Our Marketing Team at PopaDex

How to Automate Savings and Build Wealth Effortlessly

Automating your savings is one of those simple, almost boring, strategies that can completely change your financial trajectory. It’s all about setting up automatic transfers from your checking account to your savings or investment accounts.

By making saving a default, non-negotiable action, you’re taking willpower completely out of the equation. Wealth starts to build in the background, consistently, without you having to think about it.

Why Automating Your Savings Is a Financial Game Changer

Let’s be honest: manually saving money is a constant fight against our own human nature. Every payday, you’re faced with the same tired choices. Do I save now? Spend a little? Maybe I’ll just save whatever’s left over at the end of the month… which, as we all know, often ends up being nothing.

That whole process is draining, and it almost never leads to consistent results.

Learning how to automate your savings fundamentally changes this dynamic. You’re flipping the script from an active, willpower-draining chore into a passive, background habit. The core idea is simple but incredibly profound: Pay yourself first.

Overcoming Decision Fatigue

Every single day, we’re bombarded with tiny decisions that slowly chip away at our mental energy. Automating your financial contributions puts an end to the daily “should I save or not?” debate. The money is already moving and working for you before you even have a chance to second-guess the plan.

Automation transforms saving from a recurring decision into a default action. It’s the financial equivalent of setting your thermostat—you establish a comfortable setting once and let the system maintain it effortlessly.

This shift has a massive psychological impact. It frees up your mental bandwidth to focus on the bigger picture, like growing your career or refining your investment strategy, instead of getting bogged down in the tedious mechanics of moving money around. If you want to dive deeper into this concept, check out this piece on the power of automated financial workflows and how they drive efficiency.

A New Era of Financial Tools

The good news is that the tools available today make setting this up easier than ever. This isn’t just a passing trend; it’s a major evolution in how we manage our personal finances.

The global financial automation market is projected to hit $20.7 billion by 2032, growing at a rate of over 14.2% each year. This boom means more accessible and powerful tools are constantly being developed for everyday savers like us. You can read more about these financial automation trends on VenaSolutions.com.

Here’s a quick look at the core methods we’ll be diving into. Think of this as your starting toolkit.

Your Savings Automation Toolkit at a Glance

This table gives you a quick summary of the most effective methods for automating savings, which we’ll explore in detail throughout this guide.

| Automation Method | Best For | How It Works |

|---|---|---|

| Direct Deposit Splitting | Setting a non-negotiable savings base right from your paycheck. | Your employer sends a fixed amount or percentage of your pay directly to your savings account. |

| Recurring Transfers | Consistently moving money on a fixed schedule you control. | You schedule automatic transfers from your checking to savings account on specific dates. |

| Rules-Based Automation | Saving small amounts based on your daily spending habits. | Apps round up purchases, save a percentage of deposits, or split bills automatically. |

Putting a system in place to automate your savings gives you a serious advantage. It locks in consistency, speeds up progress toward your goals, and builds a rock-solid financial foundation. Now, let’s get into the specific strategies you can use to make it happen.

Building the Foundation for Your Automated Savings Plan

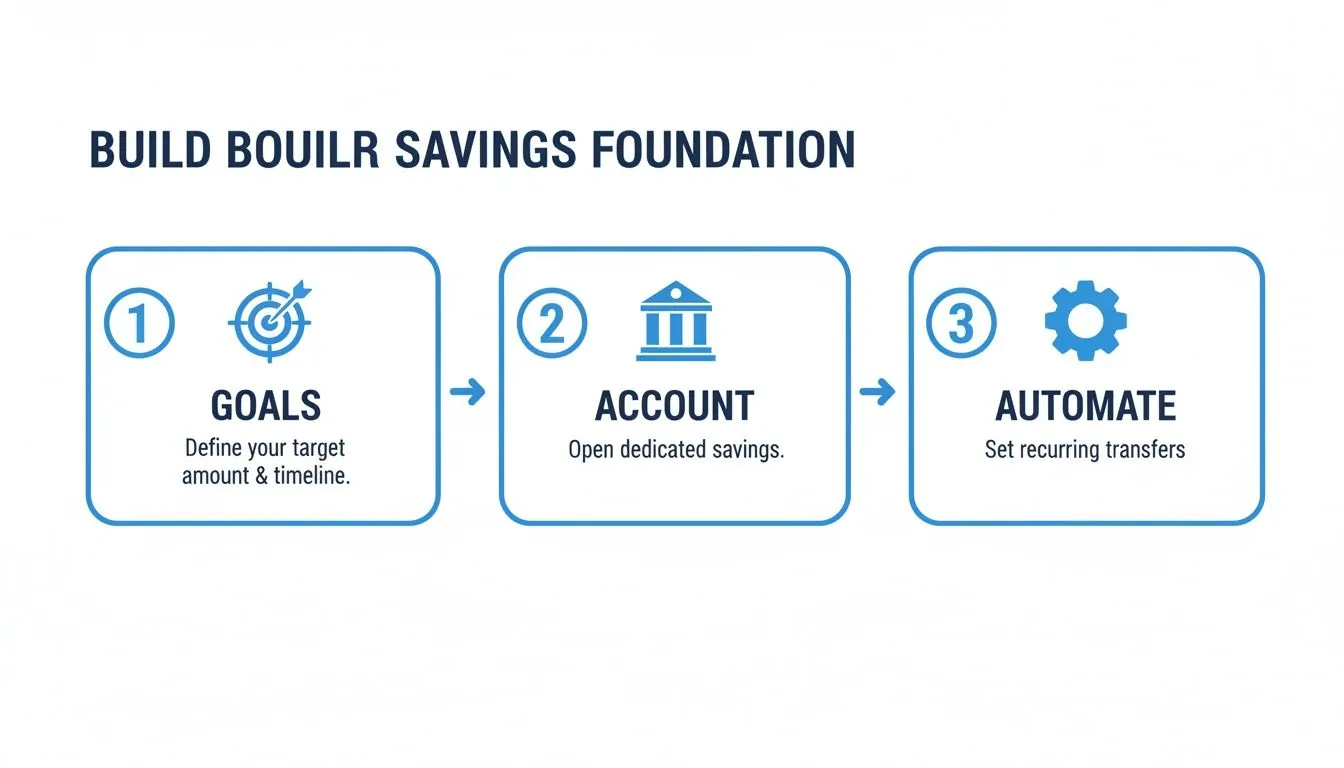

Before a single dollar moves on its own, you need to give it a destination. An automation system without a clear purpose is like a high-speed train with no tracks—it’s impressive, but it’s not going anywhere useful. The first real step is to give every dollar a job.

So, what are you really working toward? A $10,000 down payment on a house in three years? Maybe a $3,000 fund for that trip to Southeast Asia you’ve been dreaming about next summer? Vague goals like “save more” are easy to ignore and lack the motivational punch you need to stick with it.

Get specific. Attach real numbers and hard deadlines to your goals. This simple act transforms a fuzzy wish into a concrete, measurable objective. That clarity is what will keep you on track when the temptation to raid your savings for something else pops up.

Choose the Right Home for Your Savings

Once you know your “why,” your money needs a proper home—and that home can’t be your everyday checking account. Mixing your savings with your spending money is a recipe for disaster, making it far too easy to accidentally spend what you’ve set aside. The trick is to create a little bit of healthy friction by keeping them separate.

This is where a High-Yield Savings Account (HYSA) is a game-changer. Unlike the dusty old savings accounts from traditional banks that pay next to nothing, HYSAs offer significantly higher interest rates, known as the Annual Percentage Yield (APY). This means your automated savings don’t just sit there; they actually start growing and compounding all on their own, helping you hit your goals that much faster.

Setting up a separate, high-yield account is non-negotiable. It creates a psychological barrier that protects your savings from impulse buys while simultaneously putting your money to work for you.

When you’re shopping for an HYSA, a few key features will tell you if you’ve found a winner for your automation setup.

Your HYSA Selection Checklist

Look for an account that checks these boxes to build a solid foundation:

- Competitive APY: Don’t settle. Aim for an interest rate that crushes the national average. A higher APY means more free money is being added to your balance every month.

- No Monthly Maintenance Fees: Fees are the enemy of growth and can quickly wipe out the interest you’re earning. Prioritize accounts that are genuinely free to own.

- Low or No Minimum Balance: You shouldn’t be punished for starting small. Pick an account that lets you kick off your automation journey with whatever amount you’re comfortable with.

- FDIC Insurance: This is a must-have. Make sure the bank is FDIC-insured, which protects your deposits up to $250,000. It’s standard for any reputable bank, but it’s always smart to double-check for peace of mind.

With your goals clearly defined and a high-performing savings account ready to go, you’ve officially built the launchpad for your automation system. Now you’re ready for the fun part: setting up the engines that will move your money effortlessly.

Putting Your Savings on Autopilot with Your Bank

You don’t need a bunch of fancy apps to start building real wealth. Truthfully, the most powerful tools are probably sitting right inside your online banking portal, waiting for you to use them. These are the foundational moves for a true “set-it-and-forget-it” savings plan, getting your money to work for you without any ongoing effort.

The single most effective trick in the book? The direct deposit split. This is the purest definition of “paying yourself first.” Before your paycheck even has a chance to hit your checking account, a piece of it gets automatically rerouted directly to your savings. That money never co-mingles with your spending cash, so the temptation to use it is completely gone.

Automate with Direct Deposit Splits

Getting this set up is usually pretty simple. Just ask your HR department for the right form or look for an option in your company’s payroll portal to add a second bank account for direct deposits. From there, you can split it by a fixed dollar amount (like $200 per paycheck) or a percentage (maybe 10% of your take-home pay).

Splitting your direct deposit makes saving a non-negotiable, automatic action. Think of it as an automated bill you pay to your future self, making sure your own goals get top priority.

This method is gold because it takes willpower completely out of the savings equation. You just learn to live on whatever lands in your checking account, while your savings grow quietly and consistently in the background.

This simple flow breaks down the core process of getting your savings machine up and running.

As you can see, automation is that final, essential step that links your goals to your savings account, creating a system that practically runs itself.

Schedule Recurring Bank Transfers

If splitting your paycheck at the source isn’t an option, the next best thing is a scheduled recurring transfer. This is just a simple instruction you give your bank to move a set amount of money from checking to savings on a regular schedule you choose.

The key is to time it right. A killer strategy is to schedule the transfer for the day after you get paid. This mimics the “out of sight, out of mind” power of a direct deposit split, whisking the money away before you even notice it’s there.

Let’s look at a couple of real-world examples:

- The New Grad: Sarah just landed her first job and is focused on building a $5,000 emergency fund. She sets up an automatic transfer of $150 from her checking to her high-yield savings account. It’s scheduled for the 1st and 15th of every month, the days right after her paychecks hit.

- The Freelancer: Alex has an unpredictable income stream but needs to be disciplined about saving for taxes. Every time a client pays him, he manually moves 25% into a separate savings account for taxes. On top of that, he automates a recurring $200 weekly transfer to his long-term investment fund, creating a consistent savings baseline no matter how lumpy his income is.

These straightforward, bank-level automations are the bedrock of any solid financial plan. Once you get these basics locked in, you can start to explore even more ways to automate your finances with smarter tools and rules. The most important thing is just to start with these reliable methods to build unstoppable momentum.

Using Fintech Apps for Smarter Savings Automation

While direct bank transfers are the bedrock of any solid automation plan, modern fintech apps add an exciting layer of intelligence and—dare I say—fun. These tools go way beyond simple scheduled transfers. They tap into your everyday behavior to find small, hidden opportunities to save.

Suddenly, saving isn’t a chore you have to remember. It becomes an engaging background activity, almost like a rewarding game. Instead of feeling the sting of moving a big chunk of cash each month, these apps help you build wealth through dozens of tiny actions you’ll barely notice.

The Power of Micro-Savings and Round-Ups

One of the most popular features driving this trend is the “round-up.” It’s simple, but brilliant. Let’s say you buy a coffee for $3.65. An app with this feature will automatically round the purchase up to the nearest dollar ($4.00) and sweep the $0.35 difference straight into your savings or investment account.

Sure, $0.35 doesn’t sound like much. But think about how many times you swipe your card in a week. Across dozens of transactions, you could easily be setting aside an extra $30-$50 a month without feeling any pinch at all. You’re literally turning your spending habits into a savings engine.

Round-up automation is the financial equivalent of finding spare change in your couch cushions, except it happens dozens of times a week and is automatically deposited for you. This is how you automate savings without changing your lifestyle.

This micro-savings approach is perfect if you feel like you don’t have enough “extra” money to put away in big lump sums. It’s proof that you can build serious savings with amounts you’ll honestly never miss. If you’re looking for tools with these kinds of features, our guide on the best free budgeting apps is a great place to start.

Creating Your Own Savings Rules

The real magic of today’s fintech apps is their support for custom, rules-based automation. This is where you get to be the architect of your savings strategy, tailoring it to your life and goals. Think of them as “if this, then that” triggers that can connect your saving goals to almost any activity.

Here are a few ideas to get your gears turning:

- Paycheck Percentage: Set a rule to automatically transfer 10% of any deposit over $500 that hits your checking account. This is a game-changer for freelancers or anyone with an irregular income.

- Activity-Based Savings: Feeling motivated? Create a rule to save $5 every time you check in at the gym or your health app logs a completed workout. It’s a great way to link your physical and financial well-being.

- Guilty Pleasure Tax: Trying to cut back on takeout? Make a rule to automatically save $10 every time you spend money at your go-to pizza place.

This isn’t some quirky personal finance hack; it’s a proven principle borrowed from the business world. Studies show that 70% of companies using financial automation report significant cost savings and better cash flow. The same logic that helps a business’s bottom line can powerfully boost your personal savings. You can dig into more of these financial automation stats over at Quadient.com. By setting up these smart rules, you’re just applying a proven corporate strategy to your own wealth-building.

Tracking Your Progress and Staying Motivated

Getting your automated savings system up and running is a massive first step. But let’s be honest, that initial burst of excitement can wear off. The real secret to making this a long-term habit is seeing tangible results.

When your system is humming along quietly in the background, you need a way to see just how much good it’s doing. This isn’t about obsessing over every dollar; it’s about connecting those small, consistent actions to the big-picture growth of your net worth. Watching that number climb is the ultimate motivation.

Visualizing Your Financial Growth

The best way to stay plugged in is to use a tool that brings all your accounts into one place. Think of a net worth tracker as the ultimate scoreboard for your financial life. It gives you a clear, real-time dashboard showing everything from your growing savings and investments to your shrinking debts.

For instance, a tool like PopaDex pulls it all together, showing you exactly how your automated contributions are directly pumping up your overall net worth.

A visual dashboard like this changes the game. Your savings are no longer just a number in an account; they’re a chart moving up and to the right. It makes your progress impossible to ignore and helps you stick with the plan, especially on those days when you might feel a little discouraged.

Connecting Automation to Net Worth

It’s incredibly powerful to see the direct impact of your strategy. Every automated transfer, every “round-up,” and every paycheck split is a small win. A good tracker gathers all these little victories and displays them as real, meaningful progress toward your financial goals.

Tracking your net worth creates the feedback loop that keeps you motivated. It’s concrete proof that your system is working, turning the quiet, consistent act of saving into something you can see and celebrate.

This kind of visibility also helps you make smarter moves. You can quickly see which automation rules are delivering the biggest bang for your buck and spot opportunities to fine-tune your approach. If you’re looking for a dedicated tool to help, a specialized financial goal tracker provides the structure you need to set, monitor, and crush your objectives one by one.

At the end of the day, tracking is about more than just numbers—it’s about celebrating how far you’ve come. Acknowledging these milestones, big or small, reinforces the powerful habits you’re building. It’s the final piece of the puzzle that ensures your automated savings plan doesn’t just start strong but keeps building your wealth for years to come.

Got Questions About Automating Your Savings? We’ve Got Answers.

Jumping into a new way of managing your money is bound to bring up a few questions. That’s a good thing. Getting clear on the details before you connect accounts and set up rules is the final step to building a savings system you can trust completely.

Learning to automate your savings is part strategy, part technology. Let’s tackle the most common questions that pop up.

Is It Really Safe to Connect My Bank Account to These Apps?

Yes, as long as you stick with reputable, well-established players. The leading fintech companies know their entire business hinges on security. They use bank-level protections like 256-bit AES encryption to safeguard your data, both when it’s sitting still and when it’s on the move. Many also insist on two-factor authentication (2FA) to add another lock to your financial front door.

Most modern apps don’t handle the connection themselves. They use trusted intermediaries like Plaid or Finicity. This means the savings app never actually sees or stores your banking username and password. All they get is a secure token that grants them limited, read-only access.

Think of it like a digital valet key. The app gets just enough access to see your transactions for round-ups or to pull the transfers you’ve authorized, but it can’t take your account for a joyride.

Before you link anything, run a quick safety check. Make sure the app offers FDIC insurance for any cash it holds on your behalf, and spend a few minutes reading recent user reviews to get a sense of its reliability.

Can I Automate Savings if I Have an Irregular Income?

Absolutely. In fact, for anyone with a fluctuating income, automation isn’t just a convenience—it’s a game-changer. The trick is to shift your thinking from saving a fixed dollar amount to saving a fixed percentage. This builds a system that automatically flexes with your financial reality.

Instead of a rigid $200 transfer every two weeks, you can set a rule to move a percentage of every deposit into your savings account the moment it lands.

- For freelancers: Set up a rule in a fintech app to automatically route 20% of any deposit over $100 into a separate account. This way, you’re instantly setting aside money for taxes and personal goals with zero effort.

- For salespeople: When that huge commission check finally hits, your percentage-based rule scales up your savings right along with it. You capitalize on the good months without even thinking about it.

This “pay yourself first” approach means you naturally save more when times are good and ease back during leaner periods, all without having to constantly log in and make manual adjustments. You can even layer on a round-up feature to keep the savings momentum going between larger payments.

How Often Should I Tweak My Savings Automations?

Think of it as a quick financial check-up, not a constant project. A good rhythm is to review your automations once or twice a year, and always after a major life event. The goal isn’t to endlessly tinker, but to make sure your system is still aligned with where your life is headed.

Your automated savings plan should grow and change right along with you.

- Got a raise? This is the perfect moment to bump up your automated transfer amount or percentage. It’s the single best way to combat lifestyle creep and put that extra income to work.

- Paid off a big debt? Awesome. Immediately redirect the money you were sending to that car loan or student debt straight into your savings automation. Don’t let it get absorbed into your daily spending.

- Starting a new job? Your first priority should be updating your direct deposit splits and any other payroll-based automations you had set up.

These simple, periodic reviews ensure your system stays optimized and works as hard as you do for your financial future.

Ready to watch your automated savings translate into real, measurable growth? PopaDex gives you a clear, visual dashboard of your entire financial world, so you can see your net worth climb with every automatic transfer. Track your progress and stay motivated by signing up for free.