Our Marketing Team at PopaDex

What is personal financial statement: How to create and use it

Ever wonder what your entire financial life looks like on a single page? That’s exactly what a personal financial statement does. Forget complex accounting ledgers; think of it as your financial report card, giving you a crystal-clear snapshot of where you stand by listing everything you own (assets) and everything you owe (liabilities).

Your Financial Health on a Single Page

A personal financial statement is the ultimate tool for financial clarity. It’s the essential first move for anyone serious about their money, whether you’re trying to get a loan, mapping out retirement, or just want to finally get a handle on your financial situation. It answers one simple but incredibly powerful question: What is my net worth right now?

By subtracting what you owe from what you own, you get this crucial number. This single figure is your scoreboard—it tracks your progress, flags potential risks, and gives you a solid baseline for setting goals that actually mean something.

The Foundation of Financial Planning

Knowing where you stand financially is the bedrock of every smart money decision. A well-prepared statement helps you:

- Track Your Progress: See how your net worth grows (or shrinks) year after year.

- Spot Strengths and Weaknesses: Pinpoint where you might have too much debt or not enough cash on hand.

- Make Confident Decisions: Decide with clarity if you can really afford that big purchase or jump on a new investment opportunity.

These statements aren’t a new concept. They became vital back in the early 20th century as consumer credit took off and banks needed a reliable way to vet loan applicants. Their importance has only skyrocketed since. Today, the hunger for tools to track net worth is fueling massive growth in the personal finance app market, which hit USD 101.75 billion in 2023 and is projected to explode to USD 675.08 billion by 2032. You can read more about this explosive growth and its drivers.

In a nutshell, a personal financial statement turns a mountain of complex financial data into a single, understandable story. It shifts your focus from just paying monthly bills to strategically building wealth for the long haul.

Once you demystify this document, you’re armed with one of the most powerful tools for financial control. It’s not just about numbers on a page; it’s about gaining the insight you need to build the financial future you want, with purpose and confidence.

Understanding Assets, Liabilities, and Net Worth

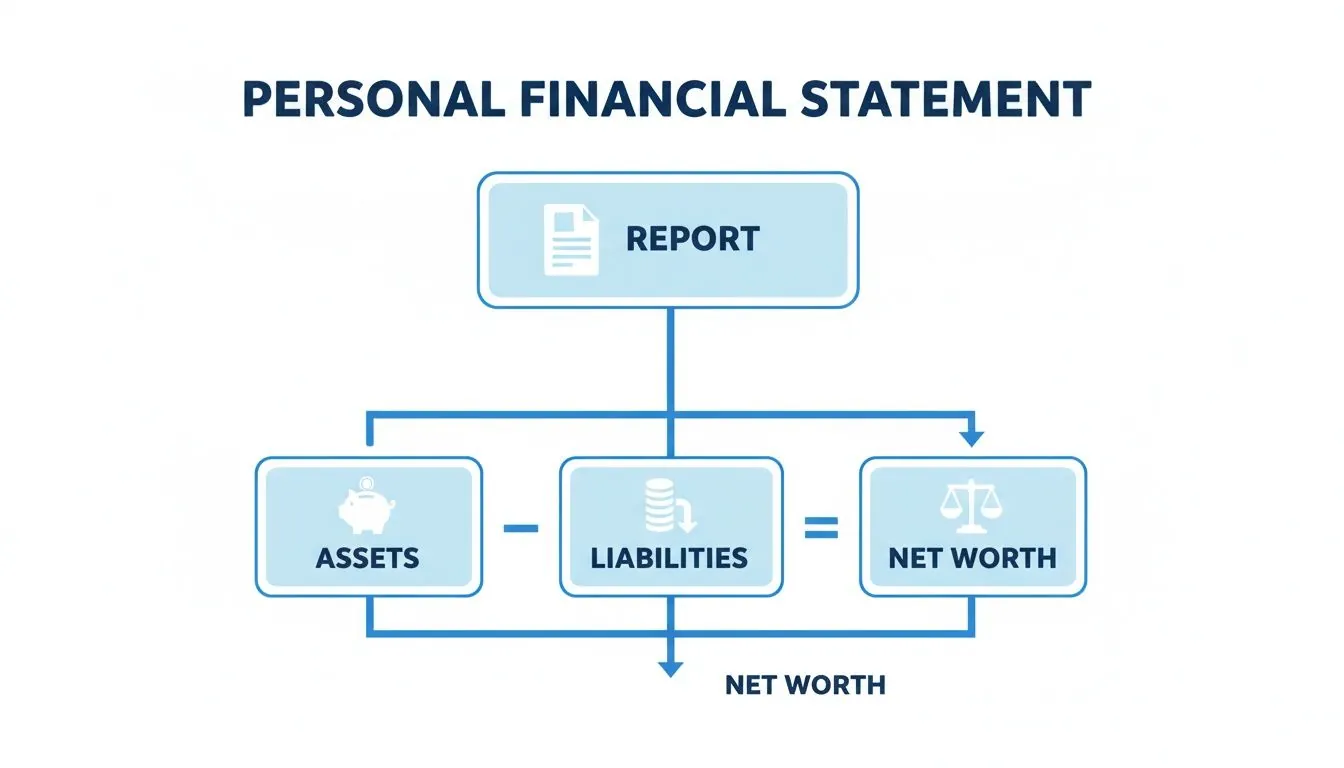

At its heart, a personal financial statement is built on just three core ideas: assets, liabilities, and net worth. Getting a handle on these concepts is the only way to get a truly clear picture of where you stand financially. They’re the building blocks for your entire financial story.

Think of it like a classic balance scale. On one side, you pile up everything you own—your assets. On the other side, you place everything you owe—your liabilities. The way the scale tips reveals your net worth.

This flowchart breaks down exactly how these pieces fit together.

As you can see, the math is simple. It all boils down to what you own minus what you owe. That final number is your true financial position.

To make this crystal clear, let’s break down the two sides of the financial scale.

Assets vs. Liabilities: A Clear Breakdown

This table gives you a straightforward look at what counts as an asset versus a liability, with real-world examples to help you categorize your own finances.

| Category | Definition | Examples |

|---|---|---|

| Assets | Anything you own that holds economic value. | Cash in the bank, stocks, bonds, your home, your car, valuable collectibles, retirement accounts (401k, IRA). |

| Liabilities | Any debt or financial obligation you owe to others. | Mortgage, car loan, student loans, credit card balances, personal loans. |

Getting these categories right is the first and most important step in building an accurate financial statement.

What Are Assets?

In simple terms, assets are all the valuable things you own. They’re the resources that add to your financial strength, whether it’s cash you can spend today or something you could sell for cash down the road.

We can group assets by how quickly you can turn them into cash:

- Liquid Assets: This is your ready money—cash and things that can become cash almost instantly. Think checking accounts, savings accounts, or a money market fund.

- Investments: These are assets you buy hoping they’ll grow in value over time. Common examples include stocks, bonds, mutual funds, and your retirement accounts like a 401(k) or IRA.

- Personal Property: This bucket holds your tangible stuff. The big ones are usually your home (real estate) and your car, but it also includes anything valuable like jewelry, art, or collectibles.

What Are Liabilities?

On the other side of the scale, liabilities are your financial obligations—a formal way of saying “your debts.” This is all the money you owe to other people or institutions.

Knowing your liabilities is just as crucial as listing your assets because every dollar of debt directly subtracts from your overall net worth. For a full picture, it’s helpful to get familiar with different kinds of debt, including understanding unsecured debt like credit cards, which aren’t backed by an asset.

Common liabilities include things like:

- Mortgage loans

- Auto loans

- Student loan balances

- Credit card debt

- Personal loans

Defining Your Net Worth

Finally, we get to the main event: net worth. It’s the result of one simple but incredibly powerful equation. It’s what’s left over after you subtract all your liabilities from all your assets. This one number is the clearest snapshot of your financial health at a single moment in time.

Formula for Net Worth: Total Assets - Total Liabilities = Net Worth

If the number is positive, you own more than you owe—congratulations! If it’s negative, you owe more than you own.

Tracking this number is a huge deal. It tells you if you’re moving in the right direction. For a more detailed walkthrough, our complete guide on how to calculate net worth breaks it all down, step by step. It’s the first move toward building a more secure financial future.

How to Build Your Financial Statement Step by Step

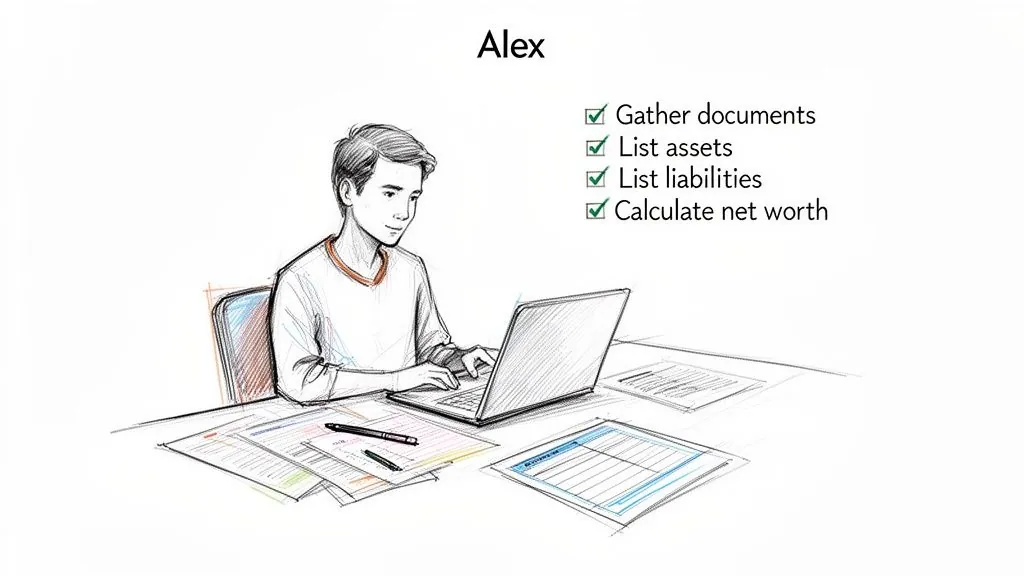

Creating a personal financial statement might sound intimidating, but it’s really just a few simple, manageable steps. Let’s make it real by following along with Alex, who’s decided to get a clear picture of his financial health for the first time. The whole process is pretty straightforward—it just takes a bit of organization.

This step-by-step guide will walk you through building your own statement, just like Alex did.

Step 1: Gather Your Financial Documents

Before you can crunch any numbers, you have to collect all your financial paperwork. This is usually the most time-consuming part, but getting it right from the start makes everything else a breeze.

Alex gets started by pulling together these key items:

- Bank Statements: He downloads the latest statements for his checking and savings accounts.

- Investment Account Summaries: Next, he logs into his 401(k) and brokerage accounts to get their current balances.

- Loan Agreements: He finds his most recent mortgage statement, auto loan bill, and student loan summary.

- Credit Card Statements: Alex pulls up the latest statement for each credit card to see exactly what he owes.

- Property Information: He grabs his property tax bill to find his home’s assessed value and uses a site like Kelley Blue Book for his car’s estimated value.

Having these documents ready eliminates guesswork and makes sure your final numbers are spot-on.

Step 2: List Your Assets

With all his info ready, Alex’s next task is to list everything he owns and pin a current market value on it. He organizes his assets into categories to keep things clean, starting with the most liquid ones first.

Here’s what Alex’s asset list looks like:

- Cash and Equivalents:

- Checking Account Balance: $3,500

- Savings Account Balance: $10,000

- Investments:

- 401(k) Retirement Fund: $45,000

- Brokerage Account (Stocks): $12,000

- Personal Property:

- Home (Current Market Value): $250,000

- Car (Estimated Value): $15,000

Total Assets: $335,500

This sum represents one side of Alex’s financial equation—everything he owns. Remember to use the current fair market value for things like your home and car, not what you originally paid.

Step 3: Compile Your Liabilities

Now for the other side of the coin. Alex lists everything he owes. It’s super important to be thorough here and include every single debt, no matter how small. Forgetting a liability will only give you an inflated, inaccurate sense of your net worth.

Alex’s liability list includes:

- Mortgage Balance: $200,000

- Car Loan Balance: $8,000

- Student Loan Balance: $25,000

- Credit Card Debt: $3,000

Total Liabilities: $236,000

Step 4: Calculate Your Net Worth

This is the final, and most satisfying, step. With his assets and liabilities tallied up, Alex has the two key numbers he needs. He plugs them into the simple net worth formula to see where he stands.

Total Assets ($335,500) - Total Liabilities ($236,000) = $99,500

Alex’s net worth is $99,500. He finally has a clear, actionable snapshot of his financial health.

To get started on your own, you can download a helpful personal financial statement template that gives you a clear structure to follow.

Putting Your Financial Statement to Work

A personal financial statement isn’t a document you create once and then file away forever. Think of it as your financial GPS—it shows you exactly where you stand so you can map out the best route to your goals. It’s a dynamic tool for making smarter, more confident decisions throughout your life.

Its most common use? Borrowing money. When you walk into a bank for a mortgage, a detailed financial statement showing a solid net worth and a responsible debt-to-asset ratio speaks volumes.

This single document gives the lender a clear, organized view of your financial health. It makes the approval process smoother and less stressful because you’re not just hoping for the best; you’re presenting a complete, professional picture of your finances.

A Roadmap for Your Financial Goals

Beyond just securing loans, your statement is a powerful motivator. Take someone dreaming of financial independence. By updating their personal financial statement every quarter, they turn an abstract goal into a real progress report.

Watching their net worth climb—even by small amounts—provides the fuel to keep saving and investing. It turns “retirement” from a vague concept into a tangible number they can actively work toward. This regular check-in helps answer critical questions like:

- Am I on track with my retirement savings?

- Can I afford to take on a new investment right now?

- Is my debt actually shrinking over time?

By transforming your goals into measurable data, the statement makes your progress feel real and keeps you accountable.

A financial statement is more than a list of assets and liabilities; it’s a narrative of your financial journey. Each update tells a new chapter of your story, showing progress, highlighting challenges, and guiding future decisions.

Making Informed Decisions Big and Small

The clarity your statement provides touches nearly every financial choice you face. It helps you accurately gauge your risk tolerance for new investments by showing you exactly how much capital you can afford to put on the line. Once you understand your complete financial picture, you can make critical decisions with confidence, like planning for wills and LPAs.

This document is the bedrock of sound estate planning, ensuring your assets are managed and distributed exactly as you wish. Whether you’re buying a car or starting a business, having a firm grasp of your net worth empowers you to act with conviction. It’s the ultimate tool for turning financial data into real-world action.

Bring Your Finances into Focus with PopaDex

While putting together a personal financial statement by hand is a fantastic way to get intimate with your numbers, let’s be honest—keeping it updated is a grind. Life moves fast, balances change every day, and last month’s snapshot is already ancient history. This is where the old-school spreadsheet method starts to break down.

The whole process can eat up your valuable time, forcing you to log into a dozen different accounts just to pull the latest data. It’s also dangerously easy to make a mistake. A single misplaced decimal or a forgotten account can throw off your entire financial picture. For expats, digital nomads, or anyone juggling money across borders, adding different currencies into the mix creates a tangled mess that spreadsheets just aren’t built to handle.

This is precisely where a dedicated tool like PopaDex comes in, turning a tedious periodic task into a source of effortless, real-time financial insight.

Your Automated Financial Snapshot

PopaDex was designed to eliminate the biggest headaches of manual tracking. Forget spending hours hunting for statements and punching numbers into a spreadsheet. Instead, you can securely connect all your accounts and get a live, automated view of your financial health. It transforms your static statement into a dynamic dashboard that actually works for you.

How does it work? The platform securely links to over 15,000 banks and financial institutions around the world. This powerful connection pulls in your latest balances automatically, so your net worth calculation is always spot-on. If you’re curious about the technology behind this, you can learn more in our guide on financial data aggregation.

This level of automation gives you a few massive advantages:

- Saves Time: Frees you from the soul-crushing cycle of manual data entry.

- Guarantees Accuracy: Wipes out the risk of typos and calculation errors.

- Provides Real-Time Clarity: Offers an up-to-the-minute view of your finances, not just a fossilized snapshot from weeks ago.

Built for a Global Financial Life

For anyone with international accounts, PopaDex has a game-changing feature: true multi-currency support. If you’re an expat, a digital nomad, or a global investor, you can finally stop wrestling with daily exchange rates to figure out your total net worth.

PopaDex automatically converts and displays all your assets and liabilities in your chosen base currency. This gives you a single, unified view of your global financial standing—something that’s practically impossible to maintain accurately with a spreadsheet.

The platform’s dashboards bring your financial data to life, making it easy to spot trends, track your progress towards goals, and understand your entire portfolio at a glance. It turns rows of confusing numbers into clear, actionable charts that tell your complete financial story. By automating the creation of your personal financial statement, PopaDex hands you back your time and gives you the clarity needed to make smarter, more confident financial moves.

Got Questions? We’ve Got Answers

Once you start digging into personal financial statements, a few common questions usually pop up. Let’s tackle them head-on so you can move forward with total confidence.

How Often Should I Update My Personal Financial Statement?

For most people, updating your statement annually is a great rhythm. It gives you a clean year-over-year comparison to see if your net worth is heading in the right direction and if you’re getting closer to those big life goals.

But “most people” isn’t everyone. The right frequency really depends on what’s happening in your financial life right now.

- Quarterly Updates: Are you aggressively paying down debt or saving for a down payment? Checking in every three months offers more immediate feedback and helps you stay motivated and on track.

- Monthly or Real-Time Updates: If your income bounces around (hello, freelancers and business owners!) or you’re actively trading investments, you need a much more frequent pulse on your numbers.

This is where automated tools completely change the game. A platform like PopaDex can sync with your accounts to give you a live, up-to-the-minute view of your finances, making manual updates a thing of the past.

What Are the Most Common Mistakes to Avoid?

Creating a financial statement is straightforward, but a few common slip-ups can paint a dangerously inaccurate picture of your financial health. Knowing what they are from the start is half the battle.

Here are the four biggest mistakes I see people make all the time:

- Forgetting Small Liabilities: It’s easy to list your mortgage, but what about that “buy now, pay later” balance for your new couch? Or a small personal loan from a family member? These little debts add up fast and can throw your numbers off.

- Overvaluing Your Assets: That car you bought for $30,000 three years ago isn’t worth that today. You have to use the fair market value—what someone would actually pay for it now. The same goes for electronics, jewelry, and other collectibles.

- Omitting Certain Assets: Don’t forget about the money sitting in your 401(k) or IRA, the cash value of a life insurance policy, or that Health Savings Account (HSA) balance. These are all valuable pieces of your financial puzzle.

- Using Outdated Information: Your financial life is always in motion. Pulling a bank balance from a statement that’s three months old is just not going to cut it. You need the most current numbers you can get your hands on.

A personal financial statement is all about clarity and honesty with yourself. A small oversight can create a false sense of security, so taking the time to be thorough is one of the best investments you can make in your financial future.

Is a Personal Financial Statement the Same as a Budget?

Nope. They’re two totally different tools, but they work together like a power duo. Confusing them is really common, but understanding their distinct jobs is the secret to smart financial management.

Think of it this way:

A personal financial statement is a snapshot. It’s a photo of your financial health—your net worth—at this exact moment. It answers the question, “Where am I right now?”

A budget, on the other hand, is a forward-looking plan. It’s your roadmap for the future, detailing how you’re going to spend and save your money next week or next month. It answers the question, “Where am I going?”

So, your financial statement tells you where you stand, and your budget is the game plan for getting where you want to go.

Ready to stop guessing and start knowing exactly where you stand? PopaDex automates your personal financial statement, connecting all your accounts to give you a live, accurate view of your net worth in one simple dashboard. Take control of your finances today by visiting https://popadex.com.