Our Marketing Team at PopaDex

What Is Tangible Net Worth Explained

When you hear “net worth,” you probably think of the total value of everything you own, minus your debts. But there’s another, more grounded number that lenders and savvy investors pay close attention to: tangible net worth.

Tangible net worth is a no-nonsense measure of value. It’s calculated based only on physical, touchable assets after all your debts are paid off. It deliberately strips away abstract, “on-paper” values like brand reputation or intellectual property, focusing squarely on what you could sell off if you had to liquidate everything tomorrow. This number gives a starkly realistic, worst-case-scenario view of financial health.

What Tangible Net Worth Really Means

Let’s use a popular local coffee shop as an example. Its total net worth includes everything from the high-tech espresso machine and bags of coffee beans to its loyal customer base and the shop’s fantastic reputation around town.

But to find its tangible net worth, you have to ignore the value of that hard-earned brand loyalty and customer goodwill. They’re valuable, sure, but you can’t exactly sell them.

Instead, you focus only on what you can physically touch, inventory, and sell:

- The building itself (if you own it)

- The coffee grinders, brewers, and refrigerators

- The tables, chairs, and current inventory

- The cash sitting in the register

Once you add up the value of these physical items and subtract all your business loans and other debts, what’s left is your tangible net worth. It’s a conservative, ground-level assessment of what your business is truly worth in solid assets.

A Foundation Built on Physical Value

Think of it like buying a house. The asking price might be inflated because it’s in a hot neighborhood with great schools—these are intangible benefits that drive up the perceived value. The house’s tangible value, however, is based on the actual bricks, lumber, and land it occupies.

Tangible net worth works the same way. It ignores the “neighborhood hype” and focuses on the “bricks.”

Tangible net worth is the financial bedrock of a person or company. It answers a critical question for lenders and investors: “If everything non-physical disappeared tomorrow, what solid value would remain?”

This metric is all about assessing risk. It’s a key financial figure used to find the real, physical value of a company’s assets after subtracting liabilities and intangible assets like goodwill or patents. A bank, for instance, might require a business to maintain a tangible net worth of $2 million as a condition for a loan. This protects the lender if the borrower defaults and assets need to be liquidated. For more on how lenders view this, check out these insights from Equirus Wealth.

Ultimately, getting a handle on this concept gives you a clear, uninflated picture of financial stability. It’s the measure of worth that remains when all the hype and abstract value is stripped away, leaving only what is real and physically present.

How to Calculate Tangible Net Worth

Figuring out your tangible net worth might sound like a job for an accountant, but it’s simpler than you think. The formula itself is pretty direct, cutting through the financial noise to give you a clear, physical value of what you own.

It all boils down to a simple equation:

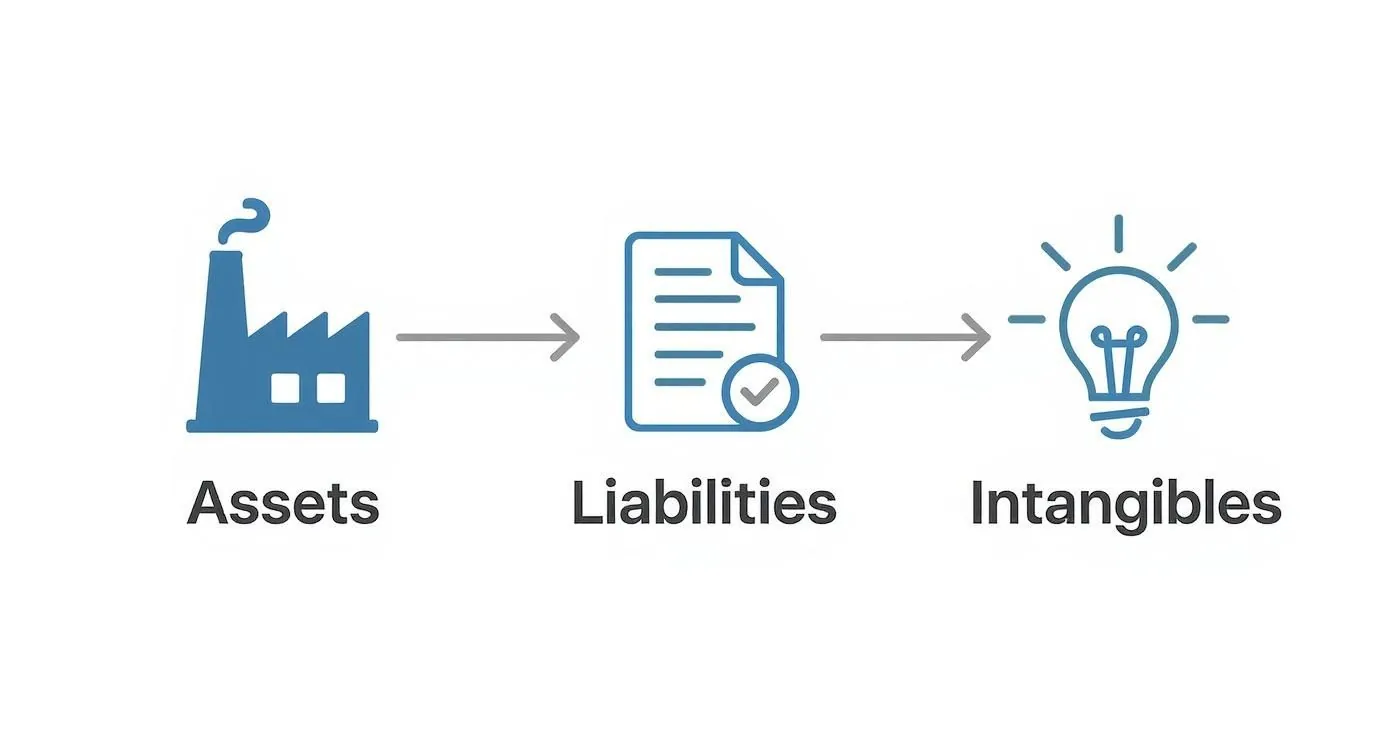

Tangible Net Worth = Total Assets - Total Liabilities - Intangible Assets

This calculation strips away your debts and any non-physical assets, leaving you with a true picture of your financial foundation—the stuff you can actually touch and sell.

Step 1: Identify Your Tangible Assets

First things first, grab a notepad or open a spreadsheet and list everything you own that has a physical presence. These are the items you can see, feel, and put a price tag on. Don’t worry about getting it perfect on the first go; just start brainstorming.

Common tangible assets include things like:

- Real Estate: The current market value of your house, any rental properties, or land you own.

- Vehicles: Your car, truck, boat, or motorcycle.

- Physical Inventory: If you run a business, this is all your unsold products and raw materials.

- Equipment and Machinery: Think computers, tools, and other gear you use for work or hobbies.

- Cash and Investments: This includes physical cash, money in the bank, stocks, and bonds.

Step 2: List Your Total Liabilities

Next up, it’s time to tally everything you owe. Liabilities are simply your financial debts or obligations to another person, bank, or company. This step is crucial because it shows what claims others have on your assets.

Your list of liabilities will probably include:

- Mortgages on your properties.

- Car loans or leases.

- Student loan balances.

- Credit card debt.

- Business loans or active lines of credit.

- Personal loans from a bank or even a family member.

To really get a handle on this, it helps to understand your balance sheet, which is just a formal way of organizing these very same assets and liabilities.

Step 3: Subtract Intangibles and Liabilities

With both lists in hand, you’re ready for the final step: the math. Start with the total value of your assets and subtract your total liabilities. From that number, subtract the value of any intangible assets you might have, like brand goodwill, patents, or trademarks (though most individuals won’t have these).

Let’s take a local coffee shop as an example. It has $200,000 in tangible assets (the building, equipment, cash in the register) and $80,000 in liabilities (loans for equipment). It has no intangible assets. Its tangible net worth is simply $200,000 - $80,000 = $120,000.

For an individual, it’s just as straightforward. Imagine someone with a $500,000 home, $50,000 in savings, a $300,000 mortgage, and $10,000 left on their car loan. Their tangible net worth would be ($500,000 + $50,000) - ($300,000 + $10,000) = $240,000.

This process gives you the most conservative, no-fluff snapshot of where you stand financially. While this is all about tangible value, you can get the bigger picture by checking out our guide on what net worth means and how to calculate it.

Why Tangible Net Worth Matters in the Real World

While tangible net worth might sound like a dry, back-office accounting term, it’s a number that carries serious weight in the moments that matter most. This goes beyond spreadsheets; it’s a figure that directly influences loan approvals, business sales, and your own financial security. Think of it as the ultimate reality check on financial stability.

Its most common stomping ground is the world of lending. When you apply for a business loan, banks and other lenders need to look past your flashy profit projections and brand buzz. They want to know what solid, physical stuff is actually backing up your financial claims. Your tangible net worth gives them that exact picture.

This number is their go-to metric for measuring risk. It answers their single most important question: “If everything goes sideways and this business fails, what real assets can we sell to get our money back?” A strong tangible net worth tells them you have a solid foundation, which makes you a much safer bet. On the flip side, a low or negative number can bring a loan application to a screeching halt, no matter how great the business idea sounds.

The process is all about identifying your assets, subtracting what you owe, and then stripping out all the non-physical “fluff” to get to the core value.

This simple flow really drives home the point: you have to systematically peel away both debts and non-physical assets to find out what a company is truly worth in cold, hard assets.

A Key Metric in Business Valuation

Beyond just getting loans, tangible net worth is crucial when it comes to buying or selling a business. For a potential buyer, it sets a baseline “liquidation value”—the absolute rock-bottom price the company’s physical assets are worth if they were sold off tomorrow. This provides a solid anchor for negotiations, making sure the final sale price is grounded in reality, not just pie-in-the-sky hopes about future profits.

Historically, this laser focus on tangible assets has been a bedrock of smart risk management. Think back to the 2008 financial crisis. Companies loaded up with intangible assets like “goodwill” were incredibly vulnerable when those imaginary values evaporated overnight. In stark contrast, businesses with a healthier tangible net worth were in a much better position to ride out the storm. In fact, data from that time showed that companies whose tangible net worth was at least 25% of their total assets had a significantly lower rate of default.

Understanding Your True Financial Position

For individuals, running this calculation gives you a brutally honest look at your financial health. It forces you to separate real, concrete equity from more volatile or abstract asset values. This metric is a close cousin to another important concept, which you can learn about in our guide on what is liquid net worth. At the end of the day, understanding your tangible net worth grounds your financial planning in reality, helping you build a more resilient and secure future.

Using Financial Ratios to Measure Risk

Knowing your tangible net worth is a great start, but the number itself is just a snapshot. Its real power comes alive when you use it to measure financial risk. By plugging your TNW into a few key financial ratios, you can move from a simple valuation to a deep, actionable understanding of a company’s stability and its ability to shoulder debt.

One of the most telling metrics out there is the Debt-to-Tangible-Net-Worth Ratio. This tool gives you a crystal-clear picture of how much a company depends on borrowing compared to the actual, physical equity its owners have in the game. It cuts through the noise to answer a critical question: “For every dollar of tangible owner equity, how much debt is this company carrying?”

Calculating the Debt-to-Tangible Net Worth Ratio

The formula couldn’t be more straightforward, yet it offers a potent look at a company’s leverage against its hard asset base. For lenders and investors, it’s a go-to indicator for gauging solvency.

Here’s the calculation:

Debt-to-Tangible Net Worth Ratio = Total Liabilities / Tangible Net Worth

A lower ratio is almost always what you want to see. It signals that the company has a strong foundation of physical assets to cover what it owes. A higher ratio, on the other hand, suggests the business is heavily leveraged, relying far more on borrowed cash than its own tangible equity. That can be a huge red flag for anyone looking to lend them money.

Let’s say a business has $500,000 in total liabilities and a tangible net worth of $1,000,000. Its ratio is a healthy 0.5, showing that its tangible assets comfortably dwarf its debts.

Interpreting the Ratio and Industry Benchmarks

So, what’s a “good” number? While it can vary by industry, there are some solid rules of thumb. In U.S. commercial lending, a debt-to-tangible-net-worth ratio below 0.5 is generally viewed as very strong. Things start getting dicey when ratios climb above 1.0 (or 100%), which often signals significant risk. It means the company owes more to its creditors than its entire physical asset base is worth.

A ratio over 1.0 is a serious warning. It means that if the business had to liquidate all its physical assets tomorrow, it still wouldn’t have enough cash to pay back its lenders, leaving shareholders with absolutely nothing.

This metric doesn’t exist in a vacuum, of course. For a more complete picture, it’s wise to compare it with other leverage indicators. A great place to start is understanding the debt-to-asset ratio calculation, which stacks liabilities against all assets, not just the tangible ones. Using these ratios together gives investors and owners a much more realistic and well-rounded assessment of financial risk.

The Common Traps in Your Tangible Net Worth Calculation

Figuring out your tangible net worth sounds simple on the surface, but a few small slip-ups can throw the whole number off. A seemingly minor oversight can easily snowball into a major miscalculation, affecting everything from your ability to secure a loan to your personal financial strategy. Knowing where people usually go wrong is the first step to getting a number you can actually trust.

One of the most common tripwires is misclassifying your assets. It’s surprisingly easy to get tangled up in items that blur the line between physical and non-physical. For example, the computer hardware on your desk is definitely a tangible asset, but the specialized software that makes it run is intangible. Getting this distinction right is absolutely critical for an accurate result.

Another huge mistake is using the wrong values for your assets. Just grabbing the price you originally paid for something—its book value—won’t cut it. You have to use the current market value, which is what you could realistically sell the asset for today. That piece of machinery you bought for $50,000 five years ago? After depreciation and wear-and-tear, it might only be worth $15,000 now.

Don’t Sweat the Big Stuff, Sweat the Small Stuff

Beyond getting your asset values right, a lot of people simply forget about hidden or overlooked liabilities. An accurate tangible net worth calculation demands a complete tally of everything you owe, not just the big-ticket items like a mortgage or car loan.

Here are a few liabilities that often slip through the cracks:

- Accrued Taxes: Think property taxes or income taxes that have been incurred but aren’t officially paid yet.

- Personal Guarantees: If you’ve co-signed a loan for a friend or family member, that potential debt is a contingent liability and counts against you.

- Unpaid Bills: This bucket includes any outstanding invoices for services, utilities, or suppliers that are waiting to be settled.

They might seem like small details, but they add up. You have to subtract them to get a true picture of your financial position.

The whole point of calculating tangible net worth is to land on a conservative, real-world valuation. If you forget liabilities or use outdated asset values, you’re just creating a falsely optimistic number that won’t help you make sound decisions.

Finally, there’s a simple but crucial error: inconsistent timing. All of your asset values and liability balances have to be calculated for the exact same date. Using a property valuation from last year with a bank balance from this morning will completely skew your results. Pick a specific “as of” date and apply it to every single item on your list. This ensures your final number is a true snapshot in time, giving you a reliable tool for navigating your financial future.

Putting Your Tangible Net Worth to Work

Calculating your tangible net worth is more than just a financial exercise; it’s about turning a static number into a dynamic tool that guides your financial future. Think of it as your personal financial dashboard. The key goes beyond knowing the number—it’s tracking it consistently.

https://www.youtube.com/embed/Xv0u5fACEEo

By updating your personal balance sheet regularly, you start to see the bigger picture. Is your tangible net worth growing, shrinking, or just treading water? This simple observation tells you whether your financial habits are actually getting you closer to your long-term goals.

Turning Data Into Action

Making this a regular habit doesn’t have to be a chore. A simple spreadsheet or financial software is all you need to keep your assets and liabilities up to date. Just set a recurring reminder—maybe quarterly or twice a year—to refresh your numbers.

This consistency is what empowers you to make smarter choices. For example:

- Spotting Trends: A steady decline in your tangible net worth could be a wake-up call to start paying down high-interest debt more aggressively.

- Measuring Progress: Seeing that number grow provides real, tangible reinforcement that your financial strategies are paying off.

- Goal Setting: Tracking gives you a realistic baseline for setting future wealth-building targets.

Monitoring your tangible net worth turns raw data into meaningful insight. It moves you from simply knowing your financial position to actively steering it in the right direction.

Once you have a clear picture, you can focus on strategies to grow it. For instance, if you come into a significant amount of money, understanding how to legally reduce tax and invest an inheritance or capital gain wisely can make a massive difference to your long-term wealth.

By making this metric a living, breathing part of your financial toolkit, you’re not just tracking numbers; you’re building a stronger foundation for lasting growth and stability.

Common Questions About Tangible Net Worth

As you start working with tangible net worth, a few questions always seem to pop up. It’s a specific metric with its own quirks, and getting a handle on them is key to using it effectively in your financial life. Let’s tackle some of the most common ones.

Can Tangible Net Worth Be Negative?

Yes, absolutely. A negative tangible net worth simply means your total liabilities—everything you owe—are greater than the current market value of your tangible assets.

This isn’t as uncommon as you might think. It happens frequently with recent graduates who have hefty student loans but haven’t had time to acquire many physical assets. Businesses that are heavily leveraged with debt can also find themselves in this position. A negative number is a clear signal of financial risk, showing you wouldn’t have enough physical stuff to sell to cover your debts if they all came due at once.

How Often Should I Calculate My Tangible Net Worth?

There’s no single magic number here, but consistency is what really matters. A great place to start is calculating it once or twice a year. That’s frequent enough to see how you’re progressing without turning it into a chore.

That said, you should definitely run the numbers again after any major financial shift. Think of events like:

- Buying or selling a house

- Receiving a significant inheritance

- Taking on a major new loan, like for a business or a car

How Does Depreciation Affect Tangible Net Worth?

Depreciation has a direct and significant impact. Since tangible net worth is all about the current market value of your assets, you have to account for the natural drop in value that most things experience over time.

For example, that car you bought for $30,000 might only be worth $18,000 on the open market a few years later. That $12,000 difference comes straight off your total tangible assets, which in turn lowers your tangible net worth. If you ignore depreciation, you’re working with an inflated, inaccurate picture of your finances.

Is Tangible Net Worth the Same as Book Value?

Nope, they’re two different animals. Book value is a pure accounting term—it’s what you originally paid for an asset, minus the accumulated depreciation recorded on the books.

Tangible net worth, on the other hand, is grounded in reality. It uses an asset’s current market value, meaning what you could realistically sell it for today. These two figures can be miles apart, especially for assets like real estate that often appreciate, while the book value might show it’s worth less over time.

Ready to stop guessing and get a precise, real-time look at your financial health? PopaDex gives you an intuitive dashboard to monitor your tangible net worth, investments, and liabilities, all in one spot. Take control of your financial future by visiting https://popadex.com to start your free trial.