Our Marketing Team at PopaDex

how to save money monthly: practical budgeting tips

If you want to save more money each month, the simplest place to start is with a clear plan for your income. The 50/30/20 rule is a fantastic framework for this. The idea is to divide your after-tax pay into three buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It’s an immediate, no-fuss way to get a handle on your cash flow.

Building Your Monthly Savings Foundation

Before you get lost in complex spreadsheets or super-restrictive budgets, the first real step is building a healthy savings mindset. Getting ahead financially isn’t about slashing every single expense that brings you joy. It’s about knowing where your money is actually going and making conscious choices that line up with what you really want long-term.

Honestly, saving can feel impossible. The personal saving rate in the U.S. was just 4.6% in August 2025, which means many people are saving less than a nickel of every dollar they earn. That number highlights a massive challenge, but it also shows there’s a huge opportunity to do better with the right approach.

Understanding The 50/30/20 Framework

Think of the 50/30/20 rule less as a rigid law and more as a powerful diagnostic tool. It gives you a quick snapshot of your spending habits and immediately flags any imbalances. It’s like a financial health check-up that shows if you’re overdoing it on “wants” or not putting enough away for your future.

Here’s how the breakdown works:

- Needs (50%): These are your non-negotiables—the expenses you absolutely have to pay. We’re talking about housing, utilities, groceries, transportation, and insurance.

- Wants (30%): This is all the discretionary spending that makes life more enjoyable but isn’t essential for survival. Think dining out, hobbies, streaming subscriptions, and travel.

- Savings & Debt (20%): This is the slice dedicated to building wealth and securing your financial future. It covers everything from building an emergency fund and contributing to retirement accounts to investing and making extra payments on high-interest debt.

Let’s look at this in a bit more detail.

The 50/30/20 Budgeting Rule Explained

This table breaks down how to allocate your after-tax income to balance needs, wants, and savings goals effectively.

| Category | Percentage Allocation | What It Covers | Example (on $4,000/month) |

|---|---|---|---|

| Needs | 50% | Rent/mortgage, utilities, groceries, insurance, essential transportation. | $2,000 |

| Wants | 30% | Dining out, entertainment, shopping, hobbies, travel. | $1,200 |

| Savings & Debt | 20% | Emergency fund, retirement, investments, extra debt payments. | $800 |

By sorting your spending into these three simple buckets, you can make informed decisions instead of just guessing where you need to cut back.

The goal is clarity, not restriction. By seeing your spending in these three buckets, you can make informed adjustments instead of guessing where to cut back. This mental shift is a crucial part of learning how to organize finances effectively for long-term success.

To get started on your own financial journey, you can check out these proven strategies to save money each month. This framework gives you a solid foundation to build upon as you get more comfortable managing your money.

Winning the Battle Against Your Biggest Expenses

Cutting out daily lattes is fine, but it’s not going to move the needle on your financial goals. If you really want to learn how to save money every month, you have to go after the big fish—the three largest spending categories that eat up most of your budget: housing, transportation, and food.

Making a few smart changes here can free up hundreds of dollars, not just a few bucks. These “Big Three” might feel like fixed costs, but there’s often more wiggle room than you think. One good decision in any of these areas can have a bigger impact than a year of small sacrifices. It’s all about working smarter, not harder.

Reassessing Your Housing Costs

For most of us, our rent or mortgage is the single biggest bill we pay each month. That makes it the perfect place to start looking for serious savings. If you’re a renter, never assume the price is set in stone.

When my last lease was up for renewal, I did some digging. I researched what similar apartments in my neighborhood were going for and discovered that new tenants were getting better deals. Armed with that data, I shot my landlord a polite email.

I reminded them I was a reliable tenant who always paid on time and kept the place in good shape. Then, I showed them the lower market rates for comparable units. The result? They knocked $150 off my monthly rent just to avoid the hassle of finding someone new.

“Your biggest expenses offer the biggest savings opportunities. A 5% reduction on a $2,000 rent payment saves you $1,200 a year. You’d have to skip over 200 coffees to save the same amount.”

Analyzing Your True Transportation Expenses

Transportation is the second area where costs can easily get out of hand. Owning a car often feels like a non-negotiable, but it’s crucial to understand the total cost, not just the monthly payment.

Think about all the hidden costs that pile up:

- Insurance: This can swing wildly depending on your car, location, and driving history.

- Fuel: Gas prices are a constant source of budget anxiety.

- Maintenance & Repairs: The USDA says clothing for a young child costs about $55 per month, but one unexpected car repair can easily blow ten times that amount out of your budget.

- Depreciation: This is the silent killer. Your car loses value every single day, which is a very real, though invisible, expense.

Do a quick cost-benefit analysis. Could you get by with public transit, ride-sharing, or even a bike for a fraction of the cost? Selling a second car or trading in a gas-guzzler for a more efficient model can instantly free up a huge chunk of your income. To truly see the numbers, you first need to know how to track expenses effectively.

Conquering Your Grocery Bill

Finally, food is a variable expense that gives you daily opportunities to save. The trick is to shift from reactive shopping to proactive planning. The two biggest budget killers here are impulse buys and food waste.

I’ve found a simple weekly meal plan works wonders. Before I even think about going to the store, I map out our dinners for the week. I check the pantry for what I already have and then build my shopping list based only on what’s missing.

This one habit stopped me from wandering aimlessly down aisles and dramatically cut down on the sad, wilted produce I used to find in my fridge. By getting a handle on these three core areas, you’re not just trimming the fat—you’re targeting the heart of your spending to unlock your real savings potential.

Putting Your Savings on Autopilot

Let’s be honest: the easiest way to save money every month is to take willpower completely out of the picture. When you automate your savings, it just happens in the background. It stops being a daily choice and becomes an effortless habit. This is the modern, supercharged version of the classic “pay yourself first” strategy.

The idea is simple but incredibly effective: set up an automatic transfer from your checking to your savings account for the exact day your paycheck lands. Don’t wait to see what’s left at the end of the month. Move your savings first, before you even have a chance to spend it. This makes your financial goals the priority, not an afterthought. For a full walkthrough, our guide can show you exactly how to automate your finances step-by-step.

The Power of High-Yield Savings

To get the most bang for your buck, don’t just transfer that money into any old savings account. Make sure it’s going into a high-yield savings account (HYSA). Unlike the accounts at most big banks that pay next to nothing, an HYSA offers a much higher interest rate. This means your money actually grows while it sits there. You’re using the same simple process, but your money is working much harder for you.

Your savings account should be a tool for building wealth, not just a digital piggy bank. An HYSA turns your savings into a source of meaningful passive income, whether it’s for your emergency fund or a long-term goal.

Effortless Micro-Saving with Modern Apps

Another great automation trick is using micro-saving apps. These tools are genius. You link them to your debit card, and they round up your daily purchases to the nearest dollar, sweeping the spare change into a separate savings or investment account.

- How it works: You grab a coffee for $3.50. The app automatically rounds it up to $4.00 and tucks that extra $0.50 away for you.

- The impact: It might sound like just a few cents here and there, but you’d be amazed at how quickly it adds up. Over a year, this “digital spare change” can easily grow into a few hundred dollars without you ever feeling the pinch.

This approach helps build a powerful saving habit, mirroring trends seen in other proactive saving cultures. For instance, the household saving rate in Ireland hit 14.0% in the first quarter of 2025, with households socking away a total of €8.2 billion through things like pension contributions and bank deposits. You can read more about these household saving trends and insights on CSO.ie.

When you combine scheduled HYSA transfers with micro-saving, you create a powerful, two-pronged system that builds your savings on autopilot.

Tackling Debt to Unlock Your Savings Potential

High-interest debt is the silent killer of your savings goals. It’s working against you around the clock, and every dollar you pay in interest is a dollar you can’t put toward your future. Paying it down is more than a financial chore; it’s one of the most powerful moves you can make to free up serious cash flow.

When you’re fighting a battle on two fronts—trying to save while servicing expensive debt—you often feel like you’re losing ground. Think of high-interest debt like a hole in your financial bucket. No matter how much you pour in (savings), money is constantly leaking out (interest payments). Plugging that hole is the fastest way to actually start filling the bucket.

Choosing Your Debt Repayment Strategy

Two proven methods can help you systematically wipe out debt: the Debt Snowball and the Debt Avalanche. The best one for you comes down to your personality and what keeps you in the game. One is all about psychological wins, while the other is pure math.

With the Debt Snowball method, you focus on paying off your smallest debts first, no matter their interest rate. You’ll make minimum payments on everything else, but every extra dollar you have gets thrown at that smallest balance. Once it’s gone, you roll that entire payment amount onto the next-smallest debt. This creates a “snowball” of momentum that can feel incredibly motivating.

On the flip side, the Debt Avalanche method targets your highest-interest debt first. While you make minimum payments on all your other accounts, you channel all available funds to the debt with the highest APR. This approach is the clear winner mathematically, saving you the most money on interest over time, but the progress can feel a bit slower at the start.

Debt Snowball vs Debt Avalanche A Comparison

Looking at these two popular strategies side-by-side can make it easier to decide which path is right for your financial journey.

| Method | How It Works | Best For | Key Benefit |

|---|---|---|---|

| Debt Snowball | Pay off debts from smallest to largest balance. | People who need quick, motivational wins to stay on track. | Psychological Boost The satisfaction of clearing debts fast builds momentum. |

| Debt Avalanche | Pay off debts from highest to lowest interest rate. | People focused on pure math and long-term savings. | Financial Efficiency Saves the most money possible on interest payments over time. |

Ultimately, the best strategy is the one you’ll stick with.

When to Consider Debt Consolidation

If you’re juggling multiple high-interest debts, like a few different credit card balances, just managing the payments can feel like a full-time job. This is where debt consolidation comes in. The idea is to take out a single, new loan to pay off all your other debts at once. The goal is to lock in a lower overall interest rate and simplify your finances down to just one monthly payment.

This approach can be a game-changer, but only if the new loan’s interest rate is significantly lower than the average rate of your existing debts. It’s a tool for simplification and cost-saving, not an excuse to take on more debt.

To see if this strategy makes sense for you, it’s worth exploring the various debt consolidation loan options available. It could be the move that simplifies your financial life and cuts down your interest payments.

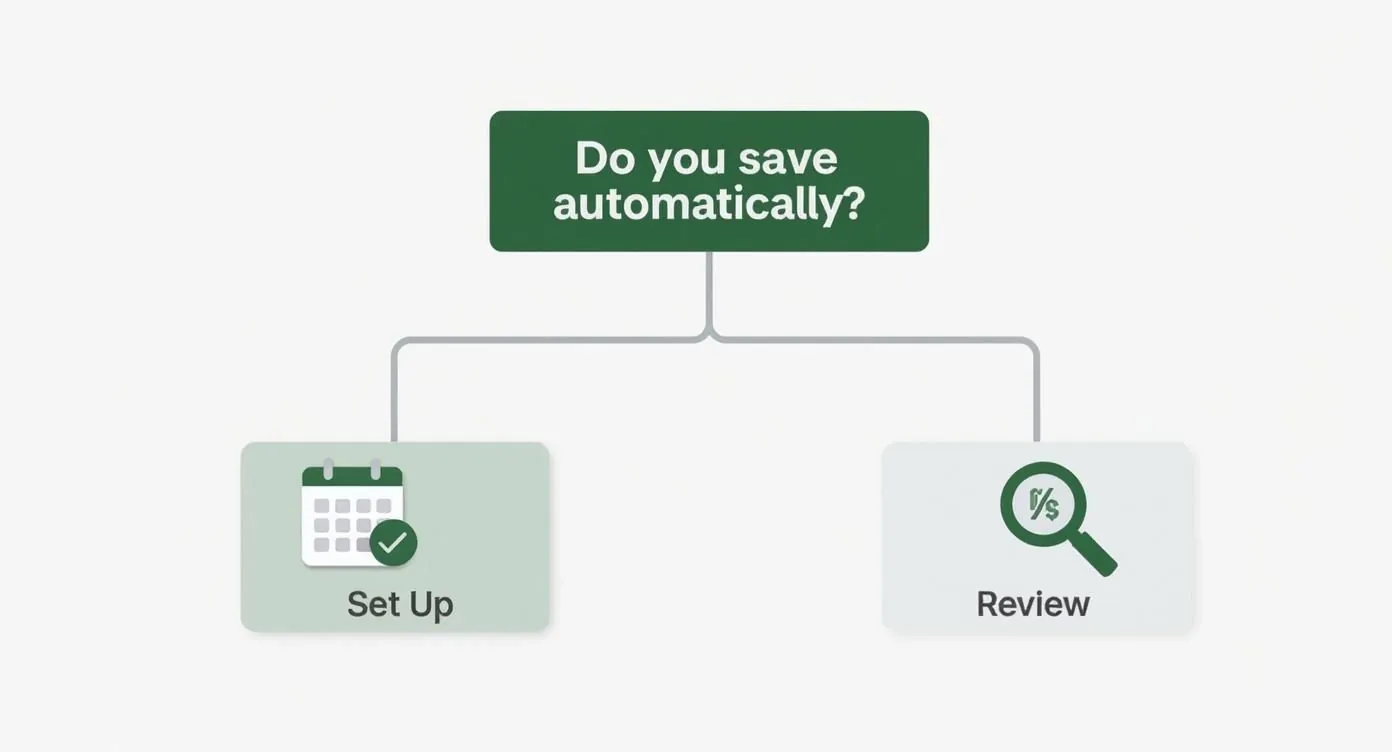

Deciding on the next step can be tricky, but the decision tree below can help you figure out where to focus your energy.

This visual guide shows that whether you’re just starting out or fine-tuning an existing system, taking proactive steps is the key to consistent saving.

Boosting Income and Spending Mindfully

https://www.youtube.com/embed/2SLSser4y6U

While cutting back on big expenses is a great start, the real secret to supercharging your savings is widening the gap between what you earn and what you spend. This isn’t a one-sided battle. It’s about tackling your finances from both ends—bringing in more cash while also becoming a more intentional consumer.

Let’s be real: saving is tough right now. Recent data shows that a staggering 73% of Americans are saving less for emergencies than they used to, mostly thanks to inflation. Even more telling, only 27% actually have enough stashed away to cover three months of essential bills. You can dig into more of these emergency savings statistics and what they mean on Bankrate.com. This highlights just how critical it is to have a solid game plan.

Smart Ways to Increase Your Monthly Income

Boosting your income doesn’t have to mean grinding away at a draining second job. Thanks to the gig economy, there are plenty of flexible ways to earn more on your own schedule.

- Monetize Your 9-to-5 Skills: Are you a writer, designer, or just really organized? Platforms like Upwork or Fiverr are full of projects you can tackle in the evenings or on weekends, using the skills you already have.

- Tap into the Gig Economy: If you’ve got a few spare hours, you can turn that time into cash with services like DoorDash, Instacart, or TaskRabbit. The trick is finding something that fits your life without leading to burnout.

Even an extra few hundred dollars a month can make a huge difference and seriously fast-track your savings goals.

Adopting Mindful Spending Habits

The other half of the equation is your spending. Shifting from a rigid, restrictive budget to a mindset of mindful spending can be a game-changer. This isn’t about depriving yourself; it’s about being intentional.

Before I make any non-essential purchase, I use the “24-hour rule.” I force myself to wait a full day before clicking “buy.” You’d be surprised how often that initial urge just disappears, saving me from impulse buys and buyer’s remorse.

Another powerful move is the subscription audit. Seriously, pull up your bank and credit card statements and track down every single recurring charge. I guarantee you’ll find at least one or two services you completely forgot you were paying for. Canceling them is an instant pay raise.

Mindful spending isn’t about saying “no” to everything you enjoy. It’s about asking “why” before you buy, making sure your spending truly aligns with your values and long-term goals.

When you pair earning a little more with spending a lot smarter, you create some powerful momentum. You’re not just cutting back; you’re actively building a stronger financial foundation that puts you in control.

Your Questions on Saving Money Answered

Even with the best strategies, life has a funny way of throwing curveballs. This is where theory meets reality. Sticking to a plan is one thing, but knowing how to adapt when things don’t go perfectly is what builds true financial resilience.

Let’s tackle some of the most common questions that pop up on the road to building serious savings.

How Much Money Should I Realistically Save Each Month?

You’ve probably heard of guidelines like the 50/30/20 rule, which suggests socking away 20% of your income. For most people just starting out, that number feels less like a goal and more like a mountain.

The best amount to save is the one you can actually stick with, even if it’s just 5% of your income to begin with. Consistency will always beat intensity. Getting into the habit of saving is the first and most important win.

The goal is progress, not perfection. Starting with a smaller, doable percentage and slowly increasing it is a sustainable path to success. A small, consistent habit will always outperform a big, abandoned goal.

Once you make saving automatic, you can look for chances to nudge that percentage higher over time.

What’s the First Thing to Do with Zero Savings?

If you’re starting from scratch, your immediate priority isn’t building wealth—it’s building a financial buffer. You need a small safety net that can absorb minor financial shocks without sending you into debt.

Your first objective: a starter emergency fund of $500 to $1,000. This small cushion is what stands between an unexpected car repair and another high-interest credit card bill.

To get the ball rolling, automate a small transfer—even just $25 per paycheck—into a separate high-yield savings account. The amount is less important than the act of starting. You’re building momentum, one small deposit at a time.

I Feel Like I’ve Cut Everything Possible. What Now?

It’s a common and incredibly frustrating place to be: you’ve trimmed every possible expense from your budget but still aren’t seeing the progress you want. When you’ve squeezed every last drop from your spending, it’s time to stop playing defense and start playing offense.

This means shifting your energy from cutting expenses to growing your income.

- Negotiate a Raise: Do your homework. Research your market value, document your wins, and build a rock-solid case for a pay increase at your current job.

- Develop New Skills: Look at what’s in demand in your field. Acquiring the right skills can open the door to a higher-paying role or a promotion right where you are.

- Start a Practical Side Hustle: Turn a skill you already have into a second stream of income. Think freelance writing, graphic design, tutoring, or even something hands-on like furniture flipping.

When you can no longer shrink your expenses, the only way forward is to expand your income. This two-pronged attack—controlling spending while boosting earnings—is how you create the real gap needed to accelerate your savings.

Ready to see your entire financial picture in one place? PopaDex helps you track your net worth, monitor investments, and set clear goals to accelerate your savings journey. Take control of your finances today.