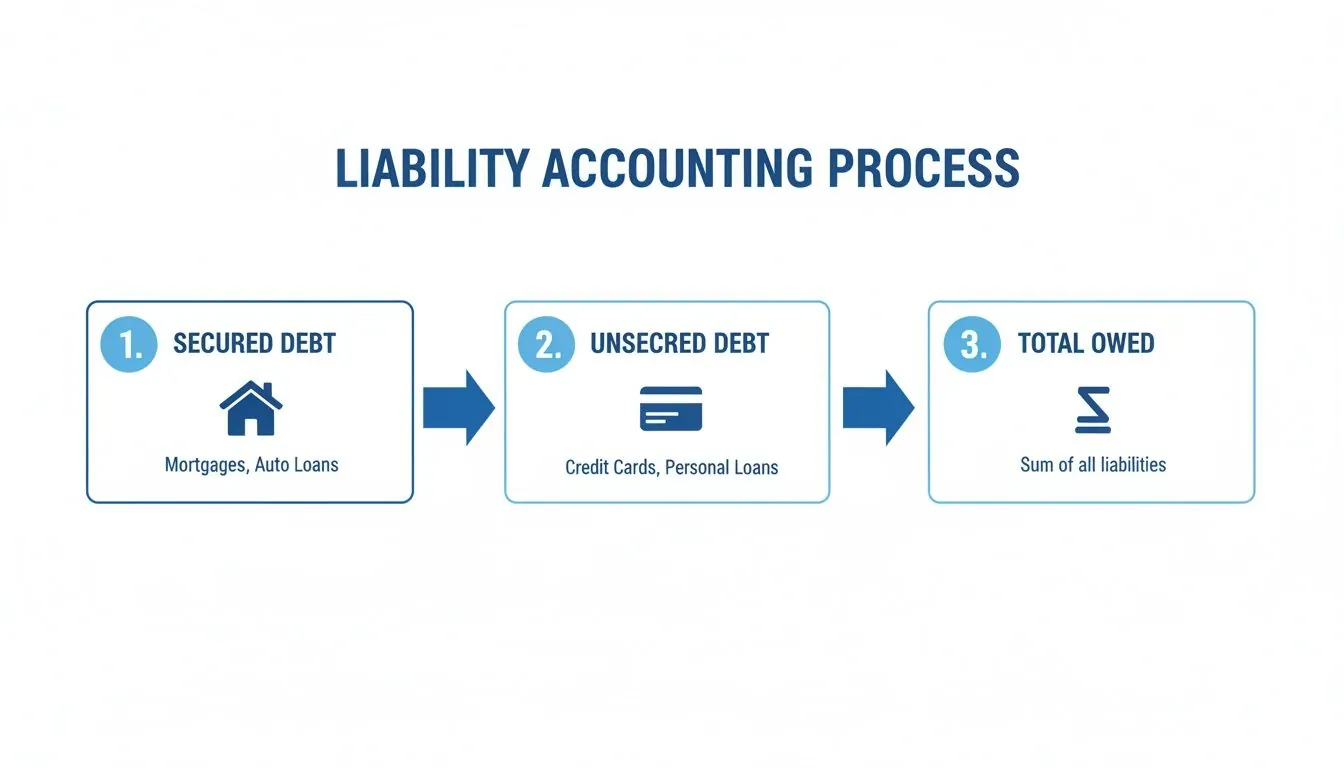

Accounting for Every Liability

Alright, we’ve tallied up everything you own. Now it’s time to flip the coin and look at what you owe. Getting a real, accurate net worth number hinges on being brutally honest and thorough here. This isn’t about making you feel bad; it’s about gaining clarity. You can’t manage what you don’t measure, and these numbers are the first step to taking control.

Your liabilities generally fall into two camps: secured and unsecured debt. Knowing the difference just helps you get organized and understand where your financial promises lie.

Unpacking Secured Debts

Secured debts are loans tied to a physical asset, like your house or your car. If you fall behind on payments, the lender has the right to take that asset back. It’s no surprise that these are usually the biggest liabilities on anyone’s personal balance sheet, so getting these numbers spot-on is critical.

Finding the exact balances is usually pretty straightforward:

- Mortgages: Just log in to your mortgage lender’s website or pull up your last statement. You’re looking for the principal balance remaining—not the original loan amount you took out years ago.

- Home Equity Loans or HELOCs: Same deal as your mortgage. Your latest statement will show the current outstanding balance.

- Auto Loans: Your lender’s website or app will have the current payoff amount for your car loan.

These figures might feel like huge hurdles, but remember, every payment you make on them builds your equity and, in turn, your net worth.

Tallying Up Unsecured Debts

Unsecured debts are the ones not backed by any collateral. This bucket includes everything from the balance on your credit card to that personal loan you took out. Because the lender has nothing to reclaim if you default, these loans almost always carry higher interest rates.

When you calculate personal net worth, you have to be meticulous here. It’s easy to shrug off a few small debts, but they can add up fast and give you a false sense of security.

Here are the usual suspects to list:

- Credit Card Balances: Log in to each and every credit card account. Write down the current statement balance for every single one.

- Student Loans: Head over to your student loan servicer’s website to find the total outstanding balance. Make sure to include both federal and private loans.

- Personal Loans: Add up any loans you’ve taken out, whether for debt consolidation, a kitchen remodel, or anything else.

- Medical Bills: Don’t gloss over any outstanding medical or dental bills you’re currently paying down.

The name of the game is tracking down the current amount owed for each. Guesstimating will only lead to a misleading net worth figure that doesn’t help you.

An honest look at your liabilities is empowering. It transforms that vague, nagging financial stress into a concrete list of numbers you can systematically start knocking down. Every dollar you pay off here directly increases your net worth.

The global wealth landscape really drives home why a complete view of both sides of your financial picture is so important. There were 41.3 million high-net-worth individuals worldwide, but a tiny fraction of them—just 1.1%—held a staggering 32.4% of that wealth. For anyone who is self-employed or seriously planning for retirement, this highlights the need for a comprehensive approach to consolidate both assets and liabilities. Tools like PopaDex are designed to simplify exactly that. You can dig into more of these global wealth trends on altrata.com.

Here’s a quick look at how PopaDex helps you visualize all your liabilities in one clear dashboard.

This view brings all your debts together, showing you exactly where you stand at a glance—from your mortgage all the way down to your credit cards.

The Debts People Often Forget

Finally, let’s talk about the small, sneaky debts that often get overlooked but can trip you up. Go through this list one last time to make sure you’ve caught everything.

- “Buy Now, Pay Later” (BNPL) Plans: Those Afterpay or Klarna purchases? They’re still debt. Tally up the remaining balances.

- Personal Loans from Family or Friends: Even if it was an informal handshake deal, it still counts. Be honest about what you still owe.

- Tax Liabilities: If you owe the IRS or another tax agency from a previous year and are on a payment plan, you need to include the remaining balance.

Once you’ve listed every single liability and its current balance, add them all together. This grand total is the second critical piece of your net worth formula. With your total assets and total liabilities now in hand, you’re ready for the final, satisfying step: subtraction.

Bringing It All Together With a Real Example

Theory is great, but numbers on a page only mean so much. To really make this stick, let’s walk through a real-world scenario to see how all the pieces—assets, liabilities, and the final calculation—come together.

We’ll follow “Alex,” a hypothetical 35-year-old tech professional. Alex has been in the workforce for a decade, bought a condo a few years back, and is diligently saving for retirement. Like most people, Alex has a mix of assets that are growing and debts that are being paid down.

Meet Alex: Our Case Study

Alex feels pretty good about their finances but has never actually sat down to run the numbers on a net worth statement. This exercise will provide a crystal-clear snapshot of their financial health, which is the first step toward making smarter, more intentional decisions.

First up, we’ll take a complete inventory of everything Alex owns. This needs to be a methodical and honest look based on current, real-world values.

Here’s a breakdown of Alex’s assets:

- Checking & Savings Accounts: A healthy emergency fund and checking balance, totaling $25,000.

- 401(k) Retirement Fund: Consistent contributions and market growth have brought the vested balance to $150,000.

- Taxable Brokerage Account: A mix of stocks and ETFs with a current market value of $45,000.

- Condo Market Value: Based on recent sales in the building and online estimators, Alex conservatively values the condo at $400,000.

- Car Value: According to Kelley Blue Book, the car’s current private-party sale value is $18,000.

Tallying it all up, Alex’s total assets come to $638,000. That number feels great on its own, but it’s only telling half the story. Now we need an equally honest look at the other side of the ledger.

Alex’s Complete Liability Picture

Next, Alex pulls up the latest statements for all outstanding debts to get the current principal balances. Getting the exact numbers here is crucial for accuracy.

- Mortgage Balance: After several years of payments, the remaining principal on the condo loan is $280,000.

- Student Loan Debt: The last remnant of college, with a remaining balance of $15,000.

- Car Loan: The outstanding loan on the vehicle is $8,000.

- Credit Card Balance: A small balance of $2,000 carried over from a recent trip.

Adding these up, Alex’s total liabilities amount to $305,000.

The magic happens when you bring both sides of the balance sheet together. It’s not just a math problem; it’s the moment of truth where your complete financial story is revealed in a single, powerful number.

Now for the simple, final calculation. We’ve laid out Alex’s financial snapshot below for clarity.

Alex’s Net Worth Calculation

| Item | Type (Asset/Liability) | Value | | :— | :— | :— | | Checking & Savings | Asset | $25,000 | | 401(k) Retirement | Asset | $150,000 | | Brokerage Account | Asset | $45,000 | | Condo Value | Asset | $400,000 | | Car Value | Asset | $18,000 | | Total Assets | | $638,000 | | Mortgage Balance | Liability | $280,000 | | Student Loan | Liability | $15,000 | | Car Loan | Liability | $8,000 | | Credit Card Balance | Liability | $2,000 | | Total Liabilities | | $305,000 | | Final Net Worth | (Assets - Liabilities) | $333,000 |

By subtracting total liabilities from total assets, Alex’s personal net worth is $333,000. This number is a tangible benchmark. Alex can now track it quarterly to see progress, set new financial goals, and stay motivated on the journey.

Two Paths to Your Own Calculation

Seeing Alex’s example makes it clear that you can do this, too. You have two great options for calculating your own net worth.

The first is the classic spreadsheet method. If you like having manual control and seeing every number laid out, a simple spreadsheet is perfect. You can create your own columns for assets and liabilities, update them periodically, and watch your net worth grow. For a head start, looking at a complete personal balance sheet example can provide a fantastic template to build from: https://popadex.com/personal-balance-sheet-example/

The second method is using a dedicated tool like PopaDex. An app automates this entire process. Instead of manually logging into every account, you can link them securely, and the platform will automatically pull your latest balances. This saves a ton of time and reduces the chance of human error, giving you a real-time view of your net worth with just a few clicks. It’s ideal for anyone who wants an effortless, always-up-to-date financial picture.

Making Your Net Worth Number Work for You

You’ve done the hard part—you’ve tracked down the statements, tallied the numbers, and done the simple math. Now you’re staring at a single figure. So, what’s next?

This number is way more than just a score. Think of it as a powerful diagnostic tool, the starting point for building a smarter financial future. The real value isn’t in the number itself but in what you decide to do with it from this day forward.

Turning Your Results Into Action

Your net worth is like a compass. It shows you exactly where you stand right now, which is the first step before you can chart a course to where you want to go—whether that’s retiring early, wiping out debt, or finally buying that dream home. The moves you make next are what will truly move the needle.

Your result is immediate, unfiltered feedback on your financial habits. A high net worth probably means your saving and investing strategies are on point. On the other hand, a negative or low number—super common for recent grads buried in student loans—simply shines a light on where you need to focus your energy.

No matter the outcome, the next step is building a plan. Here are a few ways to get started, depending on what your calculation revealed:

- If Liabilities Are Dragging You Down: Debt reduction becomes your top priority. You could try the snowball method (paying off the smallest debts first for quick wins and motivation) or the avalanche method (tackling high-interest debt first to save the most money). Every single dollar of debt you pay off is a direct boost to your net worth.

- If Your Assets Feel Stuck: It might be time to get your money working harder. Are you contributing enough to your retirement accounts to get the full employer match? Is your emergency fund just sitting there, or is it in a high-yield savings account earning some interest?

- If You Have a Solid Positive Net Worth: Now, the goal is to hit the accelerator. Look for ways to bump up your investment contributions, diversify your portfolio, or even explore new income streams. This is where you can really start to build serious momentum.

For a much deeper dive into specific tactics, check out our guide on how to increase your net worth with practical, step-by-step advice.

Your first net worth calculation is a baseline, not a final grade. The most important thing is the trend over time. A consistently rising net worth, even if it’s by a small amount each quarter, is a clear sign of financial progress.

Why You Need to Track It Regularly

Figuring out your personal net worth isn’t a one-and-done deal. To make it a genuinely useful tool, you need to track it consistently.

For most of us, a quarterly check-in is the sweet spot. It’s frequent enough to see your progress and stay motivated, but not so often that you get bogged down by the daily noise of market ups and downs.

Tracking regularly creates a powerful feedback loop. You’ll see exactly how your decisions—like finally paying off that credit card or bumping up your 401(k) contribution—affect your bottom line. Seeing that tangible evidence of progress is one of the best motivators out there.

Global trends also show why consistent tracking is so important, especially if you have international ties. Wealth migration is a massive global story, highlighting why it’s critical to calculate personal net worth with a worldwide view. Provisional data from Henley & Partners shows huge millionaire flows into markets like the UAE and the USA. For expats or gig workers with clients abroad, keeping track of cross-border assets is essential. Platforms like PopaDex make this easy, supporting over 30 countries and multi-currency accounts to help you spot opportunities in these global shifts.

Ultimately, your net worth statement is your personal financial roadmap. Use it to celebrate your wins, pinpoint areas for improvement, and guide every financial decision you make. This proactive approach is what transforms a simple number into a life-changing habit.

Common Mistakes That Throw Off Your Net Worth Calculation

When you calculate your personal net worth for the first time, it’s surprisingly easy to make small, honest mistakes that can throw off the final number. Think of this section as your troubleshooting guide—a checklist to help you sidestep the most common pitfalls so the figure you land on is one you can actually rely on.

Getting an accurate number isn’t about perfection; it’s about being methodical and realistic. These slip-ups are common but entirely avoidable with a little awareness.

Overestimating What Your Stuff is Really Worth

One of the most frequent errors is being a bit too optimistic about the value of personal belongings. That car you love might feel priceless to you, but its actual market value is what matters here. The same goes for your furniture, electronics, and even your home.

To keep your numbers grounded in reality, here’s how to do it:

- For your car: Don’t guess. Use a trusted source like Kelley Blue Book to find the private-party sale value. Be honest about its condition—dents, scratches, and mileage all count.

- For your home: A recent professional appraisal is the gold standard. For a quick check, online estimators like Zillow are fine, but be conservative. I’d even suggest knocking 5-10% off their estimate to account for market swings and selling costs.

- For other valuables: Unless you have professionally appraised art or jewelry, it’s often best to only include items worth over $1,000. Sadly, the sentimental value of your record collection doesn’t add to your bottom line.

Forgetting About the Small Debts

It’s tempting to only focus on the big-ticket liabilities like your mortgage and student loans, but those smaller debts can add up fast and quietly skew your calculation. A truly accurate net worth statement is exhaustive, leaving no stone unturned.

Take a moment to scan for these often-forgotten obligations:

- “Buy Now, Pay Later” plans from services like Afterpay or Klarna.

- Any outstanding medical or dental bills.

- Small personal loans from friends or family (yes, they count!).

- Unpaid tax balances, even if you’re on a payment plan.

Forgetting a $500 medical bill might not seem like a big deal, but these small omissions can lead to a dangerously inflated sense of financial health. When it comes to debt, precision is your best friend.

Your net worth calculation is only as strong as its weakest link. Overlooking even a single liability or overvaluing one asset can create a domino effect, leading to a final number that doesn’t reflect your true financial position.

Letting Emotions Dictate the Numbers

Let’s be real—calculating your net worth can be an emotional ride. Seeing a low or even negative number for the first time can be a gut punch, especially if you’re a recent graduate staring down a mountain of student debt. It’s crucial not to let these feelings get in the way.

A negative net worth isn’t a failing grade; it’s just your starting line. Plenty of successful people began in the red. The goal isn’t to judge the number but to establish a baseline. From there, you can focus on the trend over time, which is far more important than any single snapshot.

Similarly, try not to let daily market swings mess with your long-term perspective. Your investment portfolio might be down this week, but that’s just noise. When you calculate, use the current value, but remember to focus your energy on the long-term growth trajectory, not short-term volatility. This is where automated tools can really help, by giving you an unbiased, real-time picture of your finances without the emotional baggage.

Your Net Worth Questions, Answered

Once you start digging into the numbers, a few questions always seem to pop up. Let’s tackle them head-on so you can get a clear picture from the start and focus on what really matters: your own progress.

How Often Should I Calculate My Net Worth?

For most people, a quarterly check-in is the sweet spot. It’s frequent enough to track your progress and make smart adjustments, but not so often that you get bogged down by the daily noise of market ups and downs.

That said, if you’re in a high-intensity financial phase—like aggressively paying down debt or starting a much higher-paying job—switching to a monthly calculation can give you that extra dose of motivating feedback.

Is It Possible to Have a Negative Net Worth?

Yes, and it’s far more common than you’d think. A negative net worth simply means your total liabilities are greater than your total assets. This is a very typical starting point for recent graduates buried in student loans or new homeowners with a hefty mortgage.

Don’t look at a negative net worth as a failure. See it for what it is: your starting line. It’s the baseline you’ll use to measure all your future growth—and it can be a powerful motivator to start building wealth.

Should I Include My Car in My Assets?

Absolutely. Your car has a real market value, so it definitely belongs on your list of personal assets. For the most accurate number, look up its current private-party sale value on a trusted resource like Kelley Blue Book.

But here’s the crucial part: if you have a car loan, the outstanding balance must be listed under your liabilities. This simple step ensures you’re only counting the equity you actually have in the vehicle, not its full sticker price.

What’s a Good Net Worth for My Age?

You’ll see plenty of benchmarks and averages online, but honestly, they’re often more discouraging than helpful. A “good” net worth is simply one that is consistently moving in the right direction—upward. That’s the real sign of positive financial habits.

Focus on your own journey. Your career, where you live, and your family situation have a much bigger impact on your numbers than some generic national average. The only comparison that truly matters is you today versus you last quarter.

Free Net Worth Templates

Ready to calculate your personal net worth right now? Grab one of our free templates:

- Net Worth Statement Template — Formal balance-sheet format perfect for loan applications and financial reviews

- Net Worth Tracker for Google Sheets — Auto-updating dashboard with charts and trend tracking

- Net Worth Tracker for Excel — Offline spreadsheet with privacy-first design

Ready to stop guessing and start tracking? PopaDex gives you a real-time, accurate picture of your finances in one simple dashboard. Take control of your financial future today by visiting https://popadex.com.