Our Marketing Team at PopaDex

How to Calculate Your Net Worth A Clear Financial Guide

Calculating your net worth is the single most important step you can take to understand where you really stand financially. Forget vague worries or guessing games. This one number gives you a clear, honest snapshot of your financial position right now.

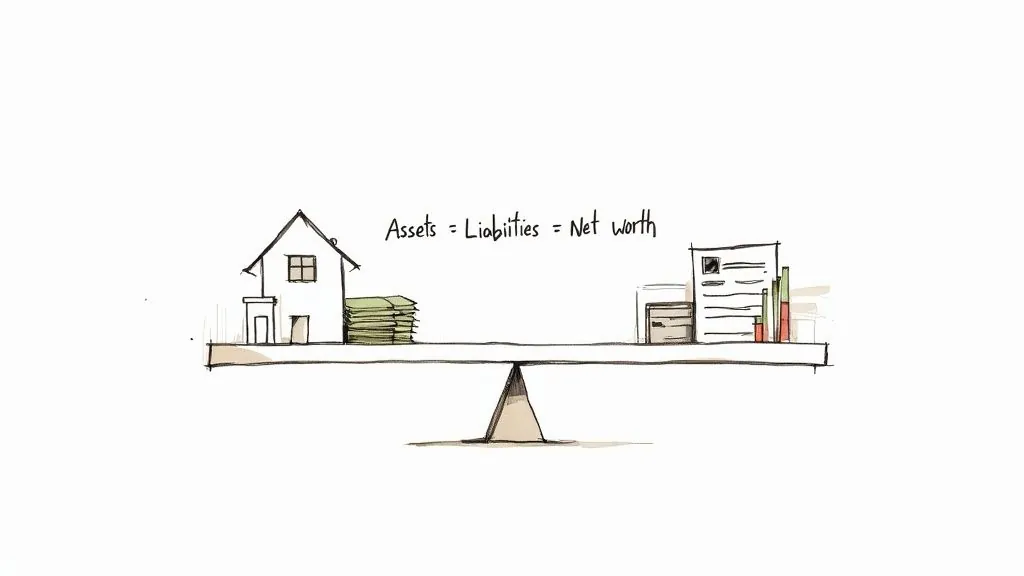

At its core, the formula is beautifully simple: Assets - Liabilities = Net Worth. It’s everything you own minus everything you owe.

Your Financial Snapshot: Understanding Net Worth

Think of your net worth as your personal financial scorecard. It’s not some exclusive metric reserved for the ultra-wealthy; it’s a vital tool for anyone serious about building a secure future. Knowing this figure helps you track your progress over time, set meaningful goals—like buying a home or retiring comfortably—and make smarter choices with your money day-to-day.

The calculation is straightforward. You’ll add up all your assets (cash, investments, property) and then subtract your total liabilities (mortgages, credit card balances, student loans).

If the final number is positive, you’re in a good spot—your assets are greater than your debts. If it’s negative, don’t panic. This is common for recent graduates buried in student loans or anyone just starting out. It just means your debts currently outweigh your assets, giving you a clear target to work on.

Assets vs. Liabilities: A Quick Breakdown

Before you start crunching numbers, you need to know what goes where. While the concepts are simple, people often overlook key items.

Here’s a quick reference to get you started.

Net Worth Calculation at a Glance

| Component | Definition | Common Examples |

|---|---|---|

| Assets | Anything you own that has monetary value. | Cash, checking/savings accounts, stocks, 401(k), real estate, vehicles, valuable collectibles. |

| Liabilities | Any debt or financial obligation you owe to others. | Mortgage, car loan, student loans, credit card balances, personal loans. |

This table covers the basics you’ll need for an accurate calculation.

This fundamental balance of assets and liabilities shapes financial realities everywhere. Just look at the global wealth figures. As of 2022, the average net worth per person worldwide was about $409,954, but that number hides some wild variations—from $6,492 in Yemen to over $156,755 in Singapore.

The goal isn’t to compare your number to anyone else’s. Your first calculation is your starting line. From here on out, the only thing that matters is your own progress.

Why This Number Matters

Figuring out your net worth brings a sense of clarity that’s hard to overstate. It shifts you from vague financial anxiety to a concrete understanding of your position. It also forces you to distinguish between your total wealth and the money you can actually access quickly. For a deeper dive, check out our guide on what is liquid net worth, which focuses on assets that can be converted to cash in a pinch.

By making this calculation a regular habit—maybe once a quarter or even once a year—you turn it into a powerful tool. You’ll see the direct impact of paying down that credit card, bumping up your 401(k) contribution, or watching an investment grow. That kind of visibility is incredibly motivating and helps you steer your financial ship with real confidence.

Gathering Your Financial Puzzle Pieces

Before you can calculate your net worth, you need to pull together a complete and honest inventory of your financial life. Think of it like assembling a puzzle; every bank statement, account balance, and loan document is a crucial piece. The goal here is to be thorough so the final number is a true reflection of your finances, not just a shot in the dark.

Let’s start with the “what you own” side of the equation—your assets. This is usually the more enjoyable part of the process.

Cataloging Your Assets

Your assets are everything you own that carries some monetary value. It’s a smart move to break them down into categories to keep things organized. For this part, you’ll need to log into your various accounts online and pull up the most recent statements.

Cash and Cash Equivalents This is the most straightforward category, covering all the liquid money you can get your hands on quickly.

- Checking Accounts: Log into your online banking portal and jot down the current balance.

- Savings Accounts: Do the same for all your savings, including any high-yield savings accounts or money market accounts.

- Physical Cash: Don’t forget about that emergency cash you might have stashed away at home.

Investments For many people, this is where a significant chunk of their net worth lives. These are your accounts designed for long-term growth.

- Retirement Accounts: Find the latest statements for your 401(k), 403(b), IRA (Roth or Traditional), and any pensions. Record the total current market value.

- Brokerage Accounts: Pop into your investment platform to find the current value of your stocks, bonds, mutual funds, and ETFs.

- Other Investments: This bucket can include things like your cryptocurrency holdings, Health Savings Accounts (HSAs), or 529 college savings plans.

Property and Valuables These are your tangible, physical assets. Figuring out their exact value takes a bit more estimation (we’ll tackle that later), but for now, just make a list.

- Real Estate: This is probably your primary home, but be sure to include any rental properties or land you own, too.

- Vehicles: List your car, truck, motorcycle, or even a boat.

- Personal Valuables: Think about high-value items you could realistically sell, like fine jewelry, art, or rare collectibles.

Your first pass at listing assets doesn’t need to be perfect. The key is to create a comprehensive list. You can refine the values in the next step, but you can’t value what you forget to list.

Identifying Your Liabilities

Now for the other side of the balance sheet: your liabilities. This is everything you owe, and being brutally honest here is non-negotiable for an accurate calculation. Overlooking even a small debt can seriously skew your final number and create a false sense of financial security.

Secured Debts These are loans backed by an asset—if you don’t pay, they can take the asset.

- Mortgage: Check your latest statement or online portal for the remaining principal balance on your home loan.

- Auto Loans: Find the outstanding balance on any vehicle loans you have.

Unsecured Debts These debts aren’t tied to a specific asset, and for many people, they make up a big part of their liabilities.

- Student Loans: Gather the current balances for all your federal and private student loans.

- Credit Card Balances: This one is crucial. Log into each credit card account and record the current statement balance, not just the minimum payment due.

- Personal Loans: Make sure to include any loans from banks, credit unions, or peer-to-peer lenders.

- Other Debts: Don’t forget about things like medical bills, outstanding taxes, or even personal loans from family members.

Trying to keep all of this information straight in your head is a recipe for disaster. To make it easier, use a structured document to keep everything organized. For a great starting point, check out this comprehensive personal financial statement template that lays out all the categories you’ll need.

Once you have all these puzzle pieces gathered—every last asset and every single liability—you’ve finished the most intensive part of this process. You now have a complete inventory of your financial world, ready to be assembled into one powerful number.

Assigning Realistic Values to Your Assets

Once you have a complete list of your assets, the next step is figuring out what they’re actually worth today. This is where a lot of people trip up. It’s tempting to use the price you paid, but that number is often irrelevant now. For an accurate picture, you need to use the Fair Market Value—what something would realistically sell for on the open market.

The difficulty of this process ranges from dead simple to a bit more involved, depending on the asset. Let’s walk through how to pin down these numbers without letting emotion get in the way.

Valuing Liquid and Financial Assets

Good news: this is the easiest part. For cash and investments, the value is clear, current, and requires zero guesswork.

- Cash Accounts: The value of your checking, savings, and money market accounts is simply the current balance. Just log into your bank’s website for the most up-to-date number.

- Investment Accounts: For your 401(k), IRA, or brokerage accounts, the value is whatever they’re worth at this moment. Your investment platform’s dashboard will show you the real-time value of your portfolio.

Yes, these numbers change daily, but for your net worth snapshot, the value on the day you’re doing the math is what matters.

Estimating the Value of Your Property

Valuing physical things like your home and car takes a little more legwork since their worth isn’t displayed on a convenient dashboard. Your goal here is to find a realistic sale price, not what you hope it’s worth.

For your home, online tools like Zillow or Redfin offer a quick “Zestimate” based on recent sales in your neighborhood. This is a perfectly fine starting point for a regular net worth check-in. However, if you’re making a major financial decision like refinancing, nothing beats a professional appraisal for a rock-solid valuation.

As for your car, its value started dropping the second you drove it off the lot. Resources like Kelley Blue Book (KBB) or Edmunds are the go-to for finding your car’s current private-party sale value. Just plug in your car’s details—make, model, year, mileage, and condition—to get a reliable estimate.

Remember to be objective. The price you wish you could get for your house isn’t the number to use. Stick to honest, conservative estimates to avoid artificially inflating your net worth.

The challenge of valuing assets goes beyond a personal finance quirk; it’s a global one. The 2025 Global Wealth Report from Boston Consulting Group (BCG) found that worldwide financial assets soared to a record $305 trillion in 2024. This massive figure shows just how much asset values can swing due to market performance and inflation, which is exactly why using current, realistic values in your own calculations is so critical. You can dig into the BCG wealth report on bcg.com for more.

Handling Personal and Collectible Items

This category can be tricky. What about your jewelry, art, furniture, or that collection of rare comic books?

The simple answer is to only include items with significant, verifiable value that you could actually sell. Your everyday furniture or old electronics have minimal resale value and usually aren’t worth the hassle of tracking.

But a high-value item—like a Rolex watch, a piece of fine art, or an antique—should absolutely be part of the equation. For these, you’ll probably need a professional appraisal to get a defensible number.

When you’re dealing with complex or high-value physical assets, turning to professional asset valuation services provides the clarity you need so you aren’t just guessing. These tangible items contribute to what’s known as your tangible net worth, a topic you can dive deeper into with our guide on what is tangible net worth.

By focusing on realistic, market-based values for everything you own, you build a net worth statement that is both accurate and genuinely useful for planning your financial future.

Putting It All Together with a Real Example

Theory is one thing, but seeing how the net worth calculation plays out in the real world makes it all click. Let’s walk through a relatable scenario to connect the dots.

Meet Alex, a 35-year-old professional who wants a clear, honest snapshot of their financial health. By digging into Alex’s numbers, we can turn this abstract concept into something tangible.

Alex’s Financial Inventory

First things first, we need to list everything Alex owns and everything they owe. Getting this right is the most important part of the whole process—the more thorough you are, the more accurate your final number will be.

Let’s start with the asset side of the ledger.

Alex’s Assets:

- Checking Account: $6,000

- High-Yield Savings Account: $20,000

- 401(k) Retirement Fund: $110,000

- Brokerage Account (Stocks/ETFs): $45,000

- Condo (Current Market Value): $350,000

- Car (Kelley Blue Book Value): $18,000

Adding it all up, Alex’s total assets come to $549,000. This figure represents the total value of everything Alex currently owns.

Now, let’s look at the other side of the equation: the liabilities. This part is just as critical for getting a true sense of where you stand.

Alex’s Liabilities:

- Mortgage Balance: $240,000

- Student Loan Balance: $35,000

- Car Loan Balance: $11,000

- Credit Card Debt: $4,000

Summing these up, Alex’s total liabilities are $290,000.

This process of assigning a realistic, current market value to your big-ticket items—like property, vehicles, and investments—is a foundational step.

You have to be honest with yourself here. Use Zillow or Redfin for your home value and Kelley Blue Book for your car. Don’t just guess.

The Final Calculation

With all the numbers gathered, the final step is simple subtraction using the classic formula: Assets - Liabilities = Net Worth.

For Alex, the math is straightforward: $549,000 (Total Assets) - $290,000 (Total Liabilities) = $259,000 (Net Worth)

That one number, $259,000, is Alex’s net worth. It’s a powerful metric that shows solid progress toward building long-term wealth, with assets comfortably outweighing debts.

Understanding this personal figure also provides context for broader economic trends. For instance, a 2025 Allianz report noted that while global financial assets hit a record high, inflation also played a huge role. This makes it crucial to accurately assess your liabilities so you don’t overestimate your true financial standing. You can find more insights by reading the full Allianz Global Wealth Report.

Your Turn to Calculate

Okay, now it’s your turn. To make this as painless as possible, we’ve put together a simple spreadsheet template with all these categories ready to go.

Pro Tip: Don’t get paralyzed trying to get every number perfect down to the last cent. The goal of your first calculation is to establish a solid baseline. You can always go back and refine the numbers later.

Our template is clean and simple—just plug in your numbers and let it do the math. By using a tool like this, you can turn a potentially messy task into a quick, ten-minute exercise.

You can download your own copy of our Net Worth Calculator Spreadsheet and fill in the blanks. It’s the perfect first step toward taking control of your financial story.

Automating Your Financial Journey with PopaDex

So, you’ve gone through the process of calculating your net worth by hand. It’s a powerful exercise, isn’t it? That single number gives you incredible clarity on where you stand. But you’ve also probably run into its biggest drawback: a manual calculation is just a static snapshot in time. The minute you finish, it’s already a little bit out of date.

Keeping that number current feels like a constant chore. This is exactly where technology steps in, turning a periodic task into a live, ongoing source of insight. Instead of battling spreadsheets and logging into a dozen different accounts every month, a tool like PopaDex can build a dynamic, real-time financial dashboard for you. It neatly solves the headaches of manual tracking by securely connecting to all your financial institutions.

From a Static Number to a Live Dashboard

The real magic of automation is moving beyond a single, backward-looking number. PopaDex securely links to your accounts—banks, investment platforms, credit cards, and loans—to pull in fresh data automatically. What you get is a live view of your finances that reflects market swings and your latest transactions, all in one place.

For you, this means having a constant, effortless pulse on your financial position. Instead of guessing how your investments did last week, you can see their direct impact on your net worth right now. This shift from a static report to a live dashboard helps you be proactive with your money, not just reactive.

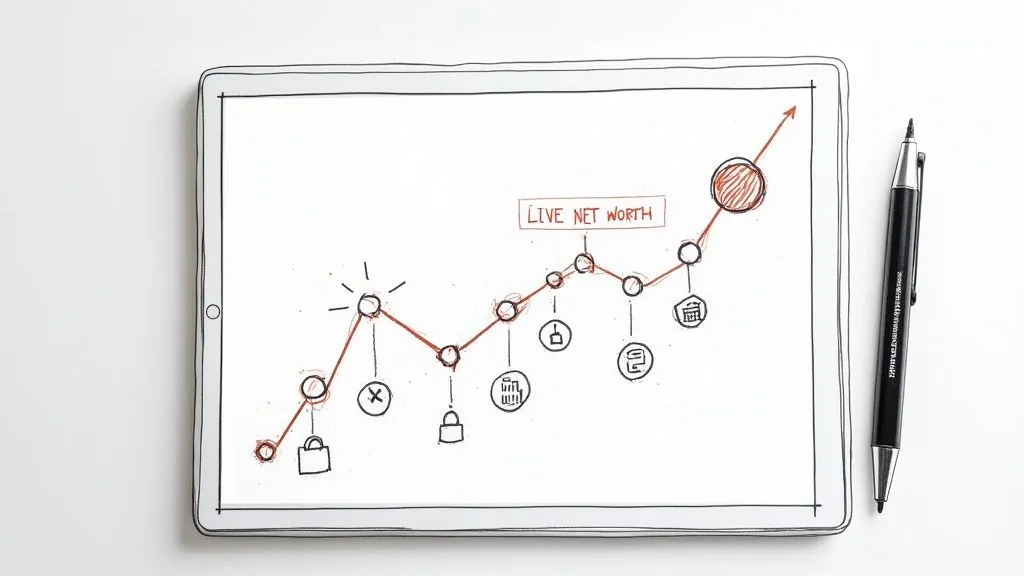

Automation turns your net worth from a historical document into a living, breathing metric. It helps you see not just where you are, but where you’re heading, in real time.

With this approach, you can make smarter decisions, faster. You’ll be able to spot trends as they happen, celebrate milestones the moment you reach them, and tweak your strategy without waiting for your next “net worth day.”

Visualizing Your Growth and Tracking Progress

Let’s be honest, numbers on a spreadsheet can be pretty dry. One of the best things about an automated tracker is seeing your financial journey visualized. Charts and graphs that actually show your net worth climbing over time? That’s genuinely motivating.

PopaDex excels at turning your raw data into visual stories that are easy to grasp.

- Historical Performance Charts: Watch your net worth trend line move up (or down) over months and years. It gives you a crystal-clear picture of your long-term progress.

- Asset and Liability Breakdowns: Instantly see your allocation. Is most of your money tied up in real estate or stocks? How much of your debt is your mortgage versus nagging credit card balances?

- Goal Tracking: You can set concrete net worth targets—like hitting your first $100,000 or reaching a specific pre-retirement number—and watch your progress bar fill up.

Here’s a glimpse of how PopaDex brings your live net worth to life, transforming complex data into a simple, actionable visual.

This kind of visual feedback loop is a game-changer for staying motivated on the path to financial independence. And for those looking to get even smarter about their money, pairing automation with tools like AI for financial analysis can take your insights to the next level.

Handling Multi-Currency and International Assets

If you’re an expat, a digital nomad, or just someone with assets in different countries, you know that manual net worth calculations get messy, fast. Juggling currency conversions and tracking international accounts is a massive headache.

This is another area where automation is a lifesaver. PopaDex was built to handle this kind of complexity effortlessly.

- Connect International Accounts: You can link bank and investment accounts from over 30 countries.

- Automatic Currency Conversion: The platform automatically converts all your foreign assets and liabilities into your chosen base currency using real-time exchange rates. No more manual math.

- Get a Unified View: The result is a single, accurate net worth figure that consolidates your entire global portfolio.

This feature alone removes one of the biggest roadblocks for anyone with an international financial life. It ensures you get a complete answer to “what’s my net worth?” no matter where your assets are. By embracing automation, you graduate from tedious manual updates to a state of constant financial clarity.

A Few Common Questions About Calculating Net Worth

Once you get past the basic assets-minus-liabilities formula, the real world throws a few curveballs. Life isn’t a simple spreadsheet, and some practical questions almost always pop up when you’re getting started.

Let’s walk through the most common ones. Getting these details right from the start means your net worth number will be a genuinely useful tool for decision-making, not just some abstract figure you look at once a year.

How Often Should I Calculate My Net Worth?

There’s no single magic answer here, but for most people, the sweet spot is quarterly or semi-annually. This rhythm is frequent enough to show you meaningful progress without turning into an obsessive, anxiety-inducing daily chore. Checking every day is a recipe for stress, as you’ll be reacting to normal, meaningless market blips.

On the flip side, waiting a full year between check-ins is too long. You’ll miss the impact of your recent financial habits and lose the chance to make timely adjustments. The goal is to find a cadence that keeps you informed and motivated.

A few timelines to consider:

- Monthly: This can be a great idea if you’re in a highly dynamic financial phase—like aggressively tackling high-interest debt or if you’re a freelancer with big swings in income.

- Quarterly: This is the most popular and practical option for a reason. It lines up nicely with investment statements and gives your financial picture enough time to actually change in a meaningful way.

- Annually: Think of this as the bare minimum. It’s useful for a big-picture, year-over-year comparison, but it won’t give you the granular insight needed to stay agile.

Ultimately, consistency beats frequency. Pick a schedule that you can actually stick with.

Should I Include Business Assets in My Personal Net Worth?

This is a huge question for any entrepreneur, freelancer, or small business owner. The short answer is: it depends entirely on your business structure.

If you’re operating as a sole proprietor or a single-member LLC, your personal and business finances are legally considered one and the same. In that scenario, yes—you should include your business assets (like the cash in your business checking account) and liabilities (like a business loan) in your personal net worth calculation.

However, if you’ve set up a separate legal entity like an S Corp or C Corp, it’s far cleaner to keep them separate. The asset you’d list on your personal net worth statement is your ownership stake in the company itself, valued at what you could realistically sell it for. You wouldn’t list the company’s individual assets and debts.

As a general rule, keeping business and personal finances separate is always a good practice for both legal protection and clear accounting. If you’re unsure, try calculating your net worth both ways—with and without the business assets—to get two different perspectives on your financial health.

What Are the Most Common Mistakes to Avoid?

It’s easy to make a few simple mistakes the first time you run the numbers. Just being aware of these common pitfalls ahead of time can make your calculation much more accurate and useful.

One of the biggest blunders is forgetting the small debts. It’s easy to overlook that “buy now, pay later” balance with Klarna or Affirm, an old medical bill you’re paying off, or even a small loan from a family member. These little liabilities can add up quickly and throw off your final number if you ignore them.

Another classic error is using the wrong values for your assets. People often default to the original purchase price for their home or car, which is almost always wrong. You need to use the current Fair Market Value—what it would actually sell for today. On that same note, don’t let sentimentality inflate the value of your personal belongings. Unless it’s a high-value collectible, the resale value of your furniture or old laptop is probably close to zero.

Finally, be careful not to overlook future tax implications. The total balance in your traditional 401(k) or IRA isn’t really all yours; a chunk of it belongs to the tax man when you eventually make withdrawals. While you don’t need to perform complex tax calculations for a basic net worth snapshot, it’s important to remember that pre-tax accounts come with a built-in future liability.

Steering clear of these common slip-ups will give you a much more honest and powerful tool for financial planning.

Ready to stop juggling spreadsheets and get a live, automated view of your financial progress? PopaDex securely connects to all your accounts to give you a real-time net worth dashboard, complete with insightful charts and multi-currency support. Take the guesswork out of your financial journey by visiting https://popadex.com to start your free trial.