Our Marketing Team at PopaDex

Cost of living in ireland: A Practical Guide to Ireland's Expenses

Let’s be upfront: Ireland isn’t cheap. A move to the Emerald Isle conjures images of rolling green hills and lively pubs, but you need to ground those dreams in financial reality. The cost of living is a significant factor, shaped by a booming economy, intense demand for housing, and a standard value-added tax (VAT) on almost everything you buy.

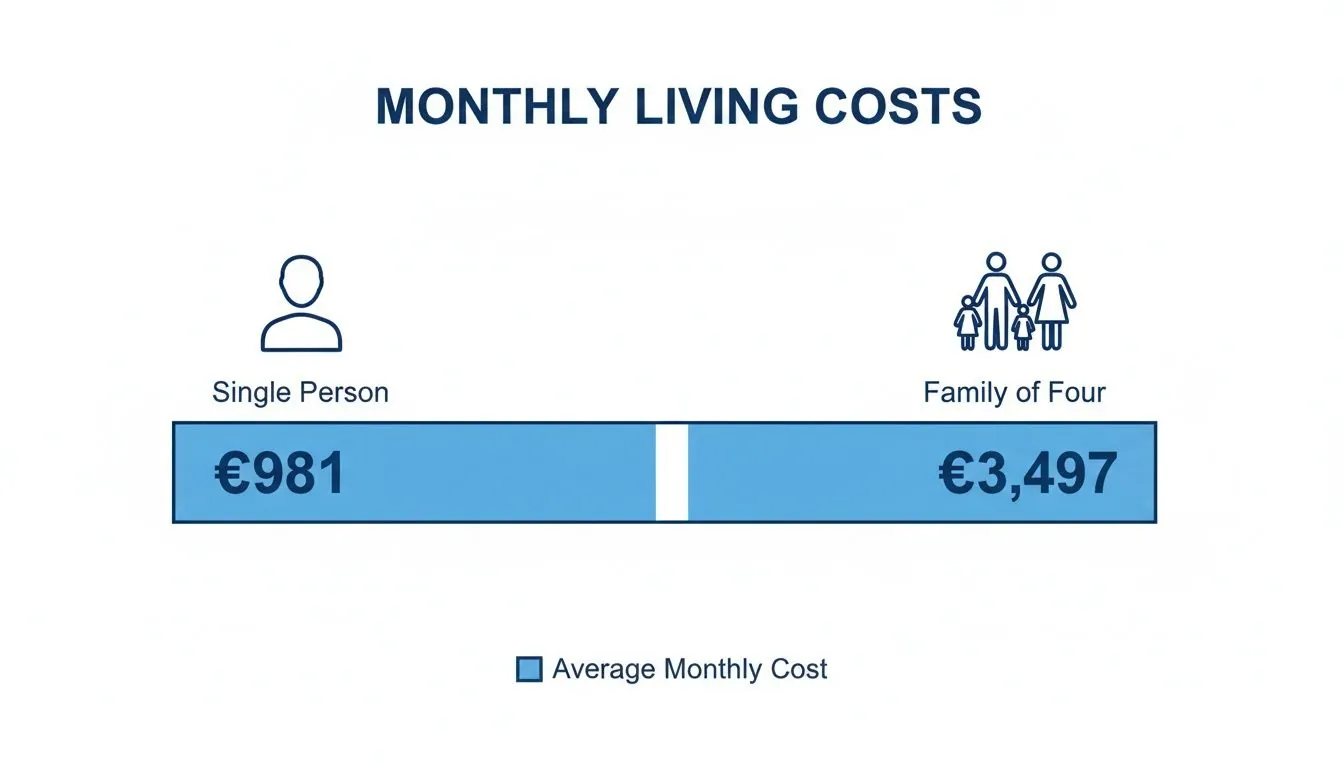

On average, a single person can expect to spend around €981 per month before rent. For a family of four, that number jumps to about €3,497, also excluding accommodation. These figures firmly place Ireland among the more expensive countries in Western Europe.

What It Really Costs to Live in Ireland

While Dublin often steals the spotlight with its premium prices, these nationwide averages give you a much better baseline. Of course, your personal spending habits will move the needle, but understanding these foundational costs is the first step toward building a budget that actually works.

Getting a handle on the day-to-day numbers is where the picture really comes into focus. Crowdsourced data shows us what real people—individuals and families—are spending every month just to live.

These estimates cover the essentials that make up your daily life:

- Groceries: Your weekly shop for food, drinks, and household supplies.

- Transportation: The cost of a monthly bus pass or running your own car.

- Utilities: Core services like electricity, heating, and internet (we’ll dive into this later).

- Leisure: The budget for dining out, grabbing a pint, and social activities.

Why Is Ireland So Expensive?

It comes down to a few key economic factors. Ireland’s robust economy is a magnet for multinational corporations and a skilled global workforce. This influx drives up demand for everything, especially housing, and supply just can’t keep up. The result? Higher prices across the board.

The real challenge for anyone moving to Ireland is balancing the high cost of living—particularly housing—with the incredible quality of life and career opportunities on offer. Nail down your budget early, and you’ll set yourself up for a smooth transition.

To give you a clearer idea, the table below breaks down these estimated monthly costs side-by-side, without factoring in rent just yet.

Estimated Monthly Living Costs in Ireland (Excluding Rent)

This table summarizes the average monthly expenses for a single person versus a family of four, covering the main spending categories you’ll need to budget for.

| Expense Category | Single Person (EUR) | Family of Four (EUR) |

|---|---|---|

| Food & Groceries | €300 - €400 | €800 - €1,200 |

| Local Transport | €100 - €150 | €250 - €400 |

| Utilities (Basic) | €150 - €250 | €250 - €400 |

| Leisure & Dining | €250 - €400 | €500 - €700 |

| Total Estimated | ~€981 | ~€3,497 |

As you can see, the costs add up quickly, especially for families. These numbers provide a realistic starting point for planning your move and managing your financial expectations.

Navigating the Irish Housing and Rental Market

Let’s get straight to it: for anyone moving to Ireland, finding a place to live will be your single biggest financial headache. The Irish housing market, especially for rentals, is intensely competitive. A booming economy and a steady stream of professionals have cranked up demand, but the supply of homes just hasn’t kept pace.

This mismatch has sent prices soaring, particularly in the big cities. In Dublin, for instance, a one-bedroom apartment in the city centre can easily sail past €2,000 a month. Need a three-bedroom for the family? You’re often looking at over €3,500. While the overall cost of living in Ireland gets a lot of attention, housing is what truly drives that reputation.

Rental Costs Across Key Cities

Dublin might set the price ceiling, but other cities aren’t exactly cheap. Cork and Galway have their own thriving job markets, and rental prices there reflect that reality. You’ll find things a little less expensive than in the capital, but the competition for good places is just as fierce.

To give you a ballpark idea, here’s what you might expect to pay for a one-bedroom flat in the city centre:

- Dublin: €1,900 - €2,400+ per month

- Cork: €1,500 - €2,100 per month

- Galway: €1,400 - €2,000 per month

- Limerick: €1,300 - €1,800 per month

You can find some relief by looking at suburbs or commuter towns, but be sure to weigh any savings against the added cost and time of your daily commute.

The numbers below show the baseline living costs before you even factor in rent, highlighting the difference between a single person and a family.

As you can see, a family of four’s non-rent expenses are already about 3.5 times higher than a single person’s. Once you throw a three-bedroom apartment into that budget, the gap becomes enormous.

This brings up a crucial question you’ll need to tackle: whether it’s cheaper to rent or buy a home. Buying requires a hefty upfront investment, but it can provide some much-needed stability in a volatile rental market. If that’s a route you’re considering, a good first step is to figure out what you’d need to save and calculate your potential down payment on a house.

Looking Beyond the Monthly Rent

Your housing budget isn’t just about the rent. There are a handful of other essential bills that will land on your doorstep every month or two.

Key Insight: A classic budgeting mistake is underestimating utilities and other housing fees. These “hidden” costs can easily add a few hundred euros to your monthly spend, so it’s critical to factor them in from day one.

Here are the other costs you need to plan for:

- Electricity and Gas: These are usually billed every two months and can run anywhere from €150 to over €300, depending on the season, your usage, and how well-insulated your home is.

- Internet and TV: A decent broadband package will set you back about €50 - €70 per month.

- Waste Collection: Often called “bin charges,” this service is privatized in many areas and typically costs between €20 - €30 a month.

- TV Licence: This one catches a lot of people by surprise. If you have any device that can receive a TV signal (and yes, that includes a laptop or phone you use to watch live TV), you are legally required to pay an annual €160 TV licence fee.

These extras are non-negotiable and need to be treated as a core part of your housing expenses. Be persistent, have your documents ready to go, and be prepared to move quickly when you find a place you like. This market waits for no one.

Budgeting for Daily Life: Groceries and Transport

Once you’ve sorted out the big fixed costs like rent, your day-to-day choices are what will truly shape your budget. These variable expenses—groceries, getting around, your social life—are where you have the most control. Getting a handle on these is the real secret to managing the cost of living in Ireland without feeling like you’re pinching every penny.

After housing, your grocery bill will almost certainly be your next biggest monthly expense. A single person can expect to spend anywhere from €70 to €100 on a weekly shop, while a family of four should probably budget between €150 and €250 per week. Of course, these numbers swing wildly depending on where you shop and what you’re putting in your basket.

Luckily, the supermarket scene in Ireland is fiercely competitive, which is great news for your wallet. You’ve got a solid range of options from budget-friendly discounters to more premium grocers.

- Aldi & Lidl: These German giants are the undisputed champions of value. They focus on high-quality own-brand products at prices that consistently undercut the competition, making them a staple for anyone looking to keep costs down.

- Tesco & Dunnes Stores: As Ireland’s largest supermarket chains, they offer a massive selection of branded goods, specialty foods, and full-service counters for meat and fish. While their prices can be higher, they constantly run promotions and have loyalty schemes that offer serious savings if you shop smart.

Getting Around: The Cost of Irish Transport

How you choose to commute will have a huge impact on your monthly spend. You really have two main paths: relying on public transport or owning a car. Each comes with its own set of costs and benefits.

Public transport is almost always the more affordable option, particularly in cities. In Dublin, for instance, you can use a Leap Card (Ireland’s travel card) which has fare caps to ensure you never overspend. The short-hop weekly cap in Dublin is around €24, making it a predictable and manageable expense.

Owning a car, on the other hand, opens up a whole new world of expenses. It’s not just the purchase price you have to think about. You’ll also need to budget for:

- Fuel: Petrol prices are consistently high, often hovering between €1.70 - €1.90 per litre.

- Insurance: This is a big one. Car insurance in Ireland is notoriously expensive, especially for expats without a local driving history. Annual premiums can easily top €1,000, even for safe drivers.

- NCT (National Car Test): A mandatory roadworthiness test for cars over four years old, costing €55 every one or two years.

- Motor Tax: An annual tax based on your car’s emissions, which can run anywhere from €120 to over €2,000.

For most people living in a city, the convenience of a car just doesn’t justify the hefty price tag. A smarter financial move is often to combine public transport with the occasional car rental or ride-share for those times you really need wheels.

The Price of a Social Life and Leisure

Finally, a budget isn’t just about covering the essentials—it’s about being able to enjoy your new home. The cost of entertainment in Ireland can add up, but this is another area where a little planning goes a long way.

A pint of Guinness in a Dublin pub will set you back €6.50 - €8.00, while a casual dinner for two at a restaurant will likely run €60 - €90. A movie ticket is usually €12 - €15, and a monthly gym membership can range from €40 to €70.

These costs are all part of the experience of living in Ireland. By factoring them into your budget from the get-go, you can soak up the culture without any financial stress. It’s all about finding that sweet spot between your spending on groceries, transport, and leisure to build a budget that lets you live comfortably and have a good time.

Understanding Your Salary and Take-Home Pay

Getting a job offer with a big, juicy salary figure feels fantastic. But that number on your contract isn’t what actually lands in your bank account each month. To really get a handle on the cost of living in Ireland, you have to look past the headline number and understand your take-home pay—the money you actually have left after the government has taken its share.

Think of your gross salary as a whole pizza. Before you can even take a bite, a few slices are automatically set aside for taxes and social insurance. What’s left on your plate is your net pay, the cash you can genuinely work with.

Luckily, for most employees in Ireland, this all happens seamlessly through the PAYE (Pay As You Earn) system. Your employer does the heavy lifting, calculating and deducting what you owe straight from your paycheck. This means no nasty surprises or massive tax bills waiting for you at the end of the year.

The Three Key Deductions from Your Paycheck

Your first Irish payslip might look a bit intimidating, but the deductions almost always boil down to three main things. Getting your head around these is the first step to building a budget that actually works.

-

PAYE (Pay As You Earn): This is your main income tax. It’s a progressive system, which just means the more you earn, the higher the percentage you pay. Ireland has two tax bands: a standard rate of 20% on income up to a certain cutoff, and a higher rate of 40% on everything you earn above that threshold.

-

USC (Universal Social Charge): This is another tax on your income, calculated separately from PAYE. The rates are much lower, but it’s something nearly everyone has to pay. Think of it as a contribution towards funding public services.

-

PRSI (Pay Related Social Insurance): This one isn’t technically a tax; it’s a social insurance contribution. Your PRSI payments fund social welfare benefits like unemployment support, illness benefit, and the state pension.

These three deductions are what separate your gross salary from your real take-home pay. It’s a significant chunk, so never, ever base your budget on that pre-tax figure. This is especially true when you consider how much prices have risen over the long term. Between January 1973 and January 2023, the price of goods and services shot up by an eye-watering 1,073%, making every euro of take-home pay that much more critical. You can read more about these historical price changes on the CSO website.

From Net Pay to Disposable Income

Once you know your net pay, there’s one more crucial step: figuring out your disposable income. This is the money you have left after paying for all your non-negotiable essentials—think rent, utilities, groceries, and transport. This is the fun money, the money you have true freedom with for saving, investing, hobbies, or travel.

Disposable income is the ultimate measure of your financial health. It’s not about how much you earn, but how much you have left after your essential life costs are covered. This is the figure that dictates your lifestyle.

This calculator shows how you can plug in your net income and fixed expenses to see exactly what’s left for you each month.

Seeing this number laid out clearly helps you make smarter choices. Can you really afford that nicer apartment, or should you cut back on eating out for a while? For a bit more perspective, you can use our salary comparison tool to see how Irish salaries stack up against other countries, giving you valuable context for your earning potential.

Comparing Living Costs Across Major Irish Cities

Let’s get one thing straight: the cost of living in Ireland isn’t a single number. It’s a story written by your postcode, and the city you choose will have the single biggest impact on your monthly budget. While national averages are a decent starting point, they don’t paint the full picture.

Think of Dublin as the financial epicentre. It’s the capital, the economic engine, and it sets the benchmark for prices—a very high benchmark. Its gravity pulls in the highest salaries but also demands the steepest prices for everything from a one-bedroom flat to a pint of Guinness.

But once you look beyond the capital, a totally different financial landscape emerges. Cities like Cork, Galway, and Limerick offer a compelling alternative, delivering a vibrant urban life without the eye-watering price tag. For many, the trade-off is more than worth it.

Dublin: The Financial Benchmark

Life in Dublin comes at a premium, and there’s no getting around it. Rent is the monster in the room, with prices easily 20-30% higher than in any other major city. That one-bedroom apartment costing €2,100 a month in Dublin? It might be closer to €1,600 down in Cork. That difference alone reshapes your entire budget.

Beyond housing, the day-to-day grind just costs more in Dublin. Public transport, groceries, and a night out with friends will all take a bigger bite out of your wallet. While the job opportunities are fantastic, especially in tech and finance, you have to ask yourself if the bigger salary truly makes up for the inflated costs.

The real question isn’t just “Can I afford Dublin?” but “What kind of lifestyle could I afford elsewhere for the same money?” More often than not, the answer points toward a much better quality of life outside the capital.

Cork, Galway, and Limerick: The Value Proposition

Cork, Ireland’s second-largest city, is a fantastic alternative. It boasts a bustling food scene and a strong base in the pharmaceutical and tech industries, all with living costs that are noticeably lower than Dublin’s. This balance makes it a top choice for anyone seeking big-city amenities on a more manageable budget.

Galway, with its bohemian vibe and world-famous arts scene, offers a similar deal. It’s a major tourist destination, which can push up some prices, but the overall cost of living remains well below Dublin’s. Meanwhile, Limerick has really come into its own as an affordable and attractive hub, especially for students and young professionals.

Cost of Living Index Dublin vs Other Irish Cities

To put this all into perspective, let’s look at the numbers. The table below uses a simple index where Dublin is the baseline at 100. It shows just how much further your euro can stretch once you leave the capital.

| City | Overall Cost Index (vs Dublin) | Rent Index (vs Dublin) | Groceries Index (vs Dublin) |

|---|---|---|---|

| Dublin | 100 | 100 | 100 |

| Cork | 88.5 | 74.1 | 96.2 |

| Galway | 89.2 | 78.5 | 98.1 |

| Limerick | 82.3 | 65.8 | 93.5 |

The data speaks for itself. Choosing Limerick over Dublin could slash your rent by nearly 35%, instantly freeing up a huge chunk of your disposable income. This kind of analysis is crucial for finding a city that aligns with both your career goals and your financial well-being.

Smart Financial Planning for Your Move to Ireland

Moving to a new country is so much more than just packing boxes and booking flights. It demands a solid financial game plan, especially when your destination is Ireland, where the cost of living can be a real eye-opener. Getting your money sorted from day one will save you a world of headaches later on.

One of your first jobs on the ground will be getting a Personal Public Service (PPS) number. You’ll need it for just about everything, from starting a job to accessing public services. With your PPS number in hand, your next stop should be the bank. Opening an Irish bank account is non-negotiable for getting paid, setting up bills, and handling daily life in euros without getting hammered by conversion fees.

Getting Your Financial House in Order

For expats, life gets a little more complicated when you’re juggling finances in different currencies and countries. It’s surprisingly easy to lose track of the big picture when your assets are scattered all over the place. That’s why getting a single, consolidated view of your global net worth isn’t just a “nice-to-have”—it’s absolutely essential for making smart decisions.

Understanding your complete financial picture helps you budget with real numbers and set achievable long-term goals. A big piece of this initial planning puzzle is the move itself, which includes things like successfully choosing an international removal company. Don’t forget to factor these upfront costs into your starting budget.

Maintaining a clear overview of your total assets and liabilities, regardless of currency or location, is the bedrock of sound financial management for any expatriate. This clarity empowers you to navigate Ireland’s high-cost environment with confidence.

Tracking Your Global Assets and Net Worth

This is where modern tools can be a lifesaver. Platforms that pull all your financial accounts together—from your new Irish bank account to your investment portfolio back home—are incredibly powerful. They give you a real-time dashboard of your entire financial life, making it much simpler to see if you’re hitting your targets.

A consolidated dashboard like this lets you watch your net worth grow, giving you a clear, tangible measure of your progress. It takes a jumble of abstract numbers from different banks and currencies and turns them into a single, actionable snapshot. Our own guide on financial planning for expats dives deeper into strategies for managing all of this.

Practical Tips for Reducing Your Costs

Living well in Ireland doesn’t have to mean draining your bank account. A few smart adjustments to your daily habits can make a huge difference to your monthly budget.

- Shop Smart for Groceries: Make the discount supermarkets like Aldi and Lidl your first stop for the weekly shop. Their prices are consistently lower than the big players like Tesco and Dunnes Stores.

- Master Public Transport: If you’re in a city, a Leap Card with fare capping is almost always a smarter financial move than owning a car. The sky-high costs of fuel, insurance, and motor tax make car ownership a serious financial commitment here.

- Review Your Utility Bills: Don’t just accept the utility providers you inherit with your new place. Hop on a comparison website once a year to see if you can find better deals on electricity, gas, and broadband.

Let’s be clear: Ireland is an expensive place to live. World Bank data shows that Ireland’s cost of living index is about 76% higher than the global average—a stat that really drives home the need for a sharp budget. You can explore more insights into global living costs on TheGlobalEconomy.com. By building these smart financial habits from the start, you can set yourself up for a secure and brilliant life on the Emerald Isle.

Common Questions About Ireland’s Cost of Living

Moving to a new country always comes with a lot of financial questions. Let’s tackle some of the most common ones people ask when figuring out the cost of living in Ireland.

What’s a Good Salary to Live Comfortably in Ireland?

This is the big one, and honestly, the answer depends entirely on your lifestyle and where you plant your roots.

If you’re single and living outside of Dublin, you should be aiming for a salary of at least €45,000 to €50,000. That should comfortably cover your rent, bills, and day-to-day spending, with a bit left over for savings and a social life.

Thinking of living in Dublin? You’ll need to adjust your expectations. For a comfortable life in the capital, you’re looking at a salary closer to €60,000 or more. For a family of four, the numbers jump significantly. A household income of €75,000 to €85,000 is a realistic target for most of the country, but that figure can easily climb past €100,000 in the Greater Dublin Area.

Is Ireland More Expensive Than the UK?

In a word, yes. While you might find higher salaries in certain industries here, the day-to-day costs, especially for housing, are generally steeper in Ireland compared to the UK.

On average, consumer prices (including rent) are about 15-20% higher in Ireland than in the UK. The real shock often comes from the rental market—Dublin prices can be a staggering 40-50% higher than in major UK cities, London excluded. Groceries, transport, and a pint at the pub also tend to cost a bit more.

How Can You Reduce Housing Costs in Ireland?

Accommodation will almost certainly be your biggest monthly expense, so any savings you can make here will have a huge impact on your overall budget. Here are a few practical tips that actually work:

- Look Beyond the City Centre: Don’t underestimate the commuter towns. Rents in suburbs and surrounding towns are significantly lower than in the city cores, and the savings often more than cover the cost of a monthly transport pass.

- Consider a House Share: Renting a room in a shared house or apartment is incredibly common, especially for singles and young professionals. It’s a fantastic way to slash your rent and utility bills in one go.

- Be Ready to Negotiate: The market is tough, but negotiation isn’t always off the table. If you can offer to sign a longer lease—say, two years instead of one—some landlords might be open to a better deal.

- Move Fast: Good value properties disappear in a flash. Have your deposit, references, and all your paperwork lined up and ready to go. When you find a place you like, you need to be able to act immediately.

Thriving in Ireland means getting a firm handle on your finances. With a tool like PopaDex, you can see all your assets and liabilities in one simple dashboard. It gives you a crystal-clear view of your net worth, helping you build a budget with real confidence.

Ready to take control? Visit PopaDex and get started for free.