Our Marketing Team at PopaDex

A Guide to the Six Financial Planning Stages

Trying to get your finances in order can feel like staring at a massive, blank map with no idea which way is north. The good news? There’s a proven route. The core financial planning stages give you a six-step framework that turns that overwhelming map into a clear, turn-by-turn guide to get you from where you are today to where you want to be.

Your Roadmap Through the Financial Planning Stages

Think of financial planning less like a one-time event and more like a continuous cycle. It’s a structured process that helps you get organized, figure out what you really want out of life, and then build a strategy to make it happen.

This journey is broken down into distinct phases, and each one builds on the last. Once you get the hang of this framework, you’ll feel more in control of your money, whether you’re just starting your career or fine-tuning a strategy you’ve had for years. It takes the whole process from feeling like a chore full of jargon to what it should be: designing a life you’re excited about.

The Proven Framework for Success

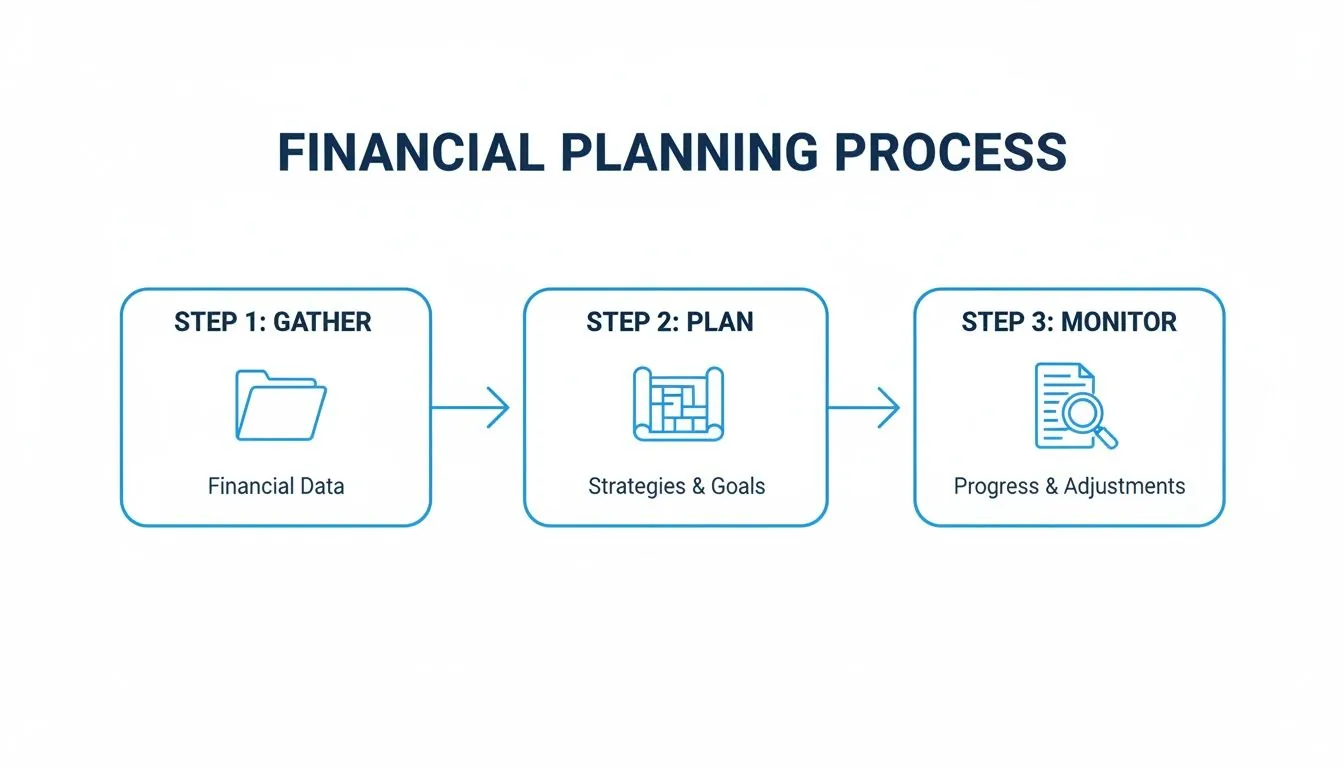

At its heart, the entire journey boils down to three simple actions: gathering information, creating a strategy, and checking in on your progress. This systematic approach is what turns fuzzy dreams into real, measurable results.

This visual guide breaks it down even further into those three fundamental steps: get your data, build your plan, and monitor everything.

What this really shows is that a solid financial plan isn’t a dusty document you create once and forget about. It’s a living system that needs regular attention to keep working for you.

This structured approach is a massive confidence booster. In fact, a staggering 80% of people with a professionally prepared financial plan feel good about retiring when they want to. Compare that to just 36% of those who don’t have a formal plan. A clear process more than doubles your retirement confidence.

The whole point of financial planning is to build a bridge between your financial reality today and the future you want. Each of these stages is a pillar holding that bridge up, making sure it’s strong enough to handle whatever life throws at it.

Of course, knowing the right time to start building that bridge is half the battle. A great strategy starts with knowing when to start retirement planning to give your money the most time to grow.

By following this kind of structured approach, you’re not just shuffling money around; you’re actively building the future you envision for yourself and your family. In the next sections, we’ll dive into each of the six stages, giving you the practical insights you need to get moving.

The Six Financial Planning Stages at a Glance

Before we break down each step in detail, here’s a quick overview of the entire process. Think of this as the “you are here” map for your financial journey. Each stage has a clear purpose, guiding you logically to the next.

| Stage Number | Stage Name | Core Purpose |

|---|---|---|

| Stage 1 | Establish the Relationship | Define the scope and set clear expectations with your planner (or yourself). |

| Stage 2 | Gather Data & Define Goals | Collect all your financial documents and clarify what you want to achieve. |

| Stage 3 | Analyze & Evaluate | Assess your current financial health to identify strengths and weaknesses. |

| Stage 4 | Develop Recommendations | Create a tailored action plan designed to meet your specific goals. |

| Stage 5 | Implement the Plan | Put your financial recommendations into action—the most critical step. |

| Stage 6 | Monitor & Review | Regularly track your progress and make adjustments as your life changes. |

This table lays out the entire roadmap. Now, let’s get into the specifics of what happens at each stop along the way.

Stage One: Establishing Your Financial Starting Point

Before you can map out any journey, you need to know exactly where you’re starting from. The first stage of financial planning is all about discovery—pinpointing where you stand today. Think of it like a doctor running diagnostics before prescribing a treatment; this foundational step gathers the raw data that will inform every single decision you make from here on out.

This is where you create a complete, honest snapshot of your financial health. It means collecting the essential documents and facing the numbers head-on, without judgment. The goal is simple: understand the resources you have and the habits that are shaping your financial reality right now.

Gathering Your Financial Puzzle Pieces

Your first task is to assemble all your financial documents. This isn’t just busywork; it’s about getting all the puzzle pieces on the table so you can finally see the full picture. Looking into methods for secure financial data acquisition can make this process both efficient and safe, ensuring your plan is built on a rock-solid foundation of accurate information.

Start by pulling together the following:

- Bank Statements: Grab these for all checking and savings accounts to see your income and daily spending patterns.

- Investment Account Summaries: This includes retirement accounts like 401(k)s or IRAs, plus any brokerage accounts.

- Debt Records: Collect statements for your mortgage, car loans, student loans, and credit cards.

- Insurance Policies: Review your coverage for life, health, disability, and property.

- Pay Stubs: These confirm your gross income, what’s being deducted, and your actual take-home pay.

With these documents organized, you have the concrete evidence needed for the next crucial calculations.

Calculating Your Net Worth

Your net worth is the ultimate financial scorecard. It’s a simple yet powerful metric you get by subtracting your total liabilities (everything you owe) from your total assets (everything you own). This single number gives you a clear, unambiguous baseline of your current financial position.

Net worth isn’t a measure of your self-worth; it’s a tool for clarity. It tells the story of your financial past and gives you the starting point for the future you want to build.

Figuring it out might sound intimidating, but it doesn’t have to be. To get started, you can use a dedicated tool like PopaDex’s free net worth tracking spreadsheet to organize your numbers and see exactly where you stand. This step turns abstract financial ideas into a tangible figure you can actually track over time.

Analyzing Your Cash Flow

While net worth is a snapshot in time, cash flow is the movie showing how your money operates month to month. It’s the simple process of tracking what’s coming in (your income) versus what’s going out (your expenses). This analysis is a real eye-opener, revealing your spending habits and showing you where your money is actually going.

Understanding your cash flow is critical because it highlights your capacity to save and invest. A positive cash flow means you have a surplus you can direct toward your goals. On the other hand, a negative cash flow is a red flag that your expenses are higher than your income—a problem you have to fix before any real progress can be made. This honest assessment is the bedrock of any financial plan that’s actually going to work.

Stage Two: Defining What Matters Most to You

Alright, you’ve crunched the numbers and have a clear snapshot of your financial starting line. Now it’s time to give all that data a purpose. This second stage is where you bridge the gap between your money and your life, turning fuzzy daydreams into tangible, actionable goals.

It all boils down to one simple question: What do you really want?

Think of the financial data from Stage One as the fuel in your tank. Fantastic, you’re ready to go. But where are you going? Without a destination, you’re just burning gas, driving in circles without getting any closer to what truly matters.

This part of the process is less about spreadsheets and more about honest self-reflection. It’s where your personal values, ambitions, and priorities step into the spotlight and become the north star for every financial move you make from here on out.

Turning Vague Dreams into SMART Goals

“I want to be rich” or “I want to retire comfortably” are nice thoughts, but they aren’t goals. They’re wishes. To make real, measurable progress, your objectives need a solid structure. That’s where the SMART goal framework is so powerful—it’s a simple filter that transforms wishy-washy ideas into concrete targets.

A goal that actually works for you should be:

- Specific: Nail down exactly what you want. Instead of “save for a house,” get precise: “save $50,000 for a down payment on a three-bedroom house in my current neighborhood.”

- Measurable: Slap a number on it. Knowing your target is $50,000 means you can track your progress and know exactly how far you have to go.

- Achievable: Be real with yourself. A good goal should stretch you, but it shouldn’t be so out of reach that you lose motivation and give up.

- Relevant: Does this goal actually align with your bigger life plan? Make sure buying that house fits into the future you envision for yourself.

- Time-bound: Give yourself a deadline. “Save $50,000 within the next four years” adds a healthy dose of urgency and creates a clear timeline.

Applying this simple framework to every major financial objective—from retiring with confidence to paying for your kid’s college—is what gives you the clarity to build a plan that actually works.

Prioritizing What Truly Matters

Here’s the thing: you’ll probably have more than one goal, and they’ll all be competing for the same dollars. This is where you have to get tough and prioritize. You can’t do it all at once, so what’s most important right now?

Is retiring five years early more important than paying for a big wedding in cash? Is crushing high-interest credit card debt a bigger priority than maxing out your 401(k)? Answering these questions is a non-negotiable step in the process.

A financial plan without clear priorities is like a to-do list with a hundred “urgent” items—it’s overwhelming and totally ineffective. Prioritization forces you to aim your energy and money where they will have the greatest impact on your life.

This is also where your personal values come into play. For a growing number of people, especially younger generations, it’s not just about the money—it’s about making sure their finances reflect their principles. That might mean investing only in socially responsible companies or building charitable giving right into their budget.

The Power of Professional Guidance

Trying to define and prioritize your life’s biggest goals can feel overwhelming. That’s why bringing in a financial advisor early on can be a game-changer. Research shows that 55% of Americans believe getting professional advice between ages 25 and 39 is “highly important” for building long-term security.

Younger investors, in particular, are focused on this alignment of values, with about a third of Millennials looking for help to connect their finances with the causes they believe in. You can dig into more of these trends by reading these insights on financial planning trends.

A good advisor can help you spot your own blind spots, make sense of complex trade-offs, and gut-check your goals to make sure they’re both ambitious and realistic. Ultimately, this stage ensures your financial plan is a true reflection of you—not just your bank account, but your deepest hopes and dreams for the future.

Stage Three: Creating Your Personalized Strategy

You’ve mapped out your financial landscape and set your sights on a destination. Now comes the most critical part of the journey: drawing the actual map. This is where analysis turns into action, and all the data you’ve gathered becomes the blueprint for your financial future.

Think of it like building a house. In the first two stages, you surveyed the land (your starting point) and decided what kind of house you wanted (your goals). Now, it’s time to draft the detailed architectural plans—the ones showing exactly how every room, wire, and pipe will work together to build a home that’s both functional and perfectly suited to you.

Assembling the Core Components of Your Plan

A solid financial plan isn’t just a random collection of accounts. It’s a cohesive system where every part has a specific job. The goal is to pick and integrate different financial tools so they work in harmony, pushing you efficiently toward your objectives.

Your personalized strategy will almost always include these key pieces:

- A Sustainable Budget: This is the foundation. Using the cash flow analysis from Stage One, you’ll build a realistic plan for spending and saving that gives every dollar a purpose.

- An Investment Portfolio: Tailored to your risk tolerance and timeline, this is the engine that drives wealth growth. It’s designed to power long-term goals like retirement.

- An Insurance Safety Net: This is what protects your plan from life’s curveballs. We’re talking life, disability, and property insurance designed to safeguard your assets and income from the unexpected.

- A Debt Reduction Plan: If you’re carrying high-interest debt, your strategy needs a clear, actionable plan—like the snowball or avalanche method—to wipe it out efficiently.

These components are meant to work in concert, creating a balanced approach that builds wealth while protecting you from getting knocked off course.

Selecting the Right Financial Tools

Once the big pieces are defined, the next step is choosing the specific tools to bring the plan to life. This isn’t about chasing the latest hot stock or getting bogged down in complex products. It’s about methodically selecting the most effective and tax-efficient vehicles for your situation.

For instance, your retirement strategy might look something like this:

- Contribute to a 401(k) up to the employer match. This is the first stop, always. It’s free money and a guaranteed return on your investment. No exceptions.

- Max out an IRA. After grabbing the match, you might shift funds to a Roth or Traditional IRA, depending on your current income and what you expect to earn in the future.

- Go back and max out your 401(k). Once the IRA is full, you circle back to your 401(k) and keep contributing until you hit the annual limit.

This tiered approach ensures you’re squeezing every last drop of value from tax benefits and employer incentives. Similar strategies get applied to other goals, whether that’s using a 529 plan for education savings or setting up a trust for estate planning. Each tool is chosen for a reason.

A well-crafted plan transforms abstract goals into a concrete action plan. It answers the question, “What exactly do I need to do with my money each month to achieve the life I want?” This clarity is what turns financial planning from a source of stress into a tool of empowerment.

Stress-Testing Your Financial Blueprint

A great set of plans doesn’t just work on sunny days; it’s built to withstand a storm. A crucial part of this stage is testing your strategy against different “what-if” scenarios. What happens if the market tanks? What if you suddenly lose your job?

This is where PopaDex’s tools for scenario forecasting and financial planning are incredibly powerful. By running simulations, you can see how your plan holds up under various economic conditions, which lets you build in contingencies and make adjustments before you need them.

This proactive approach helps ensure your strategy is resilient and adaptable. It gives you confidence that your plan can handle life’s inevitable ups and downs without derailing your long-term progress. In the end, this stage delivers a clear, actionable roadmap designed for one person: you.

Stage Four: Putting Your Financial Plan into Motion

You’ve got the blueprint. Now it’s time to break ground. This stage is all about execution—turning your carefully designed strategy into real-world action. A brilliant plan is useless if it just collects dust in a folder; this is where you actually start building your financial future.

For many people, this is the toughest step. The gap between knowing what to do and actually doing it can feel massive, often leading to procrastination or decision paralysis. Getting this stage right is what transforms your plan from a document into a reality.

From Blueprint to Reality

Think of this stage as your personal project checklist, with every task pulled directly from the plan you just built. It’s the practical, hands-on work that bridges the gap between theory and practice. Taking these steps one by one is how you build momentum and start seeing real progress.

Your implementation checklist will probably include a series of concrete actions like these:

- Opening new accounts: This could be a Roth IRA for retirement, a high-yield savings account for your emergency fund, or a 529 plan for college savings.

- Adjusting retirement contributions: Logging into your 401(k) portal to bump your contribution from 6% to 10% is a perfect example of a small action with a huge long-term impact.

- Purchasing insurance: This means actually filling out and finalizing the applications for that life or disability insurance policy you identified.

- Creating estate documents: It’s time to work with an attorney to draft your will or set up a trust, ensuring your assets are handled exactly as you wish.

Every task you check off is another brick laid in the foundation of your financial security.

Overcoming the Implementation Hurdle

So why do so many of us get stuck here? The truth is, there’s a huge difference between feeling confident and being truly prepared. While 95% of wealthy Americans report feeling confident about their finances, that bravado crumbles under scrutiny. In fact, only 21% feel confident in every aspect of their plan.

This shows a major disconnect between good intentions and real action. For instance, while 87% feel prepared to pass on wealth, over half of them don’t even have a formal estate plan. You can dig into more of these surprising findings in this report on the planning gap between confidence and action.

This hesitation usually comes down to a few common mental roadblocks.

Procrastination is the enemy of progress. The single best way to beat it is to take one small, manageable step immediately. Don’t try to do everything at once; just open one account or make one phone call today.

To move forward, you have to break massive tasks into smaller, less intimidating steps. Instead of putting “get estate plan” on your to-do list, your first step might just be “research three local estate attorneys.” This approach makes the whole process feel achievable and helps you build momentum.

In PopaDex, you can use the goal-setting features to create mini-milestones for each step. This gives you a clear path to follow and lets you celebrate the small wins along the way.

Stage Five: Monitoring and Adapting Your Plan for Life

You’ve done the hard work. You’ve built a solid financial strategy and set it in motion. That’s a huge win, but your journey isn’t over. The final—and arguably most important—stage is all about stewardship. It’s about treating your plan not as a static document you file away, but as a living, breathing guide that evolves with you.

Think of your financial plan like the GPS in your car. You’ve plugged in your destination and it’s mapped out the best route. But what happens when you hit unexpected traffic, a sudden detour, or just decide to take a more scenic road? You adjust. This monitoring stage is all about making those real-time adjustments to make sure you still get where you want to go.

The Importance of Regular Reviews

This is what keeps your plan relevant. Without regular check-ins, even the most brilliant strategy will eventually fall out of sync with your life. This isn’t just about glancing at your investment performance once a quarter; it’s a complete physical for your financial health.

A comprehensive review, which you should do at least once a year, needs to cover a few key areas to ensure everything is still working in harmony:

- Goal Progress: Are you still on track to hit your targets? Seeing your progress toward big milestones is crucial for staying motivated and knowing when to tweak your approach.

- Budget and Cash Flow: Has your income gone up or have your expenses changed? A quick review makes sure your budget still reflects what’s actually happening with your money.

- Investment Allocation: Has the market pushed your portfolio out of whack? Rebalancing is how you bring it back in line with your original risk tolerance.

- Insurance Coverage: Are you paying for protection you don’t need anymore, or do you now have gaps in your coverage? Life changes, and so should your safety net.

Using a tool to keep tabs on your progress makes this whole process feel less like a chore. For example, PopaDex’s financial goal tracker lets you see where you stand in real-time, turning a dreaded annual task into a simple, ongoing check-in. It helps you spot the small issues before they snowball into big problems.

When Life Events Trigger a Financial Review

While annual reviews are a great baseline, some life events are so significant they demand an immediate update to your financial plan. These are the moments that can completely change your goals, income, and responsibilities, making your old plan obsolete overnight.

Think of your financial plan as a custom-tailored suit. When your body changes, you don’t keep wearing a suit that no longer fits—you get it altered. Major life events are those moments that require an immediate financial refitting.

Here are the key life events that should always trigger an immediate plan review:

- Marriage or Divorce: Merging finances with a partner or separating them requires a ground-up rebuild of your budget, goals, and even your will.

- Birth or Adoption of a Child: A new family member creates immediate needs for things like college savings, more life insurance, and updated estate planning.

- Significant Career Change: A new job, a big promotion, or starting your own business will have a massive impact on your income, benefits, and retirement strategy.

- Receiving an Inheritance: A sudden windfall needs a deliberate plan. You have to decide how to best invest, save, or spend it so it aligns with your long-term vision.

- Major Purchase or Sale: Buying a home or selling a business is a huge financial shift that will ripple through every part of your plan.

This final stage is really a continuous loop: monitor, review, and adapt. It’s what ensures your financial plan remains a powerful tool that guides you effectively through all of life’s inevitable twists and turns.

Your Financial Planning Questions Answered

As you navigate the financial planning stages, it’s totally normal for questions to pop up. Getting clear on these common points gives you the confidence to make smart moves and stick with your strategy for the long haul. Let’s tackle some of the most frequent ones.

How Often Should I Review My Financial Plan?

Think of it this way: your financial plan needs a check-up at least once a year. This annual review is your chance to make sure your strategy still makes sense with what the market is doing and the progress you’ve made.

But some things can’t wait a year. You should schedule an immediate review anytime a major life event happens. These are big moments that can totally shift your financial picture, like:

- Getting married or divorced

- Welcoming a new child

- Switching jobs or getting a big pay raise (or cut)

- Receiving an inheritance or another unexpected sum of money

When these things happen, your old plan might become obsolete overnight. A quick update is essential to get back on the right track.

Can I Do Financial Planning Myself, or Do I Need an Advisor?

You can absolutely get the ball rolling on your own. In fact, the early stages—gathering your documents, calculating your net worth, and sketching out some initial goals—are fantastic DIY projects. It puts you in the driver’s seat and forces you to get familiar with your own numbers.

Where a qualified financial advisor really shines is in the more complex stuff, like crafting a sophisticated investment strategy, navigating the tax code, or managing risk. They bring an objective, expert eye to the table, helping you spot blind spots and ensuring your plan is as robust and efficient as possible.

While every stage is crucial and builds upon the last, many experts argue that Stage Two (Defining Your Goals) is the most important. A plan without clear, meaningful goals is like a map without a destination; your personal objectives are the foundation for every strategy that follows.

What Is the Most Important Stage of Financial Planning?

Every one of the financial planning stages is a critical link in the chain, but if you had to pick one, it would be the goal-setting phase. Without a clear “why,” your financial plan is just a collection of numbers with no real direction.

This is the stage where you connect your money to your life. The goals you define here—buying a house, retiring early, traveling the world—become the bedrock for every single strategy that comes after. It transforms the process from a tedious chore into a personalized roadmap to the life you actually want to live, which is a powerful motivator.

Free Financial Planning Templates

Kickstart each stage of your financial plan with the right tools:

- Personal Budget Template for Excel — 50/30/20 budget with automatic category tracking

- Irregular Income Budget Template — Built for freelancers and gig workers with variable pay

- Net Worth Statement Template — Track your assets vs liabilities over time

- Net Worth Tracker for Google Sheets — Real-time dashboard with automated calculations

Ready to master your financial planning stages with a tool that grows with you? PopaDex helps you track your net worth, monitor your goals, and see your entire financial picture in one secure place. Get the clarity you need to move confidently from one stage to the next. Start your free trial today.