Our Marketing Team at PopaDex

How to Diversify Investment Portfolio: Top Strategies

Diversifying your investment portfolio is just a fancy way of saying you’re spreading your money across different types of assets—think stocks, bonds, and real estate—to lower your overall risk. The whole point is to make sure that if one part of your portfolio takes a nosedive, it doesn’t drag everything else down with it. It’s a cornerstone strategy for anyone serious about building wealth and keeping it safe for the long haul.

Why Diversification Is Your Best Defense in a Volatile Market

We’ve all heard the old saying, “don’t put all your eggs in one basket.” That simple piece of advice is more valuable than ever. Smart diversification isn’t just about owning a random mix of stuff; it’s a deliberate plan designed to cushion the blow from a downturn in any single asset class.

Think of it like this: when one part of your portfolio zigs, another part zags. This natural counterbalance is the secret sauce to a resilient investment strategy. A well-diversified portfolio can help shield your capital during turbulent times while also positioning you to catch growth wherever it might pop up.

The Real-World Impact of Diversification

Recent market performance drives this point home. In the first quarter of 2025, a fully diversified portfolio actually gained 0.61%. Compare that to the classic 60/40 portfolio, which lost 1.45%, and the S&P 500, which fell 4.27%. That’s a stark difference, and it clearly shows the protective power of spreading your investments around when things get rocky.

But it’s not just a defensive move. It’s a proactive way to build wealth more sustainably by smoothing out the inevitable bumps you’ll hit on your investment journey.

“The goal of diversification is not necessarily to boost performance—it won’t ensure gains or guarantee against losses. It is to manage risk.”

This approach helps you sidestep the trap of making emotional, knee-jerk decisions based on short-term market noise. When one asset is struggling, another might be thriving, which helps keep your overall strategy on an even keel. This method pairs perfectly with long-term techniques like dollar-cost averaging, which you can learn more about in our guide on the topic.

If you’re looking for more ways to spread your assets effectively, these 10 investment diversification strategies are a great place to start.

To help you get a handle on the core ideas, we’ve put together a quick reference table.

Quick Guide to Core Diversification Concepts

This table breaks down the key principles of diversification, giving you a straightforward guide to the foundational concepts.

| Concept | What It Means | Why It Matters |

|---|---|---|

| Asset Allocation | Deciding how to split your money among different asset classes (e.g., 60% stocks, 30% bonds, 10% real estate). | It’s the primary driver of your portfolio’s risk and return, more so than individual stock picks. |

| Correlation | How two assets move in relation to each other. Low or negative correlation is ideal for diversification. | Assets that move in opposite directions (one zigs, the other zags) help balance out your portfolio’s performance. |

| Risk Tolerance | Your personal comfort level with the possibility of losing money. | This determines your ideal asset mix. A higher risk tolerance might mean more stocks, while a lower tolerance means more bonds. |

| Rebalancing | Periodically buying or selling assets to get your portfolio back to its original target allocation. | It prevents you from becoming over-exposed to one asset class and forces you to “buy low and sell high” systematically. |

Understanding these simple concepts is the first step toward building a portfolio that can weather any storm.

Defining Your Personal Investment Blueprint

Before you even think about buying a single stock or bond, the most important work happens right between your ears. There’s no magic formula for diversifying a portfolio; the right strategy is built around your life, your goals, and—most importantly—your gut reaction to risk.

Your journey starts by getting crystal clear on your financial goals. Are you investing for a retirement that’s 30 years away, or are you socking away cash for a down payment on a house you want in five? The answer changes absolutely everything.

A long timeline, like saving for retirement, gives you the breathing room to take on more risk. You have decades to ride out the market’s inevitable roller-coaster dips. But if your goal is just around the corner, your priority shifts to protecting what you’ve got.

Getting an Honest Read on Your Risk Tolerance

Now for the tricky part: assessing your risk tolerance. This isn’t about what you think you can handle. It’s about how you’ll actually behave when your portfolio is bleeding red.

Forget those generic online quizzes that pigeonhole you as “conservative” or “aggressive.” The real test is asking yourself some tough, what-if questions:

- How would you feel watching your portfolio plummet 20% in three months? Would you panic-sell everything, or would you see it as a chance to buy more at a discount?

- Are you genuinely okay with the wild swings of emerging markets for a shot at higher returns, or does that level of uncertainty give you heartburn?

- Do you sleep better at night prioritizing slow and steady growth, or does the thought of missing out on big gains feel worse?

Your honest answers here are worth more than any algorithm’s score. They’re the bedrock of a strategy you can actually stick to when things get messy.

The most brilliantly diversified portfolio on paper is completely useless if it scares you into making emotional, knee-jerk decisions during a market downturn. Your strategy has to match your temperament.

If you need a hand getting started, a tool like the risk tolerance quiz from Investor.gov can frame these questions in a more structured way.

As you can see, these tools prompt you to think about both your financial reality and your emotional triggers around losing money. It’s a solid first step toward building an investment blueprint that’s truly your own.

Constructing Your Portfolio with Key Asset Classes

Alright, you’ve got your personal investment blueprint. Now it’s time for the fun part: laying the bricks and mortar of your portfolio.

This is all about understanding the core asset classes—the fundamental building blocks that come together to create a solid financial structure. Thinking about how to diversify your investment portfolio is less about trying to pick individual “winners” and more about assembling a team of assets where each player has a specific job to do.

The idea isn’t to just own a random grab-bag of investments. You want to strategically combine assets that react differently when the market gets choppy. This way, while one part of your portfolio might be struggling, another could be thriving, which helps smooth out the overall ride.

The Foundation: Stocks and Bonds

For most of us, the journey starts with stocks and bonds. They’re the yin and yang of a traditional portfolio, giving you a balance of growth potential and much-needed stability.

Stocks (Equities) are your portfolio’s main engine for long-term growth. When you buy a stock, you’re buying a small piece of a company. This comes with higher volatility, but it’s where the real wealth-building happens over time.

A good diversification strategy means going beyond just owning a few familiar stocks. You need to spread your equity investments across different geographies and company sizes.

- Domestic Stocks: These are shares in companies within your home country. For a U.S. investor, this might mean holding an S&P 500 ETF (like VOO or IVV) for broad exposure to America’s largest corporations.

- International Stocks: Investing outside your home country is crucial. This includes both stable developed markets (like Europe and Japan) and higher-growth emerging markets (like Brazil and India). An ETF like VXUS can give you this global exposure all in one shot.

Bonds (Fixed Income), on the other hand, are the stabilizers. They are essentially loans you make to a government or a corporation in exchange for regular interest payments. When the stock market nosedives, bonds tend to hold their value or even go up.

- Government Bonds: Issued by national governments (like U.S. Treasuries), these are considered some of the safest investments out there—a real buffer during a downturn.

- Corporate Bonds: Issued by companies, these typically offer higher interest payments than government bonds but come with a bit more risk, depending on the company’s financial stability.

A common mistake is thinking diversification is just about owning different stocks. True diversification means owning different types of assets that don’t all move in the same direction.

Expanding Your Horizons Beyond the Basics

To build a truly resilient portfolio, you need to look beyond just stocks and bonds. Adding assets that have a low correlation to the traditional markets can dramatically improve your portfolio’s ability to weather any storm.

This is where the real-world data gets interesting. A recent Morningstar analysis showed just how powerful a broader strategy can be. A portfolio that included large-cap U.S. stocks, international equities, various bonds, and alternatives delivered positive returns while the classic 60/40 portfolio actually lost ground. You can dig into the numbers yourself in the Morningstar report on diversification.

Real Estate and Other Tangible Assets

Real Estate is another fantastic diversifier. It offers the potential for both your property’s value to grow and for you to earn income through rent.

While buying a property outright is one way to go, it’s often much easier to get exposure through Real Estate Investment Trusts (REITs). These are companies that own or finance income-producing real estate, and you can buy and sell their shares just like a stock.

As you start putting these different pieces together, keeping track of everything becomes critical. Using effective portfolio analysis tools lets you see the whole picture at a glance and make sure your strategy stays on track with your goals. The right mix of these asset classes, tailored to your personal risk tolerance, is the true key to successfully diversifying your investment portfolio.

Using Alternatives to Gain an Edge

True diversification goes beyond owning a bunch of different stocks. To build a portfolio that can weather any storm, you need to look beyond the usual suspects and include assets that don’t move in lockstep with the broader market. These are what we call alternative investments, and they can be your secret weapon during periods of economic turbulence.

This might sound complex, but getting into alternatives is easier than you’d think. For instance, you can get a slice of the property market without ever playing landlord by investing in Real Estate Investment Trusts (REITs). These are companies that own and operate income-generating properties, and you can buy their shares just like any other stock. Simple.

Then there are commodities—especially gold. Gold has a long-standing reputation as a safe-haven asset, which means its value often holds steady or even climbs when stock markets take a nosedive. This inverse relationship can be a powerful shock absorber for your portfolio when things get choppy.

Finding the Right Mix of Alternatives

So, how much should you actually put into these assets? The key is finding a balance. You want enough to make a real difference, but not so much that you’re taking on wild, unnecessary risks. The goal is to smooth out your returns over the long haul and potentially hedge against inflation, since assets like real estate and commodities often do well when the cost of living goes up.

More and more investors are catching on. A recent BlackRock report pointed out a major shift in where money is flowing, with a lot more capital heading toward liquid alternatives and commodities as people hunt for returns that aren’t tied to the S&P 500’s daily mood swings.

Think of it this way: stocks are your engine for growth and bonds provide stability. Alternatives are the specialized tools in your financial toolkit—the ones you pull out to navigate specific conditions like soaring inflation or a volatile market.

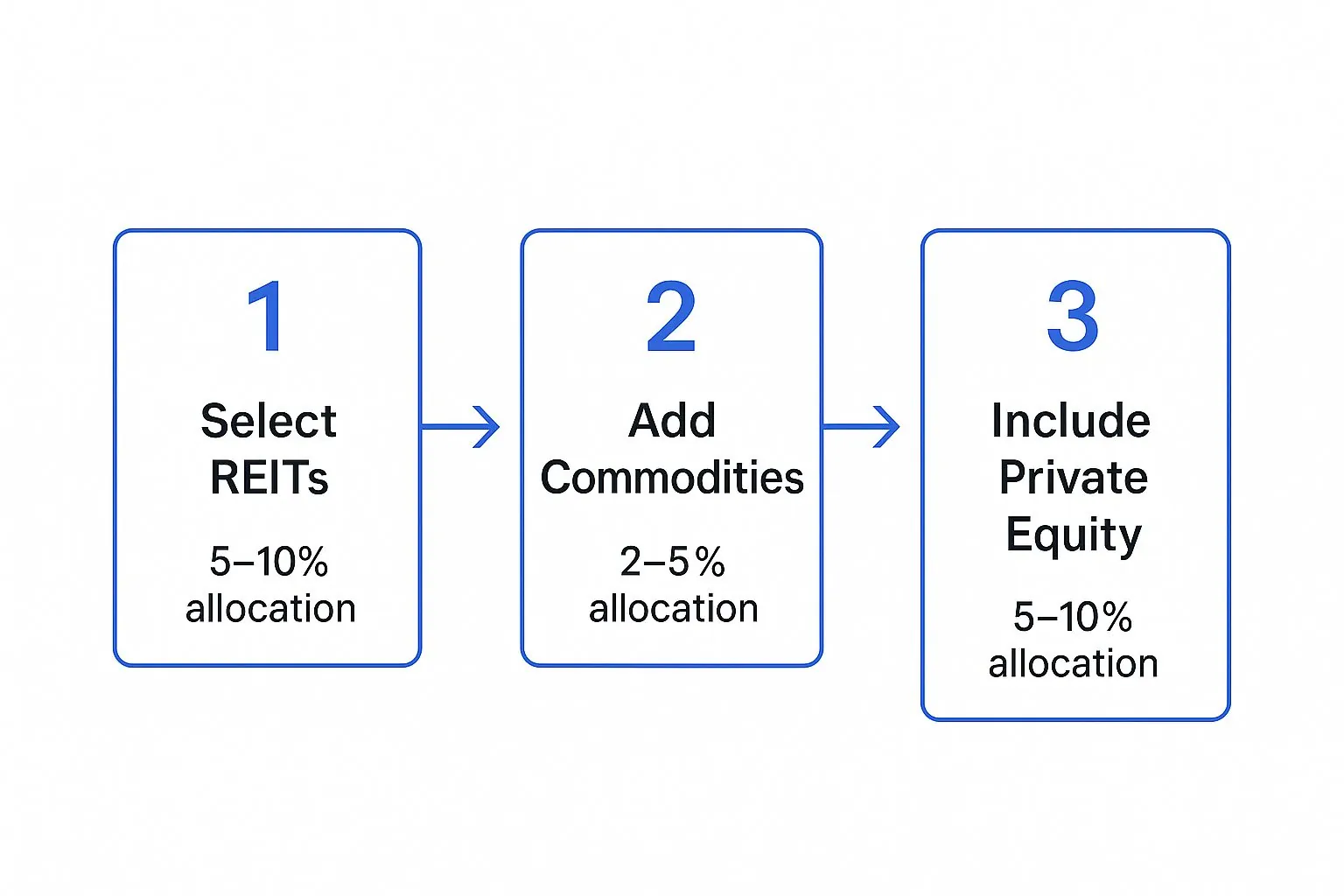

This infographic breaks down a common-sense approach for allocating a slice of your portfolio to these asset classes.

As you can see, you don’t need to go all-in. Small, strategic allocations—typically in the 2% to 10% range for each asset—can add a valuable layer of diversification without completely changing your portfolio’s risk profile.

As you start exploring the world of alternatives, you might also consider the new kid on the block: cryptocurrency. While definitely on the more volatile end of the spectrum, some investors find that learning about building a diversified crypto portfolio offers another way to step outside the traditional financial system. Just remember, integrating these digital assets requires a serious look at your own risk tolerance and long-term financial goals.

Keeping Your Portfolio on Track with Rebalancing

Putting together a diversified portfolio is a massive first step, but it’s definitely not a “set it and forget it” deal. Over time, your best-performing assets will naturally grow, taking up a bigger slice of your portfolio pie. This quiet shift, known as portfolio drift, can slowly crank up your risk level without you even realizing it.

Think about it this way: you start the year with a classic 60/40 portfolio—60% in stocks and 40% in bonds. After a fantastic run in the stock market, you might look up and find your allocation has drifted to 70/30. All of a sudden, you’re shouldering more risk than you originally signed up for, leaving you more exposed if the market takes a downturn.

This is exactly where rebalancing comes into play. It’s the simple, disciplined act of periodically buying or selling assets to pull your portfolio back to its original target allocation.

Simple Strategies for Effective Rebalancing

You don’t need a complex system to keep your portfolio in line. Most investors stick to one of two straightforward methods to decide when it’s time to make adjustments.

- Calendar-Based Rebalancing: This is the easiest approach by far. You just pick a schedule—annually, semi-annually, or quarterly—and on that day, you review and adjust your portfolio back to its targets. For most long-term investors, an annual check-in is perfectly fine.

- Percentage-Based Rebalancing: With this strategy, you set a tolerance band for each asset class, maybe 5%. If any single asset drifts more than 5% away from its target (for instance, your 60% stock allocation balloons to 66%), that’s your signal to rebalance.

Rebalancing is really just a disciplined, unemotional way of “selling high and buying low.” It forces you to trim your winners and reinvest those profits into the assets that have lagged, keeping your entire strategy locked in on your long-term goals.

Figuring out the right frequency is crucial, because rebalancing too often can rack up unnecessary transaction fees and taxes. Getting a handle on how often to rebalance your portfolio helps you find that sweet spot between maintaining your targets and keeping costs low.

The process itself is simple. If your stocks have become overweight, you sell a portion and use that cash to buy more of your underweight assets, like bonds or international funds. This systematic tune-up ensures your diversification plan stays effective and true to your original risk tolerance, year after year.

Have Questions About Portfolio Diversification? Let’s Answer Them.

Even the best-laid plans run into real-world questions. When it comes to diversifying your portfolio, a few common hurdles tend to pop up. Let’s walk through some of the questions I hear most often to clear up any confusion and keep you moving forward.

How Many Stocks Do I Really Need to Be Diversified?

There’s no single magic number, but the old wisdom suggests that holding 20 to 30 different stocks across a mix of unrelated industries is a good starting point. The idea is to protect yourself from a single company’s disaster—if one of your stocks takes a nosedive, it won’t torpedo your entire portfolio.

But let’s be realistic. For most of us, researching and managing 30 individual companies is more than a full-time job. A far more practical route is to use index funds or ETFs. An S&P 500 ETF, for example, gives you a piece of 500 of the biggest U.S. companies in one shot. It’s broad diversification without the headache.

Is the 60/40 Portfolio Obsolete?

Ah, the classic 60% stock, 40% bond portfolio. For decades, it was the go-to strategy for balancing growth with a bit of a safety net. But today’s market, with its unique inflationary pressures and interest rate swings, is definitely putting the 60/40 model to the test.

Recent history has shown that portfolios with a broader mix—think international stocks, commodities, and real estate—have often held up better during volatile times than a simple 60/40 split. It’s still a perfectly reasonable starting point, but savvy investors are now building on top of it, adding other asset classes to create a more resilient mix.

The 60/40 portfolio isn’t broken, but it’s no longer the only game in town. Think of it as a reliable foundation that you can build upon with other non-correlated assets for better protection.

Can You Be Too Diversified?

Absolutely. There’s a point of diminishing returns where you become over-diversified, a condition some people jokingly call “diworsification.” This happens when you own so many different things that the strong performance of your best investments gets diluted by everything else you hold.

You can also fall into this trap by owning too many assets that are basically the same. For instance, holding five different U.S. large-cap stock funds might feel diverse, but they’ll all likely move up and down together. True diversification goes beyond owning a lot of assets; it’s about owning a variety of assets that don’t all move in lockstep.

How Often Should I Check on My Portfolio?

For most people, a good rhythm is to review your portfolio at least once a year. An annual check-in is plenty of time to see how your asset allocation is doing and decide if you need to rebalance things back to your original targets.

Of course, you’ll also want to take a look after any major life event happens. This could be things like:

- Landing a new job with a big salary bump

- Getting married or having a child

- Getting closer to your retirement date

Checking your investments too often—daily, or even weekly—is a recipe for stress. It tempts you into making emotional decisions based on short-term market noise. A disciplined, less frequent review helps keep your eyes on the long-term prize.

Ready to see your newly diversified portfolio in one clear picture? With PopaDex, you can consolidate all your accounts—from stocks and bonds to real estate and crypto—for a real-time view of your net worth. Stop juggling spreadsheets and start making smarter decisions with our intuitive dashboards. Sign up for free and take control of your financial future today!