Our Marketing Team at PopaDex

How to Manage Personal Finances Without Giving Up Your Life

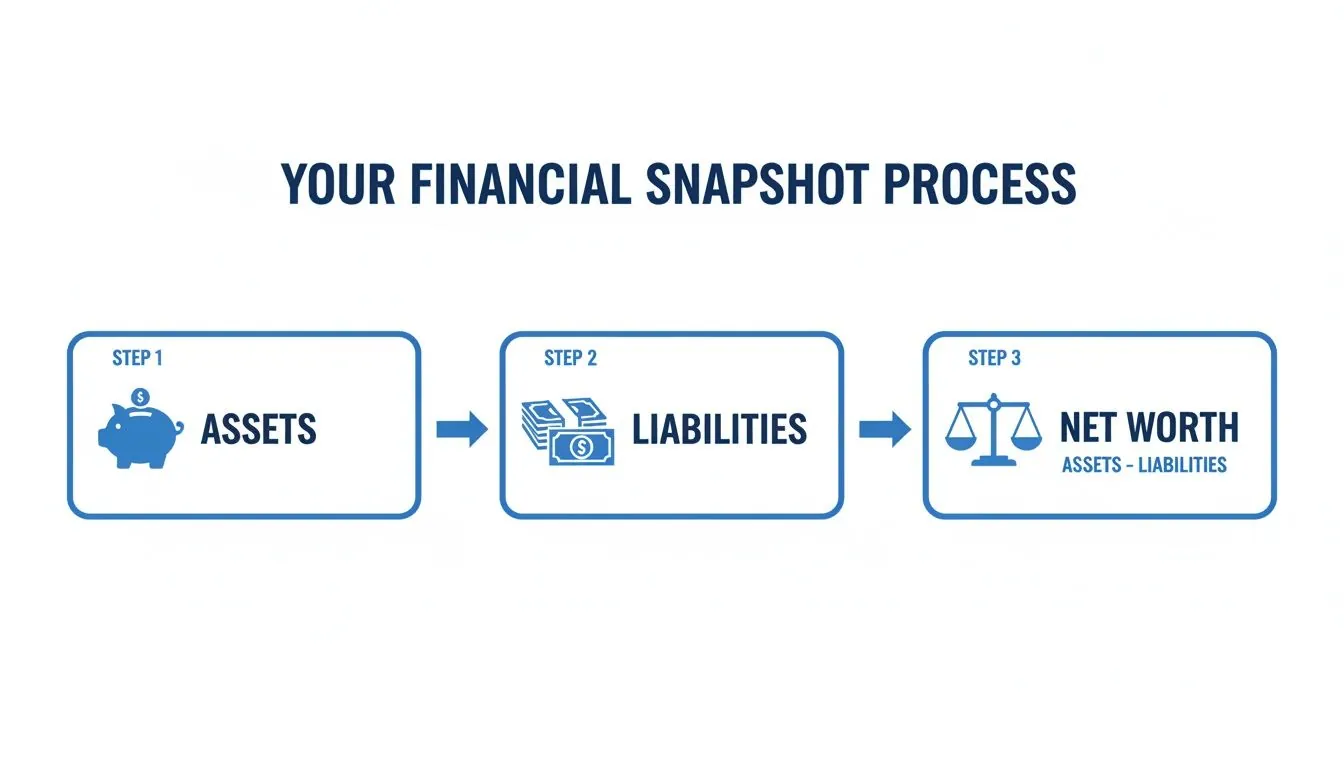

To get a real handle on your money, you first need to know where you stand. Right now. This means calculating your net worth—the simple difference between what you own and what you owe. Getting this number down is the first step to turning financial stress into a clear, actionable plan.

Your Financial Snapshot: Understanding Where You Stand

Before you can map out a trip, you need to know your starting point. Think of it like a GPS getting a lock on your current location. In personal finance, that starting point is your net worth. It’s the single most important number for tracking your financial health, but it’s one a lot of people avoid, afraid of what they might find.

Forget complicated spreadsheets. The process is a straightforward exercise of listing what you own and what you owe. This one number gives you the baseline you need to make smarter decisions and actually see your progress over time.

This simple formula is all it takes: add up your assets, subtract your liabilities, and you’ve got your net worth.

This calculation cuts through the noise, turning vague financial worries into a concrete number you can work on improving.

What Do You Own? Cataloging Your Assets

Assets are anything you own that holds monetary value. Don’t get bogged down in the details; just focus on the big items to start. The goal here is a solid estimate, not a perfect appraisal.

- Cash and Savings: This is the easy part. Tally up the balances in your checking and savings accounts, plus any physical cash you keep on hand.

- Investments: Note the current market value of your retirement accounts (like a 401(k) or IRA) and any brokerage accounts.

- Physical Property: This includes the estimated market value of your home, cars, or any other big-ticket items like jewelry. A quick search on Zillow or Kelley Blue Book will give you a realistic ballpark figure.

Pulling these numbers together might take a few minutes, but it’s the first real step toward building wealth.

What Do You Owe? Identifying Your Liabilities

Next up is everything you owe. This side of the balance sheet can feel heavy, but facing it head-on is the only way to take back control. Liabilities are just any debts or financial obligations you have.

For example, a $30,000 student loan is a liability. So is a $15,000 car loan or a $5,000 credit card balance. List them all out.

Being honest and thorough here is critical. Ignoring a debt won’t make it go away, but listing it gives you the power to create a plan to get rid of it for good.

Calculating Your Net Worth: The Moment of Truth

Once you have your two lists, the math is simple:

Assets - Liabilities = Net Worth

Let’s walk through a quick example. Say your assets (home equity, savings, investments) add up to $150,000. Your liabilities (mortgage, car loan, student debt) total $95,000. That means your current net worth is $55,000.

This is just a snapshot in time. It doesn’t define you, but it does give you an objective way to measure your financial progress. Whether the number is positive or negative, it’s your starting line.

To make this even easier, you can plug your numbers into a simple calculator.

Simple Net Worth Calculator

Here’s a straightforward template to list your assets and liabilities, helping you calculate your current financial position.

| Category | Item Example | Estimated Value |

|---|---|---|

| Assets | Checking Account | $2,500 |

| Assets | Savings Account | $10,000 |

| Assets | 401(k) / Retirement | $25,000 |

| Assets | Home Value | $350,000 |

| Assets | Vehicle Value | $15,000 |

| Liabilities | Mortgage Balance | ($300,000) |

| Liabilities | Student Loan Debt | ($30,000) |

| Liabilities | Credit Card Debt | ($5,000) |

| Liabilities | Auto Loan | ($10,000) |

| Net Worth | Total | $57,500 |

Just replace the examples with your own numbers to find your net worth. From here, every smart financial move you make will help that number grow. For a more detailed walkthrough, you can learn more about how to track your net worth in our dedicated guide.

Build Your Financial Safety Net: The Emergency Fund

Now that you have a clear picture of your net worth, it’s time to build your financial shield. Life is predictably unpredictable—a sudden car repair, a surprise medical bill, or even a job loss can pop up without warning. An emergency fund is the buffer that keeps these moments from turning into full-blown financial crises.

This isn’t just another savings account. It’s a dedicated pool of cash set aside for life’s curveballs. Without it, you might be forced to sell investments at the worst possible time or rack up high-interest credit card debt, setting your goals back months or even years.

Think of it as buying yourself peace of mind.

How Much Do You Really Need?

The classic rule of thumb is to save three to six months of essential living expenses. Notice the word essential. This isn’t your total monthly income; it’s the bare-bones amount you need to keep the lights on if your paychecks suddenly stopped.

To figure out your magic number, add up your non-negotiable monthly costs:

- Housing: Your rent or mortgage, plus property taxes and insurance.

- Utilities: The average for electricity, water, gas, and internet.

- Transportation: Car payments, insurance, and a realistic budget for gas.

- Food: Your typical monthly grocery bill—be honest!

- Debt Payments: The minimum payments on student loans, credit cards, or personal loans.

So, if your essential monthly expenses come out to $2,500, your target emergency fund would be somewhere between $7,500 (three months) and $15,000 (six months).

Which end of the range is right for you? If you have a stable job and maybe even a second income stream, three months might be plenty. But if you’re a freelancer with unpredictable income or the sole provider for your family, aiming for six months provides a much stronger safety net.

The real goal here is to build a fund that lets you handle a major financial shock without panicking. It’s the foundation you build everything else on—from paying off debt to investing for the future.

Where Should You Keep This Money?

Your emergency fund needs to be two things: safe and accessible. This is not money you want to gamble in the stock market. But it shouldn’t be so accessible that you’re tempted to dip into it for a weekend getaway.

The perfect home for this cash is a high-yield savings account (HYSA). These accounts are FDIC-insured, meaning your money is protected up to $250,000. More importantly, they offer interest rates far higher than what you’d get at a traditional bank, allowing your fund to actually grow a little while it’s on standby.

Building this fund is a cornerstone of managing your finances, yet it’s a step many people struggle with. A staggering 55% of Gen Z adults, for instance, don’t have enough savings for a three-month emergency. On the bright side, a recent report found that 32% of Americans successfully saved for emergencies last year, often by opening high-yield savings accounts that earn up to 10 times more interest than standard ones.

Start Building Your Fund Today

Staring at a five-figure savings goal can feel intimidating. But you don’t have to get there overnight. The most important thing is to just start.

Put Your Savings on Autopilot The single most effective way to build this fund is to “pay yourself first.” Set up an automatic transfer from your checking to your high-yield savings account every single payday. Even $25 or $50 per check makes a huge difference over time. Automating it removes the temptation to spend that money elsewhere and guarantees you’re making consistent progress.

If you want more practical strategies, our complete guide walks you through exactly how to build an emergency fund from the ground up. Taking this one step is one of the most empowering things you can do for your financial future.

Design a Spending Plan You Can Actually Stick With

Let’s be honest, the word “budget” makes most of us want to run for the hills. It sounds like financial punishment, full of restrictions and spreadsheets. So, let’s ditch that word. We’re going to create a spending plan.

A spending plan isn’t about telling yourself “no.” It’s about empowering you to say “yes” to the things that actually matter. It’s the tool that finally aligns your money with your life, making sure your cash flows toward your real priorities, not just random expenses.

This whole process is less about accounting and more about awareness. You’ll shift from reacting to your bank balance to proactively directing it. Vague dreams become an actual roadmap. When you know where every dollar is headed, you’re back in the driver’s seat.

Choose a Framework That Fits Your Life

There’s no magic, one-size-fits-all budget. The best method is always the one you’ll actually stick with. Your personality, lifestyle, and how complicated your finances are will all point you toward the right strategy.

Here are a couple of popular frameworks that work for a reason:

-

The 50/30/20 Rule: This is your go-to for simplicity. You just carve up your after-tax income into three piles: 50% for needs (rent, bills, groceries), 30% for wants (restaurants, hobbies, that weekend trip), and 20% for savings and knocking out debt. It’s clean, simple, and incredibly effective.

-

Zero-Based Budgeting: This one’s for the person who wants total control and loves optimizing every penny. The idea is simple: give every single dollar a job. Your income minus all your planned spending, saving, and debt payments must equal zero at the end of the month. It’s precise and powerful.

Picking the right framework is half the battle. If you’re just getting started, the 50/30/20 rule is a fantastic, low-stress entry point. But if you’ve got an irregular income or you’re on a mission to hit a big savings goal, the laser focus of zero-based budgeting might be a better fit. You can dive deeper in our complete guide on how to budget money effectively.

Track Your Spending to Reveal Your Habits

You can’t build a realistic spending plan on guesswork. The single most eye-opening thing you can do is track what you actually spend for one full month. This isn’t about judging your past choices; it’s about collecting honest data.

Use an app, a spreadsheet, or just a small notebook to jot down every single purchase. You will be surprised where your money is really going. That daily $5 coffee? It’s a $150 monthly habit. Those streaming services you signed up for and forgot about? They could be costing you hundreds a year.

This isn’t an exercise in guilt. It’s about uncovering your financial DNA so you can make intentional choices that serve your future self.

Once you have this raw data, you can build a plan that works. If you see you’re spending $400 a month on dining out, trying to slash it to $50 overnight is a recipe for failure. A more realistic goal would be cutting back to $300. Just like that, you’ve freed up $100 to throw at something you care about more, like a vacation fund or that last bit of credit card debt.

Use the Right Tools to Make It Effortless

Let’s face it: manually logging every expense gets old, fast. Luckily, we live in an age where technology can do the heavy lifting, making it so much easier to stay on track.

Many banking apps now have built-in spending trackers that automatically sort your transactions into categories. Dedicated budgeting apps can sync all your accounts in one place, giving you a full 360-degree view of your financial life. These tools transform a boring list of numbers into helpful visuals, like pie charts, showing you exactly where your money is flowing.

To create a plan that sticks, a good online budget planner can be a game-changer. These resources often come with templates and calculators that take the grunt work out of the equation, removing the friction that makes so many people quit. The easier it is to see your progress, the more motivated you’ll be to keep going.

Create a Smart Strategy for Tackling Debt

Debt can feel like running on a treadmill you just can’t get off. You’re making payments every single month, but the balance barely seems to budge. The only way to break this cycle isn’t just throwing money at the problem; it’s about building a smart, strategic plan that puts you back in control.

Before you can attack your debt, you need to know exactly what you’re up against. This means creating a complete inventory of every single debt you hold. It might feel uncomfortable, but this clarity is the very first step toward financial freedom.

Go grab the statements for everything: credit cards, student loans, car payments, personal loans, and any outstanding medical bills. Create a simple list with three key columns for each one: the total balance owed, the minimum monthly payment, and the interest rate (APR).

Choosing Your Payoff Method

Once you see the full picture laid out, you can finally choose a real strategy. There are two incredibly effective methods, and they each tap into a different psychological motivator. Neither is right or wrong—the best one is simply the one that keeps you going.

Your debt payoff plan is a personal choice. The goal is to select the method that aligns with your personality and keeps you motivated for the long haul, ensuring you stick with it until you’re debt-free.

This is where you have to be honest with yourself. Are you motivated more by quick wins, or by saving the most money over time? Let’s break down the two most popular approaches.

The Debt Snowball Method

The Debt Snowball is all about building momentum. You start by listing your debts from the smallest balance to the largest, completely ignoring their interest rates. You keep making the minimum payments on all your debts, but you throw every extra dollar you can find at the smallest one.

Once that smallest debt is gone, you feel an immediate sense of victory. You then roll the entire payment you were making on that debt (the minimum plus all the extra) into the next-smallest debt on your list. This creates a “snowball” effect, where your payment size grows as you knock out each balance, dramatically accelerating your progress.

Who it’s for: This method is perfect if you need those quick, tangible wins to stay motivated. Seeing entire balances disappear provides a powerful psychological boost that can keep you committed.

The Debt Avalanche Method

The Debt Avalanche, on the other hand, is the most mathematically sound strategy. With this method, you list your debts from the highest interest rate down to the lowest, regardless of the balance. Again, you make minimum payments on everything, but you focus all your extra cash on the debt with the highest APR.

This approach attacks your most expensive debt first, which means you’ll pay far less in total interest over the life of your loans. While the initial wins might feel slower than the snowball method, the long-term savings can be massive. For example, tackling a credit card with a 24% APR before a student loan at 6% will save you a significant amount of money.

Who it’s for: If you’re driven by the numbers and want to minimize the total cost of your debt, the avalanche method is your best bet. It requires discipline but offers the greatest financial reward.

Picking the right strategy is a key part of learning how to manage personal finances effectively. Choose the one that feels most empowering to you, create your plan, and start taking those first crucial steps toward becoming completely debt-free.

Put Your Finances on Autopilot for Effortless Growth

Let’s be honest: the secret to consistently managing your money well isn’t about having superhuman discipline. It’s about building smart systems that do the heavy lifting for you.

Willpower runs out, but a well-designed system just keeps going. Automation is how you make real, consistent progress toward your financial goals without burning yourself out with constant decisions. By letting technology handle the routine stuff, you avoid decision fatigue and the trap of emotional spending. It’s the ultimate “set it and forget it” strategy for building wealth.

Pay Yourself First—Automatically

The idea of “paying yourself first” is simple but incredibly powerful. You prioritize your savings and investment goals before you pay any bills or spend a dime on anything else. The only way to make this stick is to take yourself out of the equation completely.

Set up an automatic, recurring transfer from your checking account to your savings and investment accounts. The key is to schedule this for the day you get paid (or the day after). When that money is gone before you even see it, you naturally learn to live on what’s left.

- Your emergency fund: Even a small, automatic transfer of $50 each week into a high-yield savings account will build a serious safety net over time.

- Your retirement accounts: If your job offers a 401(k), you’re already set—contributions come right out of your paycheck. For an IRA, just set up an automatic investment from your bank.

- Your other goals: Want to save for a vacation or a down payment? Open separate savings accounts for each goal and automate the transfers. It keeps everything organized and on track.

This one move ensures you’re always making progress. It turns saving from a monthly chore into a background habit, just like breathing.

Automate Bill Payments to Protect Your Finances

Late payments are the silent killers of your financial health. They rack up expensive fees, ding your credit score, and add a ton of unnecessary stress to your life. Automating your recurring bills is probably one of the easiest financial wins you can get.

Most of your big bills—rent or mortgage, utilities, car payments, insurance—can be set to autopay. You can usually do this right on the provider’s website or through your bank’s own bill pay service.

Automating your fixed expenses doesn’t just save you from late fees; it frees up a ton of mental bandwidth. You can stop worrying about due dates and focus your energy on bigger things, like optimizing your investments or planning for the future.

If you want to get really organized with all your recurring financial tasks, checking out the best recurring task app options can give you some great tools to streamline everything.

Why a System Beats Goals Every Time

Goals are great for setting a direction, but a reliable system is what actually gets you there. Automating your finances is that system. It’s what guarantees you’ll hit your targets.

It removes the daily temptation to overspend, the mental load of remembering due dates, and the emotional tug-of-war over whether to save or splurge.

Think of it this way: your financial goals are the destination. Your automated system is the self-driving car that takes you there. You just punch in the coordinates and let it run, knowing it’s moving you forward every single day.

Answering Your Top Personal Finance Questions

Even with the best-laid plans, you’re going to run into unique situations and nagging questions. It’s just part of the process. Think of this section as your quick-reference guide for some of the most common hurdles that pop up on the journey.

We’ve pulled together the top questions people have about managing their money and broken down the answers into clear, actionable advice. Having these answers ready can be the difference between getting stuck and pushing forward with confidence.

How Do I Start Investing if I Don’t Have a Lot of Money?

Let’s bust a huge myth right now: you do not need a pile of cash to start investing. The truth is, consistency and time are far more powerful than starting with a big lump sum. You can absolutely get started with very little.

One of the simplest on-ramps is a micro-investing app. These platforms are brilliant because they let you invest with spare change, either by rounding up your daily purchases or by setting up tiny, recurring contributions. It’s a fantastic way to build the habit without feeling the pinch in your budget.

Another excellent route is opening a Roth IRA. Many brokerages let you open one with no minimum deposit, so you can contribute small amounts whenever you can. Inside the account, you can buy into low-cost index funds or ETFs, giving you instant diversification across the market without having to pick individual stocks. The real key is just to start, no matter how small, to give your money the maximum amount of time to grow.

The magic of investing lies in compounding—where your earnings start generating their own earnings. Even small, consistent contributions can grow into a significant nest egg over decades. The most important step is simply getting started.

What Is More Important: Paying Off Debt or Saving for Retirement?

This is the classic financial tug-of-war, and the best answer is almost always a balanced approach, not an all-or-nothing decision. It’s rarely smart to completely ignore one for the other. The real strategy is about doing both, but prioritizing where each dollar goes.

Your first move, nearly without exception, should be to contribute enough to your employer’s retirement plan to get the full company match. Think of this as free money—often a 50% or 100% instant return on your contribution. Passing this up is like turning down a raise.

Once you’ve secured the full match, pivot your focus to your debts.

- High-Interest Debt: This is your top priority. We’re talking about credit card balances or personal loans with double-digit interest rates. The interest on this debt is a guaranteed loss that will almost certainly outpace any investment gains. Attack it aggressively.

- Low-Interest Debt: For debts like student loans or a mortgage with a lower interest rate, you can often stick to the regular minimum payments while you ramp up your retirement contributions.

This hybrid approach lets you fight back against costly debt while still giving your retirement savings the crucial time they need to compound and grow.

How Can I Improve My Credit Score Quickly?

You don’t need to wait years to see a better credit score. While building an excellent score is a long-term game, you can see significant improvements in just a few months by laser-focusing on the two factors that matter most.

The two pillars of a healthy credit score are your on-time payment history and your credit utilization ratio. Payment history is simple: pay every single bill on time, every single month. Set up autopay for at least the minimum payments to make sure you never miss one by accident.

Your credit utilization is the percentage of your available credit that you’re currently using. Lenders want to see this number below 30%. If your cards are maxed out, your score will take a nosedive. To get a quick boost, concentrate on paying down your card balances to get that ratio as low as possible.

Here are a few more quick tips:

- Check for Errors: Pull your credit reports from all three bureaus (it’s free once a year) and immediately dispute any mistakes you find.

- Don’t Close Old Accounts: The age of your credit history is a factor. Keeping old, unused cards open (as long as they don’t have an annual fee) helps your score.

- Avoid New Credit: Don’t apply for a bunch of new loans or credit cards in a short time. Each application can cause a small, temporary dip in your score.

Should I Use a Financial Advisor?

Deciding to hire a financial advisor really comes down to your personal situation, your confidence level, and how complex your finances are. You absolutely can learn how to manage personal finances on your own, but a good advisor brings valuable expertise to the table.

Consider hiring an advisor if:

- You’re Overwhelmed: If you feel paralyzed by all the choices and aren’t taking any action, an advisor can create a clear path forward.

- You Have a Complex Situation: Major life events like an inheritance, selling a business, or planning for a special needs child often benefit from professional guidance.

- You Want a Second Opinion: Even if you feel good about your plan, having an expert review it can provide peace of mind and expose any blind spots you might have missed.

If you do decide to get help, make sure you look for a fee-only fiduciary. This is critical. It means they are legally required to act in your best interest and get paid directly by you, not by earning commissions for selling you certain products. This structure ensures their advice is aligned with your goals, not their bottom line.

Ready to stop juggling spreadsheets and gain a crystal-clear view of your financial life? PopaDex is the intuitive net worth tracker that brings all your accounts into one simple, powerful dashboard. See your progress, set meaningful goals, and take control of your financial future. Start your free trial today at popadex.com.