Our Marketing Team at PopaDex

What Is Portfolio Rebalancing And How Does It Work

Portfolio rebalancing is the surprisingly simple act of buying and selling parts of your portfolio to get it back to your original, intended asset mix. Think of it like tuning a guitar—over time, the strings drift, and you have to make small adjustments to bring everything back into harmony. It’s a core discipline for managing risk and sticking to your plan.

What Is Portfolio Rebalancing In Simple Terms?

Let’s try a different analogy. Imagine your investment portfolio is a carefully planted garden. You’ve decided on a specific layout that suits your taste and the local climate—say, 60% sun-loving flowers (your stocks) and 40% hardy, shade-tolerant ferns (your bonds). This specific mix is your sweet spot, balancing growth potential with stability.

After a long, sunny season, those flowers are going to shoot up. They’ll look fantastic, but they might start hogging all the space and sunlight, crowding out the ferns. Suddenly, your garden isn’t the balanced design you started with. It’s now heavily tilted towards the sun-loving flowers, making it more vulnerable if the weather suddenly turns cloudy for a long stretch.

Portfolio rebalancing is just a bit of financial gardening. You trim back the flowers that have grown the tallest (selling some of your best-performing stocks) and use that opportunity to plant more ferns in the shadier spots (buying more of the assets that haven’t grown as much). You’re not getting rid of the flowers—you’re just restoring the garden to its intended, healthy balance.

It’s About Managing Risk, Not Chasing Returns

Here’s the thing most people miss: at its heart, rebalancing is a risk-management tool. It’s not about trying to time the market or predict what will go up next. Instead, it’s a disciplined, systematic way to follow the oldest advice in the book: buy low and sell high.

By periodically selling what’s done well and buying what’s lagged, you keep your risk level exactly where you want it. This simple discipline prevents your portfolio from getting dangerously over-weighted in one area, which could leave you painfully exposed when—not if—the market takes a turn.

Portfolio rebalancing is nothing more than realigning your investments back to your target asset allocation after the market has knocked them out of whack. It’s how you make sure you’re sticking to the risk profile you signed up for, instead of letting market drift silently change the game for you.

This isn’t just theory; it’s standard practice for professionals. One major study looked at thousands of international equity funds and found that this is exactly what the pros do. They consistently sell assets that have shot up in value to bring their portfolios back into alignment. If you’re curious about the data, you can dig into the research on how fund managers handle rebalancing.

A Quick Breakdown

Let’s quickly summarize the core concepts of rebalancing in a simple table.

Portfolio Rebalancing at a Glance

| Concept | Simple Explanation |

|---|---|

| Target Allocation | Your ideal mix of assets (e.g., 60% stocks, 40% bonds) based on your personal goals. |

| Portfolio Drift | What happens when the market makes your actual mix drift away from your target. |

| Rebalancing Action | The simple act of selling winners and buying laggards to get back to your target. |

Ultimately, rebalancing is just about being proactive. It’s about sticking to your financial game plan instead of getting swept up in the market’s emotional highs and lows.

How Portfolio Drift Quietly Increases Your Risk

If you don’t have a disciplined game plan for your portfolio, it won’t stay aligned with your goals for long. The market’s natural ups and downs cause something called portfolio drift—a subtle but serious shift in your asset allocation. It happens so quietly you might not even notice until you’re way off track.

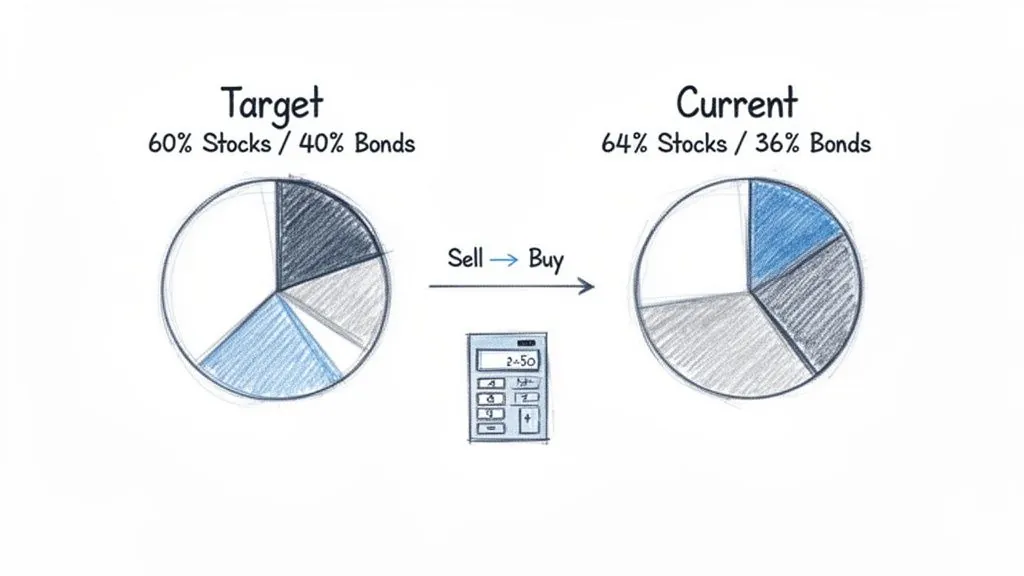

Imagine you kick off your investing journey with a classic 60/40 portfolio worth $100,000. Based on your comfort for risk, you put $60,000 in stocks and $40,000 in bonds. This is your target allocation, the strategic mix you designed to balance growth with a bit of stability.

Now, let’s fast-forward one year. Stocks had a fantastic run, and your holdings shot up by 25%. That initial $60,000 is now worth a cool $75,000. Meanwhile, your more conservative bonds delivered a modest 5% gain, growing to $42,000.

The Anatomy of Unintended Risk

On the surface, this all sounds like great news. Your total portfolio has grown to $117,000. But let’s take a closer look under the hood at your new asset mix.

- Stocks: $75,000

- Bonds: $42,000

- Total: $117,000

Do the math, and you’ll see your portfolio is now roughly 64% stocks and 36% bonds. While you’re enjoying the gains, you’ve accidentally drifted away from your original 60/40 plan. Without making a single trade, you’re now taking on more risk than you originally signed up for. That higher exposure to stocks makes your portfolio much more vulnerable if the market suddenly decides to head south.

This is the essence of portfolio drift. It’s the silent risk that builds up when your winners grow to become a much bigger piece of your financial pie.

Portfolio drift is the gap that opens between your intended investment strategy and your actual one. It’s driven by market performance and can unintentionally transform a balanced portfolio into a riskier one.

This is precisely why getting a solid handle on portfolio rebalancing is so important. It’s your main tool for closing that gap and pulling your investments back in line with your actual comfort level for risk.

When you let your portfolio drift, you’re essentially letting the market dictate your risk exposure. It might feel great during a bull run, but a market correction could deliver a much bigger blow than you were ever prepared for. To keep your portfolio well-structured, it’s worth exploring various powerful investment diversification strategies that work hand-in-hand with a regular rebalancing schedule. Staying disciplined is what keeps your risk profile intentional, not accidental.

Choosing Your Ideal Rebalancing Strategy

Once you’re sold on why rebalancing is a must-do, the natural next question is, “Okay, but how do I actually do it?” There’s no single right answer here. The best method really comes down to your goals, your personality, and just how much you enjoy tinkering with your portfolio.

Are you a “set it and forget it” type who thrives on a simple, predictable routine? Or do you prefer a more hands-on system that reacts to what the market is doing? Let’s walk through the most common strategies to find the one that feels right for you.

Of course, before you can rebalance, you need a target. Setting your overall retirement asset allocation by age is the foundation—it’s the North Star you’ll always be navigating back to.

Time-Based Rebalancing: The Simple Approach

The most straightforward way to rebalance is based on the calendar. With a time-based strategy, you simply pick a schedule—say, quarterly, semi-annually, or once a year—and stick to it. On that date, you check your portfolio and make the trades needed to get back to your targets.

It’s simple and beautifully disciplined. You don’t have to obsess over daily market news; just put a reminder in your calendar. For most long-term investors, an annual check-in is plenty to keep things from getting too out of whack without racking up trading fees. The only real downside is that it won’t react to a massive market swing that happens between your scheduled dates.

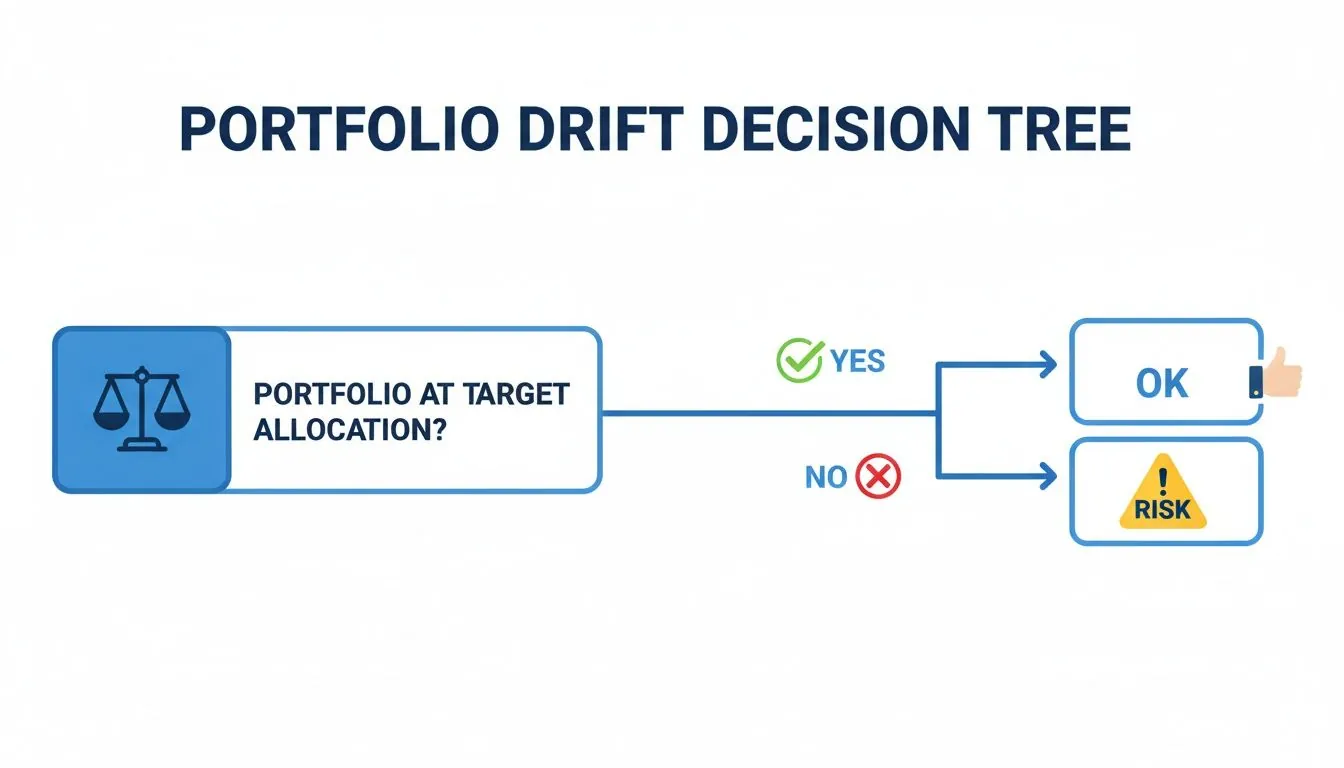

This decision tree nails the core logic:

It boils down to a single, critical question: is your portfolio where it’s supposed to be? If the answer is no, you’ve quietly taken on more risk than you planned for.

Threshold-Based Rebalancing: The Responsive Approach

If a fixed schedule feels too rigid, threshold-based rebalancing might be more your speed. This approach isn’t tied to a date on the calendar but to a specific trigger. You set a “tolerance band”—a buffer zone—around your target allocations. A common choice is 5%.

Let’s say your target is 60% stocks. If a bull run pushes that allocation up to 65%, you’ve breached the threshold. That’s your signal to rebalance. This method is far more responsive to market volatility, ensuring you only act when the drift is big enough to matter.

The real beauty of threshold rebalancing is its efficiency. You avoid pointless trades when markets are calm, but it forces you to act during major moves, making it an incredibly powerful way to manage risk systematically.

This isn’t just theory. Some research suggests this method can actually improve risk-adjusted returns over time. Using bands around 5% might even boost returns by 0.5% to 1% annually in diversified portfolios.

Comparing Rebalancing Methods

So, which one is for you? The right answer depends on your personality and how much time you want to spend on your portfolio. Let’s break down the two main approaches.

| Strategy | Best For | Pros | Cons |

|---|---|---|---|

| Time-Based | “Set it and forget it” investors who value simplicity and discipline. | Easy to remember and automate. Prevents emotional, news-driven trading. | Can miss major market swings between check-in dates. May trigger trades for tiny, insignificant drifts. |

| Threshold-Based | Hands-on investors who want a system that reacts to market volatility. | More efficient—only triggers trades when necessary. Forces you to sell high and buy low during big moves. | Requires more frequent monitoring. Can be hard to stick to during volatile periods. |

Ultimately, a time-based approach offers simplicity and discipline, while a threshold-based strategy provides a more dynamic and potentially efficient way to manage risk.

The Hybrid Model: Best of Both Worlds

Can’t decide? You don’t have to. A hybrid approach combines the discipline of a schedule with the responsiveness of triggers.

Here’s how it works: You might check your portfolio on a set schedule, like every quarter (time-based), but you only rebalance if an asset class has drifted past its threshold (threshold-based).

This strategy gives you a routine without forcing you to trade over tiny, meaningless shifts. For many people, it’s the perfect middle ground. If you’re trying to figure out the right frequency, our guide on how often to rebalance can help you drill down into what makes sense for your specific situation.

A Step-By-Step Guide To Rebalancing Your Portfolio

Knowing the theory is great, but putting it into practice is what actually builds wealth. Let’s walk through exactly how to bring a drifted portfolio back in line using our earlier example.

Remember our investor? They started with a $100,000 portfolio targeting a 60/40 split. After a nice bull run, their portfolio is now worth $117,000, but their allocation has drifted to 64% stocks and 36% bonds. Time to restore the balance.

Calculate Your New Targets

First thing’s first: you need to figure out the target dollar amounts for your current portfolio value. You’re not reverting to the original $100,000; you’re applying your percentages to the new, larger total.

- Target Stock Allocation: $117,000 x 60% = $70,200

- Target Bond Allocation: $117,000 x 40% = $46,800

Now, let’s see how that stacks up against where you are right now:

- Current Stocks: $75,000 (That’s $4,800 over your target)

- Current Bonds: $42,000 (And $4,800 under your target)

The math is simple. You need to shift $4,800 out of stocks and into bonds to get back to your 60/40 balance. The real question is how to make that happen.

Choose Your Rebalancing Method

Selling stocks to buy bonds is the most direct route, but it’s not always the smartest. If you’re investing in a taxable account, selling your winners can trigger capital gains taxes and maybe even transaction fees. Luckily, there are more elegant ways to handle this.

Rebalancing is a powerful discipline that counters our natural tendency to chase returns. It systematically forces investors to trim what’s hot and add to what’s not, which is a cornerstone of long-term risk management.

Think about using these more cost-effective methods first:

-

Rebalance with New Contributions: If you’re still in the accumulation phase and adding money, this is your best friend. Just direct all your new contributions into the asset class that’s underweight. In our example, you’d funnel the next $4,800 of new money entirely into bonds until you hit that 60/40 target. This avoids selling anything and sidesteps potential taxes.

-

Rebalance with Withdrawals: If you’re in retirement and living off your portfolio, just reverse the logic. Take your withdrawals from the asset class that’s overweight. To get back on track, you would fund your next $4,800 in distributions by selling stocks. Again, this avoids unnecessary trades and helps you systematically sell high.

These techniques cleverly turn your regular cash flow—whether it’s coming in or going out—into a powerful rebalancing tool. It’s seamless and tax-smart.

The Discipline of a Global Perspective

This process is more than just a mechanical chore; it’s a strategic defense against market swings and emotional mistakes. Research has consistently shown that a disciplined rebalancing strategy helps keep portfolios stable, particularly when you’re dealing with the extra volatility of international investments and currency fluctuations.

Think about it: a 60/40 portfolio left to its own devices during a strong bull market could easily drift into a much riskier 75/25 split. By rebalancing, you lock in gains and buy assets that are temporarily out of favor, tapping into the power of assets reverting to their long-term average performance. To dig into the data, you can learn more about how rebalancing behavior impacts global funds.

Navigating The Hidden Costs Of Rebalancing

While keeping your portfolio in line is a fantastic discipline for managing risk, pulling the trigger on those trades isn’t always free. Every transaction you make has the potential to rack up costs that can, if you’re not careful, quietly eat away at your returns over the long haul. So before you start buying and selling, it’s crucial to get a handle on the two biggest culprits: taxes and transaction fees.

When you rebalance by selling off assets that have shot up in value, you’re effectively “locking in” those profits. If those investments are sitting in a standard taxable brokerage account, that one click can trigger a capital gains tax bill. The exact amount you’ll owe depends on things like how long you held the asset and your income bracket, but it’s a direct hit to your net profit.

The Impact Of Taxes And Fees

Beyond the taxman, you’ve also got to think about transaction costs. Sure, many brokers now offer commission-free trading on stocks and ETFs, but that’s not a universal rule. Certain investments, like some mutual funds, can still come with trading fees. Even seemingly small costs can add up, especially if you’re following a strategy that calls for frequent adjustments.

These costs create a delicate balancing act. You absolutely want to keep your portfolio aligned with your goals, but you don’t want the rebalancing process itself to become so expensive that it cancels out the benefits.

The real goal of smart rebalancing isn’t just getting back to your target numbers; it’s doing it in the most cost-efficient way possible. A tax-aware strategy can make a massive difference in your real-world returns.

Smart Strategies To Minimize Costs

The good news is you can slash these hidden costs with a few simple, strategic moves. Instead of just automatically selling your winners, think about these more efficient approaches first:

-

Prioritize Tax-Advantaged Accounts: Do your rebalancing inside tax-sheltered accounts like an IRA or 401(k) whenever you can. Since trades within these accounts don’t trigger capital gains taxes, you can buy and sell to your heart’s content to get back on track without worrying about an immediate tax hit.

-

Use New Cash to Rebalance: If you’re regularly adding new money to your portfolio, this is the golden ticket. Simply direct your fresh contributions toward your underperforming, underweight asset classes. This lets you buy what’s “low” without selling anything, neatly sidestepping both taxes and transaction fees altogether.

By taking a more thoughtful approach, you can make sure your rebalancing strategy actually reinforces your financial plan instead of creating an unnecessary drag on its performance. It’s all about being both disciplined and efficient.

Automating Your Rebalancing For Long-Term Success

The best investment strategy in the world is useless if you don’t stick to it. While rebalancing is a powerful discipline, its biggest weakness is human nature—we get emotional, we get busy, and we simply forget. The best solution? Take yourself out of the day-to-day equation and let technology do the heavy lifting.

Automating your rebalancing turns a recurring chore into a seamless background process. By setting up a system, you automatically enforce the “buy low, sell high” rule without ever having to fight the emotional urge to do the exact opposite when the market gets choppy.

Set-It-And-Forget-It Automation Tools

Thankfully, modern investing gives you several great ways to put your rebalancing on autopilot and keep your portfolio in line with minimal effort.

-

Target-Date Funds: Think of these as an “all-in-one” portfolio. They’re built around a specific retirement year and automatically shift their asset mix to become more conservative as you get closer to that date. All the rebalancing happens inside the fund, completely hands-off for you.

-

Robo-Advisors: These digital platforms build and manage a diversified portfolio based on your risk tolerance. Their algorithms constantly watch your allocations and automatically place trades to fix any drift, keeping you on track 24/7.

-

Automatic Contributions: Most brokerage platforms let you set up recurring investments. You can use this to your advantage by directing these new deposits into your underweight assets, essentially rebalancing your portfolio over time with fresh cash.

The real magic of automation is consistency. It strips emotion, market timing, and guesswork out of the process. Your portfolio stays aligned with your long-term goals, no matter what the market is doing this week.

Technology for a Clearer View

While robo-advisors offer a completely hands-off experience, technology can also make a DIY approach much, much simpler. The first step to successful manual rebalancing is always having a clear, real-time picture of your asset allocation. This is where modern software makes all the difference.

Instead of wrestling with spreadsheets, you can use various portfolio analysis tools to link your accounts and get an instant, accurate snapshot of where you stand. These platforms show you exactly how far you’ve drifted from your targets, making it obvious what needs to be adjusted. That kind of clarity empowers you to make disciplined decisions quickly and get on with your life.

Common Questions About Portfolio Rebalancing

Even with a solid game plan, you’re bound to have questions when you start putting rebalancing into practice. Let’s walk through a few of the most common ones to clear things up and get you moving with confidence.

How Often Should I Rebalance?

There’s no single magic number here. Some investors like to keep it simple with a time-based schedule, maybe giving their portfolio an annual check-up. Others prefer a more hands-off, tolerance-based approach, only stepping in when an asset class drifts off target by a certain amount, like 5%.

Ultimately, the best strategy is the one you can actually stick to without overthinking it.

Many people managing retirement savings also ask how this applies to their 401(k) or 403(b). For these specific employer-sponsored plans, specialized nonprofit 401k plan consulting services can provide advice tailored to your account’s unique rules and investment options.

Can Rebalancing Lower My Returns?

In the short term, maybe. It can feel counterintuitive to sell off your high-flying stocks during a long bull market—almost like you’re leaving money on the table.

But here’s the thing: the primary goal of rebalancing isn’t about squeezing out every last drop of return. It’s about risk management. You’re trimming winners to protect your portfolio from getting dangerously overexposed to a single asset class, which is what helps you sleep at night when the market eventually turns.