Our Marketing Team at PopaDex

Managing Money Better A Practical Guide to Financial Freedom

If you want to get better with money, the first step is surprisingly simple: find out where it’s actually going. This isn’t about making yourself feel guilty or creating a restrictive budget right away. It’s about gaining total awareness of your spending habits. This one act lays the foundation for every other smart money move you’ll make.

First, Understand Where Your Money Is Going

Before you can even think about building wealth or crushing debt, you need an honest look at your cash flow. Think of it as a one-month “money audit” to see the real story behind your bank statements. Forget complex spreadsheets for now; this is purely about discovery.

This is a bigger deal than most people think. A recent study from the TIAA Institute–GFLEC found that U.S. adults, on average, could only answer 49% of basic personal‑finance questions correctly. That knowledge gap makes it incredibly hard to manage money effectively. Starting with your own spending is the fastest way to bridge that gap.

The Power of Categorization

The real magic happens when you start grouping your transactions. Listing every purchase is one thing, but categorizing them reveals patterns you never knew existed. You might be shocked to see how much those daily coffees or multiple streaming subscriptions are really costing you over 30 days.

Start with a few simple buckets:

- Fixed Expenses: Things like your rent/mortgage, insurance, and car payments that rarely change.

- Variable Necessities: Groceries, gas for the car, and utility bills that fluctuate each month.

- Discretionary Spending: The fun stuff—dining out, entertainment, shopping, and hobbies.

- Financial Goals: Any money you’re putting toward savings or paying down debt.

To help you get started, here’s a simple table you can use to capture your first 30 days of spending. It’s designed to give you a quick, high-level view of your finances.

Your First 30-Day Financial Snapshot

This template helps you categorize your spending for one month to easily spot where you might be overspending and find opportunities to save.

| Expense Category | Budgeted Amount ($) | Actual Spent ($) | Area for Review |

|---|---|---|---|

| Housing | 1,500 | 1,500 | Fixed |

| Utilities | 150 | 175 | Higher than expected |

| Groceries | 400 | 520 | Review impulse buys |

| Transportation | 200 | 250 | More ride-sharing? |

| Dining Out | 250 | 450 | Major savings opportunity |

| Subscriptions | 50 | 50 | Review what’s needed |

| Personal Care | 75 | 110 | Check spending here |

| Savings | 300 | 200 | Goal not met |

After filling this out, you’ll have a clear, data-driven picture of your financial life. No more guessing games.

This audit is about empowerment, not shame. Once you see the data, you can make intentional choices that align your spending with what you truly value. You get to create a plan that works for you, not against you.

This whole process gives you the raw data needed for every other financial strategy. If you’re looking for a simple system to get going, our guide on how to track expenses breaks it down step-by-step. This initial snapshot is your most powerful tool because it replaces guesswork with cold, hard facts—setting you up for success from day one.

Create a Spending Plan That Works for You

Let’s be honest: traditional budgets often fail. They feel rigid, restrictive, and frankly, a bit punishing. The real secret to managing money better is ditching the strict budget and adopting a flexible “spending plan.”

This isn’t about cutting out every little thing that brings you joy. It’s about being intentional. The goal is to give every single dollar a job—whether it’s covering your rent, funding a weekend getaway, or building up your savings. When you consciously direct your cash flow, your budget stops feeling like a cage and starts feeling like a tool for freedom.

Finding a Framework That Fits

A great place to start is the 50/30/20 rule. It’s a simple, straightforward framework for divvying up your after-tax income. Think of it as a solid baseline, not a set of unbreakable laws. The real magic happens when you tweak it to fit your life.

Here’s the basic breakdown:

- 50% for Needs: This bucket covers your absolute essentials. We’re talking about housing, utilities, groceries, and getting to work.

- 30% for Wants: Here’s where the fun stuff lives. This is your discretionary cash for dining out, hobbies, streaming subscriptions, and anything that isn’t a must-have.

- 20% for Savings & Debt Repayment: This portion is for your future self. It’s dedicated to building an emergency fund, investing for retirement, and knocking out high-interest debt.

A freelancer with a fluctuating income might decide to crank up their savings to 40% during a great month to build a buffer. Someone with a steady paycheck and a new mortgage might find their “Needs” are closer to 60% for a while. That’s okay. The key is to be flexible.

For a deeper look at different methods, our guide on how to budget money breaks down several other approaches you can adapt.

Your spending plan should be a mirror of your priorities, not someone else’s. If seeing the world is what you live for, you might slash your spending on new gadgets and eating out to fund your next big trip. It’s all about making intentional trade-offs.

Make Your Plan Actionable

Once you’ve settled on your target percentages, it’s time to translate them into actual dollar amounts based on your monthly income.

If you run the numbers and find your “Needs” are eating up more than 50% of your take-home pay, that’s not a failure—it’s a signal. It’s a clear sign to start looking for ways to trim your core expenses or brainstorm some new income streams.

Remember, this plan isn’t carved in stone. Life changes, and so should your plan. Revisit it every month or quarter to make sure it still makes sense for your goals and circumstances. A successful spending plan grows with you, giving you a clear path to financial control without making you feel deprived.

Build Your Financial Safety Net

Once you have a handle on your spending, it’s time to build a buffer for when life throws you a curveball. And it always does. A surprise car repair, an unexpected medical bill, or a sudden job loss can completely derail your financial progress if you’re not ready for it.

This is exactly why you need an emergency fund. Think of it as your personal financial safety net.

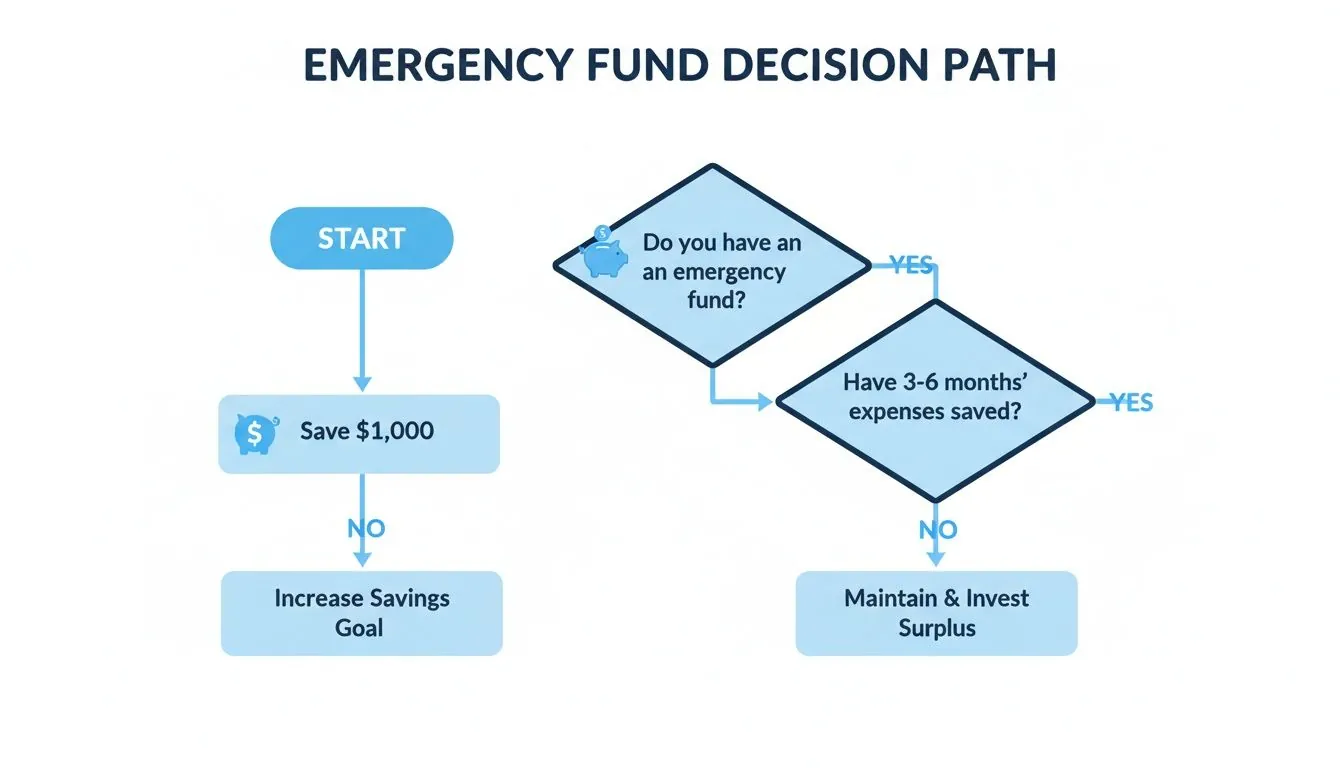

The classic rule of thumb is to save three to six months’ worth of living expenses. That number can feel massive and discouraging when you’re starting out, so let’s ignore it for now. Your first mission is much simpler: save $1,000. This starter fund is surprisingly powerful. It can turn a potential crisis into a manageable inconvenience, keeping you from swiping a credit card and digging yourself into debt.

Where to Keep and Grow Your Emergency Fund

Where you stash this cash is almost as important as having it. You need it to be accessible in a pinch, but not so easy to grab that you’ll dip into it for a late-night pizza craving.

A high-yield savings account is the perfect home for your safety net. It’s separate from your everyday checking account, which creates a helpful mental barrier. Plus, it actually earns a decent interest rate, unlike most traditional savings accounts.

Don’t underestimate how critical this step is. Recent data shows that even as bank balances have grown, true financial security hasn’t kept pace. In fact, a staggering 55% of Gen Z and 49% of Millennials don’t have enough saved to cover three months of expenses. You can dig into the numbers in the latest research on household financial health.

An emergency fund isn’t an investment; it’s insurance. Its job isn’t to make you rich. Its job is to protect the wealth you are building by keeping you out of debt when the unexpected happens.

After you hit that first $1,000 milestone, keep the momentum going. Continue contributing until you eventually reach that full three-to-six-month goal. For a more detailed game plan, check out our guide on how to build an emergency fund for some practical strategies.

Building this safety net isn’t just a box to check—it’s about buying yourself genuine peace of mind. It’s one of the most important pillars of sound financial management.

Develop a Smart Debt Repayment Strategy

If debt feels like an anchor holding you back, you’re not alone. But getting out from under it requires more than just making the minimum payments each month—it takes a focused, intentional plan.

Fortunately, there are two tried-and-true methods that have helped millions of people get control of their finances: the Debt Snowball and the Debt Avalanche. The best one for you really just depends on what makes you tick.

The Two Main Paths to Debt Freedom

The Debt Snowball method is all about psychology and momentum. With this approach, you ignore the interest rates and focus on paying off your smallest debts first. Once that tiny credit card balance is gone, you take the money you were paying on it and roll it over to the next-smallest debt.

Those quick wins can be incredibly motivating. Seeing balances disappear one by one builds a powerful sense of accomplishment that keeps you in the fight.

On the other hand, the Debt Avalanche is pure math. Here, you target the debt with the highest interest rate first, regardless of the balance. While it might take a bit longer to knock out that first account, this strategy saves you the most money in interest over the long haul. It’s the perfect fit if you’re driven by numbers and long-term efficiency.

Debt Snowball vs Debt Avalanche: Which Is Right for You?

So, how do you choose? It really comes down to a simple question: what motivates you more? Is it the thrill of quick victories or the satisfaction of knowing you’re making the most mathematically optimal choice? Both roads lead to the same destination—debt freedom—but the journey is different.

This table breaks down the core differences to help you decide.

| Feature | Debt Snowball Method | Debt Avalanche Method |

|---|---|---|

| Primary Focus | Behavioral and psychological wins | Mathematical efficiency |

| Strategy | Pay off debts from smallest balance to largest | Pay off debts from highest interest rate to lowest |

| Key Advantage | Builds momentum and motivation with quick, early wins | Saves the most money on interest over the life of the loans |

| Best For | People who need to see progress to stay motivated | Highly disciplined people focused on long-term savings |

| Potential Downside | May cost more in total interest over time | Can feel slow at the start, potentially leading to burnout |

| Psychological Impact | Creates a strong feeling of accomplishment and progress | Requires patience and a focus on the big-picture numbers |

Ultimately, there’s no “wrong” answer here. The best strategy is the one you can actually stick with until every last debt is paid off.

Before you go all-in on paying down debt, though, make sure you have a small emergency fund in place. Having at least $1,000 saved gives you a buffer against unexpected costs so you don’t have to reach for a credit card and undo all your hard work.

This flowchart illustrates it perfectly: a starter emergency fund is your first line of defense, a non-negotiable step before you aggressively attack your bigger financial goals.

Whichever strategy you choose, the key is consistency. Making extra payments—no matter how small—is what accelerates your journey out of debt and toward financial freedom.

If you’re juggling multiple high-interest debts, it might also be worth understanding debt consolidation. This can sometimes simplify your payments and even lower your overall interest rate, making it easier to stick to your plan.

By picking a strategy and committing to it, you take back control. You turn your debt from a source of stress into a measurable milestone on your path to building real wealth.

Automate Your Finances to Build Wealth

Let’s be honest: the best way to make consistent progress with your money is to take yourself out of the equation. Willpower is unreliable. A solid system that automatically moves your money where it needs to go? That’s the real secret to building wealth.

This whole process is often called “paying yourself first,” and it’s a game-changer. You just set up automatic transfers from your checking account into your savings and investment accounts. The trick is to have these transfers happen the very same day you get paid. That way, the money for your future is already put to work before you even notice it’s there.

Put Your Progress on Autopilot

Modern banking tools make this ridiculously easy. Think about it—the number of digital transactions per adult has jumped from 55 to 251 in just a few years. That massive shift shows just how central these tools have become. You can dig into the data yourself in the IMF’s latest Financial Access Survey.

Here are a few simple ways you can set this up today:

- Set Up Recurring Savings Transfers: Log into your bank’s website right now and schedule a transfer to your high-yield savings account for every payday. Even if you start with just $50 per check, you’re building a powerful habit.

- Automate Investment Contributions: If you have a 401(k) at work or a personal IRA, make sure your contributions are happening automatically. This is how you build serious long-term wealth through dollar-cost averaging without ever having to think about it.

- Use Roundup Apps: Services like Acorns or Chime can round up your everyday purchases to the nearest dollar and invest that spare change for you. It’s a completely passive way to invest without feeling any pinch in your budget.

Automation is the ultimate antidote to decision fatigue. Instead of wrestling with the choice to save or spend every time you get paid, the system just makes the right decision for you. Every. Single. Time.

This simple shift removes the emotion from saving and investing, turning your financial goals into a boring, background process. And that’s exactly what you want.

While you’re at it, set up automatic bill payments for your rent, utilities, and loans. You’ll sidestep costly late fees and keep your credit score in great shape.

Of course, automation is just one piece of the puzzle. Another cornerstone of building lasting wealth is being smart about taxes. It’s worth exploring some smart tax planning strategies for individuals to see how you can keep more of your hard-earned money. When you combine these automated systems, you’re not just saving money—you’re creating a powerful, hands-off engine for financial growth.

Common Questions About Getting Your Money Right

Jumping into the world of personal finance always kicks up a few questions. As you start trying to manage your money better, it’s totally normal to want some straight answers. Here are a few of the most common ones I hear, along with some practical advice to get you started.

How Long Does It Take to Get Good at This?

There’s no magic finish line here—managing money is really about building habits that stick. Most people start to feel a real sense of control and see actual progress within about three months of consistently tracking where their money goes and following a basic spending plan.

The goal isn’t to be perfect overnight; it’s all about consistency. After six to twelve months, you’ll find that these new habits start to feel like second nature. Making smart financial choices becomes much more intuitive and a lot less like a chore.

What’s the Single Most Important First Step?

If you do only one thing, do this: track your expenses without judging yourself. You can’t manage what you don’t measure, period.

Just give it one full month. Simply observe where your money is going. This one act gives you the raw data you need to do everything else—build a realistic budget, set goals you can actually hit, and make real, lasting changes to your financial life. It’s the foundation for everything.

Should I Pay Off Debt or Save for an Emergency Fund First?

Ah, the classic dilemma. The best approach for most people is actually a hybrid one. Financial experts generally agree on a specific order of operations to give you the most security.

First, build a “starter” emergency fund of $500 to $1,000. This small buffer is critical. It’s what keeps a flat tire or a minor repair from immediately sending you back into high-interest credit card debt.

Once you have that initial safety net, you can get aggressive. Shift your focus to paying down any high-interest debts, like credit card balances. After that toxic debt is gone, pivot right back to building your full emergency fund to cover three to six months of essential living expenses. This balanced approach protects you while you make serious progress.

Ready to stop guessing and start seeing your complete financial picture? PopaDex provides the intuitive tools you need to track your net worth, automate your progress, and make smarter decisions with your money. Start your journey to financial clarity today at https://popadex.com.