Our Marketing Team at PopaDex

How to Start Investing Money: Easy Steps for Beginners

To start investing, the formula is surprisingly simple: build a solid financial foundation, pick an investment account that fits your goals (like a Roth IRA), and then consistently buy diversified, low-cost investments. You don’t need a fortune to get started. The real magic is starting early and letting your money do the heavy lifting for you over time.

Why Investing Is Simpler Than You Think

Let’s be real, the word “investing” can sound intimidating. It probably conjures up images of Wall Street chaos and confusing stock tickers. But what if I told you the biggest secret to building wealth isn’t about perfectly timing the market, but simply about time in the market?

The truth is, investing today is more accessible than it’s ever been. It’s built for regular people, not just financial wizards.

This guide is here to cut through the noise. We’re going to show you that learning how to start investing is a skill anyone can pick up. Forget the old stereotypes. Just think of investing as a practical tool to reach your goals—whether that’s a comfortable retirement, a down payment on a house, or just a little more financial breathing room.

The Real Power of Starting Early

The most powerful engine in your investing journey is compound growth. Think of it as a snowball effect for your money. Your earnings start making their own earnings, and the whole thing gets bigger and bigger as it rolls downhill. The earlier you start, the more time that snowball has to grow.

Here’s a real-world example that brings it to life:

- Friend A starts at 25: She invests $200 every single month.

- Friend B starts at 35: He realizes he’s behind and invests $300 every month to catch up.

Assuming they both get an average 8% annual return and stop at age 65, who do you think has more money? It’s Friend A. By a long shot. The early starter ends up with over $700,000. Friend B, despite investing more money each month, only winds up with around $440,000. That huge gap is purely because of ten extra years of compounding.

The takeaway is crystal clear: How much you start with matters far less than when you start. Consistency is the true engine of wealth.

Your Roadmap to Getting Started

This guide is your step-by-step roadmap, designed to take you from initial planning to making your first investment with total confidence. We’ll show you that effective investing really boils down to two things: understanding the power of compounding and being patient. For context, historical data shows the S&P 500 has delivered an average annual return of about 10% since 1926. An investment of just $1,000 at age 25 growing at that rate could become over $17,400 by age 65. That same amount invested at 35 would only reach about $6,700. For a deeper dive, check out these global private market insights on McKinsey.com.

Here’s what you’ll learn:

- Building Your Financial Base: Before you invest a dime, you need a solid foundation. We’ll cover simple budgeting, setting up an emergency fund, and knocking out high-interest debt.

- Choosing the Right Accounts: We’ll demystify 401(k)s, Roth IRAs, and brokerage accounts so you can pick the perfect one for your goals.

- Selecting Your First Investments: You’ll learn a stress-free strategy using diversified, low-cost funds. No stock-picking skills required.

- Automating Your Growth: Discover how to put your investing on autopilot so you can build wealth without even thinking about it.

By the end, you’ll have the practical know-how to get started and feel good about it.

Building a Bulletproof Financial Foundation First

Jumping headfirst into the stock market without a solid financial base is like building a house on sand. Sure, it might look good for a little while, but the first storm that rolls in could bring the whole thing crashing down. Before you even think about investing a single dollar, you’ve got to build a foundation that can handle life’s inevitable surprises.

Jumping headfirst into the stock market without a solid financial base is like building a house on sand. Sure, it might look good for a little while, but the first storm that rolls in could bring the whole thing crashing down. Before you even think about investing a single dollar, you’ve got to build a foundation that can handle life’s inevitable surprises.

This isn’t about putting off your wealth-building goals; it’s about making them last. When you get your financial house in order first, you can invest with confidence and won’t be forced to sell your assets at the worst possible moment.

Know Where Your Money Is Going

First things first: you need to figure out exactly how much you can comfortably invest. This isn’t about scrounging for whatever cash is left over at the end of the month. It’s about creating a deliberate plan.

Start by tracking your income and expenses for one full month. A simple spreadsheet works, or you can use a budgeting app. This little exercise is often an eye-opener, revealing spending habits you never knew you had and showing you exactly where you can free up cash for your investment goals. You might be surprised how a few small tweaks can create a hefty amount to invest each month.

Key Takeaway: Budgeting isn’t about restriction; it’s about awareness. It puts you in the driver’s seat and shows you the real potential you have to start investing, even on a modest income.

Build Your Financial Safety Net

Picture this: your car breaks down, and the repair bill is $1,500. If you don’t have savings, that money might have to come from your investments, forcing you to sell at a loss. This is exactly why an emergency fund is completely non-negotiable.

Your target should be to save 3 to 6 months’ worth of essential living expenses in a high-yield savings account. This isn’t your investment money; it’s your financial shock absorber.

- What are essential expenses? Think rent or mortgage, utilities, groceries, transportation, and insurance.

- Keep it separate. This cash needs to be easy to get to, but it should be in an account separate from your daily checking to avoid the temptation of spending it.

- Start small. If saving 3-6 months feels like a mountain to climb, aim for $1,000 first. Even that small buffer makes a world of difference.

Once this safety net is in place, you can invest with the peace of mind that a surprise bill won’t derail your entire long-term strategy.

Tackle High-Interest Debt First

Not all debt is created equal. A low-interest mortgage is a completely different beast than high-interest credit card debt. Trying to out-earn a credit card’s 20%+ APR with stock market returns is an uphill battle—and an incredibly risky one.

Think of it this way: paying off high-interest debt is like getting a guaranteed investment return. When you pay off a credit card with a 22% interest rate, you’ve essentially “earned” a 22% return on your money, completely risk-free. You just can’t find that kind of guarantee anywhere else.

Here’s a practical game plan:

- Prioritize. Make a list of all your debts and their interest rates. Focus all your extra firepower on paying down anything with an interest rate above 7-8%.

- Try the hybrid strategy. While you’re aggressively tackling that high-interest debt, you can still start investing small. For example, make sure you contribute enough to your 401(k) to get the full employer match. That’s free money you should never pass up.

- Handle low-interest debt differently. For debts with lower rates (like most federal student loans or your mortgage), it often makes more sense to just pay the minimum. Why? Because historical market returns have typically been higher than those interest rates, meaning your money can work harder for you by being invested.

Laying this groundwork is a crucial part of your journey. For a deeper dive, our guide on financial planning for beginners is an excellent next step in building a comprehensive plan. With these pillars firmly in place, you’re finally ready to start investing.

Choosing the Right Investment Account for Your Life

Think of an investment account not just as a place to put your money, but as a specific tool designed for a specific job. Picking the right one from the get-go is one of the most important moves you can make, potentially saving you thousands in taxes over your lifetime.

The big question is: what’s the money for? Is it for retirement decades down the road, or for a down payment on a house in five years? Your answer is the key that unlocks which account is perfect for you.

The Big Three Account Types

For most people starting out, the universe of investment accounts really boils down to three main categories. Each one has its own set of rules and tax perks, so the trick is matching the right tool to your goal.

-

Workplace Retirement Plans (like a 401(k) or 403(b)): If your job offers one, this is almost always the best place to start. Your contributions are usually pre-tax, which lowers your taxable income right now. Plus, many companies offer an employer match—that’s literally free money.

-

Individual Retirement Arrangements (IRAs): These are accounts you open yourself. They come in two main flavors, Traditional and Roth, and both are packed with tax advantages to help you save for the long haul.

-

Taxable Brokerage Accounts: This is your flexible, all-purpose investment account. There are no contribution limits or weird withdrawal rules, but you also don’t get the special tax breaks that come with retirement accounts.

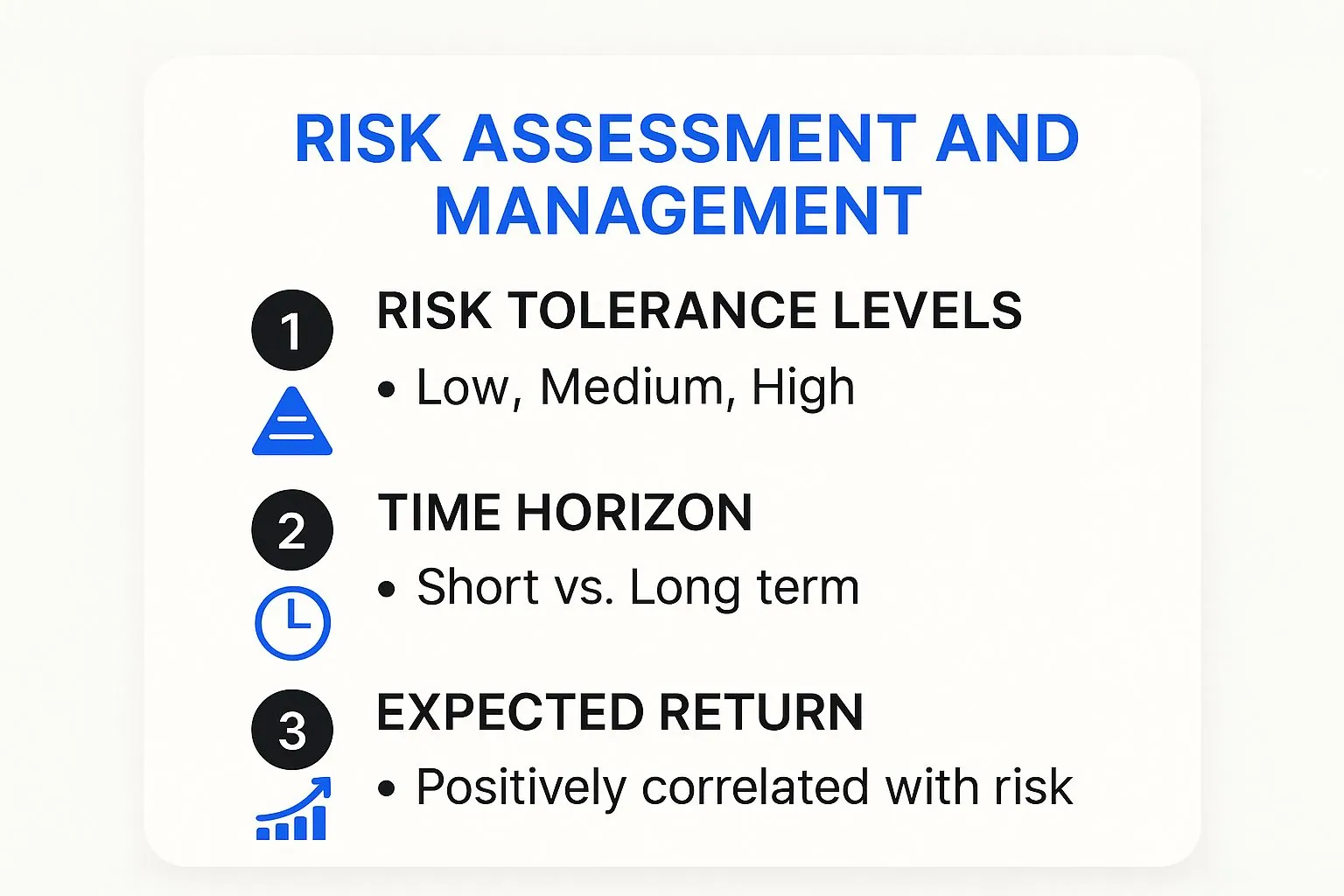

This visual helps break down the relationship between risk, time, and potential returns—a concept that applies no matter which account you choose.

As the infographic shows, having more time on your side means you can comfortably take on a bit more risk for a shot at higher returns. That’s the core principle of retirement investing.

Retirement vs. General Investing

The first major decision you’ll face is whether you need a dedicated retirement account or a standard brokerage account. Retirement accounts are built for the long game, offering huge tax advantages as a reward for leaving the money alone until you’re older.

A Roth IRA, for example, is a fantastic choice for younger investors. You put in after-tax money, but then it grows completely tax-free, and you won’t pay a dime in taxes on qualified withdrawals when you retire. A Traditional IRA is the opposite: you get a tax deduction on what you contribute today, but you’ll pay income tax on the money you take out in retirement.

The Roth vs. Traditional debate usually comes down to one question: Will your tax rate be higher now or in retirement? If you expect to be in a higher bracket later in your career, the Roth IRA is often the smarter play.

For any goal outside of retirement, a taxable brokerage account is your best friend. It’s the ideal spot for medium-term goals, like saving for a wedding, a car, or that house down payment. You have total freedom to pull your money out whenever you need it, but you will owe capital gains taxes on any profits you realize when you sell.

Making the Right Choice for You

Let’s look at a real-world example. Meet Sarah, a 28-year-old professional. Her company offers a 401(k) with a 4% match, and she’s also trying to save up for a down payment on a home in about six years.

Her smartest move is a two-part strategy:

- Max out the 401(k) match: She should contribute at least 4% of her salary to her 401(k). Not doing so is like turning down a raise. It’s free money, plain and simple.

- Open a taxable brokerage account: For her down payment fund, a brokerage account is perfect. Her money can grow faster than in a high-yield savings account, and she can access it in six years without facing any penalties.

To help you figure out the best fit for your own goals, here’s a quick breakdown of how these accounts stack up against each other.

Comparing Common Investment Accounts

| Feature | 401(k) | Roth IRA | Taxable Brokerage Account |

|---|---|---|---|

| Best For | Long-term retirement savings | Tax-free growth in retirement | Medium-term goals (5+ years) |

| Tax Advantage | Pre-tax contributions | Tax-free withdrawals | None on growth |

| Contribution Limit | High (set by IRS annually) | Moderate (set by IRS annually) | Unlimited |

| Employer Match | Often available | Not applicable | Not applicable |

| Withdrawal Rules | Penalties for early withdrawal | Contributions can be withdrawn anytime | No withdrawal restrictions |

Once you get a handle on these key differences, you can confidently pick the right account—or combination of accounts—to align with your financial timeline and bring your goals within reach.

Picking Your First Investments (Without the Guesswork)

Alright, your financial foundation is solid and you’ve picked the right account. Now for the main event: deciding what to actually put in it.

This is the part where a lot of people freeze up, picturing complicated charts and stressful decisions. But learning how to start investing money doesn’t have to be a gamble. The goal isn’t to outsmart the market or chase the “next big thing.” It’s about building a simple, powerful engine for your money that works quietly in the background.

Forget the idea that you need to become a stock-picking genius. That’s a high-stress, full-time job. A simpler, more hands-off approach is almost always more effective for the vast majority of us.

What Are You Actually Buying?

Before you build anything, you need to know your materials. For most investors, the entire universe is built on two core ingredients.

-

Stocks: Think of a stock as a tiny slice of ownership in a company. When you buy a share of Apple or Target, you become a part-owner. If the company thrives, the value of your slice goes up. Simple as that.

-

Bonds: A bond is just a loan. You’re lending money to a government or a big corporation, and they promise to pay you back in full on a set date, with regular interest payments along the way. They’re generally the calmer, more predictable cousin to stocks.

These are the fundamentals. But buying individual stocks and bonds one by one is a huge pain. It takes a ton of research and a lot of cash to get enough variety. This is where funds change the game.

The Magic of Funds: Diversification on Autopilot

Funds are the ultimate shortcut for new investors. They’re basically pre-packaged collections of dozens, hundreds, or even thousands of individual stocks and bonds, all bundled into one thing you can buy.

You’ll mainly run into two types:

- Mutual Funds: Professionally managed pools of money from tons of investors. They get priced just once a day after the market closes.

- Exchange-Traded Funds (ETFs): Very similar to mutual funds, but they trade on a stock exchange just like a regular stock. This means their price moves all day long. ETFs have become incredibly popular because they often have lower fees and are more tax-friendly.

When you buy a single share of an ETF, you instantly own a tiny piece of every company it holds. One click, and you’re diversified. This is how you reduce risk—if one company in the fund has a bad year, its poor performance is balanced out by hundreds of others that are doing just fine.

The Simple “Three-Fund Portfolio”

For most people, the most effective path is to use low-cost index funds. An index fund is a type of ETF or mutual fund that doesn’t try to be clever; it just aims to match the performance of a specific market index, like the S&P 500 (which tracks 500 of the biggest companies in the U.S.). Instead of trying to beat the market, you’re simply trying to be the market.

One of the most popular and time-tested strategies is the “three-fund portfolio.” It’s brilliant in its simplicity, giving you exposure to the entire global economy with just three investments.

Here’s what that looks like in the real world:

| Fund Type | What It Actually Holds | Why It’s In Your Portfolio |

|---|---|---|

| Total U.S. Stock Market Index Fund | A small piece of nearly every public company in the United States. | Taps into the growth potential of the entire U.S. economy. |

| Total International Stock Market Index Fund | Thousands of stocks from developed and emerging markets outside the U.S. | Spreads your risk globally, so all your eggs aren’t in one country’s basket. |

| Total U.S. Bond Market Index Fund | A mix of U.S. government and corporate bonds. | Acts as a stabilizer, helping to cushion your portfolio when the stock market gets bumpy. |

This combination is powerful. You’re diversified across different asset types (stocks and bonds) and different regions (U.S. and the rest of the world). You never have to worry about the latest news from a single company because you own a tiny slice of everything.

While stocks and bonds are the most common starting point, other asset classes exist. If you’re interested in something like real estate, checking out a real deal strategy guide for investing in rental property can give you a solid overview of that world.

Key Takeaway: You can build a globally diversified, low-stress portfolio with as few as three core investments. The name of the game is broad market exposure, not trying to pick individual winners.

With this setup, you can harness the long-term growth of the global economy. As you start building, keeping all the pieces straight is crucial. This is where a good investment portfolio tracker becomes your best friend, giving you a single, clear view of your holdings so you can stay on track.

Making Your First Investment and Putting Your Growth on Autopilot

You’ve done the hard work: you’ve built your financial base, picked an account, and even chosen your first investment. Now comes the part that feels like the biggest hurdle—actually clicking the “buy” button.

It can feel a little nerve-wracking, I get it. But the truth is, the process on most modern brokerage apps is surprisingly simple, almost anticlimactic. The real secret to building wealth isn’t the drama of that first purchase. It’s everything that comes after.

The key is turning investing from a one-off event into a consistent, almost boring, habit. This is where automation becomes your superpower, setting your financial growth on autopilot and letting your money work for you 24/7.

Placing That First Trade

Let’s pull back the curtain on this process. Once your account is funded and you’ve decided on an ETF or index fund, making the trade itself is a piece of cake.

You’ll usually just search for the fund by its ticker symbol (like “VTI” for the Vanguard Total Stock Market ETF), type in the dollar amount you want to invest, and hit confirm. Seriously, it’s often as easy as buying something on Amazon.

And please, don’t get hung up on buying at the “perfect” time. The goal isn’t to time the market—it’s to get your time in the market. Just focus on putting your plan into action.

The Magic of Dollar-Cost Averaging

After you’ve made that first investment, the most powerful strategy you can use is dollar-cost averaging. It sounds technical, but it’s incredibly simple. All it means is investing a fixed amount of money on a regular schedule—say, $100 every two weeks—no matter what the market is doing.

This simple approach comes with two huge benefits:

- It takes emotion off the table. When the market drops, our gut reaction is to panic and sell. When it’s soaring, we get greedy. Automating your buys completely removes those emotional impulses from the equation.

- You naturally buy more when prices are low. Your fixed dollar amount automatically buys more shares when the market dips and fewer shares when prices are high. Over time, this can lower your average cost per share.

Think of it as the ultimate “set it and forget it” strategy. You create a solid plan and then let the system run it for you, month after month, year after year.

Key Insight: Consistency beats timing, every single time. A simple, automated investment plan you actually stick with will almost always outperform a complicated strategy that relies on trying to guess the market’s next move.

Putting It All on Autopilot

Just about every brokerage out there will let you set up automatic, recurring investments. This is the single most effective thing you can do to make sure you stick with your plan.

Schedule a transfer from your bank to your brokerage account for the same day you get paid. It’s that simple.

This small step makes investing a priority, not an afterthought. You’re paying your future self first, before that money can disappear on something else. This discipline is the absolute bedrock of long-term wealth. Of course, as you start investing, you’ll want to know how you’re doing. A great next step is to learn how to calculate your Return on Investment so you can track your progress effectively.

Feeling like you don’t have enough money to start is a common hurdle, but even small, consistent amounts can build incredible wealth. While 55% of American adults invest, many begin with modest sums. Investing just $100 a month for 30 years at a 7% average return can grow to over $93,000—dwarfing the $36,000 you’d have if you just saved it.

This automated approach ties directly back to the financial foundation you built earlier. By creating a plan, you know exactly how much you can afford to invest on a recurring basis. If you need a refresher, check out our complete guide on how to budget your money to find the cash for your automated plan.

Got a Few Lingering Questions?

Even with a solid plan, it’s completely normal to have a few nagging questions buzzing around. Those “what ifs” are often the last little hurdle that keeps people from taking the plunge.

So, let’s tackle these common concerns head-on. Think of this as the final confidence boost you need to get started.

How Much Money Do I Actually Need to Start?

This is probably the biggest myth in investing, so let’s bust it right now: you do not need a fortune to start. Seriously. Thanks to things like fractional shares and brokerages with zero account minimums, you can get in the game with as little as $5 or $10.

The most important thing isn’t how much you start with; it’s the habit you build. Consistently investing $50 a month will do far more for you in the long run than waiting years to save up a huge lump sum. The real goal is to get your money working for you as soon as you can, no matter how small the amount.

The secret is just to begin. Starting early and being consistent—with whatever you can afford—will always beat waiting for the “perfect” time or a “large enough” sum of money.

Is the Stock Market Just a Big Casino?

I get why people think this, especially when all you see on the news are the wild daily swings. But there’s a huge difference between smart investing and just gambling.

Gambling is a short-term bet on a totally random outcome. Investing, on the other hand, is about long-term ownership in real, productive businesses. When you buy a broad market index fund, you’re not just buying a ticker symbol—you’re buying a tiny slice of the entire economy’s growth engine.

Sure, there’s always risk involved, and the market will definitely have its down years. But you manage that risk by:

- Diversifying: Never put all your eggs in one basket. Spreading your money across thousands of companies means no single company’s failure can sink you.

- Thinking Long-Term: When your timeline is five years or more, you have plenty of time to ride out the market’s inevitable bumps and benefit from the overall upward trend of economic growth.

ETFs vs. Mutual Funds: What’s the Real Difference?

Okay, let’s keep this simple. Think of ETFs and mutual funds as two different shopping baskets that both hold a mix of stocks and bonds. They do the same basic job—give you instant diversification—but they trade a little differently.

Here’s the main thing you need to know:

- ETFs (Exchange-Traded Funds) trade just like individual stocks. Their prices bounce around all day long while the market is open.

- Mutual Funds are different. They only get priced once per day, right after the market closes.

For most beginners, ETFs are usually the way to go. They tend to have lower fees, can be more tax-efficient (if you’re using a regular brokerage account), and are incredibly easy to buy and sell on any modern investing platform.

Should I Pay Off All My Debt Before Investing?

Fantastic question. The answer comes down to one thing: the interest rate on your debt. Not all debt is created equal.

If you have high-interest debt, like a credit card with a 20%+ APR, that’s a financial emergency. Paying that off gives you a guaranteed 20%+ return on your money. You’re not going to beat that by investing, so make wiping that out your absolute top priority.

But for low-interest debt—think mortgages or federal student loans that are often under 6-7%—the math changes. It often makes a ton of sense to do both at the same time. You can make your regular debt payments while also investing, because the potential long-term returns from the market are very likely to be higher than the interest you’re paying. This way, your money works harder for you.

Now that you have the knowledge and confidence to start, the next step is keeping your progress in clear view. PopaDex is the perfect tool for this, letting you see all your accounts—from investments and savings to your house—in one simple dashboard. Track your net worth as it grows and make smarter financial decisions with ease. Take control of your financial future by starting your free trial at PopaDex.