Our Marketing Team at PopaDex

Personal Net Worth Calculator: Instantly Track Assets & Liabilities

At its core, a personal net worth calculator is a tool that tells you where you stand financially. It does this by taking everything you own (your assets) and subtracting everything you owe (your liabilities). The result is a single, powerful number that acts as your personal financial scorecard.

The formula is dead simple: Assets - Liabilities = Net Worth.

Why Tracking Your Net Worth Is a Financial Game Changer

Calculating your net worth isn’t just an exercise for the ultra-wealthy—it’s one of the most important things you can do for your financial well-being. Think of it as a snapshot. It cuts through all the noise of your monthly income and spending to show you what you’ve actually built over time.

This guide isn’t about theory; it’s about giving you a clear, actionable process. By the end, you’ll have the confidence to measure your financial standing accurately, no matter where you are in your journey.

To help you get started, here’s a quick breakdown of the core components.

Your Net Worth Calculation at a Glance

This quick-reference table breaks down the core elements of your net worth, with clear examples to help you start categorizing your finances immediately.

| Component | What It Is | Common Examples |

|---|---|---|

| Assets | Anything you own that has monetary value. | Cash in bank accounts, investments (stocks, bonds), retirement funds (401k, IRA), real estate (your home), vehicles, valuable personal property. |

| Liabilities | Any debt or financial obligation you owe to others. | Mortgages, car loans, student loans, credit card balances, personal loans, medical debt. |

| Net Worth | The difference between your total assets and total liabilities. | This is the final number that represents your current financial position. It can be positive or negative. |

Think of this table as your starting point for gathering all the necessary pieces of your financial puzzle.

A Clear Measure of Financial Progress

Unlike your salary, which just shows money coming in, your net worth reveals the bigger picture. It’s the ultimate measure of financial health because it balances both sides of your financial life. This one number helps you answer the questions that really matter:

- Am I actually saving enough? If your net worth is climbing, your savings and investment strategies are paying off.

- Is my debt getting out of hand? If your liabilities are growing faster than your assets, it’s a red flag telling you to rethink your debt strategy.

- Am I on track for retirement? Watching this number grow over time is the best indicator of whether you’re building enough wealth for the future.

This clarity is especially vital when you look at global wealth distribution. The global wealth pyramid paints a stark picture: just 1.6% of adults hold 48% of the world’s wealth, while a staggering 1.55 billion people in the under-$10k tier possess only 0.6%. You can dig deeper into these global wealth trends on Voronoiapp.com. This disparity shows exactly why taking personal control of your financial measurement is non-negotiable for building your own security.

Your net worth is your financial reality check. It isn’t about comparing yourself to others; it’s about competing with the person you were yesterday and building a more secure future.

Building a Complete Picture of Your Assets

Before you can get a real sense of your financial standing, you need to roll up your sleeves and take a detailed inventory of everything you own. This is the “assets” side of your net worth equation, and getting it right is the first step toward a true financial snapshot.

Think of it like creating a personal balance sheet. A lot of people stop at their checking account balance, but what you own goes so much deeper than that. The key is to be thorough without getting lost in the weeds.

Valuing Your Liquid and Invested Assets

Let’s start with the easy stuff: your financial assets. These are often called liquid assets because you can turn them into cash without much fuss. To get their value, just pull up the most recent statements from your accounts.

- Cash and Cash Equivalents: This is what’s sitting in your checking and savings accounts, plus any money market funds. The value here is simple—it’s the current balance.

- Retirement Accounts: Log into your 401(k), IRA (Roth or Traditional), or any other employer retirement plan. The current value is what you’re looking for.

- Taxable Investment Accounts: This includes any brokerage accounts where you hold stocks, bonds, mutual funds, or ETFs. Your latest statement will give you the up-to-the-minute figure.

- Other Financial Assets: Don’t forget about things like a Health Savings Account (HSA), the cash value of a life insurance policy, or any certificates of deposit (CDs).

Keeping a close eye on these numbers is more important than ever. The UBS Global Wealth Report 2025 noted that global wealth jumped by 4.6% in 2024. While the average North American adult had a net worth of $593,347, more than half the markets studied actually saw a decline in real USD terms. This is exactly why a personal net worth calculator is so essential for charting your own course.

Assessing Your Physical and Tangible Assets

Next up are the things you can actually touch. Valuing these takes a bit more guesswork, but the goal here is to be realistic, not sentimental.

For most people, their home is their biggest asset. Understanding its value through your home’s appraisal process is key, but for a quick check, online real estate sites can give you a decent ballpark figure. Just remember to be conservative with your estimate. If you want to dig deeper into how this works, you can learn more about real estate equity in our detailed guide.

Real-World Tip: When it comes to personal items like your car or jewelry, never use the price you paid. Look up the resale value—what someone would actually pay you for it today. Kelley Blue Book is great for getting a reliable estimate on vehicles.

Here are a few other common physical assets you’ll want to add to your list:

- Vehicles: Cars, motorcycles, boats, or RVs.

- Valuable Personal Property: Think high-end jewelry, art, antiques, or collectibles. Be honest about their current market value.

- Digital Assets: This could be valuable domain names or your cryptocurrency portfolio.

- Business Interests: If you own a business, you’ll need to estimate its value. This one can get tricky, and for a truly accurate number, you might need a professional valuation.

Getting an Honest Tally of Your Liabilities

Alright, you’ve got a handle on your assets. Now it’s time to look at the other side of the balance sheet: your liabilities. This is where you list everything you owe. Getting this part right is non-negotiable for an accurate net worth calculation—every single debt has to be on the books, big or small.

This isn’t about feeling bad about debt; it’s about gaining clarity. I’ve seen plenty of people skip this step because it feels intimidating, but that number is the key. Seeing it in black and white is the first real step toward getting it under control. Without it, you’re only telling yourself half the story.

Categorizing Your Debts

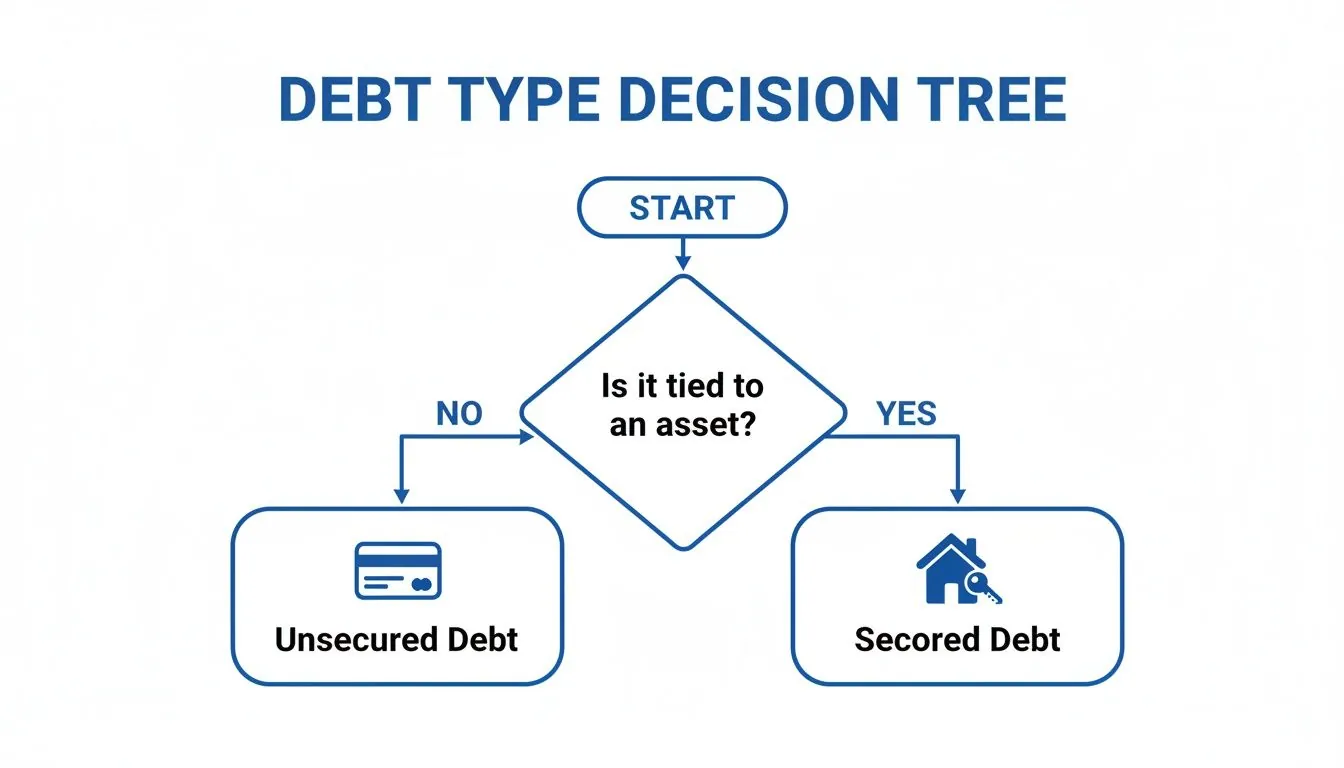

Most of what you owe will fall into two buckets: secured and unsecured debt. Knowing the difference helps you get organized and see your financial life more clearly.

Secured debts are loans backed by an asset. If you don’t pay, the lender has a claim on that item. The usual suspects here are:

- Mortgages: The loan on your house or any other real estate you own.

- Auto Loans: The financing on your car, truck, or motorcycle.

- Other Secured Loans: This could be a loan for something like a boat or an RV.

Unsecured debts aren’t tied to any physical collateral. The lender is basically trusting you to pay it back based on your credit history. These are incredibly common:

- Credit Card Balances: The total amount you owe across all your cards.

- Student Loans: This includes both federal and private student loans.

- Personal Loans: Any loan from a bank, credit union, or online lender that isn’t backed by an asset.

- Medical Debt: Unpaid bills from doctors, hospitals, or other healthcare providers.

The trick here is precision. Don’t guess or use the original loan amount. You need to log into each account and find the current principal balance—that’s the exact amount you owe today.

A common mistake I see is people forgetting about the newer, smaller forms of debt. Those “buy now, pay later” services like Klarna or Afterpay? They absolutely count as liabilities and need to be included if you want an honest tally.

Why This Tally Matters More Than You Think

Having a complete picture of your liabilities does more than just plug a number into your net worth formula. It’s the raw material for building a real financial strategy.

When you see all your debts listed out, you can immediately spot which ones are costing you the most in interest. This detailed list is the launchpad for creating a smart repayment plan. Knowing exactly where you stand empowers you to make better decisions. To see how to put this knowledge to work, check out our guide on how to pay off debt more effectively. It’s all about turning this information into action.

Handling Complex and Unique Financial Situations

Standard net worth calculators can feel like trying to fit a square peg in a round hole when your finances get a little messy. Real life rarely fits into neat boxes.

Maybe you’re an expat, a digital nomad, or just a savvy global investor. If so, you’re likely juggling assets and debts in multiple currencies. Or maybe you’re a freelancer whose income looks more like a rollercoaster than a steady paycheck. Getting an accurate number in these situations just requires a smarter approach.

Managing Fluctuating Income and Currencies

For anyone not on a fixed salary, your net worth can swing wildly from month to month if you’re not careful. To get a more stable picture, you need to normalize your earnings.

I’ve found the best way to do this is to calculate your average monthly income over the past 6-12 months. This smooths out the peaks and valleys, giving you a much more realistic baseline for your financial planning.

Dealing with multiple currencies throws a similar wrench in the works. My advice? Don’t just grab today’s exchange rate. To avoid the noise of daily market swings, consider using a 30-day average exchange rate for your conversions. It gives you a far more stable valuation over time.

A consistent methodology is more important than chasing the perfect daily exchange rate. The goal of a personal net worth calculator is to track your long-term trend, not to time the currency markets.

This global view is more critical than ever. In 2024 alone, the financial assets of private households jumped by 8.7% to hit an incredible EUR 269 trillion. North America was a huge part of that, and the US drove 53.6% of last year’s growth. You can dig into these trends in the Allianz Global Wealth Report 2025.

Valuing Assets That Aren’t Traded Publicly

So, what about the stuff you can’t just look up on a stock ticker? Valuing illiquid assets—things like art, private equity, or collectibles—is definitely part art, part science. You’ve got a few options here.

- Conservative Estimates: For personal collectibles or small business holdings, your best bet is to use a conservative, “fire sale” value. Think about what you could realistically get if you had to sell it quickly.

- Recent Comparables: Look for recent sales of similar items. For a piece of art, check auction results for the same artist. For shares in a private company, the valuation from the last funding round is a great starting point.

- Professional Appraisals: If you’re dealing with high-value assets like significant real estate or a serious art collection, a professional appraisal is the way to go. It gives you an accurate, defensible number, and you’ll probably need it for insurance or estate planning anyway.

When you’re tallying up your finances, it’s also crucial to understand the different kinds of debt you hold. This flowchart breaks it down nicely.

As the diagram shows, the main difference between secured and unsecured debt is simple: is the loan tied to a specific asset the lender can take if you don’t pay? That distinction has a big impact on your overall financial picture.

How to Automate Your Net Worth Tracking

After walking through all the manual steps, you’ve probably realized something: tracking your finances is powerful, but it’s also a serious time sink. Hunting down statements, guessing at valuations, and wrangling spreadsheets can quickly feel like a chore that’s always getting pushed to the bottom of the list.

This is where automation becomes your financial superpower. It turns a tedious, once-a-quarter task into a real-time, effortless overview of your entire financial life.

The real value of tracking your net worth comes from consistency, and doing it by hand just creates friction. Instead of spending hours pulling together data, you could be using that time to actually analyze the trends and make smarter decisions. A good personal net worth calculator removes all that administrative baggage, giving you back your most valuable asset: your time.

Let Technology Do the Heavy Lifting

This is exactly why tools like PopaDex exist. Think of it as an intelligent assistant that handles all the tedious data gathering for you. Instead of logging into a dozen different accounts, the platform securely connects to thousands of banks and financial institutions to pull your data automatically.

This automated approach completely changes how you interact with your finances.

- Real-Time Updates: Your net worth is always current. Market swings in your investment portfolio or payments on your mortgage are reflected instantly—without you lifting a finger.

- Complete Accuracy: Automation gets rid of the risk of manual errors, like typos or forgetting about an old account, ensuring your financial picture is always precise.

- Effortless Consolidation: It brings everything together in one place, from your local bank account and international investments to your mortgage and credit card debt.

You can learn more about the mechanics behind this by exploring the details of financial data aggregation on PopaDex. This technology is the engine that powers seamless and secure financial tracking.

The screenshot below gives you a peek at a PopaDex dashboard. It visualizes your assets, liabilities, and overall net worth in a clean, intuitive way.

What you’re seeing is financial clarity at a glance. It’s about transforming raw numbers into meaningful insights you can actually use to guide your decisions.

From Complex Data to Clear Insights

One of the biggest headaches with manual tracking, especially for anyone with a global footprint, is handling multiple currencies. An automated platform like PopaDex solves this instantly by converting all your international assets and liabilities into your chosen base currency. This gives you a true, apples-to-apples view of your global financial standing.

Investing in a tool that automates your net worth tracking isn’t an expense; it’s an investment in financial clarity and efficiency. The small monthly cost, often less than a few cups of coffee, buys back hours of your time and provides a level of insight that’s difficult to achieve manually.

Whether you start with a free plan to get organized or upgrade for full automation, the goal is the same: to make tracking your net worth a simple, sustainable habit.

By removing the friction of manual calculations, you are far more likely to stay engaged with your financial journey, celebrate your progress, and spot potential issues before they become major problems. Automation essentially puts your financial scorecard on autopilot, so you can focus on winning the game.

Common Questions About Calculating Net Worth

Once you start the journey of tracking your net worth, a few practical questions almost always come up. Getting these sorted out is the difference between having a number you trust and one that feels a bit fuzzy. It’s not just about getting an answer; it’s about feeling confident in your financial snapshot.

Let’s clear up some of the most common hurdles people hit when they first start out.

How Often Should I Calculate My Net Worth?

For most people, a quarterly check-in is the sweet spot. It’s frequent enough to track real progress and make smart adjustments to your financial plan, but not so often that you get bogged down by the daily chaos of market swings.

Of course, your situation might be different. If you’re on a mission to aggressively crush debt or you’re just a few years away from a big goal like retirement, switching to a monthly update can give you that extra dose of motivation and feedback. The real key isn’t the exact frequency—it’s consistency.

Don’t let perfection be the enemy of good. A consistent quarterly update is way more valuable than a sporadic, stressful attempt to track your finances every single day. Think progress, not perfection.

Should I Include My Primary Home?

Yes, absolutely. For a huge number of people, their home is their single biggest asset, and the mortgage is their largest liability. If you leave them out, the picture of your financial health is completely distorted.

Here’s how to handle it correctly:

- Value Your Home Realistically: Look up recent, comparable sales in your neighborhood or use a trusted online valuation tool to get a current market estimate. Be conservative here—this isn’t the time for wishful thinking.

- List the Full Mortgage Balance: Grab your latest mortgage statement and find the current principal balance you still owe.

- Include Both in Your Calculation: The home’s value goes into your assets column, and the mortgage balance goes into your liabilities.

Doing this properly ensures your net worth accurately reflects the home equity you’ve built, which is a massive part of your overall wealth.

What Is a Common Mistake to Avoid?

One of the easiest traps to fall into is overvaluing personal property. It’s tempting to think about your car, furniture, or electronics in terms of what you paid for them. But for your net worth, the only number that matters is what someone would actually pay for them today. Always stick to the fair market value, not the original sticker price.

Another sneaky one is forgetting about smaller debts. All those “buy now, pay later” plans from services like Klarna or Afterpay? They’re liabilities. They might seem small on their own, but they can add up fast and should definitely be included for an honest financial check-up.

Ready to stop wrestling with spreadsheets and get a clear, automated view of your finances? PopaDex securely connects to your accounts to provide a real-time, accurate picture of your net worth, so you can focus on growing it. Get started for free on PopaDex.