Our Marketing Team at PopaDex

Creating a Financial Plan That Actually Works

Let’s be real—the term “financial plan” sounds stiff and intimidating. It conjures up images of complicated spreadsheets, strict rules, and giving up everything you enjoy. But a good financial plan isn’t about restriction. It’s about freedom.

Think of it as a personal roadmap for your money, guiding every decision from your morning coffee to your biggest life goals. It’s the tool that turns vague dreams like “retire early” or “buy a house” into concrete, achievable steps.

Your Foundation For Financial Clarity

The whole point of a financial plan is to build a bridge from where you are today to where you want to be tomorrow. It’s not about cutting out lattes; it’s about making sure your spending aligns with what you actually value.

Ultimately, creating a financial plan is about making conscious choices. It gives you permission to spend on the things that bring you joy while simultaneously building a safety net and investing for your future self. It swaps financial anxiety for confidence and control.

The Four Pillars of Your Financial Plan

A truly solid financial plan doesn’t just happen. It’s built on four essential pillars that work together to create a stable and resilient financial life. By addressing each of these areas, you ensure a balanced approach that covers both your immediate needs and your long-term ambitions.

Let’s break down what these pillars are and why each one is so critical for your success.

| Pillar | What It Covers | Why It Matters for You |

|---|---|---|

| Goal Setting | Defining your short, mid, and long-term financial ambitions. This is your “why.” | Gives you the motivation and clear direction needed to stick with your plan, especially when things get tough. |

| Cash Flow Management | Tracking what money comes in and where it goes out each month. | This is the engine of your plan. Without knowing your cash flow, you can’t make effective decisions. |

| Debt Strategy | Creating a clear path to reduce what you owe, from credit cards to student loans. | Frees up your income so it can be used for building wealth instead of just paying interest. |

| Investment & Growth | Putting your money to work to build wealth over the long term. | This is how you’ll fund major goals like retirement, your kids’ education, or financial independence. |

Each pillar supports the others. You can’t effectively invest if you don’t have your cash flow under control, and you can’t pay down debt efficiently without clear goals. They all have to work in harmony.

A financial plan is a living document, not a set of rigid rules carved in stone. It should adapt as your life changes, providing guidance through every new chapter—whether it’s a career shift, a growing family, or a change in your long-term goals.

Why This Foundation Matters So Much

Without this foundational structure, you’re essentially flying blind with your money. You might be saving, but are you saving enough? You might be paying down debt, but are you doing it in the most efficient way? A plan replaces that guesswork with data-driven confidence.

The good news is that more and more people are taking this seriously. As of Q1 2025, global financial health scores have stabilized, with significant improvements seen in financial learning and planning. People are actively educating themselves, which is the first and most crucial step toward long-term security.

If you’re just starting out and this feels like a lot, don’t worry. Our guide on financial planning for beginners is the perfect place to get your bearings.

For those ready to dive deeper into investment concepts and strategies, resources like VTrader’s Academy can be incredibly helpful. They do a great job of demystifying complex topics, making the entire process feel far more approachable.

Defining What You Truly Want from Your Money

Let’s be honest: a financial plan without clear goals is just a bunch of numbers on a page. It’s like having a map but no idea where you’re going. This is where we get to the heart of it—moving beyond vague wishes like “I want to be rich” and defining what you really want your money to accomplish for you.

Your goals are the ‘why’ behind every financial move you make. To get there, we need to sort your ambitions into different buckets. A solid plan always balances what you need right now with what you dream of for the future. I find it helps to think in three distinct timeframes.

Sorting Your Goals by Time Horizon

First up, your short-term goals. These are the financial wins you want to lock down in the next year or two. Think of them as the foundation for your financial security—the things that help you sleep better at night.

Common short-term goals include:

- Building an emergency fund: The classic safety net. Aim for 3-6 months of essential living expenses to handle a sudden job loss or medical scare without panic.

- Wiping out high-interest debt: This means targeting credit cards or personal loans that are actively draining your wealth.

- Saving for a specific large purchase: This could be anything from a new laptop for your side hustle to a well-deserved vacation.

Next, we have mid-term goals. These usually have a timeline of three to ten years. These are the major life milestones that need a bit more capital and a lot more consistency to achieve.

Examples I see all the time:

- Saving for a house down payment: A huge milestone that demands a dedicated, long-term savings habit.

- Funding a wedding or another major family event: Planning for a big one-time expense without derailing your entire financial life.

- Starting a business: Scrimping and saving to get the seed money you need to finally launch your own venture.

Finally, we arrive at your long-term goals. These are the big-picture dreams, often more than a decade away. For most people, retirement is the big one. These goals are all about harnessing the power of compounding with a patient, disciplined approach to investing.

A study of wealth management firm leaders found that a top challenge is getting clients to connect their daily financial actions to their distant, long-term outcomes. Defining your goals clearly from the very start is what closes that gap.

Making Your Goals S.M.A.R.T.

Once you’ve sorted your goals, it’s time to make them real. Vague dreams are inspiring, but they’re impossible to act on. This is where the S.M.A.R.T. goal framework comes in—it turns those fuzzy aspirations into a concrete blueprint.

Here’s how it works:

- Specific: Don’t just “save for a car.” Instead, say “save for a $5,000 down payment on a used Honda CR-V.” See the difference?

- Measurable: The goal needs a number. $5,000 is a clear target you can actually track.

- Achievable: Be realistic. Can you actually hit this goal with your current income and expenses? Saving $5,000 in one month on a $3,000 income is a fantasy. Saving it over 18 months? That might just work.

- Relevant: Does this goal even fit into your larger life vision? Sure, a sports car sounds fun, but does it help you reach your primary goal of retiring early? Maybe, maybe not.

- Time-bound: Give yourself a deadline. “I will save $5,000 for the down payment within the next 18 months.”

This structure gets rid of all the ambiguity. It gives you a clear finish line and a timeframe, which makes building the right strategy so much easier.

Real-World Goal Setting Scenarios

Let’s look at how this plays out for real people.

Scenario 1: The Freelancer A freelance graphic designer deals with fluctuating income. Her number one priority is stability.

- Vague Goal: “I want to feel less stressed about money.”

- S.M.A.R.T. Goal: “I will save $12,000 (4 months of my average expenses) in a high-yield savings account for my emergency fund within the next 24 months.” This is specific, measurable, achievable, directly relevant to her stress, and time-bound.

Scenario 2: The Growing Family A couple with a young child knows they need to think about education costs.

- Vague Goal: “We need to save for college.”

- S.M.A.R.T. Goal: “We will open a 529 plan and contribute $300 per month, with the goal of having $75,000 saved by the time our child turns 18.” This defines the action, the amount, and the deadline.

When you take the time to really define and sharpen what you want, your financial plan stops being a boring budgeting chore. It becomes the most powerful tool you have for building the exact life you envision.

Getting an Honest Look at Your Financial Health

Before you can build a roadmap to your future, you need to know exactly where you’re standing right now. This means taking a clear-eyed, no-judgment look at your complete financial picture. Think of it as plugging your current coordinates into a GPS before starting a long trip.

This isn’t about feeling guilty over past spending or getting bogged down by a wall of numbers. It’s simply about gathering facts. The real goal is empowerment—arming yourself with the data you need to make smart, forward-thinking decisions. We’ll break this down into two key pieces: your financial snapshot (net worth) and your financial motion (cash flow).

Calculating Your Financial Snapshot

Your net worth is the ultimate bottom-line number for your financial health. It’s a simple yet powerful calculation that shows what you would have left if you sold everything you own and paid off every single debt.

The formula is as straightforward as they come: Assets - Liabilities = Net Worth.

- Assets are everything you own that holds monetary value. This includes the cash in your bank accounts, the current value of your investments, your home’s market value, and even the resale value of your car.

- Liabilities cover everything you owe to others. Think mortgage balances, student loans, credit card debt, car loans, and any other personal loans you might have.

Let’s say you have $15,000 in savings and investments, plus a car worth $10,000. On the flip side, you owe $8,000 on that car and $2,000 on a credit card. Your net worth is a clean $15,000. Getting this number is a crucial first step.

Your net worth is more than just a number; it’s a progress report. Tracking it over time is one of the most effective ways to see if your financial strategies are actually working. A rising net worth means you’re successfully building wealth.

When you’re getting an honest look at your financial health, it’s critical to account for all liabilities, including any existing tax obligations like back taxes. Neglecting them can throw off your entire picture. For guidance on navigating these issues, a resource like this guide on Expert Help with Back Taxes: Your IRS Relief Guide can be incredibly helpful.

Uncovering Your Real Cash Flow

If net worth is your financial snapshot, then cash flow is the movie. It shows where your money comes from and, more importantly, where it goes each month. This is where you uncover the habits and patterns that are either helping or hindering your progress.

For many people I’ve worked with, this is the most eye-opening part of the entire process. You think you know where your money is going, but the data often tells a completely different story. The goal isn’t to shame yourself for buying coffee; it’s to spot the significant spending leaks you weren’t even aware of.

To get started, you’ll need to track every dollar for at least one month, though three months gives a much more accurate picture. Manually sifting through bank and credit card statements works, but apps like PopaDex can automate the heavy lifting by categorizing your spending for you.

Essential Financial Metrics to Track

Once you have the raw data, you can calculate a few key metrics. These numbers provide a much deeper understanding of your financial situation and are essential for building a strategy that actually works for you.

Here are a few of the most important ones to keep an eye on.

Essential Financial Metrics to Track

This table outlines key personal finance metrics, how to calculate them, and what they reveal about your financial health.

| Metric | How to Calculate It | What It Tells You |

|---|---|---|

| Savings Rate | (Total Monthly Savings / Gross Monthly Income) x 100 | This shows what percentage of your income you’re setting aside for the future. A higher rate accelerates your progress. |

| Debt-to-Income (DTI) Ratio | (Total Monthly Debt Payments / Gross Monthly Income) x 100 | Lenders use this to gauge your ability to take on new debt. A high DTI can signal financial stress. |

| Emergency Fund Coverage | Total Emergency Savings / Monthly Essential Expenses | This reveals how many months you could survive financially without any income. Aim for 3-6 months as a baseline. |

These metrics move you from guessing to knowing. Instead of vaguely feeling like you “spend too much,” you can see that your “dining out” category is 15% of your take-home pay. This clarity is what makes financial planning so powerful—it replaces emotion with objective facts, giving you a solid foundation to build upon.

Building Your Personalized Financial Strategy

This is where the real work—and the real fun—begins. You’ve laid the groundwork by defining your goals and getting honest about your numbers. Now, it’s time to connect the dots and build a financial strategy that feels less like a restriction and more like a roadmap.

The goal here is to create a blueprint that’s both actionable and adaptable. It’s about turning your big ambitions into a practical, day-to-day, month-to-month plan. Forget rigid, one-size-fits-all rules. We’re looking for a system that clicks with your lifestyle and personality, because if a method feels like a chore, you simply won’t stick with it. Sustainability is the name of the game, not perfection.

Choosing Your Budgeting Style

Let’s be clear: a budget is just a tool for telling your money where to go, instead of scratching your head and wondering where it all went. But not all budgeting methods are created equal, and what works for your friend might not work for you. Think of it like finding the right workout routine—the best one is always the one you’ll actually do consistently.

Here are a few popular approaches to get you started:

- The 50/30/20 Rule: This is a fantastic starting point if you love simplicity. You allocate 50% of your after-tax income to Needs (rent, groceries, utilities), 30% to Wants (hobbies, dining out), and 20% to Savings and Debt Repayment. It gives you clear guardrails without making you track every single dollar.

- Zero-Based Budgeting: For those who crave more control and precision, this method is a game-changer. Every single dollar of your income gets a specific job, whether it’s for bills, savings, or spending. When you’re done, your income minus your expenses equals zero. It sounds intense, but tools like PopaDex can automate the tracking and make it surprisingly manageable.

- Pay-Yourself-First Method: This is the ultimate “set it and forget it” strategy. Before you pay a single bill or buy your morning coffee, you automatically transfer a predetermined amount of money to your savings and investment accounts. The rest is yours to manage however you see fit.

Want to dig deeper? Our guide on https://popadex.com/mastering-budgeting-a-path-to-financial-freedom/ can help you find the perfect match. Remember, this isn’t about restriction; it’s about being intentional with your money.

Crafting a Debt Repayment Plan

High-interest debt is like an anchor dragging on your financial progress. Every dollar you pay in interest is a dollar that isn’t working for you and your future. A clear, actionable plan to eliminate that debt is more than a good idea—it’s a non-negotiable part of any solid financial strategy.

The two most common (and effective) methods are the Debt Snowball and the Debt Avalanche.

- The Debt Snowball: You start by listing your debts from the smallest balance to the largest. Make minimum payments on everything, but throw every extra dollar you can find at that smallest debt. Once it’s gone, you take the money you were paying on it and “roll” it onto the next-smallest debt. The quick wins are incredibly motivating and build powerful momentum.

- The Debt Avalanche: This approach is all about math. You prioritize debts by their interest rate, from highest to lowest. You’ll make minimum payments on all of them but focus all your extra cash on the debt with the highest interest rate. This strategy will save you the most money in interest over time.

The best debt repayment plan is the one you will actually follow. If the psychological boost from quick victories keeps you motivated, the Snowball is your best bet. If saving the maximum amount on interest is your top priority, go with the Avalanche.

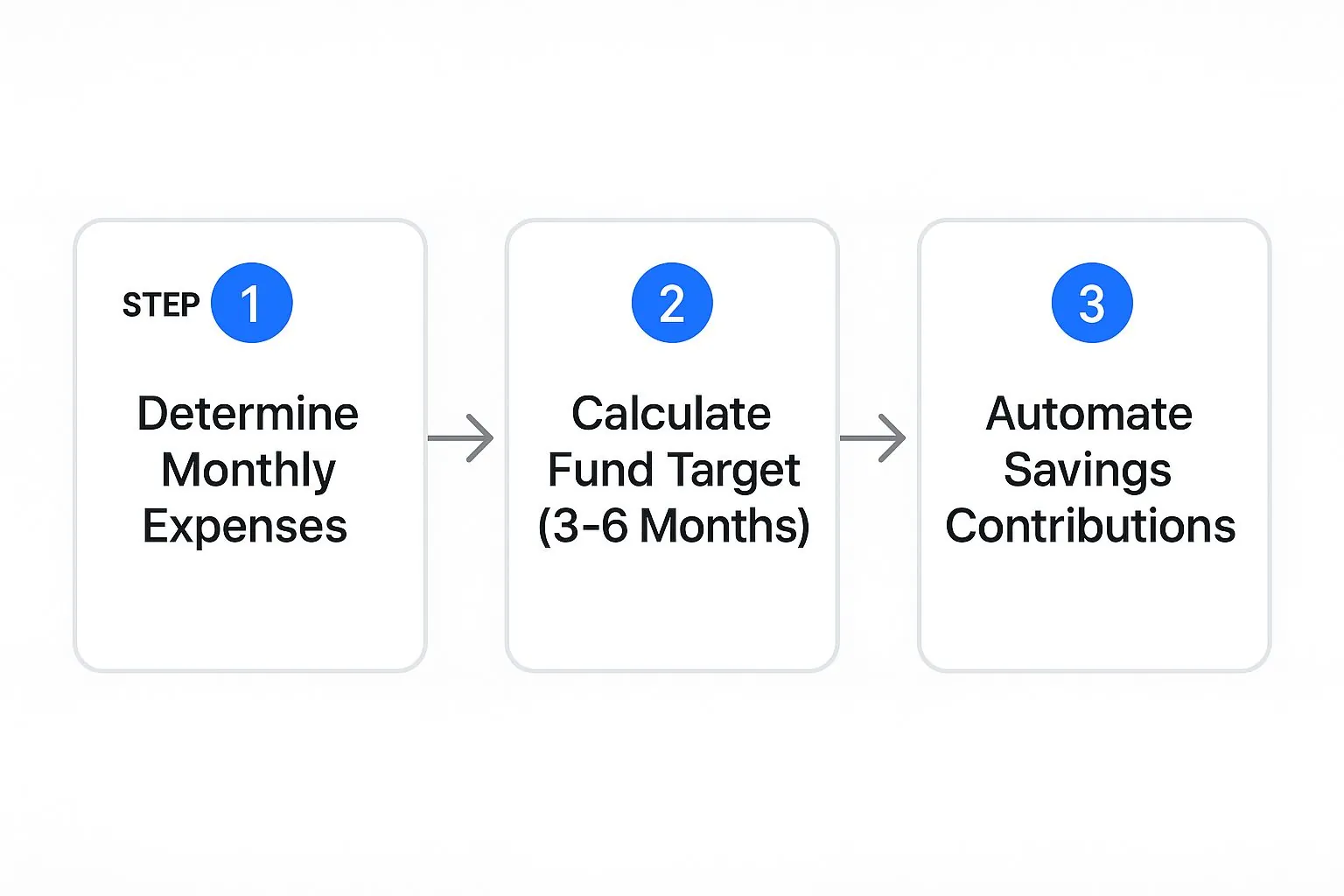

Prioritizing Your Emergency Fund

Think of your emergency fund as the firewall between you and a financial crisis. It’s the cash cushion that keeps an unexpected car repair or surprise medical bill from derailing your goals and forcing you into debt. This needs to be your #1 savings priority before you even think about aggressive investing.

This infographic breaks down just how simple building one can be.

The biggest takeaway here is that automation is your best friend. Setting up automatic transfers ensures your fund grows steadily without you having to think about it.

This kind of planning has never been more vital. The demand for expert guidance is surging, with the number of certified financial planners (CFPs) expected to hit 230,000 globally in 2025—a 3.1% jump from the previous year. Once your emergency fund is secure, the next logical step is learning about managing investment risk to make sure your hard-earned money is protected as it grows.

Putting Your Plan into Motion and Staying on Track

A perfectly crafted financial strategy is just a collection of good intentions until you bring it to life. This is where the real work—and the real progress—begins. In my experience, the single most effective habit for making sure you follow through is automation.

Honestly, it’s the secret weapon for building wealth without relying on sheer willpower day in and day out.

The concept is brilliantly simple: you tell your money where to go before you even have a chance to spend it. By setting up automatic transfers from your checking account to your savings, retirement, and investment accounts, you’re putting your future self first. It ensures your most important goals get funded like clockwork, right after each paycheck hits.

Automating Your Financial Progress

Think of automation as setting up financial guardrails for yourself. You’re intentionally designing a system where your goals get the first slice of your income, and the rest of your spending has to fit into what’s left. This simple trick sidesteps the decision fatigue that so often leads to putting things off.

Here’s a practical way to get started:

- Fund Your Emergency Savings: Set up a recurring transfer to your high-yield savings account scheduled for the day after every payday. Even a small, consistent amount builds up surprisingly fast.

- Boost Your Retirement Contributions: If you have a workplace plan like a 401(k), your contributions are likely already automated from your paycheck. For an IRA, you can easily set up an automatic investment from your bank account.

- Invest for Mid-Term Goals: For goals like a house down payment or a new car, open a separate brokerage or high-yield savings account. Automate transfers to it and give the account a motivating name, like “Future Home Fund.” It makes the goal feel more tangible.

This “pay yourself first” approach is the backbone of every successful long-term financial plan I’ve ever seen. It’s a small, one-time setup that delivers incredible value for years.

The goal goes beyond making progress, but to make progress inevitable. By automating your key financial actions, you remove friction and make saving and investing your default behavior, not an afterthought.

Establishing a Rhythm for Review

Your financial plan isn’t a “set it and forget it” document. It’s a living guide that needs to evolve as your life does. To keep it relevant and effective, you need a regular check-in cadence. This proactive review process is what keeps you on course and allows you to make smart adjustments when life—as it always does—throws you a curveball.

A structured review schedule prevents you from either anxiously micromanaging your money every day or, worse, neglecting it for years on end. Here’s a practical rhythm that works for most people.

- Monthly Check-In (15-30 Minutes): Think of this as a quick pulse check. Hop into a tool like PopaDex and review your budget and spending. Did you stick to your plan? Are there any spending categories that need a little tweaking for next month?

- Quarterly Review (1-2 Hours): Now you go a bit deeper. How’s your progress toward your short-term goals? Take a look at your investment performance. Are your debt-paydown efforts on track? This is the perfect time to make minor course corrections.

- Annual Review (Half-Day): This is your big-picture strategy session. Re-evaluate your long-term goals. Has anything significant changed in your life—a new job, a marriage, a change in income? This is where you make major adjustments to your overall plan for the year ahead.

This rhythm breaks down the intimidating task of “managing your money” into a series of small, totally manageable habits.

This hands-on approach is becoming much easier thanks to major shifts in the financial services market. The industry is seeing massive growth, largely driven by evolving investor needs and new technology. For instance, the explosion of robo-advisors is a huge factor; that market is projected to swell from $7.39 billion in 2023 to an incredible $72 billion by 2032. This kind of digital assistance complements traditional advice, making holistic financial management more accessible than ever. If you’re curious, you can discover more insights about financial advisor trends on bizplanr.ai.

Creating a financial plan is the starting line. But it’s the consistent implementation and monitoring that actually builds wealth over the long haul.

Diving into personal finance brings up a lot of questions. That’s completely normal. Building a financial plan is a big deal, and it’s smart to want to get the details right. This section tackles the most common questions we hear, with straightforward answers to help you move forward with confidence.

Think of this as your go-to resource for those “what if” and “how do I” moments.

How Often Should I Review My Financial Plan?

The perfect review schedule isn’t a single date on the calendar; it’s more like a layered rhythm. A financial plan should be a living, breathing document, not something you create once and forget about. As your life changes, your plan needs to keep up.

A good approach involves a few different check-ins:

- A Quick Monthly Check-in: Spend 15-30 minutes each month for a quick look at your budget and spending. This is just a simple pulse check to make sure your daily habits are still pointing you in the right direction.

- A Deeper Quarterly Review: Every three months, it’s time to dig a little deeper. How are you tracking toward your savings goals? How are your investments performing? This is the ideal time to make small tweaks and course corrections.

- A Big-Picture Annual Review: Once a year, block off a couple of hours for a full-scale review. Re-evaluate your long-term goals. Did your income change? Have your priorities shifted? This is when you’ll make the more significant strategic moves for the year ahead.

Most importantly, any major life event should trigger an immediate review. Getting married, having a baby, changing careers, or receiving an inheritance—all of these moments require a fresh look at your plan to make sure it still fits your new reality.

What’s The Biggest Mistake to Avoid?

If there’s one pitfall I see people fall into more than any other, it’s chasing perfection. They create these incredibly restrictive budgets or set wildly optimistic goals that are just impossible to maintain. This all-or-nothing mindset almost always ends in burnout, frustration, and eventually, ditching the plan altogether.

The best financial plan isn’t the most aggressive or the most detailed—it’s the one you can actually stick with. Sustainability beats perfection every single time. A plan that can bend without breaking is a plan that will last.

Build some breathing room into your strategy from the very beginning. Set aside money for fun and spontaneity. Accept that unexpected costs are a part of life. Your plan should be a resilient guide, not a rigid cage. Making that mental shift is often the difference between success and failure.

Do I Need a Financial Advisor to Create a Plan?

Not always, but the answer really hinges on your specific situation. For lots of people with fairly straightforward finances—like saving for a down payment or tackling debt—using a powerful tool and great online resources is more than enough to build an effective plan.

However, a certified financial advisor can be an incredibly valuable partner when your financial life gets more complicated.

You might want to think about professional guidance if you’re:

- Managing significant assets or a complex investment portfolio.

- Going through big life transitions, like retirement or selling a business.

- Dealing with tricky tax situations or estate planning.

- Feeling completely overwhelmed and just need an expert to provide structure and hold you accountable.

An advisor brings sophisticated strategies and an objective viewpoint that’s tough to replicate on your own. They can spot blind spots you might miss and help you navigate the financial world with much more confidence.

How Can I Stay Motivated to Stick With My Plan?

Motivation is a funny thing; it comes and goes. The trick isn’t to stay motivated 100% of the time, but to build a system that keeps you on track even when the initial excitement wears off. The best way to do that is to stay connected to your “why.”

Regularly visualize the goals you’re working toward. Don’t just think about saving $10,000; picture the actual vacation you’ll take with it. Keeping the end result in sharp focus is a powerful driver.

Also, celebrate the small wins along the way! Did you pay off a credit card? Hit a savings milestone? Acknowledge it. These little victories create momentum. Using an app like PopaDex, which can visualize your progress with charts and graphs, also helps make the process more engaging.

Finally, think about finding an accountability partner—a spouse, a trusted friend, or a family member who gets it. Having someone to check in with can truly make all the difference. For more detailed answers to other questions, feel free to check out our comprehensive PopaDex FAQs page.

Ready to stop guessing and start knowing exactly where your money stands? Take control of your financial future with PopaDex. Consolidate all your accounts, track your net worth in real-time, and build a plan that works for you. Start your free trial today at popadex.com and gain the clarity you deserve.