Our Marketing Team at PopaDex

What Is Wealth Accumulation and How Can You Build It?

Wealth accumulation isn’t about how big your paycheck is. It’s about what you do with that paycheck to systematically grow your assets over time. It’s the deliberate process of increasing your net worth—by buying up investments and other valuable things while keeping your debts in check.

Defining Wealth Accumulation Beyond Just a Paycheck

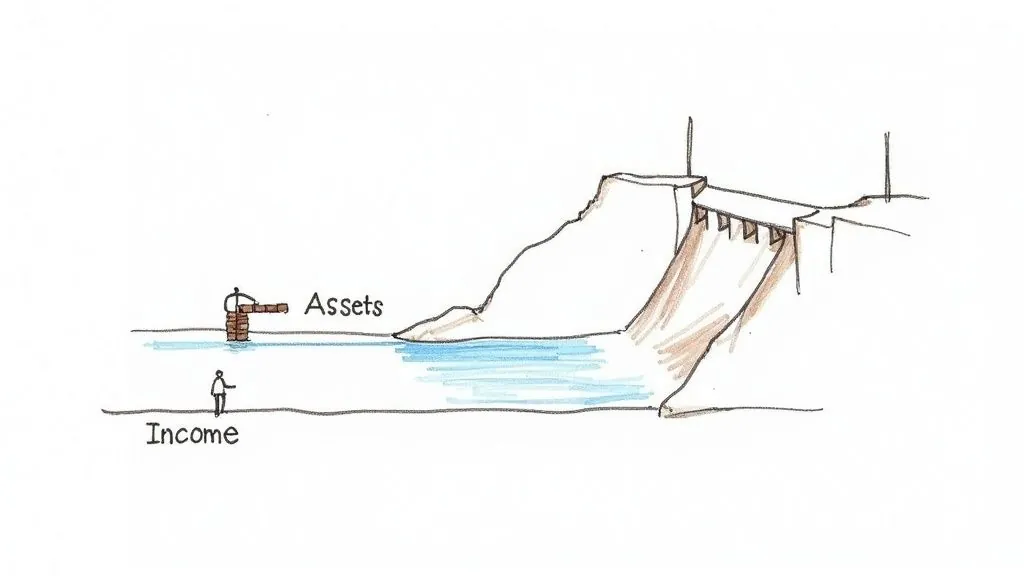

Let’s think of your financial life like a river. Your income is the water, a steady and powerful flow. But if you don’t build anything to capture it, that water just rushes past, spent on everyday expenses and disappearing downstream.

Wealth accumulation is the act of building a dam. It’s how you strategically channel that river of income into a growing reservoir of assets—things like stocks, real estate, and savings.

This reservoir doesn’t just sit there. It gets deeper and wider, eventually creating its own streams of income through interest and returns. This is the real goal: to build a financial engine that can support you, completely separate from your day job. That’s the critical difference between being rich (having a high income) and being wealthy (owning assets that work for you).

The Four Pillars of Your Financial Dam

To really get what wealth accumulation is all about, you have to know what goes into building that dam. Each piece has a specific job in creating a solid financial foundation.

Here’s a quick look at the core components that make it all work.

| Pillar | Role in Wealth Accumulation |

|---|---|

| Income | The fuel for your wealth engine. This is your salary, business profits, side hustles—any money coming in. |

| Savings | The raw material for the dam. It’s the part of your income you don’t spend, set aside specifically for building. |

| Investments | The machinery that makes your reservoir grow faster. This is where you put your savings to work in assets that can increase in value. |

| Assets & Liabilities | The final score. Assets are what you own (cash, stocks, property), while liabilities are what you owe (loans, credit card debt). |

These four pillars work together. You use your income to create savings, which you then use to buy investments (assets). All the while, you’re managing your liabilities to make sure your net worth—your assets minus your liabilities—keeps climbing.

The point of all this isn’t just to pile up money. It’s about building genuine financial freedom and security, where your assets can fund your life and your goals. This whole process is the bedrock of true financial wellness and lasting stability.

Getting a handle on these fundamentals is the first step. When you start strategically managing your income, pushing your savings rate higher, and making smart investment moves, you make the crucial shift from just earning money to actively building a financial future that lasts.

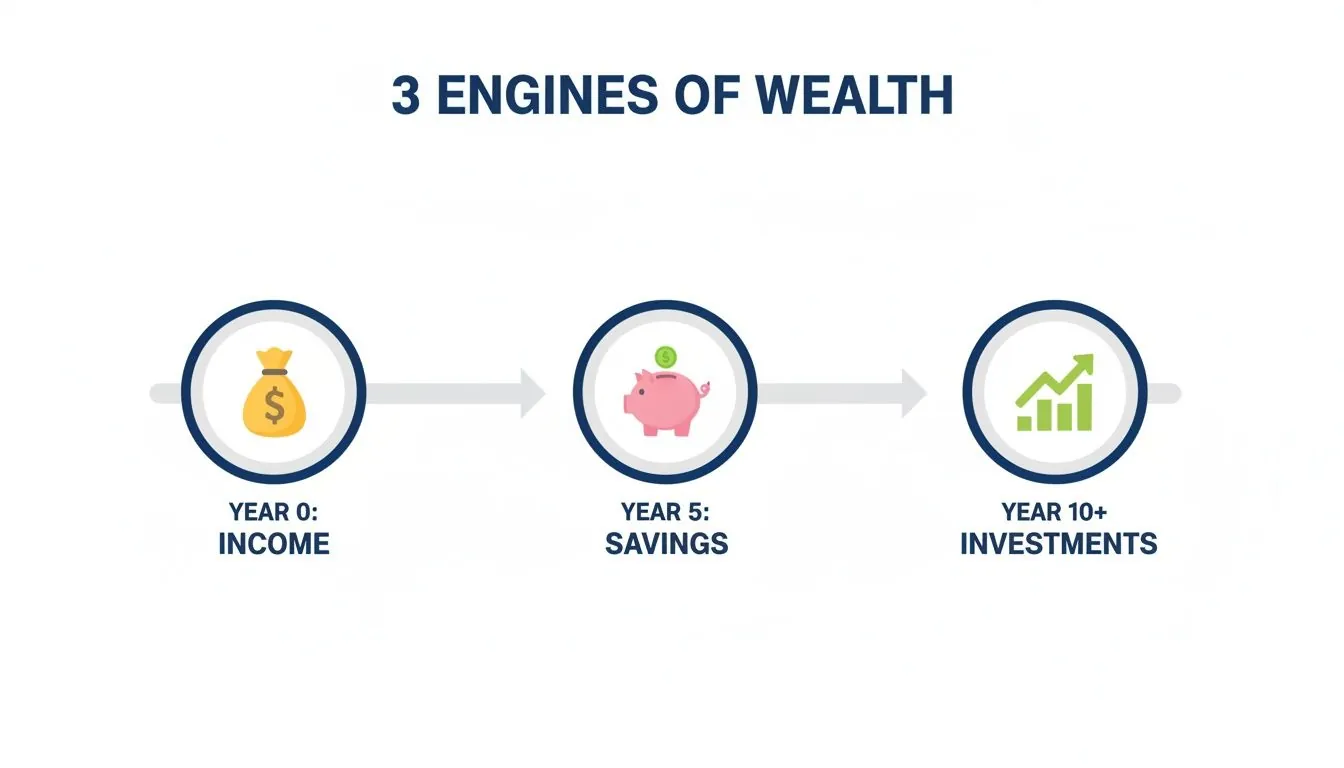

The Three Engines That Power Your Financial Growth

To really get a grip on what wealth accumulation looks like in the real world, you need to understand the three core engines that drive it: income, savings, and investments. These aren’t separate pieces; they work together like a high-performance machine.

Think of it this way: Income is the fuel. Savings is how much of that fuel you actually keep in the tank. And investments? That’s the powerful engine that turns the fuel into unstoppable forward momentum.

Your whole financial journey kicks off with income. It’s the cash flow that fuels everything else. Without it, you’re stuck at the starting line with nothing to save or invest.

But here’s the catch—a huge income doesn’t automatically make you wealthy. Plenty of high earners live paycheck to paycheck because their spending inflates right alongside their salary. The real power comes from the next engine.

Turning Fuel Into Capital With Savings

Savings is the critical bridge between earning money and building wealth. It’s the slice of your income you intentionally decide not to spend. The single most important number here is your savings rate—the percentage of your income you manage to sock away.

A high savings rate acts like a supercharger for your financial engine. It gives you direct control over how fast you can stack up capital to put to work. For example, someone earning $60,000 and saving 25% ($15,000 per year) is on a faster track to building wealth than someone earning $100,000 but only saving 10% ($10,000 per year).

The key takeaway is this: you have far more control over your savings rate than your income or investment returns. It’s the most powerful lever you can pull to speed things up, especially in the early days of your journey.

Igniting Growth Through Investments

Once you’ve got some savings built up, the final engine—investing—roars to life. Just saving money isn’t enough to build serious wealth, mainly because its value gets quietly eaten away over time. To protect your hard-earned capital, you have to be mindful of things like understanding the impact of inflation on your buying power.

Investing is simply the act of using your saved money to buy assets that can grow in value and, ideally, generate even more income.

It’s the difference between storing seeds and planting an orchard.

- Savings: Stashing apple seeds in a jar. They’re safe, but they’re not doing anything.

- Investing: Planting those seeds in good soil. With a little time, water, and sun (think of this as compounding), they grow into trees that produce more apples (your returns) year after year. Those new apples give you even more seeds to plant.

This is where the magic happens. You start shifting from relying only on active income (from your job) to building passive income (from your assets). The ultimate goal of wealth accumulation is to grow your passive income streams until they can cover your lifestyle entirely, freeing you from the need to work. That’s real financial freedom, and it’s all powered by getting these three engines working in perfect harmony.

Navigating the Four Seasons of Your Wealth Journey

Building wealth isn’t a one-time event; it’s a journey that unfolds in distinct phases, a lot like the changing seasons. Each stage of your financial life comes with its own priorities, challenges, and opportunities. Knowing which season you’re in is the key to setting the right goals and making smart moves that fit your timeline.

Think of it like farming: you plant in the spring and harvest in the fall. Your wealth-building strategy has to adapt in the same way. What works for a 25-year-old just starting their career is worlds away from what a 55-year-old needs as they gear up for retirement. This entire journey is powered by three core engines: your income, your savings, and your investments.

This visual breaks down how these three engines work together over the years to fuel your financial growth.

As you can see, there’s a clear progression. Your income fuels your savings, and those savings provide the capital for investments, which then kick off a cycle of growth on their own.

The Spring of Accumulation: Your 20s and 30s

This is your planting season. The main goal here is to lock in strong financial habits. You have an incredible advantage on your side: time. Thanks to the magic of compounding, every dollar you invest now has decades to grow.

- Key Priorities: Your checklist should be simple. Build an emergency fund that covers 3-6 months of expenses. Aggressively pay down high-interest debt like credit cards. And start investing consistently, even if it’s just small amounts. Oh, and capturing an employer 401(k) match? That’s completely non-negotiable—it’s free money.

The Summer of Growth: Your 40s and 50s

Welcome to your peak earning years. Your income is likely the highest it’s ever been, making this the prime time for aggressive growth. The seeds you planted in the spring are now growing into sturdy trees, and it’s time to help them flourish.

Your focus shifts to maximizing your savings rate and fine-tuning your investment portfolio for serious growth. This means maxing out your contributions to tax-advantaged retirement accounts and building a diversified portfolio that can handle the market’s inevitable ups and downs.

This is the stage where you have the greatest power to dramatically accelerate your net worth. The habits you built in your 20s and 30s now pay off exponentially as you funnel larger sums into your investment engine.

The Autumn of Preservation: Your 60s and Beyond

As retirement gets closer, the game changes. The strategy shifts from aggressive growth to smart preservation. You’re no longer trying to hit home runs; you’re focused on protecting the wealth you’ve carefully built over decades.

Your portfolio will likely get more conservative, with a greater emphasis on assets that generate income and less exposure to riskier stocks. This is also when legacy and estate planning move to the forefront. You’ll start thinking about how your assets will be passed on, a major factor in shaping future wealth.

In fact, a massive redistribution of wealth is already underway. Some projections estimate that $83 trillion will be transferred between generations globally in the next few decades. You can dig into more insights on this great wealth transfer in the UBS Global Wealth Report.

Practical Strategies to Accelerate Your Wealth Growth

Knowing the theory behind wealth accumulation is one thing, but actually putting it into practice is where the real magic happens. Speeding up your financial growth isn’t about some secret formula—it’s about taking a deliberate, strategic approach.

It’s about building a system where your money starts working harder for you, turning every dollar of income into a powerful engine for building real assets. These aren’t complicated tricks reserved for the ultra-wealthy. They are practical, actionable steps anyone can take to get their financial snowball rolling downhill, faster.

Master Your Cash Flow with a Purpose-Driven Budget

Let’s get one thing straight: a budget isn’t about restriction. It’s about intention. Think of it as a tool that gives you permission to spend on what truly matters while making sure you’re channeling enough capital toward your biggest goals.

Instead of just tracking where your money went last month, a purpose-driven budget flips the script. You start by identifying what you’re trying to achieve—saving for a down payment, maxing out your retirement account, or hitting a specific net worth milestone. Then, you build your spending plan around those priorities. This simple shift changes your mindset from “What do I have to cut?” to “How do I fund my goals first?”

Automate Your Savings and Investments

If there’s one habit that guarantees you’ll save and invest consistently, it’s automation. This is the classic “paying yourself first” principle, and it’s brilliant because it removes willpower and decision fatigue from the equation entirely.

Set up automatic transfers from your checking account to your savings and investment accounts for the day you get paid. When the money is moved before you even see it, you build wealth in the background without a second thought. This one simple habit ensures your financial dam is constantly being reinforced, drip by drip, paycheck by paycheck.

Leverage Tax-Advantaged Accounts

Taxes are one of the biggest drags on your investment growth. Thankfully, governments have created powerful tools designed to shield your money from the taxman and let it compound much more efficiently.

- 401(k) or 403(b): If your employer offers one, contribute at least enough to get the full company match. It’s an instant, guaranteed return on your money you won’t find anywhere else.

- Traditional IRA: Your contributions might be tax-deductible, which lowers your taxable income today. Your money then grows tax-deferred until you pull it out in retirement.

- Roth IRA: You contribute with after-tax dollars, so there’s no deduction now. But here’s the kicker: your investments grow completely tax-free, and qualified withdrawals in retirement are also tax-free.

Using these accounts is like planting your financial orchard in a super-charged greenhouse, protecting it from the elements and giving it the perfect conditions to grow faster.

While these strategies are accessible to everyone, the reality of wealth accumulation has been incredibly uneven. The top 10% of global wealth holders own roughly three-quarters of total wealth, highlighting how capital tends to concentrate over time. You can read more about these global wealth trends and how assets are distributed worldwide on Allianz.com.

Diversify Your Income Streams

Relying on a single paycheck is like standing on a one-legged stool—it’s inherently unstable. Building multiple income streams creates a vital safety net and dramatically accelerates your ability to save and invest. This doesn’t mean you need to burn yourself out working three different jobs.

Instead, the goal is to create systems that generate money with less active effort over time. You can check out our guide on passive income ideas for beginners to explore options like dividend investing, real estate, or even starting a small online business. Each new stream is another river flowing into your financial reservoir, helping you reach financial independence that much faster.

How to Measure and Track Your Financial Progress

You can’t improve what you don’t measure. In the journey of wealth accumulation, tracking your progress isn’t just another task on the to-do list—it’s the compass that keeps you pointed in the right direction. It turns abstract goals into real, tangible numbers, giving you the clarity and motivation you need to stay the course.

The ultimate scorecard for your financial health is your net worth. This single, powerful number gives you a clean snapshot of where you stand financially at any given moment.

Calculating it is surprisingly simple: just take everything you own (your assets) and subtract everything you owe (your liabilities). Watching this number consistently is the clearest way to see if your wealth-building strategies are actually paying off. Our guide on how to track net worth breaks down the step-by-step process to get you started.

Key Metrics to Monitor

While net worth is the headline number, a few other key performance indicators (KPIs) give you a much deeper look under the hood of your financial engine. Keeping an eye on these helps you spot problems early and find opportunities to kick your growth into a higher gear.

- Savings Rate: This is the percentage of your income you’re stashing away to save and invest. Honestly, it’s the most powerful lever you can pull to speed things up.

- Investment Returns: This metric shows you how hard your money is working for you. It’s crucial for knowing if your investment strategy is actually delivering the growth you need.

- Debt-to-Asset Ratio: This tells you how much of what you own is financed by debt, giving you a crystal-clear picture of your financial risk.

Regularly checking in on these numbers shifts you from passively hoping for the best to actively managing your financial future.

Simplifying Your Financial Overview

Let’s be real—manually pulling data from a dozen different bank accounts, investment platforms, and property records is a total chore. This is where modern tools can make a huge difference, automating the grunt work and saving you a ton of time.

Platforms like PopaDex are designed to pull all your financial information into one simple, visual dashboard.

![]()

This kind of centralized dashboard can show your net worth trend, asset allocation, and account balances at a glance. By consolidating everything, you get rid of the friction of logging into multiple sites and can make smarter, more informed decisions in a fraction of the time.

Seeing your net worth trend line move up and to the right is one of the most powerful motivators you can have. It turns the long, slow process of wealth accumulation into a game you can win, celebrating small victories along the way.

Ultimately, tracking your progress provides the feedback loop you need. It tells you what’s working, what isn’t, and where to focus your energy next, making sure your efforts are always aligned with your biggest goals.

The Common Mistakes That Can Derail Your Wealth Building

Knowing the right strategies is only half the battle. Just as critical is knowing which common financial traps to sidestep on your journey.

Even with the best intentions, a few simple missteps can quietly sabotage your progress. They can slow your journey to financial independence or stop it dead in its tracks. These aren’t complex financial blunders—they’re often subtle habits that eat away at your potential for growth. Understanding them is the first step toward building a more resilient plan.

Letting Lifestyle Inflation Eat Your Gains

One of the sneakiest wealth killers is lifestyle inflation. It’s what happens when your spending rises in lockstep with your income. You land a big raise, and instead of banking the extra cash, you upgrade your car, move to a nicer apartment, or start eating out three times a week.

While it feels completely natural to enjoy the fruits of your labor, letting “lifestyle creep” consume every pay bump means you’re never actually getting ahead. Your savings rate flatlines, and you end up stuck on the financial treadmill, no matter how much your paycheck grows.

The key is to make a conscious choice. When new income comes in, immediately direct a significant chunk of it toward your savings and investments before it ever has a chance to get absorbed into your daily spending.

Falling for Emotional Investing

The stock market is a rollercoaster, and it’s frighteningly easy to get swept up in the emotions of the crowd. When markets are soaring, the fear of missing out (FOMO) can tempt you to pile into hyped-up assets right at their peak. Then, when the market inevitably dips, panic sets in, leading you to sell at the worst possible time and lock in your losses.

These emotional reactions are the mortal enemy of long-term wealth building. A successful strategy requires a cool-headed, disciplined approach—one driven by logic, not fear or greed. The best defense is a good offense: create a solid investment plan based on your goals and timeline, and then stick to it. Tune out the daily noise.

Common triggers for emotional investing include:

- Market Volatility: Sudden drops can trigger a panic-selling reflex.

- “Hot” Stock Tips: Hype from friends or the media can lead to impulsive, poorly researched buys.

- Recession Fears: Widespread economic uncertainty often causes investors to flee to the perceived safety of cash, making them miss the eventual recovery.

“Analysis paralysis is the state of over-thinking a decision to the point that a choice never gets made, thereby creating a paralyzed state of inaction.”

This trap—endlessly researching the “perfect” investment or waiting for the “perfect” time to start—is just as damaging as making a bad decision. In the world of wealth building, consistency and action will beat perfectionism every single time. It’s far better to start investing small amounts in a simple, diversified fund today than to wait years on the sidelines trying to become a market wizard.

By recognizing these pitfalls, you can build defensive habits. Automate your investments, write down a clear plan, and remember that slow, steady progress is the surest path to building lasting wealth.

Common Questions on the Path to Wealth

As you start laying out your financial roadmap, a few big questions always seem to pop up. Getting clear on these early on can give you the confidence to move forward and stick to the plan.

How Much Money Do I Need to Start Investing?

Forget the old myth that you need a pile of cash to get started. These days, you can open an account with a modern brokerage and begin investing with as little as $1. Seriously. The magic of fractional shares means anyone can own a piece of the world’s best companies.

The key isn’t how much you start with—it’s that you start. Building the habit of consistency is what truly builds wealth. A small, automated weekly or monthly contribution is infinitely more powerful than waiting years to save up some imaginary “perfect” amount. The goal is simple: get your money into the game and working for you as soon as you can.

Should I Pay Off Debt or Invest First?

This is the classic financial tug-of-war. The best move almost always comes down to simple math, specifically the interest rate on your debt.

- High-Interest Debt: If you’re carrying debt with an interest rate above 7-8% (think credit cards or personal loans), that should be your number one priority. Paying off a 20% credit card is like earning a guaranteed 20% return on your money. You can’t beat that in the stock market.

- Low-Interest Debt: For things like a mortgage under 5% or a low-rate car loan, the math often flips. Over the long haul, the stock market has historically delivered returns that outpace these low rates, meaning your money could grow faster by being invested.

A smart strategy is often a hybrid one. First, contribute enough to your 401(k) to snag any employer match—that’s free money. Then, throw everything you have at the high-interest debt. Once that’s gone, you can ramp up your investing.

How Long Does It Really Take to Build Wealth?

Building wealth is a marathon, not a sprint. Anyone telling you otherwise is probably selling something. Your personal timeline will boil down to three things: how much you earn, how much you save (your savings rate), and the returns you get on your investments.

Wealth accumulation is a long-term game where consistency beats intensity. For most people, it’s a journey that spans several decades of disciplined saving and investing, powered by the incredible force of compounding interest. The earlier you start, the less you have to save.

Ready to stop guessing and start tracking your financial progress with precision? PopaDex consolidates all your accounts into one simple dashboard, giving you a clear, real-time view of your net worth. See where you stand and make smarter decisions to accelerate your wealth accumulation journey. Start tracking for free at https://popadex.com.