Our Marketing Team at PopaDex

What Is Financial Consolidation A Complete Guide

If you’ve ever tried to figure out your total financial picture by looking at a dozen different bank, investment, and credit card statements, you already understand the chaos that financial consolidation aims to solve.

Simply put, it’s the process of pulling together financial data from all your different sources into one single, clear report. Think of it like assembling a puzzle. Each account is a separate piece, but only when you put them all together do you see the complete picture of your financial health.

Understanding Financial Consolidation in Simple Terms

At its heart, financial consolidation is about moving from a fragmented view to a holistic one. For a massive company like Apple, this means rolling up the financial statements from every single one of its global subsidiaries into one master report. For you, it means gathering the numbers from your checking account, your 401(k), your brokerage app, and your mortgage statement to get a real, honest look at your net worth.

The goal is always the same: clarity and accuracy.

Without it, a business can’t steer the ship properly, and an individual is just guessing about their financial future. This goes beyond adding up numbers, though. It’s a bit more sophisticated than that. In the corporate world, for instance, a crucial step is canceling out transactions between a parent company and its subsidiary. Why? To avoid counting the same money twice and inflating the numbers.

Corporate vs Personal Consolidation

While the core idea of getting a single financial view is universal, how it’s done for a multinational corporation versus an individual couldn’t be more different.

Corporate consolidation is a highly structured, heavily regulated process, dictated by accounting standards like GAAP or IFRS. It’s not optional; it’s the law. Personal consolidation, on the other hand, is all about you. It’s a flexible, private practice focused entirely on your own wealth management and life goals. Grasping this distinction is the first step to seeing how powerful this concept can be for your own finances.

Corporate vs Personal Financial Consolidation At a Glance

To really spell it out, let’s put the two side-by-side. The table below breaks down the key differences in goals, components, and complexity.

| Aspect | Corporate Financial Consolidation | Personal Financial Consolidation |

|---|---|---|

| Primary Goal | Provide a holistic view of the entire group’s financial performance for stakeholders (investors, regulators). | Calculate personal net worth, track financial goals, and inform budgeting and investment decisions. |

| Key Components | Balance sheets, income statements, and cash flow statements from all parent and subsidiary companies. | Bank accounts, investment portfolios, retirement accounts, real estate, credit card debt, mortgages, and other loans. |

| Complexity | High. Involves complex accounting rules, intercompany eliminations, multi-currency translations, and goodwill calculations. | Low to medium. Primarily involves aggregating data from various accounts and platforms. You can learn more about how this works in our guide to financial data aggregation. |

| Regulation | Strictly regulated by accounting standards (e.g., GAAP, IFRS) and requires formal audits. | Unregulated and for personal use. The “rules” are set by the individual based on their own goals. |

As you can see, the corporate world operates on a completely different level of complexity and regulatory pressure.

The tools used also reflect this divide. For big companies, the stakes are high, and efficiency is paramount. A recent 2025 BARC survey found that 51% of companies are now using cloud-based software for their formal consolidation needs, chasing the dream of real-time, accurate data. For individuals, the tools are much more personal, focused on empowerment rather than compliance.

The Corporate Consolidation Playbook

Ever look at a corporate giant like Alphabet Inc. and wonder how it all works? You’re not just seeing one company. You’re looking at a massive family of them—Google, YouTube, Waymo, and dozens more—all operating under a single roof. Corporate financial consolidation is the formal accounting process that takes the financial stories of all these individual businesses and weaves them into one cohesive report.

This goes beyond adding up numbers. It’s a highly disciplined process designed to give investors, regulators, and the public a true and fair view of the entire group’s financial health. The goal is to strip away all the internal noise—the transactions between companies in the group—so you only see how the conglomerate as a whole is performing in the outside world.

To really get it, you first have to understand the various business structure types that make up these corporate families. The real complexity kicks in when these legally separate companies start doing business with each other, creating a tangled web of internal activity that needs to be sorted out.

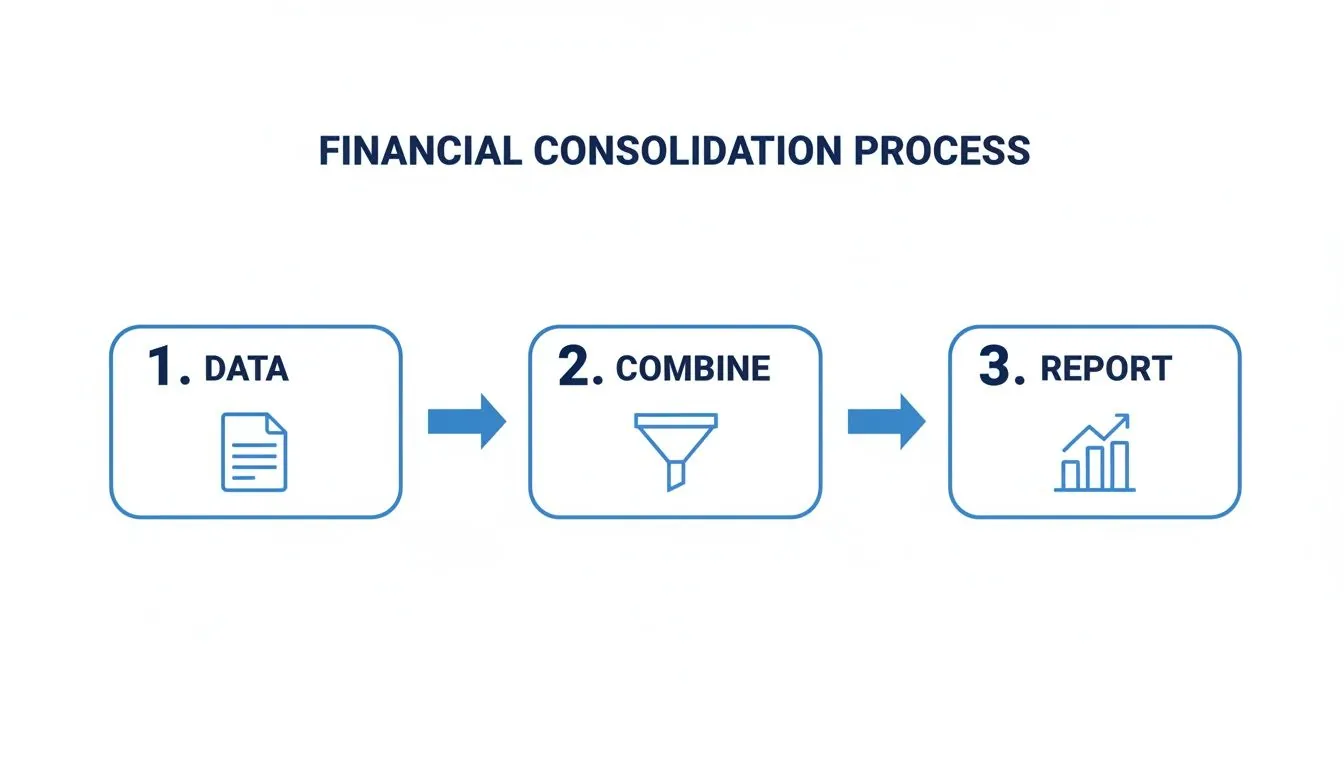

The Core Steps of Corporate Consolidation

Turning raw data from dozens of sources into a single, auditable financial statement is a step-by-step affair. While the nitty-gritty can get incredibly complex, the fundamental workflow is logical and built entirely around accuracy and transparency.

The flowchart below breaks down the three main phases of the journey, from gathering the initial data to producing the final, unified report.

Think of it like a funnel. You start with a mess of disorganized data at the top, which gets collected, standardized, and refined until a clear, singular report emerges at the bottom.

Here’s what that journey actually involves:

- Data Collection and Standardization: First things first, accountants have to gather financial statements from every single subsidiary. This data then has to be standardized, meaning it’s converted into a common chart of accounts. For multinational companies, this also means translating everything into a single reporting currency.

- Intercompany Eliminations: This is arguably the most critical piece of the puzzle. Any and all transactions between subsidiaries must be found and canceled out. For example, if one subsidiary sells $1 million in goods to another, that sale has to be eliminated. Otherwise, it would look like the group made a sale to an external customer when, in reality, the money just moved from one corporate pocket to another.

- Adjustments and Aggregation: Finally, accountants make necessary adjustments for complex items like goodwill (the premium paid for a subsidiary over its book value) and minority interest (the portion of a subsidiary not owned by the parent company). With all the adjustments made, the numbers are aggregated into the master consolidated financial statements.

The entire point of consolidation is to present the parent company and its subsidiaries as if they were a single economic entity. You’re aiming to show only the transactions that happened with the outside world.

Key Consolidation Methods Explained

Not all subsidiaries get treated the same. The accounting method used hinges entirely on how much control the parent company actually has.

- Full Consolidation: This is the go-to method when the parent company owns more than 50% of a subsidiary, giving it clear control. In this case, 100% of the subsidiary’s assets, liabilities, revenues, and expenses are rolled up into the parent’s financials.

- Equity Method: This method comes into play when ownership is significant but not controlling—typically between 20-50%. Instead of combining every line item, the parent company simply records its share of the subsidiary’s profit or loss as a single line on its own income statement.

- Cost Method: Used for smaller investments where the parent has very little influence (usually less than 20% ownership). Here, the investment is just recorded at its original purchase price. It’s only adjusted if dividends are paid out or if the investment’s value is impaired.

These different methods ensure the final consolidated report accurately reflects the parent company’s real-world economic influence over its various investments. As you can imagine, getting this right is a massive job, which is why large organizations rely on powerful financial data integration strategies and specialized software to close their books accurately and on schedule.

Why Financial Consolidation Is a Strategic Power Move

Let’s be clear: financial consolidation is more than a box-ticking exercise for the accounting team. It’s a powerful strategic tool that gives leaders the clarity they need to manage a business intelligently. When you truly grasp your company’s complete financial picture, you stop putting out fires and start building for the future.

For anyone on the outside—investors, regulators, partners—consolidated statements are a window into the soul of the company. They provide a transparent, holistic view of an organization’s health and how well it’s being run. This unified picture prevents the kind of financial games where losses get tucked away in an obscure subsidiary. What you see is what you get.

This bird’s-eye view is absolutely essential for a company’s leadership. A CEO or CFO working with a consolidated report can make far smarter decisions. They can see exactly which parts of the business are firing on all cylinders and which are lagging, allowing them to allocate resources with precision and drive targeted improvements.

Enhancing Transparency and Building Trust

One of the biggest wins from a solid consolidation process is the trust it builds. When a company presents a single, audited set of financial statements, it sends a powerful message of accountability. This goes beyond playing by the rules; it’s about showing a real commitment to honest reporting.

A consolidated financial statement is the ultimate “single source of truth.” It reassures investors, lenders, and partners that the company’s reported health isn’t an illusion created by shuffling money between different legal entities.

While this level of transparency is non-negotiable for public companies, it’s just as valuable for private businesses. A clear, consolidated view is critical when you’re looking for investment, applying for a major loan, or planning an acquisition. It makes due diligence simpler and builds the confidence needed to get deals done.

Driving Smarter Strategic Planning

Beyond keeping outsiders happy, the real magic of consolidation is how it fuels internal strategy. Executives can’t plan for the future if they’re staring at a dozen conflicting financial reports. A unified view provides the high-level perspective needed to make the tough calls.

This leads to some key strategic advantages:

- Accurate Performance Measurement: Management can finally compare the performance of different divisions or subsidiaries on a true apples-to-apples basis.

- Informed Capital Allocation: Leaders can spot which business units are generating the best return on investment, helping them decide where to inject capital for maximum growth.

- Early Risk Detection: A consolidated view can expose financial risks—like being too dependent on one subsidiary or currency—that are easy to miss when looking at each entity on its own.

Look at the banking sector, for example. Consolidation is often the endgame for mergers and acquisitions (M&A). But that activity has slowed to a crawl, with non-crisis M&A volume in the US banking sector falling to less than 50% of post-Global Financial Crisis averages, thanks in part to a tough regulatory environment. Even so, the strategic push to consolidate continues, fueled by things like a 65% spike in tech spending over the last 15 years. You can dig deeper into these US bank consolidation trends from Oliver Wyman.

Streamlining Regulatory Compliance

Finally, let’s not forget the basics: consolidation is a must-have for regulatory compliance. Standards like GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) require it for any company with a controlling stake in another business.

Sticking to these standards is about more than just avoiding fines. It ensures a company’s financial data is comparable to its peers, which is vital for benchmarking and market analysis. Modern consolidation software makes this whole process more efficient, cutting down on the risk of human error and ensuring reports get filed correctly and on time. That frees up the finance team to focus on actual strategy instead of getting lost in manual data entry.

A Practical Guide to Personal Financial Consolidation

Let’s bring the concept of financial consolidation out of the corporate boardroom and onto your kitchen table. This is more than some high-finance strategy for multinational companies; it’s a powerful tool for anyone who’s serious about building wealth. Think of it as creating your own personal “annual report”—a single, clear snapshot of your entire financial life.

Imagine trying to figure out your overall health by looking at a dozen different lab results, doctor’s notes, and fitness app readouts scattered across your desk. It’s confusing, and you’d never see the whole picture. The same goes for your money. Personal consolidation pulls everything into one dashboard: your checking and savings, your 401(k), investment portfolios, credit card balances, mortgage, and car loans.

The goal is simple: financial clarity. When you can see every asset and every liability in one place, you finally have the power to make genuinely smart decisions. This goes beyond satisfying your curiosity; it’s about turning a bunch of abstract numbers into a real, actionable plan for your life.

Building Your Personal Balance Sheet

The first step is to create a personal balance sheet. Don’t let the term intimidate you. It’s just a straightforward way of listing what you own (assets) and what you owe (liabilities). The difference between the two is your net worth, the truest measure of your financial health.

Step 1: List All Your Assets Time to gather up your statements and log into your accounts. Be thorough and sort everything into a few key buckets.

- Cash and Equivalents: This is your liquid money—everything in your checking accounts, savings accounts, and any certificates of deposit (CDs).

- Investments: Jot down the current market value of your retirement accounts (like a 401(k) or IRA), brokerage accounts, and anything else you’ve invested in.

- Physical Assets: Estimate the fair market value of your home, any investment properties you own, and your vehicles.

Step 2: Tally All Your Liabilities Next up, it’s time to look at the other side of the coin. List every single debt you’re carrying.

- Secured Debt: This covers your mortgage balance and any outstanding car loans—debts tied to a physical asset.

- Unsecured Debt: Now, add up all your credit card balances, student loans, and any personal loans you might have.

Once you have these two lists, the math is easy: Assets - Liabilities = Net Worth. This one number tells you exactly where you stand.

A consolidated view of your finances is like turning on the lights in a dark room. Suddenly, you can see where you are, where the obstacles are, and the clearest path forward to your goals.

From Manual Tracking to Automated Insight

When you’re starting out, a simple spreadsheet can get the job done. But as your financial world gets more complex, manually updating everything becomes a real chore, and it’s easy to make mistakes. This is where modern tools can really change the game.

Platforms like PopaDex were built for this exact purpose. They automate the entire process by securely connecting to your various bank and investment accounts, giving you a real-time, dynamic view of your net worth. What was once a static, once-a-year calculation becomes a living, breathing dashboard.

With this consolidated view, you can suddenly:

- Track Net Worth Over Time: There’s nothing more motivating than watching your wealth grow month by month.

- Identify Spending Leaks: A unified view often shines a light on things like redundant subscriptions or high-interest debt that’s quietly draining your resources. Our guide on how to consolidate bank accounts has some great strategies for this.

- Optimize Debt Repayment: Seeing all your debts together helps you decide which ones to attack first, whether you use the avalanche or snowball method. For homeowners, understanding the benefits of refinancing your home loan can be a huge part of this strategy.

Ultimately, personal financial consolidation puts you in the driver’s seat. It makes you the CFO of your own life, armed with the clarity you need to build a secure and prosperous future.

Financial Consolidation in the Real World

Theory is great, but seeing financial consolidation in action is where the lightbulb really goes on. Let’s step away from the definitions and dive into three relatable stories. Each one shows how bringing everything together financially solves real problems and helps people hit their goals by creating a single, clear view of their money.

The Multinational Maze: Global Tech Inc.

First up, imagine “Global Tech Inc.,” a growing company with big offices in Germany and Japan. The German team works in Euros (€), while the Japanese team uses Yen (¥). This year, the German office loaned €2 million to the Japan office to get a new product off the ground, creating what’s called an intercompany loan.

Now, Global Tech’s finance team has a couple of headaches. They have to convert all the financial reports from Euros and Yen into their main currency, US Dollars ($). But more importantly, they need to make that €2 million loan disappear during consolidation. If they don’t, the company’s books will show both an asset (the money Germany is owed) and a liability (the money Japan owes), making the company look bigger on paper than it actually is.

By performing a proper corporate consolidation, Global Tech creates one clean report that shows its true global health, without any currency weirdness or internal loans muddying the waters. This is the kind of clarity investors need to see.

This image captures the reality for so many people and businesses today—juggling different income streams and projects across the globe.

When your finances are this spread out, a consolidated view is more than a nice-to-have; it’s absolutely essential for making smart decisions and planning for the future.

The Freelancer’s Focus: Maria the Designer

Next, let’s look at Maria, a freelance graphic designer who’s killing it. Money comes in from different clients and lands in various bank accounts. She also has a brokerage account for her investments, a high-yield savings account for taxes, and a credit card just for business stuff.

For years, Maria felt like she was just guessing. She knew she was making money, but she had no real idea what her net worth was or if she was actually getting ahead. She was stuck in the weeds, looking at individual account balances instead of the big picture.

So, Maria decided to try personal financial consolidation. She used a tool to link all her accounts and built her first-ever personal balance sheet. Suddenly, she could see a clear, real-time number: her assets minus her liabilities. This unified view was an eye-opener. It showed her she was saving less than she realized and gave her the motivation to set a real goal: increase her investment contributions by 15%.

The Family’s Financial Plan: The Chen Family

Finally, meet the Chens. They have two kids getting close to college, a mortgage, and a handful of retirement accounts between them. Their financial life felt messy and complicated. They needed a single strategy to manage their budget, see if their college savings were on track, and figure out if they could pay off their mortgage faster.

Their biggest problem was a lack of coordination. Each piece of their financial puzzle was managed in a silo. It was impossible to know how one decision, like throwing extra money at the mortgage, would affect their ability to save for tuition.

The Chens decided to consolidate their finances by building a master family dashboard. This let them:

- Track their total net worth as one family unit.

- See how their 529 college savings plans were growing compared to their goals.

- Play with different mortgage payment scenarios to understand the long-term impact.

That consolidated view changed everything. Their money talks went from stressful arguments to collaborative planning sessions based on actual data.

This drive to consolidate goes beyond the personal; it’s a huge force in the business world, too, especially in fields like asset management. A deep dive into 270 asset managers revealed the average firm doubled its assets under management (AuM) over ten years, mostly through consolidation. These trends show that combining financial strength is often a key move for growth in tough markets. You can find more on these consolidation strategies from BCG.

Got Questions About Financial Consolidation? We’ve Got Answers.

Even after you get the hang of it, a few common questions always seem to surface when talking about financial consolidation. Let’s tackle them head-on to clear up any lingering confusion and make sure you’re confident in how it all works.

Consolidation vs. Aggregation: What’s the Real Difference?

This is a great question because people mix these terms up all the time, but they mean very different things. The easiest way to remember it is that aggregation is just adding things up, while consolidation is adding things up and cleaning up the results.

Imagine you’re making a smoothie. Aggregation is just throwing all your ingredients into the blender—the fruit, the yogurt, the spinach. You’ve combined them, but that’s as far as it goes. Consolidation is the entire process: adding the ingredients, blending them into one smooth mix, and maybe even straining out the raspberry seeds. It’s a more refined, complete process.

In the world of finance, it breaks down like this:

- Aggregation is what you do for your personal net worth. You’re simply adding the balances from your various bank accounts, investment portfolios, and debts.

- Consolidation is the official accounting move for businesses. It involves summing up the numbers plus making crucial adjustments, like removing transactions between a parent company and its subsidiary so nothing gets counted twice.

So, for your own finances, you’re almost always aggregating. For corporate accounting, they’re truly consolidating.

How Often Should a Business Consolidate Its Finances?

The rhythm of business consolidation is almost always locked into its reporting schedule. The right frequency really boils down to two things: what management needs to make smart decisions, and what regulators or investors require to stay compliant.

Most companies follow a pretty standard tiered schedule:

- Monthly: This is the go-to for internal review. It gives the leadership team a fresh look at performance so they can steer the ship and make quick adjustments.

- Quarterly: This is the standard for publicly traded companies. They need to report their earnings and financial health to their investors every three months.

- Annually: The big one. The annual consolidated report is the most detailed, giving shareholders, tax authorities, and regulators a complete picture of the entire year.

At the end of the day, the right cadence is whatever gives the company clear insights for strategy and meets all external demands, without completely burning out the finance team.

Can I Use a Spreadsheet for Personal Consolidation?

Absolutely! A spreadsheet is a fantastic starting point for getting a handle on your personal finances. It’s a straightforward and effective way to list out everything you own (assets) and everything you owe (liabilities) to see your net worth for the very first time.

But spreadsheets have one glaring weakness: they are 100% manual. You have to remember to log in and update every single number—your checking account, your 401(k) balance, your credit card debt—every single time you want an accurate snapshot. As you add more accounts and investments, this gets old fast and becomes a breeding ground for typos and errors.

This is exactly where dedicated financial apps come in. They do the heavy lifting for you by automatically pulling in the data, giving you a real-time, accurate picture of your financial health without all the manual data entry. You get a much more dynamic and timely view of your progress, minus the headache and risk of human error.

Ready to graduate from manual spreadsheets and get a live, automated view of your entire financial world? PopaDex securely connects all your accounts in one place, giving you the clarity you need to build wealth with confidence. Start tracking your net worth for free today.