Our Marketing Team at PopaDex

The Best Way to Track Finances for Total Control

Let’s be honest—the best way to track finances isn’t about finding a single, magical app that does everything. The real secret is building a hybrid system. You need one automated tool for the daily grind and a simple spreadsheet for your big-picture goals.

Your Starting Point for Financial Clarity

This guide is your roadmap to combining the effortless data-gathering of an app with the intentional focus of a manual planner. We’re going to solve that common frustration of scattered accounts and financial guesswork, giving you a clear view of where your money is actually going.

The goal here is to move beyond just passively watching numbers go up and down. When you have a solid tracking system in place, you can make confident decisions. It doesn’t matter if you’re saving for a down payment, planning for retirement, or just trying to get a handle on your monthly cash flow—clarity is power.

Why a Hybrid System Works Best

When you blend automation with manual oversight, you truly get the best of both worlds. An app can pull in thousands of transactions automatically, saving you hours of painful data entry. It’s no wonder the personal finance app market is projected to hit $412.22 billion by 2029.

But here’s the key: manually updating a simple spreadsheet for your net worth forces you to actually engage with your progress. That intentional check-in keeps you connected to your goals in a way automation can’t. Whether you’re just starting out or refining your process, a core part of financial control is creating a personal budget that works for you.

A successful financial tracking system goes beyond recording the past; it’s about actively shaping your future. It provides the clarity needed to turn goals into reality.

Comparing Financial Tracking Methods

To get started, it helps to understand your options. Each method has its own strengths and weaknesses, and the best choice often depends on your personality and how much detail you want to manage.

Here’s a quick breakdown to help you decide what fits your style:

| Method | Best For | Pros | Cons |

|---|---|---|---|

| Manual Spreadsheets | DIY enthusiasts who want total control and customization. | Highly flexible, no cost, forces you to engage with your numbers. | Time-consuming, prone to human error, no real-time updates. |

| Automated Apps | Busy individuals who want a hands-off, real-time overview. | Saves time, automatically categorizes spending, provides alerts. | Can have subscription fees, potential privacy concerns, may miscategorize transactions. |

| Hybrid System | The goal-oriented person who wants both automation and intentional review. | Best of both worlds: automated data plus manual focus on goals. | Requires managing two systems, initial setup takes a bit more effort. |

As you can see, the hybrid approach we recommend leverages the strengths of both automated apps and manual spreadsheets while minimizing their individual drawbacks. This balanced method gives you comprehensive data without sacrificing personal engagement.

Choosing Your Financial Tracking Toolkit

The right tools can make or break your financial tracking habits, but let’s be clear: the “best” option is deeply personal. It’s less about finding a perfect, magical app and more about choosing a system you’ll actually stick with. The best way to track your finances is the one that fits your personality and goals, not someone else’s.

It all boils down to a trade-off between control and convenience. Do you want granular, hands-on management, or would you rather have automated, real-time updates without lifting a finger?

A freelancer with a fluctuating income might get a ton of value from a detailed budgeting app like YNAB, where you assign every single dollar a job. On the other hand, someone focused on long-term investing might just need an all-in-one dashboard like Empower paired with a simple spreadsheet for the big picture.

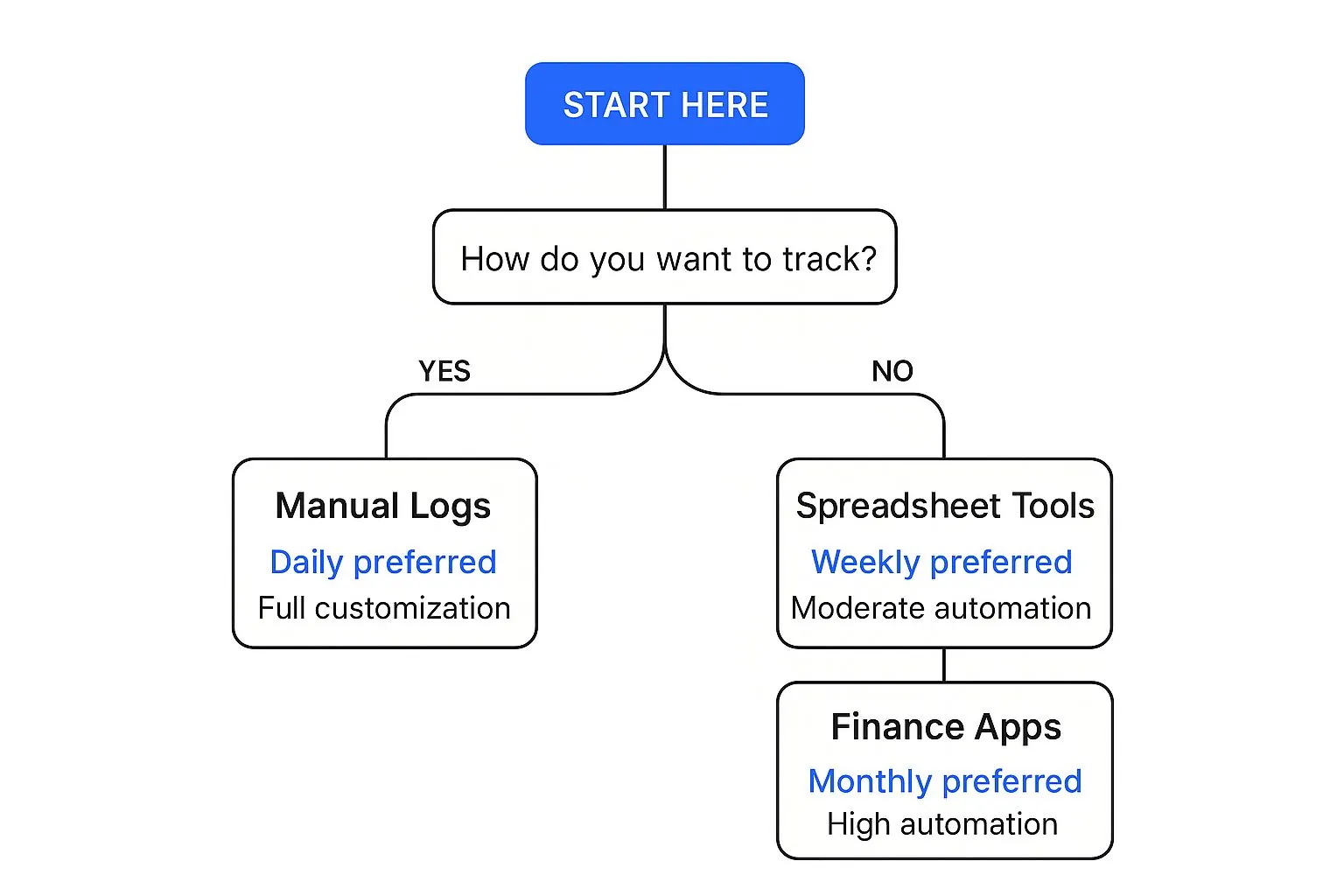

This decision tree can help you figure out which path makes the most sense for you, based on how much effort you’re willing to put in and how often you want to check in.

As the infographic shows, it’s a pretty clear path. The more automation you crave, the more you’ll lean towards dedicated apps. They require a bit more setup upfront but save you a ton of time in the long run.

Finding Your Perfect Match

To land on a system you won’t ditch after a month, ask yourself a few honest questions:

- What’s Your Main Goal? Are you trying to aggressively crush debt, or is your focus on growing your investments? Slashing debt often demands detailed expense tracking, while investment growth is better served by a high-level overview.

- How Much Time Can You Commit? Be realistic. If you only have 15 minutes a week, a highly automated app is your best friend. But if you actually enjoy digging into the numbers, a spreadsheet offers endless customization possibilities.

- What’s Your Budget? Many of the most powerful apps come with a subscription fee. While a free spreadsheet is tempting, the time-saving features of a paid tool—like automatic transaction syncing and categorization—can be well worth the small investment.

The ultimate aim here is to create a single source of truth for your entire financial life. Whether it’s an app, a spreadsheet, or some combination, it must give you a clear and immediate answer to the question, “How am I doing?”

No matter which tool you pick, its core job is to pull all your data together effectively. For a deeper dive into consolidating everything you own and owe, check out our complete guide on using a powerful net worth tracker. It’ll help you build that essential big-picture view from day one.

Building Your Central Financial Dashboard

Alright, you’ve picked your tools. Now it’s time to build your financial command center. The goal here is to create a single source of truth that kills the mental clutter of logging into a dozen different apps and websites. This is how you finally get that complete, real-time picture of your money.

If you went with an automated app, the initial setup is all about securely connecting your various accounts. This means linking everything: checking and savings, credit cards, investment portfolios, and even your loans. Don’t rush this part. Accurate connections are the bedrock of reliable tracking.

Setting Up for Success

Most modern financial apps use bank-level security to protect your data, but it’s still on you to lock things down. First things first: enable multi-factor authentication (MFA) immediately. It’s a simple step, but it’s an incredibly powerful shield against anyone trying to snoop around your accounts.

Once your accounts are linked, spend a few minutes customizing your dashboard. Here’s a pro tip I swear by: set up custom transaction rules from day one. For instance, create a rule that automatically tags any payment to “Spotify” or “Netflix” under a “Subscriptions” category. Doing this upfront keeps your data clean and your spending categories accurate without you having to manually fix things later.

Your dashboard’s real job is to turn raw data into clear answers. It should instantly tell you where you stand, so you can spend less time hunting for information and more time making smart decisions with it.

For those of you using a spreadsheet or a hybrid approach, building your dashboard is a more hands-on—but highly rewarding—process. The aim is to create a high-level overview of your most important numbers. To get a running start, you can check out our detailed guide on creating a comprehensive net worth dashboard.

At a minimum, an effective spreadsheet needs to track these key areas:

- Assets: List everything you own that holds value—cash, investments, property, the works.

- Liabilities: Detail everything you owe, from credit card balances and student loans to your mortgage.

- Net Worth: This is the simple but powerful calculation of Assets - Liabilities. Make a point to update it every single month to see your progress.

This manual update forces a monthly check-in, keeping you connected to your bigger financial picture in a way that pure automation sometimes can’t. It’s a crucial habit for anyone serious about tracking their finances for long-term growth.

Turning Tracking Data into Smart Decisions

Collecting all your financial data is just step one. The real magic happens when you start turning those numbers into action. This is where you move from just tracking your money to actually controlling it. You’ll start to uncover hidden spending patterns—those little “money leaks” you never even knew were there.

For instance, after a month, you might glance at your spending and see the “Miscellaneous” category is way bigger than you expected. When you dig in, you find it’s not one big purchase, but a hundred small ones: daily coffees, random online buys, and a few subscriptions you forgot you were even paying for. This isn’t about making you feel guilty; it’s about awareness. Suddenly, you see exactly where your money is going.

From Insights to Action

Once you spot a pattern, you can make a change. Let’s say you realize you’re spending $50 a month on streaming services you barely use. That’s a clear, actionable insight. You can cancel them, and voilà—you’ve just freed up cash.

That newfound money can immediately be put to work. You could redirect it to a high-yield savings account or throw it at that nagging high-interest credit card balance.

The goal here is to reframe how you see financial tracking. It stops being a restrictive chore and becomes an empowering tool. Seeing the numbers clearly actually reduces anxiety because it puts you back in the driver’s seat.

This process becomes even more vital when the economy gets shaky. With ongoing inflation, understanding your cash flow is non-negotiable. In 2025, even with wages rising an average of 3.6%, inflation sitting at 2.7% squeezed a lot of household budgets. It’s that tight gap that makes every dollar count. You can see a great breakdown of how these trends affect personal finance in this insightful report from Stacker.

Advanced Financial Strategies

Once you get comfortable with basic tracking, you can start using your data for more sophisticated planning. It’s no longer just about budgeting; it’s about looking ahead. For a structured way to project future outcomes based on your current data, our guide on scenario forecasting and financial planning is a great next step.

With a solid financial dashboard in place, you can even begin to implement more advanced financial methods. For example, if your investments or income involve multiple currencies, your data becomes the foundation for exploring strategies for managing foreign exchange risk. Every smart financial move you make starts with having clear, accurate numbers to work with.

Establishing a Sustainable Review Rhythm

Let’s be honest: consistency is what separates a fleeting financial whim from a powerful, wealth-building habit. Forget about those intense, hour-long spreadsheet sessions you’ll ditch by February. The real key is building a simple rhythm that fits into your life, not one that hijacks it.

Let’s be honest: consistency is what separates a fleeting financial whim from a powerful, wealth-building habit. Forget about those intense, hour-long spreadsheet sessions you’ll ditch by February. The real key is building a simple rhythm that fits into your life, not one that hijacks it.

The goal isn’t to spend more time staring at numbers. It’s about creating a few low-effort touchpoints that keep you connected to your money without leading to burnout. Think of it as a flexible system that adapts as your life and finances evolve.

Designing Your Review Cadence

I’ve found the best approach is to think in three distinct tiers. Each one has a clear purpose and a time commitment that feels completely manageable, ensuring you cover everything from the day-to-day details to the big-picture strategy.

- The Weekly Sync (10 Minutes) This is your quickest check-in. Just open your tracking app, categorize any new transactions, and give your accounts a quick once-over. The goal is simple: keep your data clean so it doesn’t become a bigger job later.

- The Monthly Review (30 Minutes) Time for a slightly deeper dive. Look at your overall spending for the past month. Did you hit your savings target? Awesome, celebrate that win! If not, see where you can adjust your budget for the month ahead.

- The Quarterly Check-up (1 Hour) This is your strategic session. Block out an hour to update your net worth, check your progress toward big goals like retirement or a down payment, and tweak your investment strategy if needed.

Your financial review shouldn’t feel like a chore. It’s a scheduled moment of empowerment where you confirm you are in control and moving in the right direction.

This layered system is designed to prevent overwhelm. The quick weekly sync stops the small tasks from piling up into a monster project. Meanwhile, the monthly and quarterly reviews give you the dedicated space you need to think strategically and make intentional moves with your money.

Common Questions About Tracking Your Finances

Getting started with tracking your finances always brings up a few practical questions that most guides gloss over. Let’s tackle some of the most common hurdles you might run into, so you can keep your momentum going without getting stuck.

One of the first things people ask is, “What about cash?” It’s simpler than you think. If you’re using an automated app, just log a manual transaction for any cash you spend. Pay $20 for lunch? Pop it into your “Food & Dining” category. This way, your digital records stay complete and accurate.

Another common fear is falling behind. Life happens, and you might miss categorizing a week’s worth of transactions. Don’t let a small slip-up derail everything. The key is to avoid getting overwhelmed. Just focus on getting the current week up to date, and then circle back to the missed period when you have an extra 15 minutes. It’s all about progress, not perfection.

Is It Safe to Link My Bank Accounts?

This is a big one, and it’s smart to be cautious. Reputable financial apps don’t mess around with security. They use bank-level measures like AES-256 encryption to protect your data, both when it’s stored and when it’s zipping across the internet. Many also use third-party services that tokenize your login details, which means the app itself never even stores your actual bank username or password.

To make sure you’re protected:

- Always use multi-factor authentication (MFA). This is your single best defense against anyone trying to get into your account.

- Review app permissions. Take a quick look at what data the app is accessing and why.

- Stick with well-known, trusted apps. Go for established players with a solid security track record.

The reality is, a major barrier to getting on top of your money is often a lack of confidence in the tools and concepts themselves. Making smart financial decisions starts with understanding the basics.

This confidence gap is surprisingly widespread. A recent study found that U.S. adults could only answer 49% of financial literacy questions correctly, a number that hasn’t budged in years. This just goes to show why feeling comfortable with your tools is so crucial for long-term success. You can dig into these personal finance findings to see just how much knowledge impacts how we manage our money.

Ready to build a complete picture of your financial life with a tool you can trust? PopaDex gives you a secure, all-in-one dashboard to track your net worth, investments, and daily spending with ease. Start your free trial today at https://popadex.com.