Our Marketing Team at PopaDex

A Simple Guide to Financial Literacy Basics

Think of financial literacy as your personal guide to handling money. It’s not about memorizing complex economic theories; it’s about having the practical know-how to make smart, confident decisions every single day. It’s the foundation for building a secure future and achieving your goals.

Why Financial Literacy Matters Now More Than Ever

Trying to manage your finances without understanding the basics is like navigating a new city without a map. You might get where you’re going eventually, but you’ll probably hit a lot of dead ends, take some wrong turns, and feel stressed the entire time.

Financial literacy is that map. It gives you the clarity to get from where you are to where you want to be—whether that’s buying a home, retiring comfortably, or just living without that constant, nagging anxiety about money.

Without this knowledge, you’re essentially flying blind. Small decisions can snowball into huge problems, like racking up high-interest debt or missing out on the incredible power of compound growth. With it, you’re in control.

The Real-World Impact of Financial Knowledge

The gap between knowing and not knowing is huge. Recent data shows just how much of a challenge financial education remains. For instance, in 2025, U.S. adults correctly answered only 49% of personal finance questions on the P-Fin Index—a number that hasn’t budged since 2017.

This knowledge gap is directly linked to financial fragility, proving just how vital these skills are for day-to-day stability. You can dig deeper into these findings and what they mean for different people over at the TIAA Institute-GFLEC website.

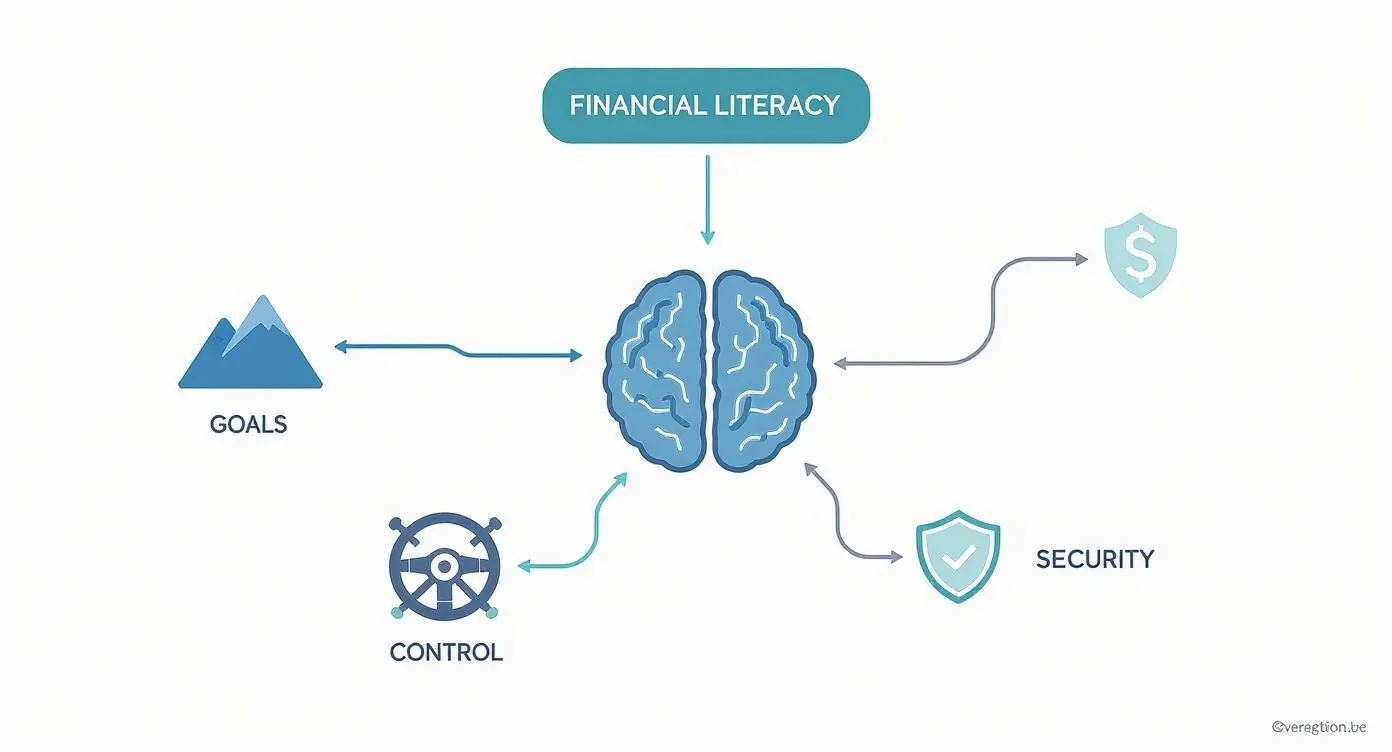

This infographic breaks down the core pillars of financial literacy and shows how they all connect.

As you can see, true financial literacy is more than one thing. It’s an interconnected system that helps you hit your goals while staying on solid ground.

Financial literacy is the bedrock of a secure future. It transforms money from a source of stress into a tool for building the life you want.

Ultimately, getting a grip on the basics is about more than just numbers on a spreadsheet. It’s about empowerment. It’s about giving yourself the ability to:

- Make informed decisions on everything from your daily budget to your long-term investments.

- Avoid common pitfalls like crushing debt and sneaky financial scams.

- Build a strong foundation that actually supports your biggest life goals.

Master Your Cash Flow with a Smart Budget

Let’s be honest—when most people hear the word “budget,” they think of restriction, sacrifice, and cutting out all the fun. But a good budget is the exact opposite. It’s an empowerment tool.

Think of it less like a diet for your wallet and more like a game plan for your life. A budget is simply about telling your money where to go, so you can finally achieve what really matters to you. It helps you see where every dollar is going, shines a light on those sneaky unconscious spending habits, and turns financial guesswork into intentional action. This is the first, most crucial step toward gaining total control over your cash flow and one of the most important financial literacy basics you can master.

Finding the Right Budgeting Method for You

There’s no magic “best” budget out there. The only one that works is the one you’ll actually stick with. Different methods click with different personalities, so the goal is to find a system that feels natural and keeps you motivated.

Here are a few of the most popular and effective strategies to get you started:

- The 50/30/20 Rule: This is a fantastic starting point if you’re new to budgeting. You simply split your after-tax income into three buckets: 50% for needs (rent, utilities, groceries), 30% for wants (hobbies, dining out), and 20% for savings and debt repayment. It’s straightforward and gives you a balanced approach without getting bogged down in tiny details.

- Zero-Based Budgeting: Perfect for the detail-oriented person who wants maximum control. With this method, every single dollar gets a specific job. You take your monthly income and assign all of it to expenses, savings, and debt until your income minus your outgoings equals zero. It forces you to be incredibly intentional with your spending.

- The Envelope System: If you’re a hands-on, visual person, this cash-based approach is for you. You create physical (or digital) envelopes for different spending categories like “Groceries” or “Fun Money” and put a set amount of cash in each at the start of the month. When an envelope is empty, that’s it—no more spending in that category until next month. Overspending becomes practically impossible.

A budget is simply you telling your money where to go, instead of wondering where it went. It’s the difference between being the driver of your financial life and just being a passenger.

Choosing the right approach is everything. To really dig into these strategies and figure out which one fits you best, checking out a detailed guide on mastering budgeting can provide a clear path to financial freedom.

Choosing Your Best Budgeting Method

A comparison of popular budgeting strategies to help you select the one that best fits your financial personality and goals.

| Budgeting Method | Best For | Key Principle |

|---|---|---|

| 50/30/20 Rule | Beginners looking for simplicity and flexibility. | Allocate income into three broad categories: Needs (50%), Wants (30%), and Savings (20%). |

| Zero-Based Budgeting | Detail-oriented individuals who want total control over every dollar. | Assign every dollar of income a specific “job,” ensuring Income - Expenses = 0. |

| Envelope System | Visual, hands-on people who struggle with overspending on debit/credit cards. | Use cash allocated into physical envelopes for specific spending categories. |

Finding a method that aligns with your natural tendencies is the secret to making your budget stick for the long haul.

From Theory to Action

Once you’ve picked a method, the real magic happens when you put it into practice. This is where a tool like PopaDex completely changes the game.

Instead of wrestling with clunky spreadsheets or a stack of paper envelopes, you can link all your accounts in one place. PopaDex can automatically categorize your transactions and let you see in real-time how your spending stacks up against your budget. That kind of clarity transforms budgeting from a chore you dread into a powerful, motivating habit.

Build Your Financial Safety Net Through Saving

Once your budget is dialed in and you know where your money is going, it’s time to build a buffer between you and life’s inevitable curveballs. Saving goes beyond stashing cash away for a rainy day; it’s about building a financial shock absorber. It’s what protects all your hard work.

Once your budget is dialed in and you know where your money is going, it’s time to build a buffer between you and life’s inevitable curveballs. Saving goes beyond stashing cash away for a rainy day; it’s about building a financial shock absorber. It’s what protects all your hard work.

This safety net gives you breathing room and prevents a single unexpected bill from blowing up your entire financial plan.

Think of saving as intentionally setting money aside for different future goals. An emergency fund is your top priority—this should cover 3-6 months of essential living expenses if you lose your job or face a medical crisis. Beyond that, you might have a down payment fund for a future home or sinking funds for predictable big buys like a new car or a much-needed vacation.

The Power of Paying Yourself First

The single most effective way to build these funds is to pay yourself first. It’s a simple concept that completely flips the script on traditional saving. Instead of saving whatever is left over at the end of the month, you treat saving like your most important bill.

The ‘pay yourself first’ method ensures your future goals are a top priority, not an afterthought. It automates your success by making saving a consistent, effortless habit.

Set up automatic transfers from your checking to your savings account the day you get paid. This takes willpower and forgetfulness out of the equation. It’s a simple move that guarantees you’re consistently building wealth without even thinking about it.

Even a small, consistent amount can make a huge difference. If you’re starting from square one, check out our guide on how to build an emergency fund from scratch.

Where You Save Your Money Matters

Just as important as how much you save is where you keep it. The right account helps your money grow safely while still being there when you need it.

- Traditional Savings Accounts: Offered by most brick-and-mortar banks, these are secure and insured but usually offer rock-bottom interest rates. A decent starting point, but you can do better.

- High-Yield Savings Accounts (HYSAs): These are the game-changer. Often found at online banks, HYSAs offer significantly higher interest rates, letting your cash grow and fight off inflation while it sits.

- Money Market Accounts (MMAs): Think of these as a hybrid between a checking and savings account. They offer competitive interest rates and might come with check-writing or debit card access.

Parking your emergency fund and other short-term savings in an HYSA or MMA is a smart move. It ensures your money is more than sitting idle—it’s working for you, even in the background. With PopaDex, you can easily track these different savings accounts, giving you a crystal-clear view of your progress toward each one of your goals.

Make Your Money Work for You Through Investing

While saving is about building a financial safety net, investing is what actually grows your long-term wealth. It’s the engine of financial freedom.

Think of it like planting a tree. You start with a small seed (your initial investment). With consistent care (regular contributions) and time, that seed grows into something substantial that can provide shade—and financial security—for years to come.

Lots of people get intimidated by investing, picturing complicated charts and the chaos of Wall Street. But investing is no longer just for the pros. At its core, it’s simply using your money to buy assets that have the potential to grow in value. This is a massive step in your financial literacy basics, moving you from just protecting your money to actively making it work for you.

Understanding the Building Blocks of Investing

You don’t need to be an expert to get started. Honestly, you just need to grasp a few key concepts. The most common investment types are surprisingly straightforward:

- Stocks: When you buy a stock, you’re purchasing a tiny slice of ownership in a company. If the company does well and its value increases, so does the value of your slice.

- Bonds: Think of a bond as a loan you give to a government or a big corporation. In return, they promise to pay you interest over a set period and then give your original investment back at the end. They’re generally considered less risky than stocks.

- Mutual Funds & ETFs: These are like baskets that hold a mix of stocks, bonds, or other assets. Buying into one lets you instantly spread your money across many different companies, which is a great way to manage risk without having to pick individual winners.

The best part? You don’t need a fortune to begin. Modern apps and brokerage accounts let you start with just a few dollars.

The Magic of Compound Interest

If investing has a superpower, it’s compound interest. This is where your investment returns start earning their own returns. Over time, this creates a snowball effect that can turn small, regular contributions into a serious nest egg.

Imagine you invest $100 every month. Over 30 years, assuming a 7% average annual return, you would have put in $36,000 of your own money. But thanks to the power of compounding, your account could be worth over $120,000. That’s the magic of putting your money to work and letting it grow on its own.

Investing is a long-term game. It’s not about timing the market, but about time in the market. Consistency and patience are your greatest assets.

No matter where you put your money, the goal is for it to grow. A key part of that is knowing how to measure its success; learning how to calculate Return on Investment will empower you to make much smarter decisions.

Taking the First Step

Getting started is often the hardest part, but it doesn’t have to be a huge leap. If you’re ready to make your money work harder, our guide on how to start investing money breaks down the entire process into simple, actionable steps.

Using a tool like PopaDex helps you see the whole picture. When you track your investment accounts right alongside your savings, debts, and other assets, you get a real-time view of your net worth as it grows. That clarity is a powerful motivator to stay the course and watch your financial tree flourish.

Tackle Debt and Boost Your Financial Health

Debt can feel like running a race with a heavy backpack on—it slows you down and makes every single step harder. But with a solid game plan, you can start lightening that load and eventually take it off for good. Getting a handle on your debt is one of the core financial literacy basics that has a massive impact on your overall well-being.

It helps to know that not all debt is created equal. There’s “good debt” and “bad debt.” Good debt is usually an investment in your future that can grow your net worth over time, like a mortgage for a home or student loans for an education. Bad debt, on the other hand, comes from high-interest loans for things that lose value, like credit card balances from last month’s shopping spree.

Choosing Your Debt Paydown Strategy

When you’re ready to start knocking down those balances, two proven methods come to mind: the Debt Snowball and the Debt Avalanche. The right one for you really boils down to what gets you fired up—quick psychological wins or pure mathematical efficiency.

- The Debt Snowball Method: You list your debts from the smallest balance to the largest, ignoring the interest rates for a moment. You’ll make minimum payments on everything except the smallest debt, which you attack with every extra dollar you can find. Once that’s gone, you roll that entire payment amount into the next-smallest debt. It’s all about building momentum, and those early wins feel great.

- The Debt Avalanche Method: With this approach, you list your debts by interest rate, from highest to lowest. You still make minimum payments on everything, but you throw all your extra cash at the debt with the highest interest rate. This method saves you the most money in interest over time, making it the most efficient choice from a numbers perspective.

Whichever method you choose, consistency is key. The goal is to create a focused plan that you can stick with until you’re debt-free.

No matter which path you take, a crucial step is thoroughly understanding your credit card statements so you can track your progress and stay on target.

The Connection Between Debt and Your Credit Score

Think of your credit score as your financial report card. It’s a three-digit number lenders use to figure out how risky it might be to lend you money. Paying down your debt has a direct and powerful impact on this score, mostly by improving your credit utilization ratio—that’s the amount of credit you’re using compared to your total available credit.

As you shrink your credit card balances and other loans, that ratio drops, which lenders absolutely love to see. A lower debt load shows you’re responsible, and that can give your score a serious boost. A higher score then opens the door to better interest rates on future loans, potentially saving you thousands.

The effort to tackle debt goes beyond the personal; it’s part of a larger global push for better financial health. The World Bank noted that in 2024, only 40% of adults in developing economies saved money in a financial account. While this is a significant 16-percentage point increase since 2021, it shows there’s still a long way to go in promoting financial literacy and access to the right money management tools.

Answering Your Top Financial Questions

Starting any new journey brings up a ton of questions, and getting a handle on your finances is no different. It’s totally normal to feel a bit unsure as you begin putting these ideas into action. This section is here to tackle some of the most common questions, giving you straightforward answers so you can move forward with confidence.

Think of this as a final pep talk—a chance to clear up any last-minute doubts before you roll up your sleeves and get to work.

Where Should I Start If I Feel Overwhelmed?

The sheer volume of financial advice out there can be paralyzing. If you’re looking at a mountain of information and don’t know where to take the first step, the answer is simple: start with your budget.

Your budget is the foundation for everything else. It’s the diagnostic tool that shows you exactly where your money is going right now—and that’s the single most important piece of information you can have. Before you start stressing about investment strategies or complex debt payoff plans, just focus on tracking your income and expenses for one month.

This one act will bring more clarity than a hundred articles. It’s not about restriction; it’s about awareness. Once you have that, every other decision becomes much clearer and far less intimidating.

How Do I Stay Motivated When I Hit a Setback?

Everyone hits a financial speed bump. An unexpected car repair shows up, or you have a month where you just plain overspend. It’s not a matter of if it will happen, but when. The trick is not to let one mistake derail your entire plan.

Financial progress isn’t a straight line; it’s a series of steps forward and the occasional step back. The most important thing is to keep moving in the right direction, no matter how small the steps are.

Here are a few ways to get back on track:

- Revisit Your “Why”: Why did you start this in the first place? Was it to feel secure? To buy a home? To finally travel without guilt? Reminding yourself of the big picture can be the fuel you need.

- Focus on Small Wins: Did you stick to your grocery budget this week? Pay a little extra on your credit card? Acknowledge and celebrate these small victories. They add up.

- Automate Your Success: Set up automatic transfers to your savings and investment accounts. This makes sure you’re making progress even when your motivation is running low.

Motivation is fickle. Good systems, on the other hand, will keep you on course no matter what.

Which Financial Goal Should I Prioritize First?

When you’re juggling multiple goals—saving for retirement, killing off debt, and building an emergency fund—it’s tough to know what to tackle first. While everyone’s situation is a little different, here’s a solid rule of thumb for prioritizing:

- Build a Starter Emergency Fund: Your first mission is to get at least $1,000 into a separate savings account. This small buffer keeps minor emergencies from turning into major debt.

- Pay Down High-Interest Debt: Any debt with an interest rate over 7-8%, like credit card balances, is a financial anchor. It’s actively working against you and should be your top priority.

- Fully Fund Your Emergency Savings: Once the expensive debt is gone, focus on beefing up your emergency fund to cover 3-6 months of essential living expenses.

With that safety net firmly in place, you can start investing for long-term goals like retirement with much more confidence. Mastering these basics is a real challenge, especially for younger generations. Recent data shows that financial literacy among Gen Z is alarmingly low, with an average score of just 38% on the P-Fin Index. This really drives home why building these foundational habits early on is so critical for long-term stability. You can dig deeper into these trends in a detailed report on financial literacy statistics.

Ready to stop guessing and start knowing exactly where your money stands? PopaDex brings all your accounts into one simple, clear dashboard, giving you the real-time clarity you need to track your net worth, manage your budget, and achieve your goals. Take control of your financial future today by visiting https://popadex.com.