Our Marketing Team at PopaDex

Personal Finance Checklist: 7 Steps to Financial Success

Navigating the world of money can feel overwhelming. With conflicting advice and endless options, it’s easy to get lost, especially when trying to manage everything from daily spending to long-term investments. That’s where a structured approach makes all the difference. Think of this personal finance checklist not as a rigid set of rules, but as your strategic roadmap to building a resilient financial foundation. It provides a clear, actionable framework designed to bring order to your financial life.

Whether you’re a young professional building wealth, a gig-worker managing irregular income, or an experienced investor looking to optimize your strategy, these seven essential tasks will empower you to make confident decisions and measure real progress. Systematically addressing each point, from building an emergency fund to tracking your net worth, transforms financial chaos into clarity. This guide offers the specific details needed to move from theory to action. For those looking to dive deeper into various aspects of financial education and explore additional perspectives, you might find valuable insights from resources such as this list of sixteen of the best investing and personal finance blogs and podcasts. Let’s begin building your financial future, one checkmark at a time.

1. Build an Emergency Fund (3-6 Months of Expenses)

The first, non-negotiable step on any personal finance checklist is establishing a robust emergency fund. This is more than another savings account; it’s your primary defense against life’s unexpected financial shocks. An emergency fund is a liquid savings account holding enough cash to cover 3 to 6 months of essential living expenses, such as housing, utilities, food, and transportation. Its sole purpose is to provide a financial cushion for true emergencies like a sudden job loss, an unexpected medical bill, or a critical home repair.

Having this fund in place prevents you from derailing your long-term financial goals or resorting to high-interest debt, like credit cards or personal loans, when a crisis strikes. It provides peace of mind and financial stability, allowing you to handle setbacks without panic.

How to Implement Your Emergency Fund

Creating a fully funded emergency reserve takes time and discipline, but a systematic approach makes it achievable. The key is to start small and automate the process.

- Calculate Your Target: First, determine your exact monthly essential expenses. Tally up your mortgage or rent, groceries, utilities, insurance, and minimum debt payments. If this amount is $4,000, your target emergency fund is between $12,000 (3 months) and $24,000 (6 months).

- Start with a Mini-Fund: Popularized by experts like Dave Ramsey, the “baby step” approach is highly effective. Aim for a $1,000 mini-emergency fund first. This initial goal is less intimidating and provides an immediate, tangible buffer for small emergencies.

- Automate Your Savings: The most powerful tool for building savings is automation. Set up a recurring, automatic transfer from your checking account to a separate high-yield savings account (HYSA) each payday. Even a modest amount, like $100 per paycheck, adds up significantly over time.

- Choose the Right Account: Keep your emergency fund separate from your daily checking account to reduce the temptation to spend it. Open an account at a different institution, like Ally Bank or Marcus by Goldman Sachs. These online banks typically offer higher interest rates, allowing your fund to grow passively.

For example, if your target is $15,000, you could set up an automatic transfer of $250 every two weeks. This would have you contributing $6,500 per year, reaching your goal in just over two years without feeling the strain of a large lump-sum contribution. The most crucial part of this personal finance checklist item is consistency.

2. Create and Stick to a Monthly Budget

With a starter emergency fund in place, the next essential item on your personal finance checklist is creating and consistently following a monthly budget. A budget is more than just tracking expenses; it’s a proactive plan that gives every dollar you earn a specific job. By allocating your income to categories like housing, savings, and entertainment before the month begins, you take control of your money and ensure your spending aligns with your financial goals.

This forward-looking approach, often called zero-based budgeting, prevents overspending and eliminates the guesswork from your finances. It empowers you to make conscious decisions about where your money goes, transforming your income from a reactive resource into a powerful tool for building wealth.

How to Implement Your Monthly Budget

A successful budget is one you can stick to, which means finding a method that suits your lifestyle. The key is to be intentional, consistent, and flexible.

- Choose Your Method: Select a framework that makes sense for you. The 50/30/20 rule, popularized by Senator Elizabeth Warren, is a great starting point: allocate 50% of your take-home pay to needs, 30% to wants, and 20% to savings and debt repayment. Alternatively, a more detailed zero-based budget, championed by platforms like YNAB (You Need A Budget), assigns a specific purpose to every single dollar.

- Use Technology to Your Advantage: Manual spreadsheets work, but budgeting apps like YNAB, Mint, or EveryDollar automate the process. They link to your accounts, categorize transactions, and provide a clear, real-time view of your spending against your plan.

- Plan for Irregular Expenses: A common budgeting pitfall is forgetting non-monthly expenses like annual insurance premiums or holiday gifts. Calculate the total annual cost of these items and divide by 12, then set aside that smaller amount each month in a separate savings category.

- Review and Adjust Regularly: A budget is not a set-it-and-forget-it document. Set aside 15-20 minutes each week to review your spending, categorize transactions, and make adjustments. This habit keeps you engaged and helps you quickly correct course if you overspend. For a deeper dive into effective strategies, you can explore our complete guide to mastering budgeting on popadex.com.

For example, if your monthly take-home pay is $5,000, the 50/30/20 rule would allocate $2,500 for needs (rent, groceries), $1,500 for wants (dining out, hobbies), and $1,000 for savings. This simple framework provides both structure and freedom, making your financial goals achievable.

3. Pay Off High-Interest Debt Strategically

After securing an initial emergency fund, the next critical step on your personal finance checklist is to aggressively tackle high-interest debt. This type of debt, often from credit cards or personal loans, can silently drain your income through steep interest charges, making it incredibly difficult to build wealth. A strategic repayment plan focuses your resources on eliminating these liabilities efficiently, freeing up your cash flow for future investments and goals.

Adopting a systematic approach prevents you from feeling overwhelmed and ensures your payments make the biggest possible impact. By prioritizing which debts to pay off first, you can either save the most money on interest or create powerful psychological momentum, both of which are effective paths to becoming debt-free.

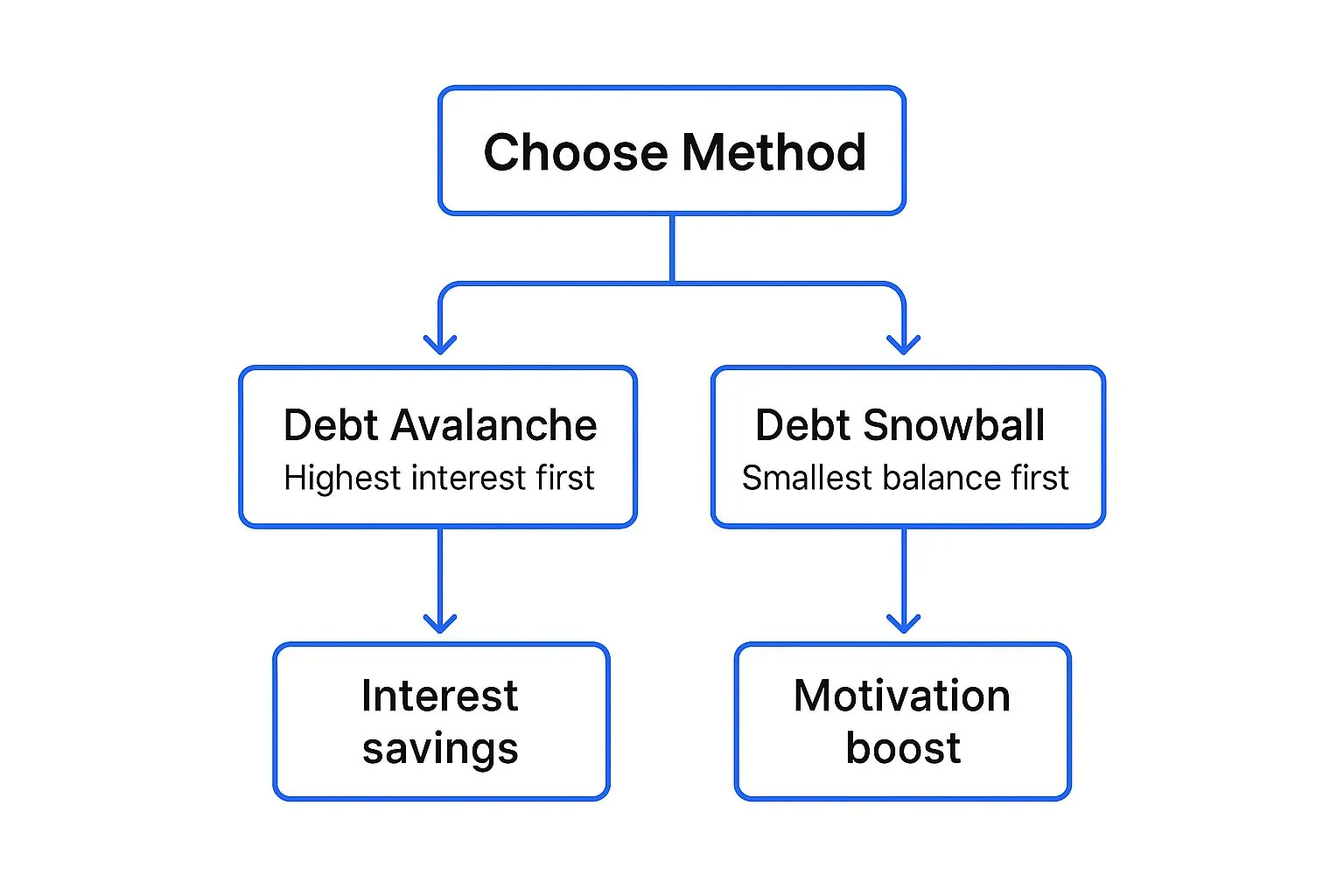

This decision tree infographic illustrates the two primary strategies for paying off debt.

The visualization helps you choose a path based on whether your primary goal is minimizing interest costs (Avalanche) or building motivational momentum (Snowball).

How to Implement Your Debt Repayment Strategy

Choosing the right method and sticking to it is the key to successfully eliminating debt. Both the Avalanche and Snowball methods require a disciplined, focused approach.

- List All Your Debts: Create a comprehensive list of every debt you owe. For each one, note the total balance, the minimum monthly payment, and the annual percentage rate (APR). This clarity is the foundation of your plan.

- Choose Your Method (Avalanche vs. Snowball): The Debt Avalanche method involves making minimum payments on all debts and directing any extra money toward the debt with the highest interest rate. This approach saves the most money over time. The Debt Snowball method, popularized by Dave Ramsey, involves paying off the smallest balance first for a quick psychological win, which can boost motivation.

- Automate Your Payments: Set up automatic payments for at least the minimum on all your accounts to avoid late fees. Then, schedule an additional, larger payment for your target debt account each payday.

- Stop Accumulating New Debt: A crucial part of this process is to stop using credit cards or taking on new loans while you are actively paying down balances. You cannot dig your way out of a hole if you are still digging.

For example, using the avalanche method, if you have a $5,000 credit card balance at 22% APR and a $15,000 student loan at 6% APR, you would direct all extra payments to the credit card first. This strategic focus is an essential part of any effective personal finance checklist.

4. Maximize Employer 401(k) Match

After establishing an emergency fund and tackling high-interest debt, the next critical item on your personal finance checklist is to capitalize on your employer’s 401(k) match. This is often described as “free money” because it represents an immediate, guaranteed return on your investment. A company match is an employer contribution made to your retirement account, contingent upon your own contributions. Its purpose is to incentivize employees to save for retirement.

Failing to contribute enough to receive the full match is like turning down a portion of your salary. It’s one of the most powerful and effortless ways to accelerate your retirement savings. For example, if your employer matches 50% of your contributions up to 6% of your salary, you are effectively earning a 50% return on that portion of your savings before it even sees any market growth.

How to Implement Your 401(k) Match Strategy

Maximizing this benefit is straightforward and can be automated directly through your company’s payroll system. The goal is to set your contribution rate and then let it work for you in the background.

- Find Your Match Percentage: First, contact your HR or benefits department to determine the exact details of your company’s matching program. A common formula is a dollar-for-dollar match up to 3% of your salary, and then fifty cents on the dollar for the next 2%. In this case, you would need to contribute 5% of your salary to receive the full 4% match.

- Set Your Contribution Rate: Log in to your 401(k) provider’s portal (like Fidelity or Vanguard) and set your contribution percentage to at least the minimum required for the full match. Do this immediately upon becoming eligible.

- Automate Increases: A powerful strategy is to increase your contribution by 1% each time you receive a raise or annual cost-of-living adjustment. This method, often called “auto-escalation,” allows you to boost your savings rate without feeling a pinch in your take-home pay.

- Choose Low-Cost Investments: Within your 401(k), opt for low-cost index funds or target-date funds. These options typically have lower expense ratios, ensuring that fees don’t erode your long-term returns. While maximizing your employer’s 401(k) match is a cornerstone of financial planning, it’s also vital to have a clear understanding your 401(k) rights and protections from IRS actions.

For instance, if you earn $60,000 and your employer matches 100% up to 3%, you should contribute at least $1,800 per year (3%). Your employer will add another $1,800, instantly doubling your contribution to $3,600. This personal finance checklist item is your fastest path to significant retirement account growth.

5. Track Net Worth Monthly

While budgeting tracks your cash flow, your net worth is the ultimate scorecard for your financial health. This crucial metric on any comprehensive personal finance checklist provides a high-level snapshot of your progress toward wealth building. It’s calculated by subtracting your total liabilities (what you owe) from your total assets (what you own). Tracking this number monthly reveals the true impact of your saving, investing, and debt-repayment efforts over time.

Monitoring your net worth shifts your focus from merely managing monthly expenses to building long-term wealth. It helps you see how your assets are growing and your debts are shrinking, providing powerful motivation to stay on course. This single figure tells you whether you are moving forward, standing still, or falling behind on your financial journey.

How to Implement Net Worth Tracking

Getting a clear picture of your net worth is easier than ever with modern tools and a simple, consistent process. Automation is your best friend here, as it removes the manual labor and provides real-time updates.

- Consolidate Your Accounts: The first step is to gather all your financial information. List all assets (checking/savings accounts, retirement funds like 401(k)s and IRAs, brokerage accounts, real estate) and all liabilities (mortgages, car loans, student loans, credit card debt).

- Use an Aggregator App: Manually updating a spreadsheet works, but apps like Personal Capital (now Empower Personal Dashboard) or Mint automate the process. Link your accounts once, and the app will pull the data to calculate and display your net worth automatically. This is the most efficient way to get a consistent, up-to-date view.

- Focus on the Trend: Don’t get discouraged by short-term market fluctuations that might cause your net worth to dip month-to-month. The key is to focus on the long-term trend. Is the line generally moving up and to the right over six months or a year? That’s the sign of progress.

- Set Annual Growth Goals: Make your tracking actionable by setting a specific goal, such as increasing your net worth by $20,000 or 15% in the next year. This turns a passive metric into an active target to work toward.

For instance, you might start with assets of $150,000 (investments, savings, home equity) and liabilities of $80,000 (mortgage, student loan), for a net worth of $70,000. By tracking it, you can watch it grow as you pay down your mortgage and your investments appreciate. For a more detailed guide, you can learn more about how to track your net worth on popadex.com.

6. Optimize Insurance Coverage

A crucial yet often overlooked item on any personal finance checklist is optimizing your insurance coverage. Insurance serves as a financial safety net, protecting your assets and income from catastrophic events that could otherwise wipe out years of progress. This involves regularly reviewing and adjusting your policies, including health, auto, home/renters, disability, and life insurance, to ensure you have adequate protection without being over-insured.

The goal is to transfer the risk of major financial loss to an insurance company, safeguarding your savings, investments, and future earnings. Proper coverage prevents a single unexpected event, like a serious illness, car accident, or house fire, from completely derailing your financial plan and forcing you into debt. It is a foundational element of responsible risk management.

How to Implement Your Insurance Review

A proactive and systematic approach to managing your insurance policies ensures your coverage evolves with your life circumstances. The key is to schedule regular check-ins and shop around to find the best value.

- Audit Your Current Policies: First, gather all your insurance documents. Review your coverage limits, deductibles, and premiums. Does your homeowner’s policy reflect the recent kitchen renovation? Is your life insurance sufficient now that you have a child?

- Shop Rates Annually: Loyalty to an insurer rarely pays off. Use comparison tools or contact an independent agent annually to compare quotes. A small amount of time spent shopping can yield significant savings, sometimes hundreds of dollars per year.

- Adjust Coverage for Life Events: Major life changes are a trigger for an immediate insurance review. Getting married, buying a home, having a baby, or getting a significant raise are all events that require you to reassess your coverage needs to protect your growing assets and responsibilities.

- Bundle and Save: Most insurers, like Progressive or Geico, offer discounts for bundling multiple policies, such as auto and home insurance. Inquiring about these discounts is a simple way to lower your total premium without sacrificing protection.

For example, after having a child, you might purchase a term life insurance policy equal to 10 times your annual income to secure your family’s future. Similarly, if your emergency fund has grown large enough, you could increase your auto insurance deductible from $500 to $1,000, which would lower your monthly premium. This step in the personal finance checklist is about being proactive, not reactive.

7. Establish Multiple Income Streams

A key strategy to accelerate wealth creation and build financial resilience is to move beyond a single source of income. Establishing multiple income streams involves creating additional channels for cash flow outside of your primary job. This diversification reduces your reliance on one employer and provides a powerful safety net against economic downturns or unexpected job loss. It fundamentally shifts your financial foundation from a single pillar to a multi-supported structure.

Adding new income sources, whether active side hustles or passive investments, significantly enhances your ability to save, invest, and achieve your financial goals faster. It’s a proactive step toward building a more secure and flexible financial future, transforming your earning potential from a fixed ceiling into a dynamic, growing asset. This approach is a cornerstone for anyone serious about completing their personal finance checklist and building lasting wealth.

How to Implement Multiple Income Streams

Building additional income streams requires identifying your skills and assets and strategically deploying them. The goal is to start small, validate an idea, and scale what works without overwhelming yourself.

- Leverage Existing Skills: The fastest way to start is by monetizing what you already know. If you are a skilled writer, marketer, or developer, you can offer freelance consulting services. If you have deep professional knowledge, consider creating an online course or writing an e-book.

- Invest for Passive Income: Put your capital to work for you. This can include investing in dividend-paying stocks that provide quarterly cash flow or purchasing a rental property to generate monthly rental income. These methods require upfront capital but can become largely passive over time.

- Start Small and Reinvest: You don’t need a revolutionary idea to begin. Start a small side business like pet-sitting or tutoring. Critically, reinvest the initial profits back into the venture to accelerate its growth rather than treating it as disposable income.

- Track and Optimize: Not all income streams are created equal. Meticulously track the time you invest versus the income generated for each venture. This data will help you decide where to focus your energy and what to automate or eliminate.

For instance, a software developer could start by taking on a single freelance project for $2,000. Instead of spending that money, they could use it to build a small software-as-a-service (SaaS) product that generates $100 per month in recurring revenue. By consistently creating and nurturing these streams, you can build a robust financial life. This diversification is a vital component of a comprehensive strategy for achieving financial independence.

7-Point Personal Finance Checklist Comparison

| Item | Implementation Complexity | Resource Requirements | Expected Outcomes | Ideal Use Cases | Key Advantages |

|---|---|---|---|---|---|

| Build an Emergency Fund | Moderate (requires discipline) | Low to Moderate (steady savings) | Financial security; crisis preparedness | Individuals needing a safety net for unexpected events | Prevents high-interest debt reliance; peace of mind |

| Create and Stick to a Monthly Budget | Moderate to High (ongoing tracking) | Low (time, apps/spreadsheets) | Controlled spending; improved financial awareness | Those wanting spending control and goal alignment | Increases financial visibility; reduces overspending |

| Pay Off High-Interest Debt Strategically | High (requires consistent payments) | Moderate (extra payments + discipline) | Reduced debt and interest costs; improved credit | Individuals with multiple debts seeking efficient payoff | Saves money on interest; psychological motivation |

| Maximize Employer 401(k) Match | Low (easy payroll setup) | Low to Moderate (contributions) | Retirement wealth growth; tax benefits | Employees with access to employer-sponsored plans | Immediate 100% ROI via matching; tax advantages |

| Track Net Worth Monthly | Moderate (data collection/updates) | Low (time, tracking tools/apps) | Comprehensive financial health overview | Those focused on long-term wealth tracking | Clear financial snapshot; motivates progress |

| Optimize Insurance Coverage | Moderate (policy review/adjustment) | Low to Moderate (premium costs) | Reduced financial risk from catastrophes | Individuals/families managing risk protection | Saves money via shopping; peace of mind |

| Establish Multiple Income Streams | High (time and effort intensive) | High (time, skills, possible capital) | Increased financial security; accelerated growth | Those able to pursue side hustles or investments | Diversifies income; builds passive revenue |

From Checklist to Lifestyle: Putting Your Financial Plan into Action

Completing a personal finance checklist is a monumental achievement, representing a significant first step toward financial clarity and control. You have methodically addressed the pillars of a strong financial foundation, from building a robust emergency fund to strategically eliminating high-interest debt and tracking your net worth. This is far more than just ticking boxes; it is the act of architecting a more secure and prosperous future for yourself.

However, the true power of this checklist isn’t in its one-time completion. The real, lasting transformation occurs when these actions evolve from a series of tasks into ingrained, sustainable habits. Financial health is not a destination you arrive at, but a dynamic, ongoing journey of mindful decisions, consistent review, and disciplined commitment.

From Tasks to Habits: Internalizing Your Checklist

The items we’ve covered, such as creating a budget, maximizing your 401(k) match, and optimizing insurance, are not set-it-and-forget-it activities. They are living components of your financial life that require periodic attention.

- Review your budget quarterly. Life changes, and so do your income and expenses. A quarterly check-in ensures your budget remains a relevant and effective tool, not an outdated document.

- Re-evaluate debt annually. As you pay down balances or as interest rates shift, your debt repayment strategy might need a refresh.

- Assess insurance at major life events. Getting married, buying a home, or having a child are all critical moments to ensure your coverage still adequately protects your growing assets and responsibilities.

By turning these check-ins into routines, you move from a reactive state of managing financial emergencies to a proactive state of building enduring wealth. This shift in mindset is the most valuable takeaway from any personal finance checklist.

The Broader Impact: More Than Just Money

Mastering these financial principles builds more than just a healthy bank account. It cultivates resilience, giving you the confidence to navigate unexpected job losses or economic downturns. It fosters freedom, empowering you to pursue career changes, travel, or other life goals without being shackled by financial anxiety.

As you transition your checklist into a sustainable financial lifestyle, remember that long-term goals like retirement planning are crucial components. Ensuring your short-term actions align with your long-term vision is key to building a comprehensive financial strategy. For those looking to deepen their understanding of this critical area, you can explore comprehensive retirement planning resources to help map out your path to a secure future.

Ultimately, this checklist is your map. You have navigated the initial terrain successfully. Now, the goal is to keep it open, refer to it often, and let it guide you as you continue your journey. Celebrate your progress, learn from your setbacks, and remember that every consistent, positive action you take is a powerful investment in yourself.

Ready to automate your progress and make tracking your financial health effortless? Sign up for PopaDex to seamlessly monitor your net worth, investments, and overall financial picture in one place. Turn your personal finance checklist into a dynamic, real-time dashboard with PopaDex today.