Our Marketing Team at PopaDex

Clear Expat Tax Advice for Americans Abroad

If you’re an American living abroad, the first step toward financial peace of mind is getting a handle on your tax obligations. The single most important piece of expat tax advice is this: the United States taxes you based on citizenship, not where you live. This means your worldwide income is subject to U.S. tax laws, no matter where you currently call home.

Your Core Responsibilities as a US Expat

The idea of filing U.S. taxes from another country can feel overwhelming, but the core principle is actually pretty simple. Think of it as a financial link back to your home country that doesn’t disappear just because you’ve moved.

Fortunately, the system isn’t designed to punish you. It includes powerful tools specifically meant to prevent you from being taxed twice on the same dollar.

Your main job is to report all your income, whether it’s a salary in Singapore, rental income from a flat in Spain, or investment gains back in the States. You’ll typically do this on the standard Form 1040, just like everyone else back home.

Essential Tools to Prevent Double Taxation

To make this fair, the IRS gives expats two primary tools to work with. These aren’t loopholes; they are established provisions designed to ease the financial burden of living and working overseas.

-

Foreign Earned Income Exclusion (FEIE): This lets you exclude a huge chunk of your foreign salary from your U.S. tax return. For 2024, that amount is $126,500. It’s an incredibly effective way to lower—or even completely wipe out—your U.S. tax bill, especially if you live in a low or no-tax country.

-

Foreign Tax Credit (FTC): This is a dollar-for-dollar credit for income taxes you’ve already paid to your host country. If you live somewhere with higher taxes than the U.S. (think much of Western Europe), the FTC can often be even more powerful than the FEIE.

The real key is understanding how your filing obligation and these relief provisions work together. Your goal isn’t just to file, but to file in the most financially savvy way possible.

Navigating these rules is a critical part of solid financial planning for expats, as it has a direct impact on your take-home pay and long-term savings. To get a complete picture of what’s required of you as an American overseas, check out this practical guide on how to file US taxes from abroad. Mastering these concepts will empower you to stay compliant while keeping more of your hard-earned money.

Mastering the Foreign Earned Income Exclusion

The Foreign Earned Income Exclusion (FEIE) is easily one of the most powerful tools in an expat’s financial arsenal. Think of it as the IRS simply agreeing to ignore a huge chunk of your salary. When you get it right, the FEIE can dramatically slash—or even completely wipe out—your U.S. tax bill.

This provision is the bedrock of U.S. expat tax strategy, letting Americans abroad shield a significant part of what they earn from federal taxes. For the 2025 tax year, you can exclude up to $130,000 of your foreign income. If you’re married and both of you work abroad, that number doubles to a combined $260,000, which is a massive saving. You can see more on these updated figures in this expat tax guide on bankrate.com.

But here’s the catch: it’s not automatic. You have to formally claim the exclusion on your tax return by filing Form 2555. More importantly, you first have to prove to the IRS that your life and work are genuinely based outside the United States.

Proving Your Connection to a Foreign Country

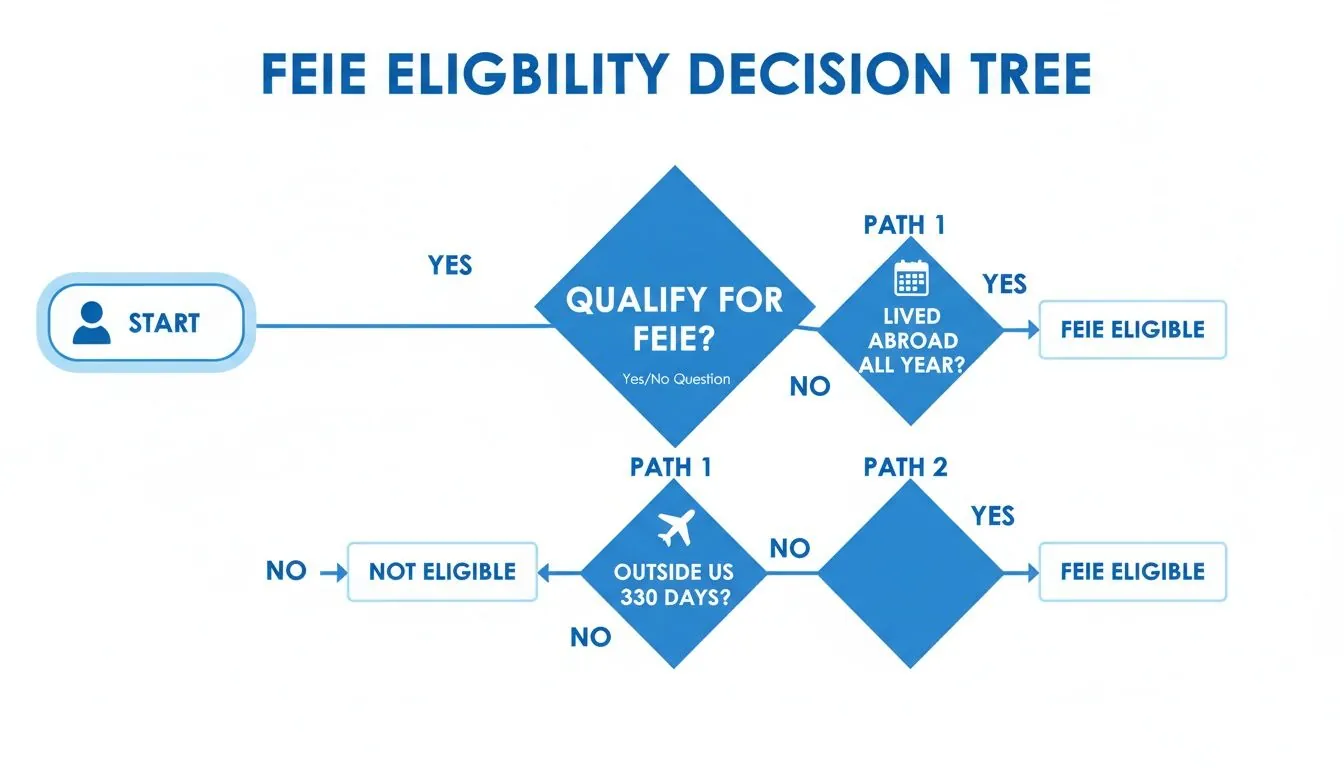

To get your hands on the FEIE, you have to pass one of two crucial tests. These are designed to separate someone on a long holiday from a true expat who has put down roots abroad. Which one you choose comes down entirely to your personal situation.

-

Bona Fide Residence Test: This test is for expats who’ve moved to a new country for the long haul, covering at least one full calendar year. It’s all about your intent. The IRS is looking for proof that you’ve actually built a life there—think long-term apartment leases, local bank accounts, and getting involved in the community. It’s less about counting days and more about proving your new country is your real home base.

-

Physical Presence Test: This one is a straight-up numbers game, making it perfect for digital nomads or contractors who jump between countries. To pass, you must be physically outside the U.S. in a foreign country (or several) for at least 330 full days within any 12-month period. The days don’t need to be consecutive, but be careful—even a quick trip over international waters can reset your count.

The most important takeaway is that you must choose the test that best reflects your situation. The Bona Fide Residence test offers more flexibility for visiting the U.S., but the Physical Presence Test is a straightforward mathematical calculation.

To make this even clearer, let’s break down who each test is really for and what it requires.

FEIE Eligibility Tests at a Glance

This table compares the two key tests to qualify for the Foreign Earned Income Exclusion, helping you quickly identify which path suits your circumstances.

| Qualification Test | Who It’s For | Key Requirement |

|---|---|---|

| Bona Fide Residence Test | Expats with a permanent home abroad for an entire tax year or longer. | Prove your intention to reside in a foreign country indefinitely. |

| Physical Presence Test | Digital nomads, contractors, or expats who move frequently. | Be physically present in a foreign country for 330 days in any 12-month period. |

Choosing the right test from the get-go saves a lot of headaches later on. If you’re settled in one place, the Bona Fide test is usually the better fit. If your life is more transient, the Physical Presence test is your ticket.

What Income Qualifies for the Exclusion

The FEIE only applies to foreign earned income. This is money you get for services you performed while outside the U.S. It usually covers your salary, wages, bonuses, and professional fees.

It’s just as important to know what doesn’t count:

- Investment income (dividends, interest, capital gains)

- Pension or annuity payments

- Social Security benefits

- Pay received as a U.S. government employee

On top of the FEIE, you might also be able to claim the Foreign Housing Exclusion (or a deduction if you’re self-employed). This lets you exclude certain housing costs—like rent and utilities—that go above a base amount, offering even more tax relief if you’re living in an expensive city like London or Tokyo.

Choosing Between FEIE and the Foreign Tax Credit

This is one of the biggest financial decisions you’ll make as an American abroad: Should you use the Foreign Earned Income Exclusion (FEIE) or the Foreign Tax Credit (FTC)? Both are designed to prevent the headache of double taxation, but they get there in completely different ways.

Picking the right one can literally save you thousands of dollars each year, so it’s critical to understand how they work.

Think of the FEIE as an invisibility cloak for your income. It lets you tell the IRS to simply ignore a large chunk of what you earned abroad. Poof, it’s gone from your U.S. tax calculation. The Foreign Tax Credit, on the other hand, is a direct, dollar-for-dollar credit for the income taxes you’ve already paid to your host country. It’s like getting a direct discount on your U.S. tax bill.

Before you go any further, the first step is figuring out if you even qualify for the FEIE. This decision tree breaks it down for you.

As you can see, you have to spend a significant amount of time outside the U.S. to qualify, meeting either the Bona Fide Residence Test or the Physical Presence Test.

High-Tax Country vs. Low-Tax Country Scenarios

The single biggest clue for which to choose is your local tax rate. Your decision often becomes crystal clear when you look at how much tax you’re paying where you live.

-

Living in a High-Tax Country (think Germany, France, or Canada): If you’re paying more in foreign taxes than you would in U.S. taxes, the Foreign Tax Credit is almost always your best bet. Why? The credit you get for taxes paid abroad will likely be big enough to completely wipe out your U.S. tax liability. You might even have leftover credits to carry forward to future years.

-

Living in a Low- or No-Tax Country (like the UAE, Qatar, or Monaco): In this case, the FEIE is usually the clear winner. Since you’re paying little to no income tax locally, you won’t have any foreign taxes to claim as a credit. The FEIE lets you exclude a huge portion of your income, slashing your U.S. taxable income and, in many cases, eliminating your tax bill entirely.

The rule of thumb is pretty straightforward: If you’ve already paid high taxes to another country, use the FTC to get credit for it. If you haven’t paid much (or any) tax abroad, use the FEIE to make your income invisible to the IRS.

Factors That Can Change the Game

While the local tax rate is the main driver, other parts of your financial life can tip the scales. This isn’t just about one tax year; it’s about your entire long-term picture.

When you’re looking for expat tax advice, keep these other factors in mind:

- Retirement Savings: Using the FEIE can limit or even prevent you from contributing to U.S. retirement accounts like a traditional or Roth IRA. The FTC has no such restriction.

- Kids and Family: This is a big one. Taking the FEIE might stop you from claiming the refundable part of the Child Tax Credit, which can be a significant amount of money for families.

- Types of Income: The FEIE only works on earned income—like your salary or self-employment income. The FTC, however, can be applied to taxes you’ve paid on both earned and unearned income, like from investments.

Choosing between the FEIE and FTC isn’t a permanent, irreversible decision, but there are rules that can make it tricky to switch back and forth. It’s always a smart move to review your situation every year and make sure you’re still using the strategy that saves you the most money.

Decoding FBAR and FATCA Reporting Rules

Living abroad means your US tax obligations stretch beyond the standard Form 1040. You’ll quickly run into two acronyms that every expat needs to know: FBAR and FATCA. While they sound similar, they’re entirely different beasts with their own rules and massive penalties for non-compliance.

Here’s the simplest way to think about it: the FBAR is a report to the Treasury’s financial crime-fighting division, while FATCA is a report to the IRS. Both are about transparency, but they serve different agencies for different reasons.

First up is the FBAR (Report of Foreign Bank and Financial Accounts), which is filed using FinCEN Form 114. You have to file this if the combined total of all your foreign financial accounts hit $10,000 at any point during the year. That threshold is lower than you think—a single paycheck or a quick transfer can easily push you over the limit.

FBAR vs. FATCA: Key Differences

Then there’s FATCA (Foreign Account Tax Compliance Act). This one is reported on Form 8938, which you attach directly to your annual income tax return. Thankfully, the filing thresholds for FATCA are much, much higher.

For instance, a single expat only has to file Form 8938 if their foreign assets top $200,000 on the last day of the year or $300,000 at any time. As you can see, that’s a world away from the FBAR’s $10,000 trigger.

Let’s break down the core differences so you can keep them straight:

- Who You Report To: The FBAR goes to FinCEN (Financial Crimes Enforcement Network), a bureau within the Treasury Department. FATCA goes straight to the IRS.

- The Form: FBAR requires FinCEN Form 114, which you file online, completely separate from your taxes. FATCA uses Form 8938, which gets attached to your Form 1040.

- The Threshold: FBAR kicks in at a low $10,000 combined balance. FATCA starts much higher, at $200,000 for single expats living abroad.

- The Deadline: The FBAR is technically due April 15th but comes with an automatic extension to October 15th. The FATCA deadline simply follows your tax return’s due date (June 15th for expats, extendable to October 15th).

It’s critical to understand that these requirements are independent. You might need to file one, both, or neither. Hitting the FBAR threshold doesn’t mean you automatically have to file for FATCA, and vice-versa.

What Actually Counts as a “Financial Account”?

This is where many expats get tripped up. The term “financial account” is surprisingly broad and goes way beyond your everyday checking and savings accounts. To stay compliant, you need to understand the full scope of what the US government is looking at. You can dig into a detailed breakdown of foreign asset reporting requirements to make sure nothing slips through the cracks.

Generally, you’ll need to report:

- Bank accounts (checking, savings, time deposits)

- Brokerage and securities accounts

- Commodity futures or options accounts

- Insurance policies or annuities that have a cash value

- Mutual funds and other similar pooled funds

Ignoring these forms is a terrible idea. The penalties are staggering. A non-willful FBAR violation can cost you up to $10,000 per account, per year. If the IRS decides you willfully failed to file, the penalty can jump to the greater of $100,000 or 50% of the account’s balance. Getting this right isn’t just good advice—it’s essential.

How Global Tax Incentives Can Benefit You

Your choice of where to live can have a massive impact on your finances. While U.S. tax obligations follow you everywhere, many countries are actively competing for American talent and investment with attractive tax programs designed to make your move worthwhile.

This isn’t just about finding a zero-tax haven; it’s about making a strategic decision that lines up your lifestyle with your financial goals. By understanding and taking advantage of these global incentives, you can turn tax planning from a domestic chore into an exciting international strategy.

A Case Study in Smart Relocation: Greece

To see how this works in the real world, let’s look at Greece. The country has become a hotspot for expats looking for low-tax options, especially with its flat tax incentives aimed at retirees and high-net-worth individuals. For retirees, a standout 7% flat tax on all worldwide income, including pensions, applies for up to 10 years, drawing thousands to its sunny shores. You can explore more about how Greece’s incentives stack up against other low-tax countries for expats on globalcitizensolutions.com.

This type of program, often called a “non-domicile” or “non-dom” regime, essentially allows qualifying foreign residents to pay a fixed, predictable tax on their foreign income. It simplifies tax planning and can lead to huge savings, especially for those with large investment portfolios or pensions. It’s a clear example of a country using tax policy to attract wealth and talent.

By seeking out countries with favorable tax policies, you’re not avoiding your U.S. obligations—you’re optimizing your global financial picture. The goal is to legally minimize your overall tax burden across jurisdictions.

Of course, these benefits come with rules attached. You’ll typically need to meet specific criteria related to residency, investment, and proving you haven’t been a tax resident there in the recent past. Successful cross-border financial planning involves digging into these rules to make sure you qualify.

For those thinking about starting a business abroad, getting a handle on local corporate tax rules is just as critical. For example, you can learn how to register for corporate tax in the UAE to see how different places approach business incentives. The key is to do your homework and align your move with a country whose policies best support your financial situation, whether you’re retiring, working, or launching a new venture.

Avoiding Common and Costly Expat Tax Mistakes

Navigating U.S. taxes while living abroad can feel like you’re walking through a minefield. Even the most organized person can trip over a small detail that ends up costing them big time.

Knowing where the common pitfalls are is the best expat tax advice you can get. It’s the key to making sure you have a smooth, penalty-free filing season.

A classic mistake is getting the deadlines mixed up. While most expats get an automatic two-month filing extension to June 15th, any taxes you actually owe are still due on April 15th. If you miss that payment deadline, the IRS starts charging interest and penalties right away.

Another huge oversight is simply forgetting to report all your income. That online side hustle you picked up? The small amount of rent you collect from a property back home? It all counts. The IRS wants to know about your worldwide income, and failing to report it is a major red flag.

The Problem of State Tax Residency

One of the sneakiest—and most expensive—traps for an American abroad is thinking you’re free from state taxes just because you moved. This is a dangerous assumption.

States like California, Virginia, and New Mexico are notoriously “sticky.” This means they make it incredibly difficult to sever your ties for tax purposes. Simply packing your bags and hopping on a plane isn’t nearly enough to get you off their radar. They’ll dig into a whole host of factors to decide if you’ve truly cut ties.

Many expats successfully break residency every year, but it requires deliberate action. You can’t just leave; you must document your departure by severing financial, professional, and personal connections to your former state.

For instance, you could find yourself on the hook for state taxes on your global income if you don’t take care of a few critical details. Failing to do the following can keep you tied to your old state:

- Cancel your driver’s license: Hanging onto your state license looks like you plan on coming back.

- Update voter registration: Staying on the local voter rolls is a huge indicator of residency.

- Close local bank accounts: Maintaining significant financial accounts in the state works against your claim of non-residency.

Getting this wrong can lead to a surprise tax bill for thousands of dollars. Being proactive and methodically cutting these ties is absolutely crucial to protecting your finances while you’re living and working overseas.

Your Top Expat Tax Questions, Answered

Navigating your obligations as an American abroad can feel tricky, and it’s natural for specific questions to pop up. Here’s some straightforward advice on the most common issues we see expats facing.

Do I Still Have to File If I Pay Local Taxes?

Yes, you absolutely do. The U.S. operates on a citizenship-based taxation system, which is unique in the world. This means if you meet the income filing threshold, you must file a federal return reporting your worldwide income, regardless of where you live or if you’ve already paid taxes to another country.

But don’t worry—the system is designed to prevent you from being taxed twice on the same dollar. You can use powerful tools like the Foreign Tax Credit (FTC), which gives you a dollar-for-dollar credit for taxes paid to your host country. For many expats, this credit completely wipes out their U.S. tax bill.

What if I’ve Never Filed Expat Taxes Before?

If you’re just learning about your filing duties, the first thing to know is: don’t panic. This is a common situation, and the IRS has a specific program just for you called the Streamlined Filing Compliance Procedures.

This program is a lifeline for taxpayers who non-willfully (meaning, unintentionally) failed to file. It allows you to get caught up on past-due tax returns and foreign bank account reports (FBARs) with significantly reduced or even zero penalties. It’s always far better to address this proactively than to wait for the IRS to find you.

You cannot use both the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit on the same income. However, an advanced strategy involves using the FEIE on your salary and the FTC on unearned income like investments.

Does My Foreign Spouse’s Income Affect My U.S. Taxes?

That all depends on how you choose to file. If you file as Married Filing Separately, you generally only need to report your own income. This is often the simplest path.

However, you might consider filing as Married Filing Jointly to access certain tax benefits, like higher standard deductions. If you go this route, you must report your spouse’s entire worldwide income on your U.S. tax return. This decision has major financial implications and is something you’ll want to carefully consider, maybe even with a tax professional.

Get the complete picture of your global finances. PopaDex helps you track your entire portfolio, from international bank accounts to global investments, all in one secure place. Start managing your net worth with total confidence at https://popadex.com.