Our Marketing Team at PopaDex

Understanding Tax Brackets A Guide for Investors and Expats

Don’t let tax brackets scare you. The single most important thing to know is this: only the money you earn within a specific income range gets taxed at that range’s rate.

It’s one of the biggest myths in personal finance that getting a pay raise will somehow hurt you by pushing all your income into a higher tax bracket. It just doesn’t work that way. A better way to think about it is like filling a series of buckets—each bucket has to be filled to the brim and taxed before any money spills over into the next, higher-taxed bucket.

What Are Tax Brackets Really?

At its core, understanding how tax brackets work is a fundamental piece of financial literacy basics that everyone should get comfortable with. They’re the building blocks of a progressive tax system, which is just a fancy way of saying that people who earn more pay a higher percentage of their income in taxes.

Instead of one flat tax rate hitting every dollar you make, your income gets sliced into different portions. Each portion, or “bracket,” is taxed at a progressively higher rate.

This tiered approach is designed to be fair:

- Lower earners end up paying a much smaller percentage of their total income in taxes.

- Higher earners contribute a larger percentage, but crucially, only on the income that actually falls into those top-tier brackets.

This structure isn’t just a local quirk; it’s the global standard for building more equitable tax policies. Of course, some countries take this principle to the extreme. In Denmark, for example, the top marginal personal income tax rate can hit 55.9% when you combine national and local taxes. You can get a better sense of how different countries stack up over at World Population Review.

Before we dive deeper, let’s get our terms straight. These are the concepts we’ll be using throughout this guide, so it helps to have a quick reference.

Quick Guide to Tax Bracket Terminology

| Term | Simple Explanation |

|---|---|

| Tax Brackets | Different income ranges, each taxed at a specific rate. |

| Progressive Tax System | A system where tax rates increase as income increases. |

| Marginal Tax Rate | The tax rate you pay on your next dollar of income. It’s the rate of your highest tax bracket. |

| Effective Tax Rate | Your average tax rate, calculated by dividing your total tax paid by your total taxable income. |

| Taxable Income | The portion of your gross income that is actually subject to tax after deductions and exemptions. |

Getting these definitions down will make the rest of our examples and strategies much easier to follow.

The key takeaway is simple: You are never punished for earning more money. Each extra dollar you earn is taxed at the rate for its specific bracket, while all the money you earned before it stays locked in at the lower rates of the previous brackets.

Once you truly grasp this progressive structure, you’re on your way to smarter financial planning. It helps you anticipate your tax bill and make better decisions with your money, whether you’re saving for retirement, managing investments, or navigating the complexities of multi-currency income as an expat.

Marginal vs. Effective Tax Rate: What You Actually Pay

When you stare at a tax chart, it’s easy to fixate on the highest percentage your income falls into. That big number is your marginal tax rate, and it’s probably the most misunderstood concept in personal finance. Here’s the good news: it’s the rate you pay on your next dollar earned, not on your entire salary.

Grasping this one distinction is the key to conquering any fear you have about earning more money.

There’s a persistent myth that getting a raise can somehow push you into a higher bracket and leave you with less money. That’s just not how it works. Our progressive tax system is designed to prevent that from ever happening. Think of it like filling buckets with water—you have to fill the first, smaller bucket completely before any water spills over into the next, larger one.

Your Marginal Tax Rate Explained

Your marginal rate is just the tax percentage applied to the very last chunk of your income. For instance, if you’re a single filer and your taxable income lands you in the 24% bracket, only the dollars you earn within that specific bracket get taxed at 24%.

Every single dollar you earned before hitting that bracket is still taxed at the lower rates of 10%, 12%, and 22%. A bonus or a raise gets taxed at your highest marginal rate, but it never, ever goes back in time to increase the tax on the money you already made in the lower brackets.

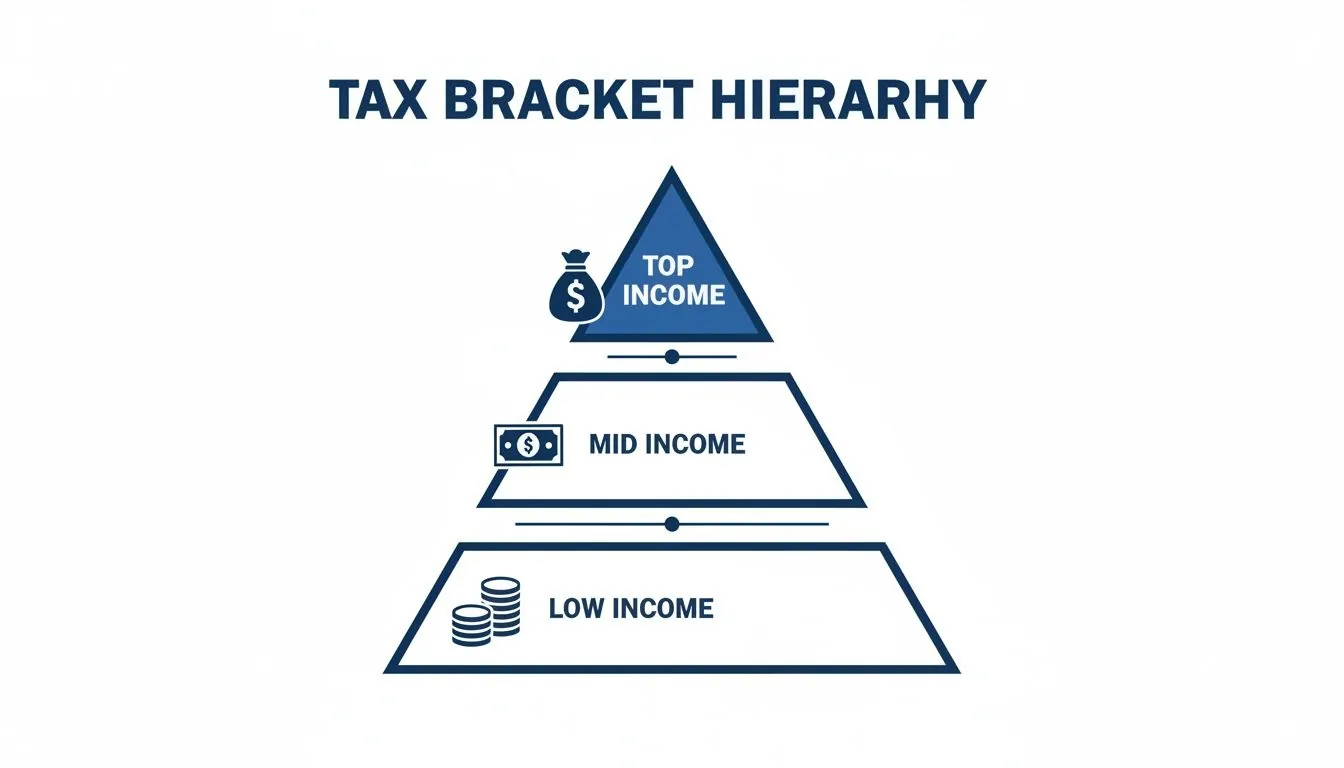

This is why you’ll often see income tax visualized as a pyramid.

As you can see, only the very peak of your income is hit with the highest rates. The foundation of your earnings always benefits from the lower rates at the bottom.

Calculating Your Effective Tax Rate

While the marginal rate is useful for planning your next financial move, your effective tax rate tells the real story of what you’re paying. This is your total tax bill divided by your total taxable income, giving you the true average rate you paid across all the brackets.

Your effective tax rate will always be lower than your marginal tax rate (unless you’re in the very bottom bracket). Think of it as your personal, blended tax rate—it’s the real measure of your tax burden.

Let’s walk through a quick example. Imagine a single filer with $60,000 in taxable income. Their marginal tax rate is 22%, but their actual tax bill isn’t anywhere near 22% of $60,000.

Here’s how the math really works:

- The first slice of their income is taxed at 10%.

- The next chunk is taxed at 12%.

- Only the final amount that falls into the 22% bracket is taxed at that rate.

After adding up the tax owed from each of those brackets, the total tax bill comes out to around $8,680. Now, to find the effective rate, we just do some simple division:

$8,680 (Total Tax) ÷ $60,000 (Total Income) = 14.5%

So, even though this person is “in” the 22% bracket, their actual, blended tax rate is a much more manageable 14.5%. This is a game-changer. It proves that earning more money always means more take-home pay, making that promotion or side hustle a clear financial win.

How Tax Brackets Work in the Real World

Theory is a good place to start, but tax brackets don’t really click until you see them play out in real life. Everyone’s financial situation is different, and seeing how various income structures get taxed shows you just how logical a progressive system can be. Let’s move from abstract concepts to concrete examples.

We’ll walk through three common scenarios: a professional with a steady paycheck, a freelancer with less predictable income, and an expat juggling multiple currencies. Each one breaks down the tax math step-by-step, showing exactly how the final tax bill and effective tax rate are figured out.

Think of these as frameworks you can adapt to your own financial life, no matter how simple or complex it might feel.

Example 1: The Salaried Professional

Let’s start with Alex, a young professional with a stable job. After accounting for all deductions, Alex’s taxable income for the year is $75,000. We can use a simplified tax structure to see how this income is taxed piece by piece as it fills up each bracket.

Here’s a look at how the calculation works. Notice how only the income within each bracket is taxed at that specific rate.

Sample Tax Calculation for a Single Filer

| Income Range (Tax Bracket) | Tax Rate | Income in this Bracket | Tax Owed |

|---|---|---|---|

| $0 – $12,000 | 10% | $12,000 | $1,200 |

| $12,001 – $48,000 | 12% | $36,000 | $4,320 |

| $48,001 – $95,000 | 22% | $27,000 | $5,940 |

| Total | $75,000 | $11,460 |

Alex’s total tax bill comes out to $11,460. To find the effective tax rate—the actual percentage of income paid in taxes—we just divide the total tax by the total taxable income: $11,460 ÷ $75,000 = 15.3%.

Even though Alex’s income spills into the 22% bracket, the actual tax hit is much lower. This is the magic of marginal rates.

Example 2: The Freelancer with Variable Income

Next up is Maya, a freelancer whose income isn’t quite as predictable. This year, her taxable income is $90,000. The calculation is similar to Alex’s, but the real difference for Maya is in the planning.

Since she doesn’t have an employer withholding taxes from each paycheck, the responsibility is all hers. She has to proactively set aside money to make quarterly estimated tax payments throughout the year.

For freelancers like Maya, managing cash flow is everything. It’s on her to avoid underpayment penalties, which makes tools like PopaDex incredibly useful for tracking income streams and estimating tax liabilities on the fly.

Example 3: The Expat Earning Abroad

Finally, let’s look at Liam, an expat working in Japan. This is where things get more complex, with foreign exchange rates and international tax treaties coming into play. Looking at a country’s top tax rate can be seriously misleading if you don’t have the full picture.

For instance, Japan’s national income tax has a top rate of 45%. But that’s not the whole story. Local inhabitant taxes tack on another 10%, pushing the combined peak marginal rate to nearly 56% for 2025.

But here’s the thing: those highest rates only kick in for income above ¥40 million (around $267,000 USD). After factoring in deductions, only a tiny fraction of taxpayers ever see that rate. It just goes to show how critical it is to look beyond the headline numbers.

Liam has to navigate the tax laws of his home country and Japan. He’d likely use things like the Foreign Tax Credit to avoid being taxed twice on the same income. Understanding how these international agreements and local tax systems work together is non-negotiable for any expat’s financial plan. You can explore how tax rates compare across different countries to see just how much things vary.

Common Misconceptions That Cost You Money

Misinformation about taxes can lead to some truly baffling financial decisions, like being afraid of a raise or turning down a side hustle. It sounds crazy, but it happens. If you’re serious about building wealth, you need to see these myths for what they are.

Let’s clear the air and tackle the most common—and costly—misunderstandings head-on.

The biggest myth, by a long shot, is the idea that a pay increase could somehow leave you with less take-home pay. This is completely, 100% false. The fear is that earning just one dollar more pushes your entire income into a higher tax bracket, where it all gets taxed at that new, higher rate.

Thankfully, our progressive tax system doesn’t work like that at all. As we’ve seen, only the dollars you earn within that new, higher bracket are taxed at that rate. Every dollar you earned before that point is still taxed at the lower rates from the brackets below it. You will always take home more money after earning more. Full stop.

Myth One: My Bracket Is My Tax Rate

Another frequent point of confusion is looking at your top tax bracket and thinking that’s your actual tax bill. If you find yourself in the 24% bracket, it absolutely does not mean you’re handing over 24% of your total income to the government. That number only applies to your last, highest dollars earned.

The number you should actually care about is your effective tax rate—your total tax paid divided by your total income. This is the true measure of your tax burden, and it will almost always be significantly lower than your top marginal rate. Believing this myth causes people to dramatically overestimate what they owe.

Myth Two: Tax Brackets Are Static

Lots of people just assume tax brackets are set in stone. The truth is, they change almost every year to keep up with inflation, a process called indexing. Without it, even a small cost-of-living raise could bump you into a higher bracket, hiking your tax bill without any real increase in your buying power.

This quiet, inflation-driven tax increase has a name: “bracket creep.” It’s a stealthy force that can eat away at your wealth over time if you’re not paying attention to the annual adjustments made by tax authorities.

Staying on top of these yearly changes is a non-negotiable part of smart financial planning. It ensures your strategies for saving and investing are based on today’s reality, not on last year’s outdated figures. Making decisions with incomplete information is a surefire way to hurt your own bottom line.

Using Tax Brackets for Strategic Financial Planning

Understanding tax brackets is one thing. Actually using that knowledge to build wealth is where the real magic happens. Once you have a firm grasp of how your income is taxed, you can start making proactive decisions that lower your tax bill and free up more money to save, invest, and grow.

This isn’t about shady loopholes or complex schemes. It’s about using the tax code as it was designed to maximize your financial potential. This approach turns tax season from a reactive chore into a forward-looking opportunity to boost your financial health.

Strategies for Investors and Savers

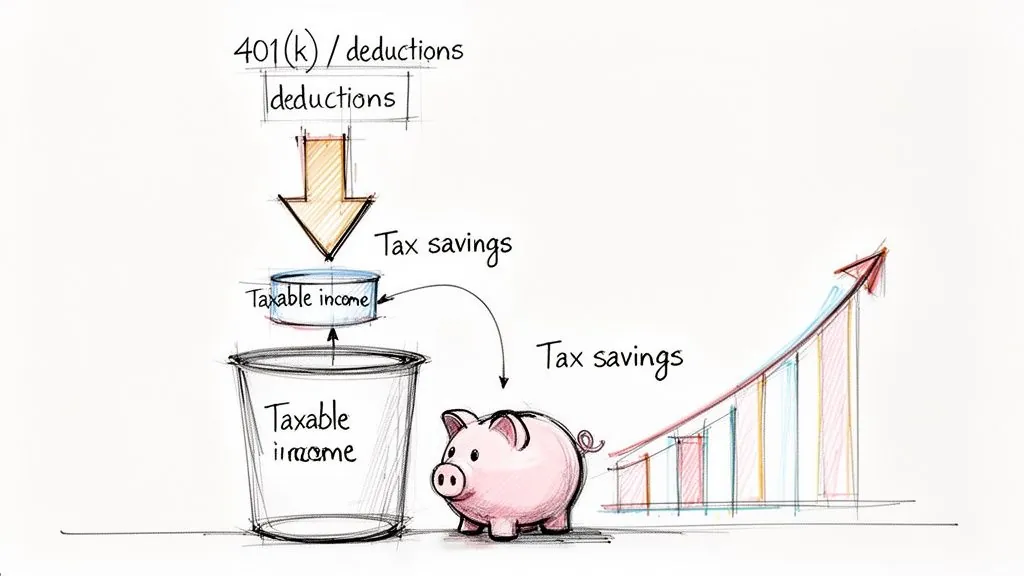

For investors, the most powerful tool in the shed is the tax-advantaged retirement account. Contributions to accounts like a traditional 401(k) or IRA are often tax-deductible, which is just a fancy way of saying they reduce your taxable income for the year. This one simple action can sometimes be enough to keep a chunk of your earnings from spilling into a higher tax bracket.

Let’s say you’re right on the edge of the 24% bracket. By maxing out your 401(k) contribution, you could lower your taxable income enough to stay comfortably in the 22% bracket. You save money on taxes now while building your nest egg for the future. It’s a classic win-win.

The goal is simple: pay tax on as little of your top-earning dollars as possible. Every dollar you put into a retirement account is a dollar that isn’t taxed at your highest marginal rate today. Instead, it gets to work for you, growing tax-deferred until you need it in retirement.

Planning for the Self-Employed and Expats

If you’re self-employed, think of your business deductions as your best friend. Every legitimate business expense you claim—from your home office to software subscriptions—reduces your net business income. This directly lowers your taxable income and gives you a surprising amount of control over which tax brackets your earnings fall into.

For expats, the game is all about avoiding double taxation. Getting familiar with tools like the Foreign Tax Credit or the Foreign Earned Income Exclusion is non-negotiable. These provisions are designed to prevent you from paying tax to two different countries on the very same income, which protects your hard-earned money. Navigating tax treaties and local rules is just part of the playbook for a financially savvy expat.

Keeping an Eye on Global Changes

Tax laws aren’t set in stone. They shift with economic policy and new government priorities. For anyone trying to optimize their finances, paying attention to broader policy shifts like Trump’s ‘Big Beautiful’ Tax Bill is crucial for long-term planning.

These changes reveal how governments are constantly trying to balance revenue with economic growth. Just look at the 2025 global updates: Cuba hiked its top rate from 20% to a staggering 50%, while India simplified its system with a flat 30% rate above ₹15 lakh—a choice now made by 70 million filers. Staying aware of these shifts helps you avoid nasty surprises, like the UK’s 60% ‘fiscal cliff’ at £100,000 where personal allowances start to disappear.

Ultimately, weaving this knowledge into your bigger financial picture is the final, most important step. When you actively manage your income and deductions, you transform from a passive taxpayer into the architect of your financial future—a core principle we dive into in our guide on creating a financial plan.

Weaving Tax Awareness into Your Financial Health

Most people treat taxes like an annual chore, a mad scramble every April. But what if you viewed it differently? The smartest financial operators connect their tax planning with their everyday finances, turning a yearly headache into a source of ongoing insight.

When you start estimating your after-tax income each month, you get a much clearer picture of your actual spending power. This isn’t just an academic exercise; it’s about grounding your financial reality. Integrating that after-tax figure into your budget gives you a more accurate forecast for savings and cash flow.

Estimate Your After-Tax Cash Flow

Think of it as giving yourself an honest paycheck. It’s pretty straightforward:

- Start with your gross income and subtract your projected taxes to find your net income.

- Use a simple formula or a tool like PopaDex with custom fields to automatically set aside a percentage for taxes.

- Keep an eye on transaction updates to see how your real take-home pay shifts.

Once you’ve got that down, the next step is to see how different tax strategies actually affect what lands in your bank account.

The screenshot below from a PopaDex dashboard shows exactly this—tracking post-tax income trends over time. This kind of view instantly highlights how moves like upping your retirement contributions impact your immediate cash flow.

Track Your Tax-Saving Strategies in Real Time

This is where the magic happens. Instead of waiting until tax season, you can monitor the impact of your decisions as you make them.

- Keep a running tally of your retirement contributions and see your taxable income drop.

- If you’re self-employed, log business expenses on the go so nothing gets missed.

- Set custom alerts to notify you if your effective tax rate creeps past a certain threshold.

Consistent tracking transforms tax planning from a reactive scramble into a proactive financial tool.

These small, practical actions are what keep you on track. For instance, bumping up your 401(k) contribution by just 2% could lower your taxable income by a surprising amount each month. Logging every single deductible expense as it happens means no more frantic searches for receipts in April.

And for those of us with international finances, staying on top of reporting is non-negotiable. If you hold assets abroad, make sure you understand your obligations by reading our guide on foreign asset reporting requirements. Similarly, for businesses with a global footprint, knowing the rules for things like corporate tax filing in the UAE is a critical piece of the puzzle.

Finally, pull it all together by integrating your after-tax estimates into your net worth calculations. This is how you see the direct link between smart tax savings and accelerating your wealth. PopaDex’s net worth tracker even auto-updates asset values in over 30 currencies, keeping your global portfolio perfectly in sync.

By building these tax insights right into your financial dashboards, you turn raw numbers into strategic decisions. You’re no longer just tracking money—you’re guiding it.

Got Questions About Tax Brackets? We’ve Got Answers.

Even after you get the hang of how tax brackets work, a few common questions always seem to pop up. Let’s dig into some of the things people often ask once they start putting this knowledge to use.

How Do Deductions and Credits Fit into All This?

This is a fantastic question because they work in completely different ways, and one is way more powerful than the other.

Think of tax deductions (like contributing to a traditional IRA or 401k) as a way to shrink your taxable income before the IRS even starts its calculation. Deductions lower the total amount of income that’s subject to tax in the first place. Sometimes, this is enough to bump your highest-earning dollars down into a lower tax bracket, which is a nice win.

Tax credits, on the other hand, are the real superstars. A tax credit reduces your final tax bill dollar-for-dollar after everything has been calculated. Credits don’t mess with your bracket at all—they just directly slash the amount of cash you actually have to send to the government.

Do My State and City Have Tax Brackets, Too?

Yep, most likely. The federal system is just one piece of the puzzle. Most U.S. states with an income tax have their own progressive tax bracket systems, which are totally separate from the federal ones. A few states keep it simple with a single flat tax rate, and a lucky few have no state income tax at all.

It’s absolutely essential to get familiar with your specific state and local tax laws. These rates and brackets can take a big bite out of your income and have a major impact on your overall tax burden.

What’s the Difference Between Filing Status and a Tax Bracket?

Your filing status is what you tell the IRS about your household situation—are you Single, Married Filing Jointly, Head of Household, etc.? This choice is the very first step, and it determines which set of tax brackets you’ll use.

Each filing status has its own unique income ranges for every tax rate. Your tax bracket is simply the specific income tier your earnings fall into within the set of rules defined by your filing status. So, you pick your filing status first, and that tells you which playbook of brackets to follow.

Ready to stop guessing and see your true after-tax income and net worth? PopaDex connects all your accounts to give you a clear, real-time picture of your entire financial world. Take control of your finances today at https://popadex.com.