Our Marketing Team at PopaDex

How to Avoid Currency Conversion Fees and Save Money Abroad

Want to avoid currency conversion fees? It’s simpler than you think. The golden rule is to always pay in the local currency when you’re abroad. Combine that with a card that has no foreign transaction fees and you’re already ahead of the game. For frequent travelers or digital nomads, modern multi-currency accounts are the final piece of the puzzle.

This goes beyond saving a few cents; it’s a strategy to stop the quiet bleed of hidden charges that inflate every international purchase you make.

The Hidden Fees Draining Your Travel Budget

Have you ever come back from a trip, looked at your bank statement, and had that sinking feeling that the numbers just don’t add up? You’re not imagining things. The culprit is almost always a string of small, nearly invisible charges called currency conversion fees. These costs silently chip away at your money every time you swipe your card, pull cash from an ATM, or send money across a border.

Let’s put this into a real-world context. You’re in Paris, settling a hotel bill for €200. The card machine gives you a choice: pay in Euros (€) or your home currency, say US Dollars ($). Paying in dollars feels familiar and easy, but that convenience is a costly trap. You’ve just encountered Dynamic Currency Conversion (DCC), one of the most common ways travelers get fleeced.

Key Strategies for Avoiding Conversion Fees

Here’s a quick look at the most effective ways to save money on currency conversion, giving you a clear overview before we dive into the details.

| Strategy | Potential Savings | Best For |

|---|---|---|

| Always Pay in Local Currency | 3-8% on each transaction | Every traveler using a card abroad. |

| Use Fee-Free Cards | 1-3% on all foreign spending | Anyone who travels, even occasionally. |

| Multi-Currency Accounts | 1-5% vs. traditional banks | Digital nomads, expats, frequent travelers. |

| Peer-to-Peer FX Services | Up to 8x cheaper than banks | Sending larger sums of money internationally. |

By mastering these four areas, you can virtually eliminate the unnecessary fees that eat into your travel budget.

Why Do These Fees Even Exist?

At its heart, the foreign exchange market is a colossal global business. Projections show that by 2025, global FX trading will reach an astonishing $9.6 trillion per day. Banks, card networks, and merchants all want a piece of that action, so they add their own markups to the exchange rate.

When you accept DCC, the merchant’s bank sets its own terrible exchange rate, often padding it with a fee of 3-5% or more. That €200 hotel bill? You could be paying an extra $6-$10 just for picking the “convenient” option.

The single most effective habit you can build is to always refuse the offer to pay in your home currency. Just by consistently choosing the local currency, you can sidestep up to 95% of these inflated DCC fees.

Your Roadmap to Saving Money

Understanding how this works is the first step. The great news is that avoiding these fees is completely within your control. You don’t need a degree in finance—just a few smart habits and the right tools.

The strategies we’re about to cover are practical and easy to implement. We’ll look at everything from the best cards to keep in your wallet to using modern financial apps that give you a fair shake. And if you’re moving larger amounts of money, it’s worth exploring the cheapest way to send money internationally with platforms designed for just that.

This guide will give you a clear action plan, breaking down:

- The best cards for international travel that have zero foreign transaction fees.

- How to confidently say “no” to DCC at card machines and ATMs.

- Using fintech solutions like multi-currency accounts to get much better exchange rates.

By the end, you’ll know exactly how to protect your money and make every dollar, pound, or euro go further on your next adventure.

Picking the Right Cards for International Travel

The most powerful tool for slashing unnecessary fees is probably already in your wallet—or at least it should be. Choosing the right credit and debit cards is hands-down the most critical decision you’ll make before you travel, shop on a foreign website, or send money overseas. This choice alone determines whether you’re paying the bank’s hidden markups or keeping that cash for yourself.

Forget your standard bank card. Seriously. It’s likely costing you an extra 1-3% on every single transaction you make abroad. The real goal is to build a small, strategic lineup of cards specifically designed for international use.

The Must-Have: A No-Foreign-Transaction-Fee Credit Card

A credit card with no foreign transaction fees (FTFs) is completely non-negotiable for anyone crossing borders. These cards should be your go-to for hotels, restaurants, and any larger purchases where you can rack up rewards without paying extra for the privilege.

Think about it this way: a typical credit card hits you with a 3% FTF. On a trip where you spend $2,000, that’s an extra $60 straight to your bank for absolutely nothing. A no-FTF card, like a Chase Sapphire Preferred or Capital One Venture, completely wipes out this cost. They handle the currency conversion on their end using a rate that’s incredibly close to the real mid-market rate—far better than anything a local merchant will ever offer you.

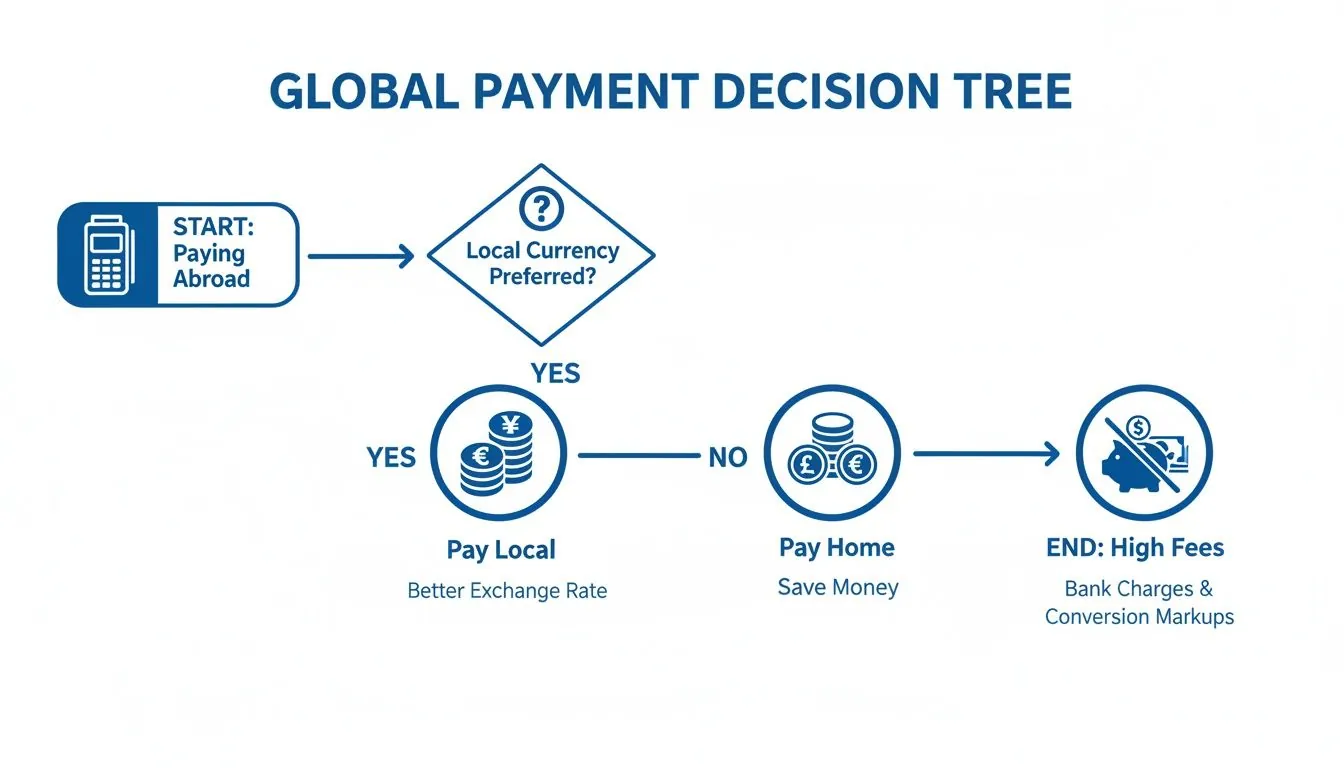

This simple flowchart lays out the crucial choice you’ll face at every payment terminal and shows exactly why picking the local currency is the key to saving money.

As you can see, letting the machine charge you in your home currency triggers something called Dynamic Currency Conversion, which comes with terrible exchange rates. Always, always choose to pay in the local currency.

Your Go-To for Cash: Travel-Friendly Debit Cards

While credit cards are perfect for most purchases, you’re going to need cash at some point. This is where a travel-focused debit card is an absolute game-changer. Using your regular debit card at a foreign ATM can unleash a triple-whammy of fees: a foreign transaction fee from your bank, an ATM usage fee from your bank, and another service fee from the local ATM operator. It’s ridiculous.

A much smarter move is to use a debit card from a provider like Charles Schwab Bank, which is famous for reimbursing all ATM fees worldwide. This means you can pull out local currency from pretty much any machine without even thinking about the cost. It’s the best way to dodge the horrible exchange rates and high commissions you’ll find at those currency exchange kiosks in airports and tourist traps.

Pro Tip: Never, ever use a credit card for ATM withdrawals. These are treated as a “cash advance,” meaning they start racking up sky-high interest the second the money is in your hand, on top of a nasty cash advance fee. Just don’t do it.

So, Which Cards Are Right for You?

The perfect combination of cards really depends on your travel style and spending habits. Here’s a quick breakdown to help you figure out what belongs in your wallet.

| Card Type | Best For | Key Benefit | Potential Downside |

|---|---|---|---|

| No-FTF Credit Card | Daily spending, hotels, flights | Earns rewards, no transaction fees | Requires good credit, high interest on balances |

| Travel Debit Card | ATM cash withdrawals | Reimburses ATM fees worldwide | Few rewards, requires opening a new account |

| Prepaid Travel Card | Budget-conscious travelers | Lock in exchange rates, limit spending | Often has poor rates and sneaky hidden fees |

For most people, pairing a no-FTF credit card for purchases with a fee-reimbursing debit card for cash is the golden ticket. This setup covers all your bases and ensures you’re always getting the best possible deal.

Of course, managing multiple accounts across borders—especially for expats and digital nomads—can get tricky. Our guide to expat banking dives deeper into handling finances when you live a global life.

Ultimately, the goal is to have financial tools that work for you, not against you. A few minutes of research before your next trip can easily save you hundreds of dollars down the road.

How to Sidestep the Dynamic Currency Conversion Trap

Picture this: you’re at a restaurant in Rome, feeling great after a fantastic meal. The waiter brings the card machine, and a question pops up: “Pay in EUR or USD?” It seems helpful, right? A thoughtful offer to show you the cost in your familiar home currency.

Don’t fall for it. This is a calculated and costly trap known as Dynamic Currency Conversion (DCC).

This “service” is one of the most common ways travellers get fleeced, and knowing how to dodge it is fundamental to smart spending abroad. When you choose to pay in your home currency, you’re not getting a favour. You’re giving the merchant’s bank—not your own—permission to handle the currency conversion on the spot. They do this using their own terrible exchange rate, which can be 3-8% worse than the rate your bank would give you.

That difference adds up fast. On a €500 hotel bill, agreeing to DCC could easily cost you an extra $25-$40 for absolutely nothing. It preys on our desire for familiarity, but the cost of that comfort is always steep.

Recognizing and Refusing DCC in the Wild

The key to avoiding this trap is simple vigilance. DCC can show up in a few different disguises, and you need to be ready for it every single time you pull out your card.

You’ll see it on payment terminals at:

- Restaurants and cafes

- Retail stores and souvenir shops

- Hotel check-out desks

- Even at ATMs when you’re withdrawing cash

The prompt will always be some version of asking if you want to pay in the local currency or your home currency. Sometimes it’s a clear question, but other times it’s just two buttons on the screen—one with the local symbol (€, £, ¥) and one with your own ($).

There’s only one rule, and it’s non-negotiable: Always, without exception, choose to pay in the local currency. This forces your own bank or card provider to handle the conversion, and they’ll do it at a much more competitive rate.

What to Say and Do at the Point of Sale

Sometimes a well-meaning (but misinformed) cashier will try to “help” by pressing the home currency button for you. You need to be proactive.

As you hand over your card, just say, “Please charge me in Euros,” or whatever the local currency is. This sets the expectation right away.

If the machine is handed to you, take a beat and actually read the screen.

- Look for currency codes: Find the option that shows the local currency (e.g., EUR, GBP, JPY, THB).

- Pick the right button: It’s usually the green or “accept” button that corresponds to the local amount.

- Check the receipt: Before you sign or pop in your PIN, double-check that the final amount is listed in the local currency. If it’s not, ask them to cancel the transaction and run it again correctly.

What if the Machine Chooses for You?

On rare occasions, a merchant’s terminal might be rigged to automatically select DCC without giving you a choice. If you check your receipt and see you were charged in your home currency against your wishes, you have the right to challenge it.

Ask the merchant to void the transaction and re-process it correctly. If they refuse or can’t, make a note on the receipt itself (something like, “Charged in USD without consent”) before you sign it. Then, get in touch with your card issuer later to explain what happened. Most banks know this is a shady practice and can often help you out.

By making “pay in local” a hard-and-fast habit, you take control back from opportunistic payment processors and keep your money where it belongs: in your pocket.

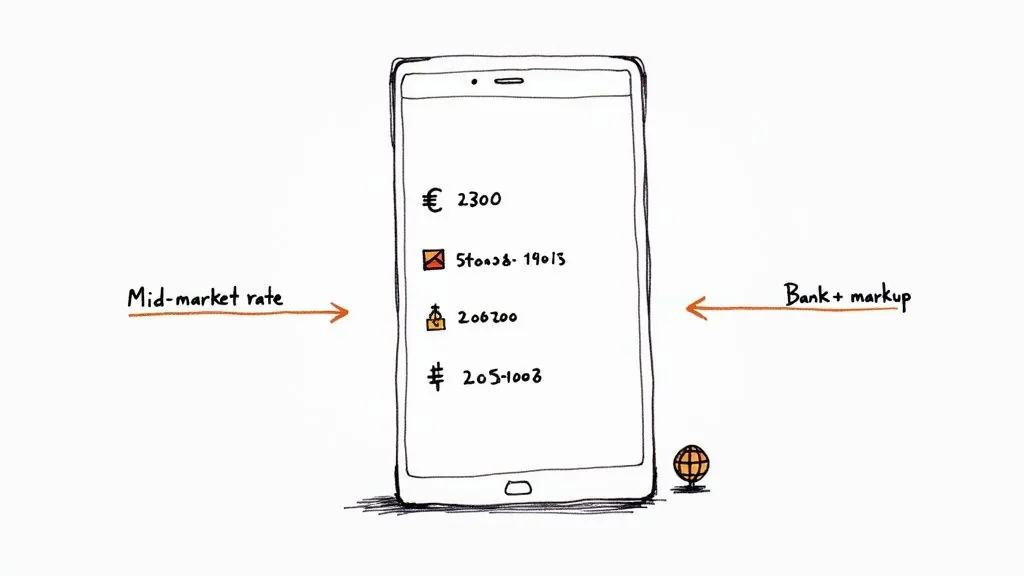

Tap Into Fintech for Mid-Market Exchange Rates

For the longest time, traditional banks had a stranglehold on international money, padding exchange rates with hefty markups that quietly ate into your funds. But the rise of financial technology (fintech) has blown that system wide open, giving regular people access to the kind of rates once reserved for massive financial institutions.

This shift puts the power right back where it belongs: in your hands.

Modern platforms like Wise and Revolut built their entire business on a simple, disruptive idea—you deserve the real exchange rate. They operate on the mid-market rate, which is the exact midpoint between what buyers are willing to pay and sellers are willing to accept for a currency. Think of it as the “true” rate you see on Google or Reuters, with no hidden fees baked in.

How Multi-Currency Accounts Have Changed the Game

At the heart of this fintech revolution is the multi-currency account. Instead of being stuck with a single bank account in your home currency, these apps let you open local bank details and hold balances in dozens of different currencies at the same time.

Let’s say you’re a freelancer in the U.S. working with a client in the UK. The old way involved your client sending you British pounds, which your U.S. bank would then convert into dollars at a terrible rate. Now, you can just give them UK bank details (a sort code and account number) right from your Wise or Revolut app. The money lands in your account as pounds, with zero conversion and zero fees.

From there, you’re in the driver’s seat. You can:

- Hold the pounds until you need them for a future trip to London.

- Spend them directly with a linked debit card when you’re in the UK, bypassing conversion fees entirely.

- Convert them to dollars (or any other currency) inside the app, locking in the mid-market rate whenever you decide the time is right.

This is what true financial control looks like. You get to decide when and how your money is exchanged, not a bank looking to skim a profit off the top.

The Real-World Savings in Action

Let’s put some numbers to this to see just how much you can save. Imagine you need to send $1,000 USD to a friend’s bank account in Germany, and it has to arrive as Euros (€).

| Transfer Method | Exchange Rate Markup | Transfer Fee | Final Amount Received (Approx.) |

|---|---|---|---|

| Traditional Bank | 2% - 4% markup | $25 - $45 | €875 - €895 |

| Fintech App (e.g., Wise) | ~0% markup (mid-market) | ~$7 (0.7% fee) | €915 |

The difference is staggering. Your friend in Germany receives almost €40 more just because you sidestepped the bank’s inflated rate and high fixed fees. While traditional banks mark up rates by 2-4% on average, fintech apps save users up to 8x more by sticking to the real rate.

Many of these platforms let you hold balances in over 50 currencies, helping you dodge conversion fees that can nibble away 0.4% to 2% of every single transaction.

By using fintech, you’re doing more than just moving money—you’re preserving its value across borders. It turns currency exchange from a costly headache into a simple, transparent process that you control.

Take Back Control of Your Global Finances

Opening an account with one of these services is refreshingly simple and usually takes just a few minutes on your phone. You’ll need to verify your identity, but the whole process is designed to be painless. Once you’re set up, you have an incredibly powerful tool for managing your international finances.

Of course, holding funds in multiple currencies can make it tricky to see your true financial picture. To get a clear, unified view of your net worth, check out our guide on currency exchange rate tracking to learn how to monitor the impact of currency fluctuations.

And for those exploring the very edge of modern finance, it’s worth looking into emerging alternatives like using stablecoins to pay overseas.

Ultimately, these tools empower you to be proactive. You’re no longer just a passive participant in an unfair system—you’re a savvy global citizen.

Withdrawing Cash Abroad Without Overpaying

Even as the world goes digital, you just can’t get by without local cash sometimes. Think small cafes, bustling street markets, or leaving a tip for great service. But the simple act of using a foreign ATM can feel like walking through a minefield of hidden fees.

One wrong button press can turn a quick withdrawal into a costly mistake.

These sneaky charges usually come from three places. First, your own bank might hit you with a foreign transaction fee, which is typically a percentage of what you take out. Second, the local ATM operator often tacks on its own usage fee, a flat charge just for using their machine. And finally, there’s the dreaded Dynamic Currency Conversion (DCC), which offers to convert the transaction for you—at a truly terrible rate.

The trick to getting cash without getting ripped off is to strategically sidestep these three fees. With a little bit of planning, it’s easier than you think.

Your ATM Withdrawal Playbook

The absolute best way to start is by using a debit card built for travel. Cards from providers like Charles Schwab Bank are legendary among savvy travelers for one huge reason: they reimburse all ATM fees charged by other banks, anywhere in the world. This single feature wipes out one of the most common and annoying costs of getting cash.

If you don’t have a fee-reimbursing card, your next best move is to withdraw cash less often. Since local ATM fees are usually a fixed amount, maybe $3-$5, it makes way more sense to take out a larger sum, like $200, once a week instead of pulling out $40 every other day. You’ll massively cut down on the impact of those flat service charges.

Crucial Reminder: When the ATM screen asks if you want the transaction in the local currency or your home currency, always, always choose the local currency. Hitting “yes” to their conversion offer is just you giving them permission to use an inflated exchange rate. It’s a guaranteed way to lose money.

ATM Safety and Best Practices

Avoiding fees is only half the battle. Making sure your money and information are secure is just as critical. A few simple habits can make all the difference.

- Stick to Bank-Affiliated ATMs: Whenever you can, use machines that are physically attached to or inside a real bank branch. They’re far less likely to be tampered with than standalone ATMs in tourist hotspots or convenience stores.

- Withdraw During Bank Hours: Try to use ATMs during the day when the bank is actually open. If the machine decides to eat your card, you can walk inside and get help right away instead of being stuck until the next business day.

- Shield Your PIN: This one’s simple but vital. Always cover the keypad with your other hand when you’re punching in your Personal Identification Number. Glance around and be aware of anyone standing uncomfortably close.

- Inspect the Machine: Before you put your card in, give the card slot and keypad a quick once-over. Does anything look loose, bulky, or out of place? Those could be signs of a “skimmer” designed to steal your card data.

By combining a fee-friendly debit card with smart withdrawal habits and basic security checks, you can get the local cash you need with total confidence. This way, you’re not wasting your travel budget on needless fees just to grab money for a taxi or a morning coffee.

Your Questions About Currency Fees, Answered

Spending money abroad can feel like a minefield of hidden charges. Let’s clear up some of the most common questions so you can navigate international payments with confidence and keep more of your money.

Is It Really Always Cheaper to Pay in the Local Currency?

Yes. Without a doubt. Every single time.

When a card machine gives you the option to pay in your home currency, it’s a sneaky trap called Dynamic Currency Conversion (DCC). This isn’t a friendly service; it’s a way for the merchant’s payment processor to set its own, often terrible, exchange rate. We’re talking markups of 3-7% on top of the real rate.

Always, always choose to pay in the local currency. By doing so, you’re letting your own bank or card network (like Visa or Mastercard) handle the conversion. Their rates are far more competitive and transparent, saving you a significant chunk of cash on every single purchase.

Do I Still Need to Tell My Bank I’m Traveling?

It’s a smart move, even if it feels a bit old-fashioned. While most modern banks have sophisticated fraud detection systems, why risk it?

Giving your bank a quick heads-up is a simple preventative measure. It usually takes less than a minute in your banking app or online portal to set up a travel alert. This little step can prevent the nightmare scenario of your card being frozen for “suspicious activity” right when you’re trying to pay for dinner in a new city. It’s a tiny bit of effort for a whole lot of peace of mind.

The core difference lies in who charges the fee and why. A Foreign Transaction Fee is a simple penalty from your bank for spending abroad. A Currency Conversion Fee is the hidden cost within a bad exchange rate, usually from DCC. You can avoid both with the right card and the right habits.

What’s the Difference Between a Currency Conversion Fee and a Foreign Transaction Fee?

It’s easy to confuse these two, but they are separate charges that can both eat into your travel budget. Think of them this way:

-

Foreign Transaction Fee: This is a straightforward penalty, usually 1-3%, that your bank tacks on just for the privilege of processing a transaction outside your home country. The best travel cards get rid of this fee entirely.

-

Currency Conversion Fee: This one is sneakier. It’s not an obvious line item on your statement. Instead, it’s the profit margin baked into a poor exchange rate, almost always thanks to DCC. You sidestep this by always paying in the local currency.

Getting a handle on these fees is the first step. But remember, currency values themselves are constantly shifting. For a deeper look into protecting your finances from these movements, check out our guide on how to hedge currency risk.

Ready to get a crystal-clear view of your entire financial world, no matter how many currencies you hold? With PopaDex, you can track all your assets and liabilities in one simple dashboard. Stop guessing and start seeing your true net worth today.