Our Marketing Team at PopaDex

Save on Mortgage with amortization calculator with extra payments

An amortization calculator that handles extra payments is an absolute game-changer. It’s the tool that shows you, down to the penny, how much time and money you can claw back from your lender just by paying a little more than the minimum.

By plugging in one-time or recurring extra payments, you can instantly see your new payoff date and total interest savings. It transforms a vague idea—”I should pay more on my mortgage”—into a concrete, motivating financial plan.

The True Impact of Extra Mortgage Payments

Ever wonder what an extra hundred or two really does to a massive loan like a mortgage? The results are often staggering. Let’s get right into the mechanics to see how every dollar you pay over the minimum works exponentially harder for you.

This powerful effect all comes down to how loans are structured. Interest is front-loaded, meaning in the early years of a mortgage, the vast majority of your payment goes straight to interest. Only a tiny fraction actually chips away at your principal balance.

But when you make an extra payment, you can direct it 100% to the principal.

Why Early Payments Matter Most

Knocking down your principal balance early is the key. Since interest is calculated based on what you still owe, a smaller principal means less interest gets tacked on each month.

This creates a snowball effect of savings that dramatically speeds up your journey to being debt-free. It’s about so much more than just paying off a loan faster; it’s about reclaiming thousands of dollars in interest and gaining years of financial freedom. If you’re new to this, getting a handle on understanding your mortgage basics is a great first step.

A Real-World Mortgage Example

Let’s look at a common scenario to see this in action.

Imagine you take out a $405,000 mortgage—a pretty typical loan size when median home prices are around $400k. On a 30-year term at 6.625% interest, your standard monthly payment is about $2,594. Over the life of the loan, you’d be on track to pay a whopping $539,000 in interest alone.

But what if you added just $200 extra to your payment each month?

Let’s break down the difference that small change makes.

Standard vs Extra Payment Mortgage Scenario At a Glance

Here’s a side-by-side look at how that extra $200 per month completely transforms the loan.

| Metric | Standard Payment Plan | With $200 Extra Monthly Payment |

|---|---|---|

| Loan Payoff Time | 30 Years (360 months) | 24 Years, 5 Months (293 months) |

| Total Interest Paid | ~$539,000 | ~$423,177 |

| Total Savings | $0 | $115,823 in interest saved |

| Time Saved | 0 | 67 months (5 years, 7 months) |

The numbers don’t lie. That small, consistent effort of paying an extra $200 shaves over five and a half years off the mortgage and keeps over $115,000 of your hard-earned money in your pocket.

This is exactly why an extra payment calculator is so powerful. It makes these long-term benefits tangible today, giving you a clear roadmap to becoming debt-free faster than you ever thought possible.

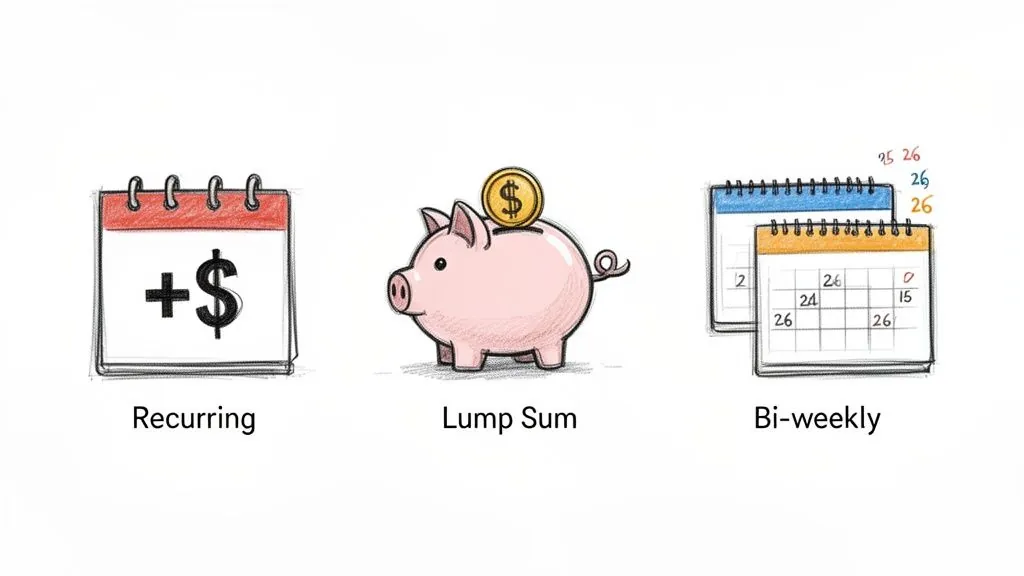

Finding the Right Extra Payment Strategy for You

Let’s be real: accelerating your loan payoff isn’t a one-size-fits-all deal. The best method really boils down to your own financial habits and how your cash flow works. The trick is to figure out a sustainable rhythm, whether that means steady, consistent payments or bigger, opportunistic ones.

The goal here is simple: pick a strategy you can actually stick with. For a lot of people, this means baking a small, extra amount into their monthly budget and putting it on autopilot. Others might find it easier to throw unexpected windfalls—like a bonus or tax refund—at their principal balance to make a serious dent.

Recurring Monthly Additions

This is probably the most common—and for good reason, the most effective—strategy out there. Just by adding a consistent, budgeted amount to each monthly payment, even if it’s just $100 or $200, you’re constantly chipping away at that principal. It’s a brilliant way to put the power of compounding savings to work for you, month after month.

The biggest win here is predictability. You set it up once and just let it roll, turning a small, manageable sacrifice into massive long-term savings without much ongoing effort. It’s the perfect move if you thrive on routine and want to build debt reduction right into your regular financial plan. For some ideas on how to structure this, our guide on creating a debt payoff calculator spreadsheet is a great place to start.

One-Time Lump Sum Payments

Ever get an annual bonus, a nice tax refund, or maybe even an inheritance? Dropping that cash on your loan as a one-time lump sum payment can have a truly dramatic effect. When you make a large, targeted payment straight to the principal, you can instantly wipe out years of future interest payments.

This approach works great for people with variable income or those who prefer to attack debt with significant, opportunistic hits rather than smaller monthly ones.

Pro Tip: When you’re making a lump-sum payment, always contact your lender and specify that you want the entire amount applied directly to the principal. If you don’t, they might just apply it to future scheduled payments, which completely cancels out the interest-saving benefit.

The Bi-Weekly Payment Method

The bi-weekly plan is a sneaky-smart way to squeeze in an extra payment each year without really feeling it. Instead of making 12 monthly payments, you make a half-payment every two weeks. Since there are 26 two-week periods in a year, this adds up to 13 full monthly payments annually.

This strategy has been a stealth weapon in mortgage amortization since the 90s. That extra payment painlessly speeds up your payoff schedule. And with prepayment penalties now affecting just 2% of U.S. loans as of 2024, most borrowers can try it out risk-free. Run the numbers in an amortization calculator with extra payments, and you’ll see this can easily shave four to eight years off a typical loan. MortgageCalculator.org has a great tool that shows you how this saves thousands in interest.

How to Build Your Own Amortization Calculator

While online tools get the job done quickly, there’s a certain power in building your own amortization calculator from scratch in a spreadsheet. It’s like looking under the hood of your loan—you get unparalleled control, demystify the numbers, and can play with unlimited “what-if” scenarios.

Let’s walk through how you can create a powerful, personalized tool in Google Sheets or Excel.

First things first, you need to set up your core input fields. Think of these as the control panel for your entire calculator. Pop them right at the top of your sheet so they’re easy to find and tweak.

- Loan Amount: The total principal you borrowed (e.g., $350,000).

- Annual Interest Rate: Your loan’s yearly interest rate (e.g., 6.75%).

- Loan Term (Years): The original length of the loan (e.g., 30).

- Payments Per Year: This is almost always 12 for a standard mortgage.

- Start Date of Loan: The date of your very first payment.

Getting these right is key, as every other calculation will pull from these cells.

Setting Up Your Amortization Table

Now for the main event: the amortization schedule itself. This table is where you’ll see the magic happen, breaking down every single payment and showing your balance shrink over time.

You’ll want to create six main columns:

- Payment Number

- Beginning Balance

- Principal Paid

- Interest Paid

- Extra Payment

- Ending Balance

This layout gives you a crystal-clear, payment-by-payment view of your loan’s journey. That “Extra Payment” column is our secret weapon—it’s where you’ll model how throwing extra cash at your principal can change everything. If you want to see how other financial tools are structured, exploring different mortgage calculators can give you some great ideas.

The Formulas That Power Your Calculator

With the structure in place, it’s time to bring it to life with formulas. Luckily, most spreadsheet programs have built-in financial functions that do the heavy lifting for us.

The most important one is for your scheduled monthly payment. In Excel or Google Sheets, the PMT function is your best friend here. It calculates the fixed payment for a loan based on a constant interest rate. The formula generally looks like this: =PMT(rate, nper, pv). Here, rate is the interest rate per period, nper is the total number of payments, and pv is the loan amount.

To figure out how much of that payment actually chips away at your loan, you’ll use the PPMT function. It tells you the principal portion for any given payment. And for the bank’s cut? The IPMT function calculates the interest portion. These two functions are the engine of your amortization schedule.

Crucial Insight: The entire system works because the Ending Balance for one row becomes the Beginning Balance for the next. Your Ending Balance formula should be simple:

Beginning Balance - Principal Paid - Extra Payment. This little formula is vital because it ensures any extra payments immediately cut down the principal for the next month’s interest calculation.

Making It Dynamic with Extra Payments

This is where your homemade calculator really shines. To create a truly powerful amortization calculator with extra payments, you need to make it interactive. Set up some dedicated cells near your main inputs to handle different types of extra payments.

- Recurring Extra Payment: Create a single cell where you can type in a fixed amount (say, $250) that gets added to every single payment.

- One-Time Extra Payment: This one is slightly more advanced. Set up a small table with two columns: one for the payment number (or date) and another for the lump-sum amount. Your “Extra Payment” column formula can then use a lookup function (like

VLOOKUPorXLOOKUP) to pull this amount in at exactly the right time.

By structuring it this way, you can instantly see the impact of adding a consistent $250 a month versus making a single $10,000 payment in year five. For a deeper look at the math behind this, our guide on the mortgage amortization calculator breaks it down even further. When you build this yourself, you gain a deep, intuitive understanding of how to accelerate your journey to being completely debt-free.

See Your Way to a Paid-Off Home

Let’s be honest, staring at a spreadsheet full of numbers is hardly inspiring. To really stay motivated on the long road to paying off your mortgage, you need to see your progress. This is where a good amortization calculator with extra payments shines—it turns that boring data into charts that actually mean something.

These visuals make the numbers real. Most calculators will spit out a payoff chart that shows two critical lines. One tracks your loan balance with just the standard payments. The other, much steeper line, shows how quickly that balance drops when you throw in your extra contributions. It’s instant, tangible proof that your hard work is paying off.

From Data to a Dynamic Roadmap

To see this in action, imagine a $500,000 loan. A simple line graph will immediately show a huge wedge-shaped area between the two payoff curves. That “wedge” isn’t just empty space; it represents the thousands of dollars in interest you’re saving and all the years you’re shaving off your mortgage term.

Once you understand these charts, your static amortization schedule becomes a dynamic roadmap. It helps you make smarter decisions, like figuring out the best time to make a lump-sum payment. You can literally see how a bonus you apply in year three saves way more interest than that same amount would if you waited until year twenty.

A visual amortization chart does more than just track progress—it gamifies your debt reduction. Watching the ‘extra payment’ line dive below the ‘standard’ line provides a powerful psychological boost, encouraging you to stay the course.

This strategy is more important than ever. With millions of new mortgages locked in at higher rates, finding ways to pay them down faster is crucial. Financial experts have shown just how big a difference extra payments can make. For a $500,000, 30-year loan at 6.8%, adding a modest $500 extra each month can save you over $182,000 in interest and get you mortgage-free seven years sooner.

The payoff charts in these calculators make that gap crystal clear—plotting the difference between a 360-month slog and a much quicker 276-month finish line. It’s an incredible visual reminder of the power of chipping away at your principal early and often. For more examples of how extra payments can accelerate your payoff, check out the resources at Allstate.com.

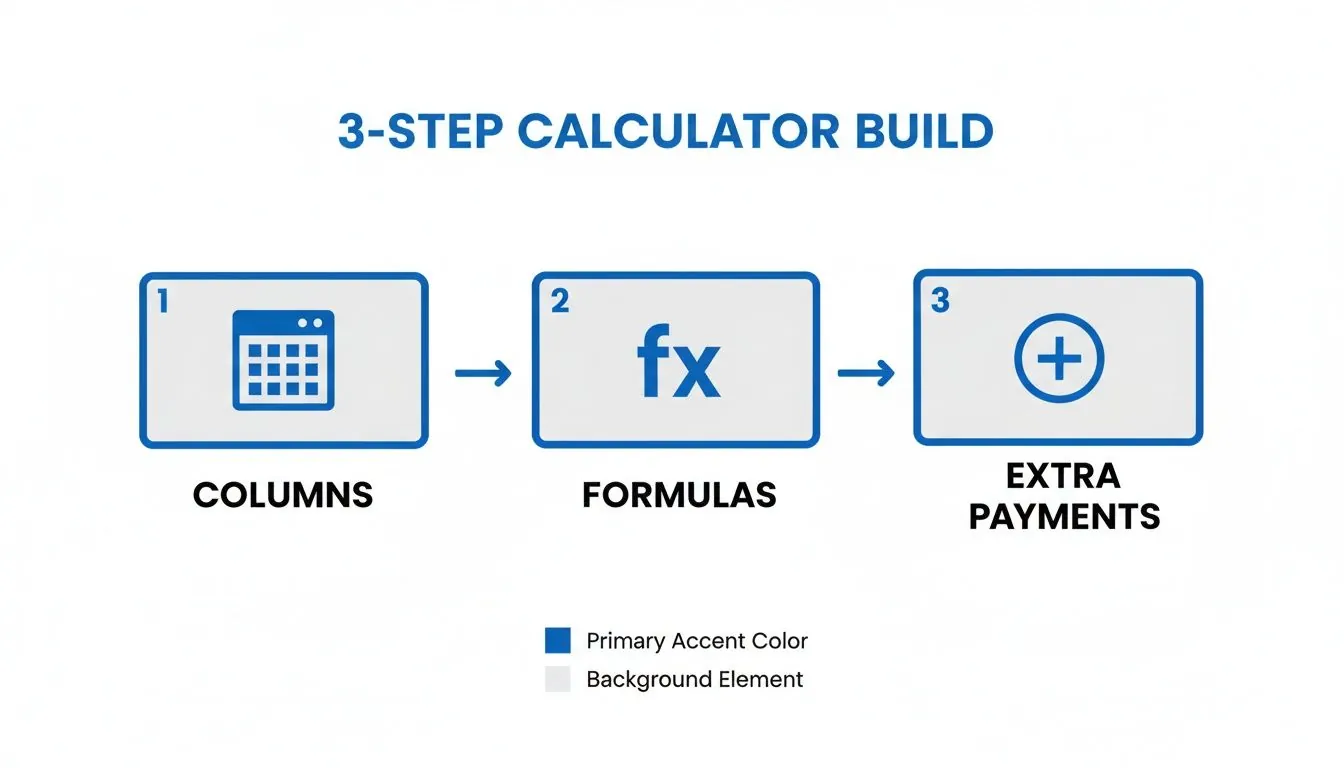

Putting It All Together Visually

As we covered earlier, building your own calculator in a spreadsheet comes down to three main parts: setting up your columns, plugging in the right formulas, and adding fields for your extra payments.

This simple three-step process is all it takes to create the foundation. From there, you can generate the powerful visuals that will map out your journey to finally owning your home free and clear.

Connecting Your Mortgage Payoff to Your Net Worth

Making extra payments on your mortgage isn’t just about getting out of debt sooner; it’s one of the most direct ways to build wealth. Every extra dollar you send to your lender hits your largest liability, giving your net worth a guaranteed, measurable boost. It’s a powerful financial move with a predictable return.

Think about the simple net worth equation: Assets - Liabilities = Net Worth. Your home is probably your biggest asset, but the mortgage tied to it is your biggest liability. As you aggressively chip away at that mortgage principal, you’re literally converting debt into equity, increasing your net worth dollar for dollar.

From Calculator Data to Your Personal Balance Sheet

This is where the real magic happens. The numbers you get from an amortization calculator with extra payments aren’t just figures on a screen—they’re the blueprint for your financial growth. You walk away with two critical pieces of information: your new, faster payoff date and a clear projection of your equity growth.

You can take this data and plug it straight into your personal balance sheet, whether you use a dedicated tool like PopaDex or a simple spreadsheet you’ve built yourself. Instead of just seeing your mortgage balance trickle down once a year, you can map out its rapid decline based on your accelerated schedule.

Your accelerated amortization schedule is more than a debt-reduction plan—it’s a real-time wealth creation engine. By tracking it, you transform a liability into a visible, growing asset on your personal balance sheet.

This simple step gives you a forward-looking view of your entire financial picture. You stop being a passive bill-payer and become an active manager of your largest asset, watching your equity—the part of the home you actually own—climb faster than you ever thought possible.

Integrating Your Progress for a Complete Financial Picture

For anyone managing assets in different currencies, this kind of integration is even more critical. Paying down a mortgage in one currency has a direct and significant impact on your total net worth when you look at your entire global portfolio. A clear tracking system makes sure you never lose sight of the complete picture.

Here’s how you can turn your calculator’s projections into an actionable tracking system:

- Update Your Liability Schedule: Take the new amortization schedule and use it to project your mortgage balance month by month. Update your net worth tracker to reflect this much faster decline.

- Track Your Home Equity: As your loan balance drops, your home equity skyrockets. Chart this growth right alongside your other investments to see exactly how your real estate asset is performing.

- Set New Financial Milestones: That new payoff date isn’t just an endpoint; it’s a new beginning. Use it to set fresh goals. Maybe you’ll be mortgage-free five years earlier—what could you do with all that freed-up cash flow?

By actively connecting your mortgage payoff strategy to your overall net worth, you gain a much clearer, more motivating view of your financial journey. You’re not just killing off a debt; you are systematically building a more secure and prosperous future for yourself.

Common Questions About Extra Mortgage Payments

Once you start playing with an amortization calculator with extra payments, you’ll see just how powerful a few extra dollars can be. But it’s natural for some questions to pop up. Making extra payments is a brilliant move, but doing it the right way is what unlocks all the savings.

Let’s walk through some of the most common things people wonder about when they’re ready to start attacking their mortgage.

How Do I Ensure My Extra Payment Goes to Principal?

This is, without a doubt, the most important part of the entire strategy. You have to be crystal clear with your lender: any extra money you send must be applied directly to the principal balance only.

If you just toss extra money into your payment without instructions, many lenders will simply hold it and apply it to your next month’s bill—principal, interest, and all. That completely defeats the purpose and saves you nothing.

Here’s how to make sure every dollar counts:

- Use the Online Portal: Most lenders have a specific field in their online payment system labeled “additional principal payment” or something similar. Use that box. Every single time.

- Mail a Check? Be Specific: If you’re old-school and mailing a check, write “For Principal Only” and your loan number in the memo line. You can’t be too obvious about it.

- Always Verify: This is non-negotiable. After you make an extra payment, check your next monthly statement. Confirm that the extra funds were applied correctly and that your principal balance dropped by that exact amount.

A simple instruction is the difference between saving tens of thousands in interest or just paying next month’s bill early. Never assume your lender knows what you want—tell them.

Monthly Extras vs. a Yearly Lump Sum

Ah, the classic debate. Is it better to chip away with smaller, consistent payments or save up for one massive payment once a year?

From a pure math perspective, the sooner you reduce the principal, the more interest you save. This makes smaller, extra payments each month the winner. Each time you knock down the principal, even by a little, the next month’s interest calculation is based on that smaller balance. It creates a compounding effect of savings over the year.

A big lump sum from a work bonus is always a fantastic move, but don’t wait for it. If you can afford to send extra now, do it now.

Should I Pay Down My Mortgage or Invest?

This is one of the biggest questions in personal finance, and the “right” answer really depends on your risk tolerance and the numbers involved.

Think of it this way: the “return” you get from an extra mortgage payment is guaranteed. It’s exactly equal to your loan’s interest rate. If your mortgage is at 6.5%, paying it down is like earning a risk-free 6.5% on your money. You can’t lose.

The alternative is to invest that cash. If you’re confident you can beat your mortgage rate with after-tax returns in the stock market, that route could be mathematically better. But don’t underestimate the psychological win of owning your home outright. For many people, that feeling of total financial security is priceless.

Can I Use This Calculator for Other Loans?

Absolutely! The math behind amortization works the same for most installment loans. You can easily adapt this kind of calculator or spreadsheet for:

- Auto Loans

- Personal Loans

- Private Student Loans

Just plug in the loan’s principal, interest rate, and term. The extra payment feature is especially powerful against high-interest debt, where you can slash interest costs even more dramatically than on a mortgage.

Ready to see how an accelerated mortgage payoff fits into your total financial picture? With PopaDex, you can track your shrinking mortgage balance alongside all your other assets and watch your net worth climb. Start your free trial at PopaDex.com today and see it all in one place.