Our Marketing Team at PopaDex

Salary Conversion by Country A Global Pay Guide

That $100,000 salary offer? Its actual value is a moving target, completely dependent on where you lay your head at night. This is the whole idea behind salary conversion by country: figuring out what your income truly buys you in another part of the world. It’s a process that goes way beyond a simple currency exchange and dives into the real cost of living on the ground.

Why a $100K Salary Feels Different Everywhere

Looking at a job offer from another country is a mix of excitement and pure confusion. A six-figure salary sounds fantastic on paper, but what does it actually get you in Berlin versus Boston? The answer is all about understanding your salary’s true “power,” which can swing wildly from one city to the next.

Think of it like a car’s gas mileage. That same gallon of gas—or in this case, a dollar earned—will take you much further on an open highway than it will in bumper-to-bumper city traffic. Your income works the same way; its financial mileage is dictated by the local economic terrain. A lower salary in a city with cheap rent and affordable groceries can easily lead to a better lifestyle than a higher one in an expensive metropolis.

The Global Pay Gap in Action

And we’re not talking about small changes here; the differences can be staggering. A look at global salary data shows the average monthly net salary in Switzerland is a whopping $8,218, while in Luxembourg, it’s around $6,740. The United States comes in at $6,562. Compare that to many developing nations where average wages often fall below $500 per month. You can dig into more of this global salary comparison data to see just how wide the gap is.

To make a smart global career move, you need to get a handle on a few key concepts, which we’ll break down in this guide:

- Purchasing Power Parity (PPP): This is the real-deal measure of what your money is worth.

- Cost-of-Living Adjustments (COLA): This is how companies try to even things out for their international employees.

- Hidden Factors: We’ll look at why you absolutely cannot ignore things like taxes, healthcare, and housing.

By the end of this, you’ll see that a good salary conversion goes beyond the number on your contract. It’s about understanding the lifestyle that number actually supports.

From Theory to Financial Reality

This table offers a quick snapshot of how the same nominal salary translates into different real-world purchasing power across various economic landscapes.

At a Glance: How Salary Value Changes Globally

| Key Concept | What It Means for Your Salary | Real-World Scenario |

|---|---|---|

| Nominal Salary | The face value of your paycheck in the local currency. | You’re offered $100,000 a year to work in San Francisco. |

| Exchange Rate | A simple currency swap that ignores local prices. | That $100,000 becomes roughly €92,000 in Berlin. Sounds great, but it’s not the full story. |

| Purchasing Power | The actual amount of goods and services you can buy. | Your €92,000 in Berlin buys you a larger apartment, more dinners out, and cheaper groceries than your $100,000 would in San Francisco. |

| Real Salary | Your salary adjusted for purchasing power and cost of living. | Though the number is smaller, your real salary in Berlin gives you a higher standard of living and more disposable income. |

Ultimately, the biggest mistake you can make is failing to look past that surface number. An impressive-looking salary in Zurich could get chewed up by some of the world’s highest living costs, leaving you with less cash in your pocket than a more modest salary in Lisbon might.

This guide gives you the framework to compare offers accurately. We want to make sure your next international move is a financial step forward, not a surprising step back. We’ll give you the tools to see past the currency symbols and understand the true value of your hard-earned money.

Decoding the Three Core Conversion Methods

So, you’re trying to figure out what a salary is actually worth in another country. It’s a common puzzle, but the answer is rarely as simple as plugging numbers into a currency converter. To get the real story, you need to look a little deeper.

Let’s break down the three main ways to think about salary conversion. We’ll start with the most basic and build up to the most accurate, so you can see how the picture gets clearer with each step. Getting this right is crucial—relying on the wrong method can lead to some nasty financial surprises down the road.

Method 1: Direct Currency Exchange

This is the one everyone knows. The direct currency exchange rate (often called the spot rate) is what you see on Google or your banking app. It’s a straightforward number that tells you how many euros you’ll get for your dollars right now.

For instance, say you’re offered $80,000 in the US. If the exchange rate is €0.92 to the dollar, a quick calculation shows you’d have €73,600 in Germany. Simple, right? It’s a necessary first step, but it’s also incredibly misleading if you stop there.

Why? Because this method completely ignores the most important factor: what that money can actually buy. It works on the flawed assumption that a euro in Berlin has the same spending power as its dollar equivalent in Boston. Spoiler alert: it almost never does. This is the single biggest mistake people make when evaluating an international offer.

The Key Takeaway: Direct exchange is a starting point, not a conclusion. It only tells you how much foreign currency you’ll have, not how far it will go.

Method 2: Purchasing Power Parity

This brings us to a much smarter way of looking at things: Purchasing Power Parity (PPP). This concept tackles the real question: “How much stuff can I actually afford?” Instead of just swapping currencies, PPP compares the cost of a standard “basket of goods” in different countries to measure a currency’s true buying power.

The most famous (and fun) example of this is The Economist’s Big Mac Index. The logic is simple: a Big Mac is pretty much the same product no matter where you buy it. If one costs $5.70 in the US but only €4.50 in Spain, it suggests your money for everyday items simply stretches further in Spain.

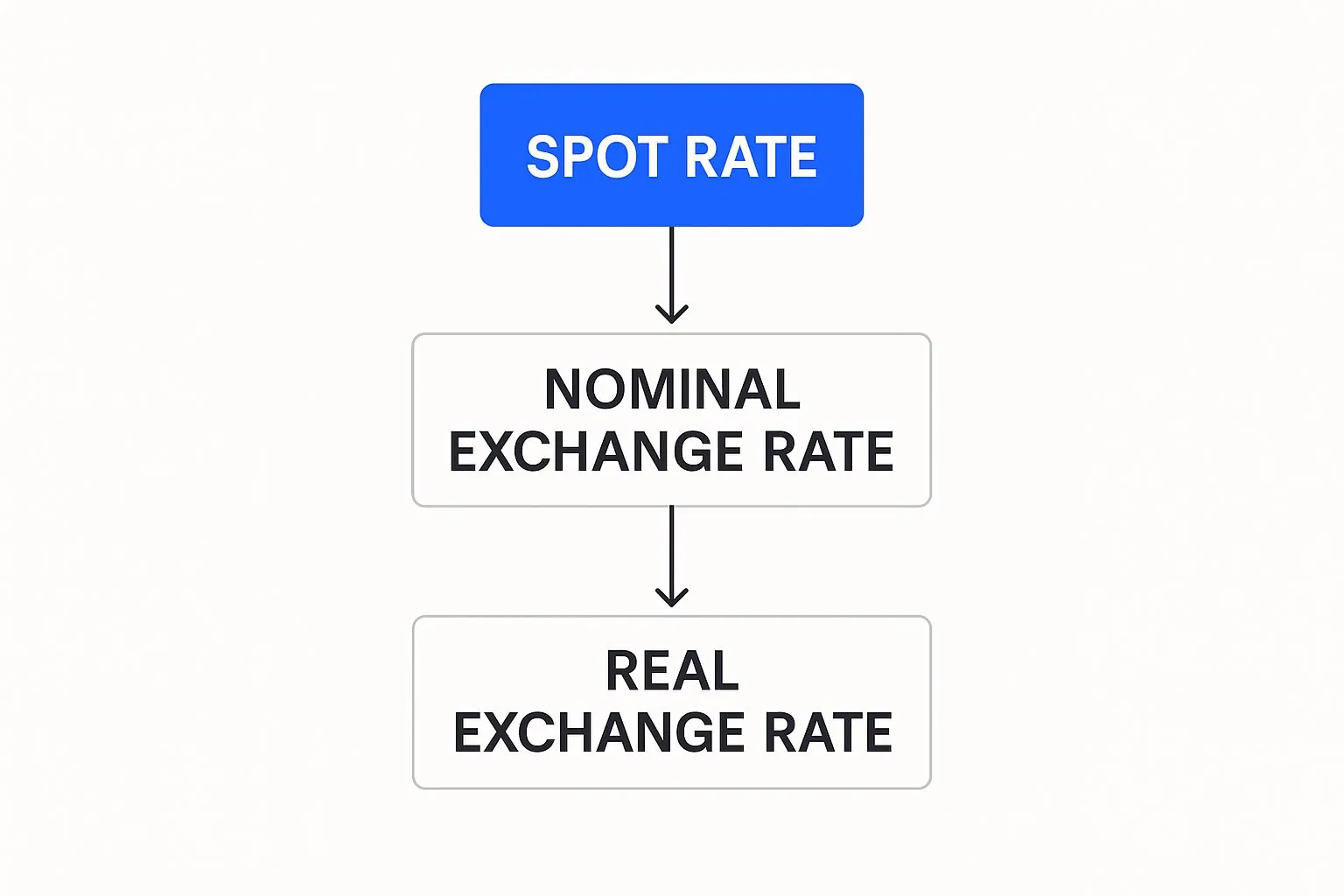

This infographic helps visualize how these concepts build on each other, moving from a superficial number to a much more realistic view.

As you can see, the nominal exchange rate is just the tip of the iceberg. The real exchange rate, which factors in local prices, gives you a far more accurate picture of your financial life. For any serious salary conversion by country analysis, PPP is a much better tool because it starts to reflect your potential lifestyle.

You can see just how big these differences are when you look at wages around the world. Minimum wage, for example, ranges from as low as $46 a month in Nigeria to $3,254 in Luxembourg. A PPP-based lens helps make sense of these huge gaps, showing it’s less about the raw number and more about what it buys locally. This guide to minimum wage levels by country really highlights the global disparities.

The Key Takeaway: PPP adjusts for what things actually cost on the ground, giving you a much clearer idea of the lifestyle a salary can support.

Method 3: Cost-of-Living Adjustment

Finally, we arrive at the gold standard: the Cost-of-Living Adjustment (COLA). This is the highly detailed method that big multinational companies use when creating compensation packages for their employees moving abroad. Its entire purpose is to ensure you can maintain a similar standard of living, no matter where you’re based.

COLA goes way beyond a generic basket of goods. It’s a meticulous calculation that compares hundreds of specific expenses between two cities. We’re talking about everything:

- Housing: The rent or mortgage for a comparable home.

- Groceries: What you’ll actually pay for your weekly shopping.

- Transportation: The cost of a monthly transit pass, gas, and car maintenance.

- Healthcare: Insurance premiums and typical out-of-pocket costs.

- Education: Tuition for international schools, if that’s a factor.

- Taxes: Critical differences in income and sales tax.

For example, if an analysis shows that living in Zurich is 30% more expensive than your home city of Austin, a company would likely apply a +30% COLA to your base salary. The goal is to make sure your disposable income—the money you have left after all the bills are paid—stays about the same. It’s the most precise way to handle a salary conversion because it’s tailored to individual circumstances and specific locations.

The Key Takeaway: COLA is the most comprehensive method, designed to neutralize the financial impact of a move by adjusting your salary to match local costs precisely.

The Hidden Factors That Shape Your Real Pay

A salary conversion calculator will spit out a number, but that’s just the beginning of the story. To really wrap your head around what an international job offer means for your life and your wallet, you have to dig deeper.

Think of the converted salary as the headline. The real story is in the fine print—the hidden variables that determine what you actually get to keep and what your lifestyle will look like. Overlooking these details is the single biggest mistake people make when planning a move abroad. A huge salary on paper can wither away under the pressure of high taxes and a brutal rental market.

The Great Tax Divide

The first, and arguably most important, factor is the local tax system. Tax policies are wildly different from country to country, and they directly dictate how much of your paycheck ever makes it into your bank account.

Let’s look at two completely different worlds:

- Dubai, UAE: This place is famous for its 0% personal income tax. If you earn $100,000, you take home pretty much all of it. That’s a massive financial leg up.

- Sweden: On the other hand, Sweden funds its incredible social programs with high taxes. That same $100,000 salary could be hit with a marginal tax rate over 50%. You keep less, but you get extensive public services in return.

This isn’t just about numbers; it’s about a fundamental difference in how a country operates. Any meaningful salary conversion by country has to be based on your net, after-tax income.

Housing: The Anchor of Your Budget

Right after taxes, housing is almost always the biggest line item in your budget. The cost of rent can make or break a move, completely changing the real value of your salary.

For instance, a modern one-bedroom apartment in the heart of Tokyo can easily run you over $1,500 a month. Head over to Mexico City, and a similar apartment in a great neighborhood might only cost around $700. That $800 monthly difference adds up to nearly $10,000 in your pocket each year, just by choosing a different city.

Your real salary goes beyond what you earn; it’s what you have left after paying for a place to live. A lower housing cost directly translates to greater financial freedom and a higher standard of living.

To put this into perspective, let’s compare some key costs across different international cities. A high salary in one city might not go as far as a more modest one in another once you factor in non-negotiable expenses like rent.

Comparing Essential Costs in Major Global Hubs

This table offers a side-by-side look at how key living expenses dramatically alter the real value of a salary in different international cities.

| City | Average Monthly Rent (1-BR City Center) | Average Net Salary (USD) | Effective Local Salary Index |

|---|---|---|---|

| New York, USA | ~$4,200 | $6,500 | Very High Cost, High Salary |

| London, UK | ~$2,800 | $4,800 | High Cost, Moderate Salary |

| Tokyo, Japan | ~$1,500 | $3,200 | Moderate Cost, Moderate Salary |

| Dubai, UAE | ~$2,000 | $5,500 (tax-free) | High Cost, Very High Net Salary |

| Mexico City, Mexico | ~$700 | $1,200 | Low Cost, Lower Salary |

As you can see, the relationship between salary and major costs like rent is what truly defines your purchasing power. A tax-free salary in Dubai, for example, gives you significantly more breathing room than a comparable gross salary in London.

Beyond Rent and Taxes: The Daily Grind Costs

While taxes and housing are the heavy hitters, a whole host of smaller daily and monthly costs can quietly eat away at your income. If you don’t account for them, your budget will be a work of fiction.

These are the crucial factors you can’t ignore:

- Healthcare: Is there a public system, or are you on the hook for expensive private insurance? A family’s health insurance in the U.S. can cost a small fortune every month, a cost that’s practically zero in places like the UK with its National Health Service.

- Transportation: Do you need to own a car, or is the public transit amazing and cheap? Buying, insuring, and fueling a car in a city like Singapore is incredibly expensive. In Berlin, a monthly transit pass is a much smarter, more affordable choice.

- Social Security & Pensions: Many countries require you to contribute to social security or pension funds right out of your paycheck. It’s a form of forced savings, which is great for the future, but it definitely reduces your cash flow today.

To get a real feel for your potential new life, you need to dive into the specifics. For example, you can explore the true cost of living in Cyprus to see how these daily expenses stack up. And since your money will be crossing borders, even small currency shifts can affect your budget, so understanding how to start managing foreign exchange risk is a smart move for your personal finances.

By creating a detailed checklist of these hidden costs, you can move beyond a simple currency conversion and build a financial plan that actually works in the real world.

Putting Salary Conversion into Practice

All the theory in the world is great, but nothing beats seeing how the numbers play out in real life. Let’s walk through a few scenarios to see how a salary conversion by country actually works for real people making big career moves.

These examples will show you just how dramatically things like the local cost of living, taxes, and economic conditions can change the true value of your paycheck. We’re about to turn a confusing financial puzzle into a clear, actionable picture.

Case Study 1: The US Software Engineer in Lisbon

First up is Alex, a software engineer in Austin, Texas, making a solid $120,000 a year. A company in Lisbon, Portugal, offers Alex a job for €75,000.

On the surface, this looks like a huge pay cut. A straight currency conversion (at about $1.08 per euro) makes the offer roughly $81,000. Why would anyone take that?

This is exactly where a Cost-of-Living Adjustment (COLA) completely changes the game.

- The Salaries: $120,000 in Austin vs. €75,000 (~$81,000) in Lisbon.

- The Twist (Cost of Living): Lisbon is around 45% cheaper to live in than Austin. Rent alone can be 60-70% less expensive.

- The Tax Factor: While Portugal has a progressive tax system, the lower salary base means Alex’s effective tax rate is perfectly manageable.

Once Alex crunches all the numbers, the story flips. That $39,000 drop in salary doesn’t just disappear—it’s swallowed whole by the massive reduction in daily expenses. After factoring in cheaper rent, groceries, public transit, and nights out, Alex’s disposable income (the cash left after all the bills are paid) could actually be 10-15% higher in Lisbon.

This is the perfect example of why you can’t just look at the salary number. A lower income in a more affordable city can easily lead to a better lifestyle and more money in your savings account.

Case Study 2: The UK Marketing Director in Dubai

Now, let’s look at Sarah, a marketing director from London earning £70,000 (about $88,000). She gets an offer to move to Dubai for a new role paying AED 400,000.

A quick currency conversion shows the Dubai salary is around $109,000. That’s already a nice bump.

But the real game-changer isn’t the exchange rate. It’s the tax.

- London Take-Home Pay: In the UK, a £70,000 salary is hit with income tax and National Insurance. After all is said and done, Sarah actually takes home about £50,500 (or $63,500).

- Dubai Take-Home Pay: The United Arab Emirates has 0% personal income tax. Sarah’s take-home pay in Dubai is the full AED 400,000 (or $109,000).

This difference is staggering. Even with Dubai’s notoriously high cost of living, the jump in net pay is so huge it completely transforms her financial picture. Her actual take-home pay skyrockets by over 70%. This massive boost gives her more than enough to cover the higher rent in Dubai while still having far more spending and saving power than she ever did in London. It’s a powerful lesson in how taxes can be the single most important factor.

Case Study 3: The Freelancer in Buenos Aires

Finally, let’s look at something a bit more complicated. Meet Marco, a freelance graphic designer living in Buenos Aires, Argentina. He bills his US client $4,000 per month, paid in US dollars. His situation highlights the wild ride of hyperinflation and tricky exchange rates.

In Argentina, there’s an official government exchange rate and a much more favorable unofficial rate known as the “blue dollar.” Knowing how to navigate this is everything.

- The Challenge: If Marco converts his pay at the official bank rate, he loses a huge chunk of its value. On top of that, Argentina’s inflation has been over 200% annually, meaning the peso’s value is in constant freefall.

- The Strategy: Marco uses financial services that let him tap into the “blue dollar” rate, which can nearly double the amount of pesos he gets for his dollars. He’s also careful to only convert what he needs for his immediate expenses, keeping the rest of his savings in dollars to shield them from devaluation.

Marco’s case proves that in some countries, a simple salary conversion by country is not nearly enough. You have to get smart about the local economic realities, like inflation and currency controls, just to protect your earnings.

For anyone in a situation like this, having a powerful financial tool is non-negotiable. Using a salary comparison by country calculator can give you a much clearer sense of where you truly stand. For Marco, his real income goes beyond the $4,000 he bills; it’s how effectively he can turn that into spending power in one of the world’s most volatile economies.

Your Toolkit for Accurate Salary Comparisons

Knowing the theory behind salary conversion is one thing, but actually putting it to work requires the right tools. When you’re staring at an international job offer, you need to move past the abstract ideas and get your hands on some hard data. This section is your resource library, designed to help you build a truly clear financial picture.

We’ll explore a few different types of tools: crowd-sourced data hubs, a classic economic snapshot, and modern financial dashboards. Each one gives you a unique angle for a proper salary conversion by country. Knowing which tool to use, and when, is the secret to setting a realistic budget and negotiating with confidence.

The Crowd-Sourced Data Powerhouse: Numbeo

When you need to know the price of a gallon of milk or the average rent for a one-bedroom apartment in downtown Lisbon, Numbeo is where you turn. It’s the world’s biggest database of user-submitted prices for everyday goods and services.

Think of it as a gigantic, living survey where real people in thousands of cities are constantly reporting what they actually pay. Its power lies in that incredible, city-specific detail.

- Best For: Getting a super-detailed breakdown of day-to-day living expenses in a specific city.

- Strengths: Its city-level data is massive, user-contributed prices give you a real-time feel, and the cost-of-living calculator is fantastic for comparing two places side-by-side.

- Weaknesses: Because it’s crowd-sourced, you might find some inconsistencies or slightly outdated info, especially in less-populated areas. Always cross-reference.

The Classic PPP Snapshot: The Big Mac Index

Created by The Economist, the Big Mac Index is a wonderfully simple and effective way to wrap your head around Purchasing Power Parity (PPP). The logic is straightforward: a Big Mac is the same product no matter where you buy it, so its price should be roughly the same after you account for currency exchange.

If a Big Mac is cheaper in one country, that currency is considered “undervalued,” which means your money goes further. If it’s more expensive, the currency is “overvalued.”

The Big Mac Index isn’t a precise scientific instrument, but it’s a brilliant at-a-glance indicator of a country’s general affordability. It cuts through all the complex economic jargon and gives you an instant gut-check on your potential buying power.

The Modern Financial Command Center: PopaDex

Numbeo tells you what things cost and the Big Mac Index gives you a quick economic vibe check. But a tool like PopaDex helps you see how that new salary actually fits into your entire financial life. After all, a true salary conversion is more than a one-time calculation; it’s about understanding how that income impacts your net worth, especially when you’re juggling multiple currencies.

Here’s a look at the PopaDex dashboard, which pulls all your different financial accounts into one place.

This holistic view is a game-changer for expats or anyone managing assets across borders. It shows you exactly how a new salary impacts your savings, investments, and debts in real time.

Modern platforms like this are built for the reality of a global financial life. They go beyond a simple pre-move comparison and become a tool for active, ongoing financial management.

- Best For: Expats, remote workers, or anyone managing assets in multiple currencies who needs to see their total financial picture.

- Strengths: It can sync bank accounts, investments, and property from over 30 countries, tracks your net worth in real time, and gives you a clear dashboard for financial planning.

- Weaknesses: It’s more of a comprehensive personal finance tracker than a quick, pre-move comparison calculator.

By combining the strengths of these tools—Numbeo for the nitty-gritty costs, the Big Mac Index for a quick reality check, and PopaDex for managing the whole picture—you build a powerful decision-making toolkit. This layered approach helps you not only make a smart choice today but also stay in firm control of your finances long after you’ve settled in.

Making Your Global Move with Financial Confidence

Taking your career international is one of the most exciting things you can do, but let’s be honest—the financial side can feel a little daunting. As we’ve walked through, figuring out a salary conversion by country goes way beyond a quick Google search for the exchange rate. It’s about understanding what a number on paper actually means for your day-to-day life.

We started with the basics, seeing how simple currency exchanges can be misleading. Then, we dove deeper into the real-world clarity that concepts like Purchasing Power Parity provide. You’ve seen how easily hidden costs, like local taxes and wildly different housing markets, can completely change your budget. Each piece of the puzzle gets you closer to a true picture of your financial life abroad.

Armed with this knowledge, you’re not just looking at a job offer anymore; you’re evaluating a life offer. You can now step into negotiations with confidence, ask the smart questions, and build a budget that makes your big move a huge win, not a financial headache.

Planning Your Financial Future Abroad

To really feel secure in your decision, you have to look beyond the salary and start understanding the complete cost of relocating internationally. Thinking about the one-time moving expenses alongside your new monthly budget is key to getting started on the right foot.

Ultimately, getting salary conversion right is more than a math problem—it’s your strategic edge. It allows you to build a successful, sustainable global career with your eyes wide open, ready for whatever comes next.

As you plan your next steps, putting together a solid financial roadmap is non-negotiable. Our guide on expat financial planning offers a great framework for managing your money across borders, making sure your financial well-being is just as strong as your new career.

Frequently Asked Questions

Thinking about working abroad brings up a ton of questions, especially around money. Let’s break down some of the most common ones with straightforward, practical answers.

What Is the Biggest Mistake When Comparing Salaries?

The single biggest mistake is looking at the direct currency exchange rate and calling it a day. It’s a classic trap. This simple math completely ignores how much your money will actually buy you in a new place.

For example, a high salary in Zurich might sound amazing, but it could easily give you a lower standard of living than a smaller paycheck in Valencia once you account for rent, groceries, and daily expenses. You absolutely have to look at purchasing power parity (PPP) or a cost-of-living index to get a true picture.

How Do Companies Calculate Expat Pay?

Big international companies often use what’s called a “balance sheet” approach for employees they send abroad. The idea is to keep your financial life whole, as if you’d never left home.

They start with your home-country salary and then add a series of adjustments to make it work in the new location.

- Cost-of-Living Adjustment (COLA): This bridges the gap if daily life is more expensive.

- Housing Allowance: A specific amount to cover reasonable accommodation costs.

- Tax Equalization: This ensures you don’t pay more (or less) in taxes than you would have at home.

- Mobility or Hardship Premium: Sometimes, an extra incentive is added for the trouble of moving or for heading to a particularly challenging location.

The Bottom Line: The goal goes beyond converting your old salary into a new currency. It’s to protect your purchasing power and ensure you can maintain your standard of living. Knowing this is a huge advantage when you negotiate.

Should I Negotiate Based on Local Rates or My Old Salary?

This is a great question. You need to know both, but you should always negotiate based on the local market rate for your specific role and experience.

Your old salary is just a personal benchmark; it has little to do with what a company in a new country is willing to pay. Walking into a negotiation armed with data on local salaries puts you in a much stronger position. A good strategy is to aim for the higher end of the local salary range to give yourself a cushion for all the unknowns that come with a big move.

Ready to stop guessing and get a crystal-clear view of your finances across borders? You can track your net worth, manage accounts in different currencies, and plan your next global move with total confidence. Start your free trial with PopaDex today and finally see your entire financial world in one place. Get started with PopaDex.

Now You Know Your Pay — Are You Building Wealth?

Salary is what you earn. Net worth is what you keep. Track whether your income is actually building wealth — connect your accounts in under 2 minutes with PopaDex.

Now You Know Your Pay — Are You Building Wealth?

Salary is what you earn. Net worth is what you keep. Track whether your income is actually building wealth — connect your accounts in under 2 minutes with PopaDex.