Our Marketing Team at PopaDex

How to Pay Off Debt A Practical Guide

The first step in taking control of your debt isn’t some complex financial maneuver—it’s deceptively simple. You need to create an honest, complete inventory of everything you owe. This is where you gather up all your statements and lay the cards on the table, turning vague anxiety into actionable data.

Your Financial Snapshot: Creating a Clear Debt Inventory

Before you can attack your debt, you have to know exactly what you’re up against. I know, facing those numbers head-on feels intimidating, but this single action is the most critical part of your entire journey. This isn’t about judging past decisions; it’s about gathering intelligence to build a winning strategy.

Think of it like a general preparing for battle. You wouldn’t send troops into the field without a map, right? A debt inventory is your financial map, revealing every hill and valley you need to navigate. This clarity stops the guesswork and ends the cycle of feeling overwhelmed by an unknown enemy.

Gathering Your Financial Documents

Time to roll up your sleeves and collect every single document related to what you owe. Don’t leave anything out, no matter how small it seems. The goal here is 100% transparency.

Your list should include:

- Credit Card Statements: Pull the most recent statement for every single card, from major bank cards to that store card you forgot about.

- Loan Agreements: This means auto loans, personal loans, and even your mortgage.

- Student Loan Details: Log into your federal and private loan servicer portals to get the latest, most accurate info.

- Medical Bills: Grab any outstanding bills from hospitals, clinics, or doctors that haven’t been paid off.

- Other Debts: Don’t forget “buy now, pay later” balances or any personal loans from family or friends.

Once you have everything, create a simple list or spreadsheet. For each debt, you need four key pieces of information: the creditor, the total balance, the minimum monthly payment, and the interest rate (APR). To make this even easier, you might find using a single tool to see everything in one place is a game-changer. For a deeper look at organizing this, check out our guide on using a net worth tracking spreadsheet.

To help you get started, here’s a straightforward template to organize your debt inventory.

Your Personal Debt Inventory

Use this template to organize every debt you have. This clarity is the first step toward creating an effective payoff plan.

| Creditor Name | Type of Debt (e.g., Credit Card, Student Loan) | Total Balance | Minimum Monthly Payment | Interest Rate (APR) |

|---|---|---|---|---|

Filling this out will give you the complete picture you need to move forward with confidence.

Why This Step Cannot Be Skipped

Ignoring the full scope of your debt is like trying to navigate a ship in thick fog. You might feel like you’re moving, but you have no idea if you’re headed toward your destination or straight for the rocks. A complete inventory empowers you to make smart, informed decisions.

This foundational step transforms a vague cloud of financial stress into a concrete list of problems you can solve one by one. It’s the moment you stop being a victim of your debt and start becoming its master.

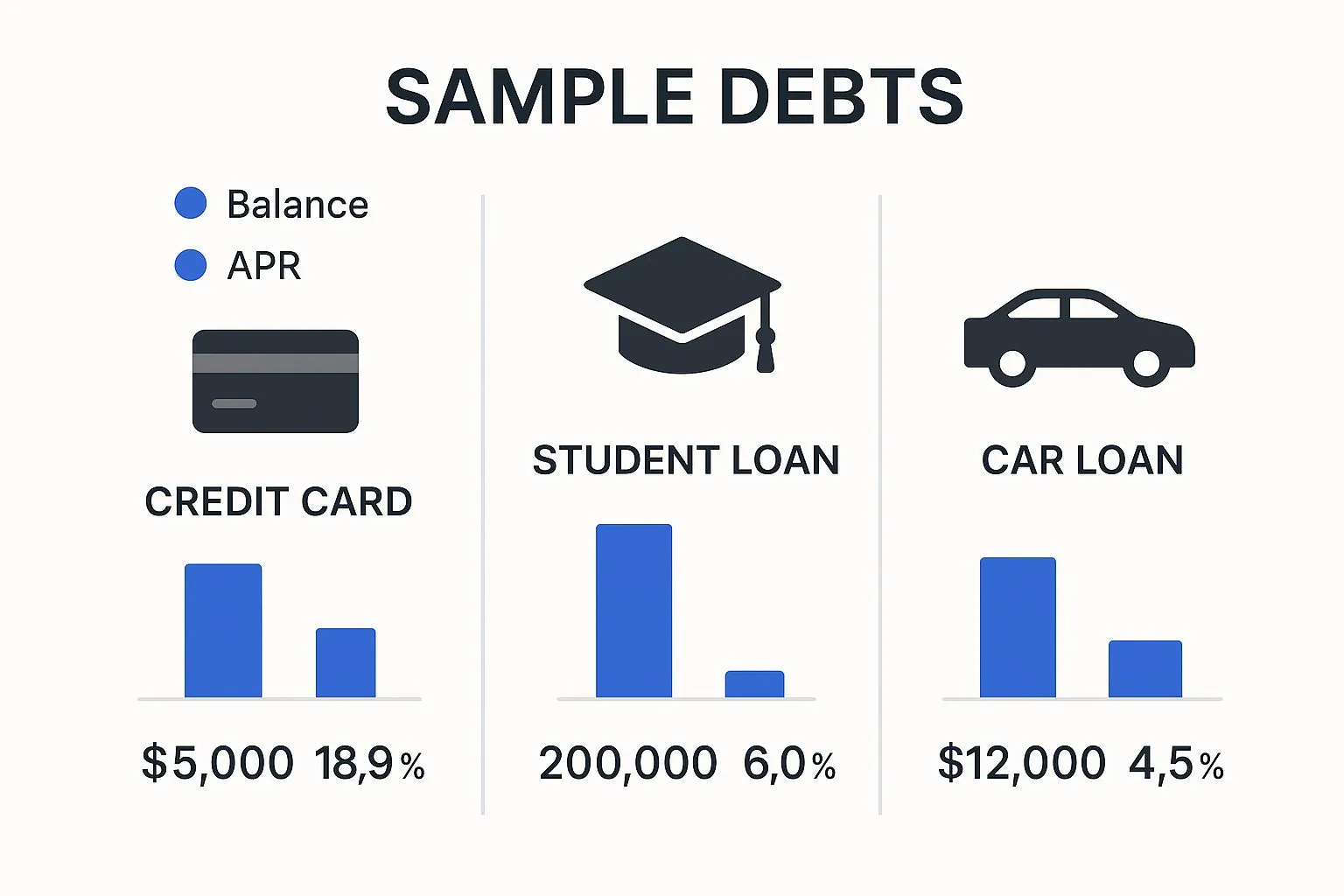

The image below shows just how different your debts can be, which is why seeing all the numbers is so critical.

This example makes it obvious: the credit card has the smallest balance but by far the highest interest rate. That’s a crucial detail that will directly influence which payoff strategy you choose later on.

Choosing Your Strategy: The Snowball vs. Avalanche Method

Okay, you’ve done the hard part—you’ve laid all your debts out on the table and you know exactly what you’re up against. Now for the fun part: deciding how you’re going to attack them.

The two heavyweights in the debt payoff world are the Debt Snowball and the Debt Avalanche.

Think of these less as rigid financial plans and more as two different philosophies for getting to the finish line. One is all about psychology and momentum, while the other is pure, cold, hard math. Let’s break down how they work in the real world so you can pick the one that you’ll actually stick with.

The Debt Snowball: Winning with Momentum

The Debt Snowball method is designed for anyone who thrives on seeing progress. It’s all about building momentum with quick, tangible wins. If you need that little boost of motivation to keep going, this is probably your best bet.

Here’s the game plan:

- Order Your Debts: Line up all your debts from the smallest balance to the largest. Don’t even look at the interest rates for now.

- Focus Your Attack: Keep making the minimum payments on everything. But every single extra cent you can find goes directly to the debt with the smallest balance.

- Celebrate and Roll: Once that smallest debt is gone—poof!—you celebrate that win. Then you take its entire payment (the minimum plus all the extra cash) and “roll” it over to the next smallest debt on your list.

This creates a powerful “snowball” effect. With each debt you knock out, the amount you’re throwing at the next one gets bigger and bigger, making you feel like an unstoppable debt-crushing machine.

Popularized by financial guru Dave Ramsey, the Debt Snowball is a classic for a reason. It taps into behavioral psychology, using those early victories to keep you disciplined. A 2019 survey revealed that 65% of people using this method cleared their consumer debts within three years, a significant jump from the 42% using other strategies. You can dive deeper into the history behind various debt strategies and government policies to see how these ideas have evolved.

The Debt Avalanche: Saving the Most Money

If the Snowball is about feeling good, the Avalanche is all about being ruthlessly efficient. This is the numbers-driven approach. The goal here is simple: pay the least amount of interest possible and get out of debt for the lowest total cost.

The steps are nearly identical, but the target is different:

- Order by APR: List your debts from the highest interest rate (APR) down to the lowest. The actual balance doesn’t matter for this ranking.

- Target High Interest: You’ll make minimum payments on all your debts, but every spare dollar is aimed squarely at the one with the highest APR.

- Rinse and Repeat: Once that high-interest monster is slain, you take its entire payment and apply it to the debt with the next-highest APR.

With this strategy, you’re systematically taking out the debts that are costing you the most money first. It might take longer to get your first “win” if your highest-APR debt has a big balance, but mathematically, this is the fastest and cheapest path to becoming debt-free.

A Real-World Comparison

Let’s make this tangible. Imagine these three debts are sitting on your list:

- Store Credit Card: $500 at a painful 24.99% APR

- Personal Loan: $3,000 at 11% APR

- Auto Loan: $8,000 at 5.5% APR

With the Debt Snowball, you’d laser-focus on that $500 store card. Why? Because it’s the smallest. Paying it off quickly gives you an incredible psychological boost and the confidence to keep going.

Using the Debt Avalanche, you’d also attack the $500 store card first. But the reason is different—it’s because that 24.99% interest rate is an absolute killer. In this case, both roads lead to the same starting point. But if your personal loan had a higher APR, the Avalanche would demand you tackle it first, despite its larger balance.

Snowball vs Avalanche: Which Method Is Right for You?

Still on the fence? This table breaks down the core differences to help you decide which approach aligns with your personality and financial style.

| Feature | Debt Snowball | Debt Avalanche |

|---|---|---|

| Primary Goal | Build motivation through quick wins | Minimize total interest paid |

| Debt Order | Smallest balance to largest balance | Highest APR to lowest APR |

| Best For | People who need to see fast progress to stay motivated | People who are disciplined and want the most efficient path |

| Psychological Edge | High. Early wins provide a powerful emotional boost. | Lower. It can take a while to pay off the first debt. |

| Financial Edge | You may pay more in total interest over time. | Mathematically the fastest and cheapest way to eliminate debt. |

| Core Principle | Behavior and momentum | Logic and math |

The big question you need to ask yourself is: What will keep me in the fight? Are you motivated by checking debts off a list, or by the knowledge that you’re saving every possible dollar?

Ultimately, there’s no single “correct” answer. The best strategy is the one you can commit to month after month without giving up. Pick the path that feels right for you, and start walking.

Crafting a Budget You Can Actually Live With

Any solid debt payoff strategy, whether it’s the Snowball or the Avalanche method, needs fuel to keep going. And that fuel? It comes directly from your budget.

Let’s be real, though. The word “budget” probably makes you think of complicated spreadsheets and saying goodbye to everything you enjoy. That’s a surefire way to burn out and give up.

The secret to learning how to pay off debt isn’t about deprivation; it’s about being intentional. A good budget doesn’t just track your spending—it forces your money to align with your most important goals, like finally becoming debt-free.

Find Your Money with a Spending Audit

Before you can tell your money where to go, you have to see where it’s been going on its own. This is where a quick and simple ‘spending audit’ is a game-changer. Think of it as a judgment-free look at the last 30 to 60 days of your financial life.

Just pull up your recent bank and credit card statements and start sorting your purchases into basic categories. You don’t need fancy software for this; a simple notebook or spreadsheet will do the trick just fine. Add up what you spent on essentials like housing and groceries, then do the same for variable costs like dining out, subscriptions, and entertainment.

I can almost guarantee you’ll find some surprises. That “quick” daily coffee might be costing you over $100 a month. You might even be paying for three different streaming services you forgot you had. These aren’t failures; they’re opportunities—small, painless cuts that can free up a surprising amount of cash for your debt payoff plan.

The 50/30/20 Rule: A Simple Framework

Once you have a clear picture of your spending, you need a simple framework to guide your money going forward. The 50/30/20 rule is a fantastic place to start because it’s so flexible and easy to remember. It just splits your after-tax income into three buckets:

- 50% for Needs: This slice of the pie covers your absolute must-haves. We’re talking about housing, utilities, groceries, transportation, and your minimum debt payments. These are the bills that have to be paid every month, no matter what.

- 30% for Wants: This is the fun stuff—everything that makes life more enjoyable but isn’t strictly necessary for survival. This includes going out to eat, your hobbies, Netflix, and vacation savings.

- 20% for Savings & Debt Repayment: This final chunk is all about building your financial future. It covers retirement contributions, building an emergency fund, and—most importantly for our mission—making extra payments on your debt.

This framework helps you attack your debt aggressively without feeling like you have to give up your entire life. It’s a balanced approach that makes the whole process sustainable. If you want to dive deeper, our guide on how to budget money breaks down this method and a few others in great detail.

Your budget is not a financial straitjacket; it’s a tool for freedom. It gives you permission to spend on your priorities—and right now, your main priority is getting out of debt.

Making It Work for You

Remember, the 50/30/20 rule is a guideline, not a law set in stone. If you live in an expensive city and your “Needs” are closer to 60% of your income, that’s okay. You’ll just need to adjust somewhere else, maybe by trimming your “Wants” down to 20% to keep your debt repayment goals on track.

The real power here comes from making conscious choices. Maybe you realize you’re spending $150 a month on lunches out and unused subscriptions. What if you redirected that exact amount to your highest-interest credit card? That one small change could save you hundreds in interest and knock months off your payoff timeline.

To get a truly professional handle on your budget, using a solid cash flow analysis template can be a huge help in seeing exactly where every dollar goes.

Finally, your budget isn’t a “set it and forget it” document. Life changes, and so should your budget. Check in with it every month to see what’s working and what isn’t. By staying flexible and focused, you’ll build a powerful financial plan that puts you on the fast track to becoming completely debt-free.

How to Accelerate Your Debt Payoff

Once you have a budget and a clear payoff strategy, it’s time to shift from defense to offense. Making only minimum payments is like trying to empty the ocean with a teaspoon—it’s slow, frustrating, and the interest just keeps rolling in like the tide. If you’re serious about learning how to pay off debt efficiently, you have to find ways to throw more cash at your balances.

This all comes down to creating a bigger gap between what you earn and what you spend. We’ll dive into two powerful ways to make this happen: boosting your income and making strategic cuts to your spending. You’d be surprised how combining even small efforts in both areas can create a serious financial surplus to speed up your journey to freedom.

Boosting Your Income on Your Terms

Finding extra money doesn’t have to mean clocking in for a traditional second job. The modern gig economy gives you incredible flexibility to earn more cash in short bursts, even if you only have a few hours to spare each week. The trick is to find something that fits the schedule and skills you already have.

Consider a few flexible options:

- Leverage a Skill You Already Have: Are you a wizard with words, a graphic design pro, or an Excel guru? Websites like Upwork or Fiverr are full of clients looking for freelancers for project-based help.

- Turn Your Car into an Asset: Driving for a rideshare service or delivering food can be done whenever you find a free moment, whether it’s an hour after your day job or a full day on the weekend.

- Monetize Your Unused Stuff: Services like Turo let you rent out your car when it would otherwise be sitting idle. You could also think about renting out a spare room or even specialized tools you own.

Even an extra $200 a month channeled directly toward your debt can make a massive difference. It’s not just about the numbers; it’s about reclaiming a sense of control and actively building the momentum you need to crush your financial goals.

Strategically Cutting Your Major Expenses

While earning more is a great move, plugging the leaks in your current budget is just as critical. I’m not talking about skipping your morning latte—I’m talking about high-impact areas where a little effort can lead to big savings. Your recurring monthly bills are the perfect place to start.

Most people assume their monthly bills for things like cable, internet, and cell phones are set in stone. The reality is, these rates are often negotiable. A single phone call can unlock significant savings you can immediately redirect to your debt.

A quick call to your provider to simply ask for a better rate is surprisingly effective. Tell them you’re reviewing your budget and looking for ways to lower your expenses. Ask if they have any new promotions or loyalty discounts available. More often than not, they’d rather give you a better deal than risk losing you as a customer.

Mastering the Art of Negotiation

Negotiating bills can feel intimidating, but it’s a skill that pays for itself over and over again. A little preparation makes all the difference. Before you dial, do a quick search for what their competitors are offering so you can mention specific prices.

Here’s a simple script you can adapt:

“Hi, I’ve been a loyal customer for X years, and I’m currently looking at my budget. I’ve noticed [Competitor Name] is offering a similar plan for [Price]. I’d much rather stay with you, but I need a more competitive rate. Is there anything you can do to help lower my monthly bill?”

This approach is polite, direct, and shows you’ve done your homework. The worst they can say is no, but even a small reduction of $20-$30 per month adds up to hundreds of dollars a year. That’s money that can now go toward paying down debt. You can use this same tactic for car insurance, gym memberships, and other recurring services. Pairing these savings with a tool like our debt payoff calculator spreadsheet will show you exactly how much faster you can hit your goals.

The data backs this up. The U.S. Federal Reserve has shown that making only minimum payments on a $5,000 credit card balance at 18% interest can take over 10 years and cost $4,500 in interest alone. But if you add an extra $100 per month? You could clear that same debt in under four years and save thousands. It’s easy to see why global surveys found that disciplined budgeting and automatic payments improve debt payoff success by 30%-40%.

Smart Ways to Lower Your Interest Rates

High-interest rates are the real enemy when you’re trying to pay off debt. They quietly pad your balances each month, making you feel like you’re stuck on a treadmill. If you want to make real progress and see those principal balances shrink, you have to get aggressive about lowering the rates you’re paying. That’s how more of your hard-earned money starts working for you, not against you.

Let’s walk through a few proven tactics for tackling high APRs, from consolidation loans and balance transfers to good old-fashioned negotiation. Each one offers a different path toward cutting your interest costs and speeding up your journey to being debt-free.

Using a Debt Consolidation Loan

Think of a debt consolidation loan as a way to simplify and save. You take out one new personal loan and use those funds to wipe out several high-interest debts, like multiple credit cards or lingering medical bills. The key is to lock in a new loan with a much lower interest rate than the average of the debts you’re paying off.

This strategy immediately cleans up your financial life, replacing a handful of monthly payments with just one predictable bill. But the real win is the interest savings. A lower rate means a bigger chunk of your payment goes toward the principal balance every single month. This can shave years off your repayment schedule and save you a ton of cash.

For instance, someone consolidating $10,000 of credit card debt from a 15% APR down to a personal loan at 7% APR could potentially cut their payoff time from seven years to under four. That single move could reduce the total interest paid by around 40%. You can see how these personal finance strategies fit into the bigger picture by looking at data on global debt management.

Leveraging a Balance Transfer Credit Card

A balance transfer credit card is another seriously powerful tool. These cards often feature a promotional period—usually between 12 and 21 months—where you pay 0% APR on balances you move over from other high-interest cards.

You’re essentially getting an interest-free loan for a year or more, which creates a golden opportunity to make a huge dent in your debt. During that intro period, every single dollar you pay goes straight to the principal. It’s an amazing way to attack your balance without interest constantly working against you.

This approach does require some discipline, though. Keep these things in mind:

- Balance Transfer Fees: You’ll almost always pay a one-time fee, typically 3% to 5% of the amount you transfer.

- The Cliff: If you don’t clear the balance before the promo period ends, the remaining amount gets hit with the card’s standard (and often very high) interest rate.

- Credit Requirements: The best offers are reserved for people with good to excellent credit, so you’ll need a solid score to qualify.

Calling Your Creditors to Negotiate

Sometimes, the simplest approach works best. A lot of people don’t even realize this is an option, but you can often negotiate your credit card interest rates. A quick phone call to your credit card company could easily result in a lower APR, especially if you have a history of paying on time.

When you call, be friendly but direct. Let them know you’re serious about paying down your debt and that a lower rate would help you get there faster.

“Hi, I’m reviewing my finances and working hard to pay down my balance. I’ve been a loyal customer for [Number] years and I’m hoping you can help me with a lower interest rate. Is there anything you can do for me?”

This little script is all it takes to open the conversation. If the first person you talk to says no, don’t give up. Politely ask to speak with a supervisor or someone in the retention department—they usually have more power to make you a better offer to keep you as a customer.

Even shaving a few percentage points off your APR can save you hundreds of dollars over time. It’s absolutely a call worth making.

Staying Motivated on Your Path to Financial Freedom

Let’s be real: paying off debt is a marathon, not a sprint. The initial adrenaline rush you get from finally making a budget and picking a payoff strategy is incredible. But keeping that fire alive over months—or even years—takes real work. It’s completely normal for your motivation to wane, so the trick is to have systems in place to keep you on track when willpower alone isn’t enough.

One of the best ways to stay in the game is to see your progress. I mean really see it. A visual tracker, like a chart you color in or a digital dashboard, turns abstract numbers into a tangible win. Every single time you knock out a balance or throw extra cash at a loan, you get that little hit of satisfaction that keeps you going.

Create a Supportive Environment

You don’t have to do this alone. In fact, you probably shouldn’t. Sharing your goals with a trusted partner, friend, or family member can be a game-changer. This isn’t about having someone scrutinize your spending; it’s about having an accountability partner who celebrates your wins and gives you a pep talk when you feel like throwing in the towel.

Another key part of your support system? A small emergency fund. Even just $500 or $1,000 tucked away can be the difference between a minor hiccup and a full-blown crisis. Think of it as a buffer. When the car needs a new tire or an unexpected medical bill pops up, you can handle it without reaching for a credit card and undoing all your hard work.

Life after debt goes beyond reaching a zero balance; it’s about fundamentally shifting your relationship with money from a defensive posture of repayment to an offensive one of wealth creation.

As you get into the nitty-gritty of your debt-free journey, keeping your eye on the prize is everything. Understanding frameworks like setting SMART goals helps you turn a vague wish into a concrete plan. Breaking down a huge goal into smaller, specific milestones makes the whole process feel less overwhelming and gives you plenty of reasons to celebrate along the way.

Shifting to a Wealth-Building Mindset

Here’s where things get really exciting: planning for what’s next. As you start to see the light at the end of the tunnel, begin dreaming about your “after-debt” life. What will you do with all that cash you were sending to creditors every month?

This is your pivot point—the moment you switch from a repayment mindset to a wealth-building mindset. That extra $300, $500, or $1,000 a month is now your tool for building the future you want.

Here are a few ideas for redirecting that newfound cash flow:

- Supercharge Your Retirement: Max out your 401(k) contributions or open an IRA.

- Build a Real Emergency Fund: Beef up that starter fund to cover a full 3-6 months of living expenses.

- Invest for Big Goals: Start a fund for a down payment on a house or open a taxable brokerage account.

The skills you master while getting out of debt—budgeting, discipline, saying “no” to impulse buys—are the exact same skills that build serious wealth. By planning what comes next, you’re not just running from something negative; you’re running toward a positive, prosperous future. And that makes the final push so much easier.

Common Questions on the Path to Debt-Free

As you start wrestling your debt to the ground, a lot of questions pop up. It’s totally normal. Getting good, straight answers is what keeps you motivated and moving in the right direction. Let’s dig into some of the most common ones I hear.

Should I Stop Investing to Pay Off My Debt?

This one’s a classic, and the best answer usually comes down to simple math. You need to pit the interest rate you’re paying on your debt against the return you could reasonably expect from your investments.

Think about it this way: if you’re carrying a credit card with a brutal 22% APR, finding a guaranteed investment that can beat that is pretty much impossible. In a scenario like that, it makes a ton of financial sense to hit pause on investing and throw every spare dollar at that high-interest monster.

But the script flips if your only debt is something like a mortgage with a low 4% interest rate. In that case, continuing to invest—especially if you’re getting an employer match in your 401(k)—is almost always the smarter long-term play. The growth potential of your investments is very likely to outrun the cost of that low-rate debt.

As a rule of thumb, it’s wise to focus on paying down any debt with an interest rate higher than what the stock market historically returns, which is in the ballpark of 7-10% per year.

What if I Can Only Make the Minimum Payments?

Finding yourself in a spot where only minimum payments feel possible is tough, but the absolute first priority is to not fall behind. Stay current, no matter what.

From there, it’s time to get surgical with your budget. Comb through every single expense to see if you can squeeze out even a little extra cash. You’d be surprised what you can find.

Even an extra $25 a month tossed at your debt can start to chip away at the principal and save you money on interest over time. If that’s just not in the cards, then you have to shift your focus to the other side of the financial equation: boosting your income. That could mean picking up a side gig, asking for a raise, or finding a better-paying job.

Ready to stop guessing and start seeing real progress? PopaDex gives you the interactive dashboards and powerful calculators you need to build a clear, actionable debt payoff plan. See all your numbers in one place and finally take control. Get started at popadex.com and build your plan today.