Our Marketing Team at PopaDex

Consolidate Bank Accounts for Simpler Finances

Juggling multiple bank accounts can feel like trying to solve a puzzle with pieces from different boxes. You might have a checking account from your college days, a joint account with your partner, and maybe a high-yield savings account you opened for a good rate. Each has its own login, its own rules, and its own monthly statement. It’s a lot to track, and honestly, it’s easy for things to slip through the cracks.

To consolidate bank accounts is to consciously simplify your financial life. It means closing those extra, redundant accounts and funneling your money through one primary checking and one primary savings account. The result? Immediate clarity and a much firmer grip on your finances.

Why Consolidating Bank Accounts Is a Smart Move

When your money is scattered across different banks, getting a clear, real-time picture of your financial health is nearly impossible. You’re constantly toggling between apps and trying to piece together a mental budget. It’s not just inconvenient; it creates mental clutter and financial blind spots.

Bringing everything under one roof creates a single source of truth for your money. This goes beyond being tidy—it’s a strategic move that gives you a real advantage.

Here’s a quick look at the major wins you can expect when you simplify your banking setup.

Key Benefits of Bank Account Consolidation

| Benefit | How It Helps You |

|---|---|

| Fewer Bank Fees | Less exposure to monthly maintenance charges, low-balance penalties, and other sneaky fees that chip away at your savings. |

| Simpler Budgeting | When all your income and spending flow through one place, tracking where your money goes becomes incredibly straightforward. |

| Tighter Financial Oversight | A unified view makes it easier to spot strange transactions, catch potential fraud early, and identify opportunities to save more. |

Ultimately, consolidating your accounts gives you a clearer, more accurate financial story without all the noise.

Gaining Real Clarity and Control

The biggest payoff from consolidation is cutting through the financial static. Instead of spending time cobbling together data from different statements, you can answer the most important question—”Where is my money really going?”—in seconds. That kind of focus is what empowers you to make smarter, more intentional financial decisions. For a complete overview of where you stand after consolidating, use our free Excel net worth tracker to see all your accounts in one place.

This push for simplicity is more than a personal finance hack; it’s a trend that has reshaped the entire banking industry. In fact, over the last 40 years, the number of banking institutions in the United States has dropped by an incredible 75% since the early 1980s. You can read more about how the banking market is changing on Morgan Stanley’s blog. This massive industry shift toward efficiency is a powerful lesson you can apply directly to your own wallet.

By bringing your finances under one roof, you aren’t just tidying up; you’re building a more resilient and transparent financial foundation. It’s the first practical step toward taking command of your financial future.

After Consolidation: Build a Single Source of Truth

Closing extra accounts is only step one. Step two is tracking all remaining checking, savings, and investment accounts in one dashboard so your monthly review is fast and consistent.

A practical setup looks like this:

- Keep one operating checking account and one high-yield savings account.

- Keep specialist accounts only when they have a clear role (for example, brokerage or tax reserves).

- Track every active account in one place and review net worth monthly.

If you’re comparing tools to do this, start with our personal finance dashboard comparison.

Consolidated Accounts Work Best With One Dashboard

Use PopaDex to track every remaining bank and investment account after consolidation, so you can monitor cash flow, net worth, and progress without spreadsheet sprawl.

Your Pre-Consolidation Financial Checklist

Jumping into account consolidation without a plan is a recipe for missed payments and late fees. A smooth transition starts with solid prep work. Think of it as creating a financial blueprint before you start knocking down walls—you need a complete picture of your financial plumbing to avoid any nasty surprises.

Jumping into account consolidation without a plan is a recipe for missed payments and late fees. A smooth transition starts with solid prep work. Think of it as creating a financial blueprint before you start knocking down walls—you need a complete picture of your financial plumbing to avoid any nasty surprises.

Your first move? Gather the last three to six months of bank statements from every single account you plan on closing. This paper trail is a goldmine of information, revealing every automated transaction you might have forgotten about.

Create Your Financial Inventory

With your statements in hand, it’s time to map out all the automated activity tied to those old accounts. The goal here is to create a master list of every single financial connection. Don’t gloss over anything, no matter how small it seems.

Your inventory should pinpoint:

- Direct Deposits: This is usually your paycheck, but don’t forget other income sources like freelance work (a dedicated bank account for freelancers can simplify this), government benefits, or even investment dividends.

- Automatic Bill Payments: Comb through your statements line by line for any recurring charges. We’re talking about the big stuff like your mortgage or rent, utilities, insurance premiums, and car payments, plus any automated credit card payments.

- Recurring Subscriptions: These are the ones that are so easy to miss. Think Netflix, Spotify, gym memberships, and software subscriptions. A failed payment here can be a major headache.

- Scheduled Transfers: Make a note of any automatic transfers you’ve set up, whether it’s moving money to savings, a child’s account, or an investment portfolio.

I can’t stress this enough: creating this detailed inventory is the single most important step in the entire process. It’s what stands between you and the chaos of a declined card or an unexpected late-payment notice.

Getting a handle on these financial commitments is a cornerstone of smart personal finance. If you’re just getting started, our guide on https://popadex.com/financial-planning-for-beginners is a fantastic resource. This level of organization is even more critical for major life changes, making it a key part of successful financial planning for international retirement.

Choosing the Right Primary Bank Account for You

This is probably the single most important decision you’ll make when you consolidate bank accounts. You aren’t just picking a new logo; you’re choosing a financial partner for your daily life. The “best” bank doesn’t exist—the right choice hinges entirely on your lifestyle, your financial goals, and what you actually value in a banking relationship.

So, what really matters to you? Is it the convenience of walking into a nearby branch for face-to-face help? Or are you hunting for the absolute highest interest rates on your savings? Your answer is the first step in deciding between a traditional brick-and-mortar bank and a modern online-only option.

This decision is more relevant than ever, as the banking world itself is consolidating. In 2025, a whopping 48% of U.S. bank executives said their teams would consider a merger. The main reasons? To gain the scale needed for tech investments (43%) and to expand their geographic footprint (37%). As banks combine, their services and fees can change overnight, making your initial choice even more critical. You can dig into the strategic motivations behind bank mergers in recent industry reports.

Evaluating Key Account Features

Before you commit, you have to look past the slick marketing and dive into the fine print. These are the details that will impact your money day in and day out.

Here’s a practical checklist for your evaluation:

- Fees and Minimums: Hunt for accounts with no monthly maintenance fees or with balance requirements you can easily meet. What are the charges for overdrafts, wire transfers, or using an out-of-network ATM?

- Interest Rates (APY): Compare the Annual Percentage Yield on both checking and savings accounts. You’ll almost always find that online banks offer significantly higher rates.

- Technology and Accessibility: A top-notch mobile app is non-negotiable today. It needs to have mobile check deposit, dead-simple transfers, and rock-solid security features.

- Customer Service: How do you get help when something goes wrong? Check for 24/7 phone support, secure online chat, or the option for in-person help if that’s important to you.

Pro Tip: I always recommend this to friends: open a “test” savings account with a small deposit at a bank you’re eyeing. Use their app and website for a few weeks. This gives you a real feel for the user experience before you go through the hassle of moving your entire financial life.

Brick-and-Mortar vs. Online Banks: A Quick Comparison

Ultimately, your decision often boils down to this classic matchup. Neither is universally “better”—they just serve different priorities.

| Feature | Traditional Bank | Online-Only Bank |

|---|---|---|

| Best For | Relationship-based services, handling complex transactions (like a mortgage), and getting in-person support. | Maximizing interest rates, people who are comfortable with tech, and avoiding most common banking fees. |

| Key Pro | Access to a physical branch and a team of tellers and bankers you can talk to face-to-face. | Higher APYs and lower overhead costs, which means more savings for you. |

| Key Con | Often saddle you with lower interest rates and a longer list of potential fees. | No physical branches, which can make depositing cash a real headache. |

A Practical Guide to Making the Switch

Alright, you’ve picked your new primary bank. Now for the fun part: actually making the move. A little organization here goes a long way in preventing missed payments or surprise fees down the road. The first step is simple—open and fund your new account.

I always recommend starting small. Just transfer enough to get the account active and satisfy any minimum balance rules. This gets the ball rolling without moving all your money at once, giving you some time to play around with the new app and get a feel for things.

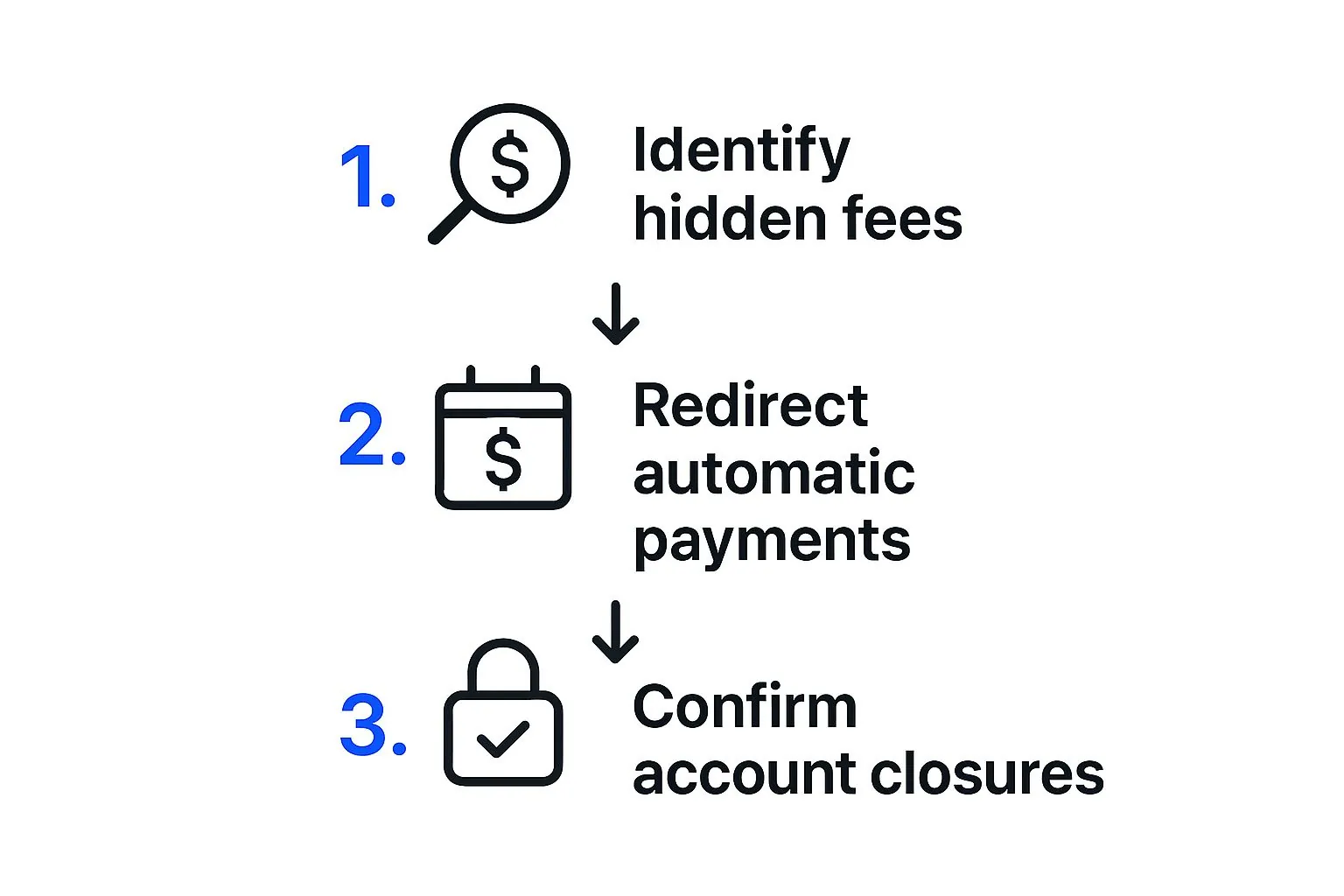

Redirecting Your Financial Traffic

This next part is where precision really counts: rerouting all your automated financial activity. Start with the easy one—your direct deposits. Grab your new account and routing numbers and update your payroll information or any other source of recurring income.

Next up, it’s time to tackle your automatic payments. Pull out that list you made earlier and start updating your payment details for every single one. Think about everything:

- Mortgage or rent payments

- Utility bills and insurance premiums

- Car loans and credit card bills

- Those sneaky streaming services and gym memberships

This visual gives a good, quick overview of how the process should flow.

As you can see, it’s all about a logical sequence: identify what you have, redirect it, and then double-check that it worked. Skipping a step is how you end up with late fees and headaches.

My Pro Tip: Don’t be in a rush to close your old accounts. Leave them open with a small buffer—maybe $50 or $100—for at least one full billing cycle. This gives you a safety net to catch any payments you might have missed before you fully cut ties.

Finalizing the Consolidation

Once you’ve seen all your direct deposits land in the new account and all your auto-payments come out correctly, you’re in the home stretch. It’s finally time to close out the old accounts. Transfer any leftover cash to your new primary account, making sure the old balances hit zero.

Your last step is to call your old banks and have them formally close each account. Make sure to ask for written confirmation that the account has been closed with a zero balance. Trust me, you want this piece of paper. It’s your proof if any weird “zombie fees” pop up on a supposedly dead account later. This kind of cleanup is a huge part of good financial hygiene, and you can learn more about how to organize your finances in our other guides.

Optimizing Your New Streamlined Finances

Getting your accounts consolidated is a huge win, but your work isn’t quite over. In fact, this is where the real fun starts. The first month is all about making sure everything landed in the right place. Keep a close eye on your new primary account to verify that all your automated financial traffic—from paychecks to bill payments—is flowing smoothly. No surprise late fees, please.

Getting your accounts consolidated is a huge win, but your work isn’t quite over. In fact, this is where the real fun starts. The first month is all about making sure everything landed in the right place. Keep a close eye on your new primary account to verify that all your automated financial traffic—from paychecks to bill payments—is flowing smoothly. No surprise late fees, please.

With your finances finally simplified, you can shift your focus from organizing to optimizing. This is your chance to turn that tidy setup into a powerful engine for building wealth. Think of it this way: consolidation was the first, essential step. Now you’re ready to truly master financial management for whatever goals you have, personal or business.

Supercharge Your Financial Habits

A simplified view of your money makes it so much easier to be proactive. Instead of just letting your cash sit there, now’s the perfect time to explore your new bank’s features and put that money to work.

Here are a few things you can do right away:

- Automate Your Savings: This is a classic for a reason. Set up recurring transfers to your savings or investment accounts that trigger the day your paycheck hits. Pay yourself first.

- Explore Budgeting Tools: Most modern banks have built-in tools that categorize your spending, and pairing them with one of the best free budgeting apps can be even more powerful. It’s an eye-opening way to see exactly where your money is really going each month.

- Set Real Financial Goals: Whether you’re saving for a down payment or just a much-needed vacation, use this newfound clarity to set tangible goals you can actually track. A Google Sheets net worth tracker can help you visualize your progress toward those milestones over time.

Your simplified account is more than a place to hold money; it’s a launchpad for building smarter financial habits. The clarity you’ve gained is your greatest asset for future growth.

This strategy of simplification goes beyond a personal finance hack; it’s happening across the banking industry. A global banking outlook report shows that as interest rates potentially fall in 2025, banks will be pushed to consolidate and streamline their own operations.

If you’re ready to take your new setup even further, check out our guide on how to organize your finances.

Have Lingering Questions About Consolidation?

You’re almost at the finish line, but it’s totally normal to have a few last-minute questions pop up. Making a big change to how you manage your money is a big deal, and you want to be sure you’ve covered all your bases. Let’s tackle some of the most common worries people have right before they make the final switch.

Will This Mess Up My Credit Score?

This is probably the #1 concern I hear, and the answer is usually a relief. For the most part, closing a standard checking or savings account has no direct impact on your credit score.

Why? Because these types of deposit accounts aren’t about borrowing money, so they aren’t reported to the big credit bureaus like Equifax, Experian, or TransUnion. Your credit history is all about how you manage debt, not how you manage your cash.

Now, there is one small exception. If the checking account you’re closing has an overdraft line of credit attached, that is a form of credit. Closing it will reduce your total available credit, which could cause a very minor, temporary dip in your score.

What About Consolidating With a Partner?

Joining finances is a huge milestone for any couple. It’s a practical move that makes budgeting, paying bills, and saving for big goals like a house or vacation so much simpler. It’s about building a financial life together.

The actual process is pretty straightforward:

- Pick a bank together. You can either add one partner to an existing account or start fresh with a brand-new joint account.

- Show up as a team. Banks will almost always require both people to be physically present with valid IDs to open a joint account or add a name to an existing one.

- Redirect your finances. Once the new joint account is ready, you can start moving your direct deposits and automatic payments over. A systematic approach works best here.

When you manage money together, you’re agreeing on your hopes, dreams, and goals—and on how to reach them. It removes secrecy around spending and creates a powerful sense of financial unity.

Simplify Your Financial Life

PopaDex helps you track all your accounts in one place with our net worth dashboard, plus grow your savings with 4.5% APY.

Getting rid of the old, scattered accounts and moving forward with one clear financial hub is an incredibly empowering step.

After you’ve successfully consolidated your bank accounts, the real fun begins: seeing your entire financial world in one place. With PopaDex, you can track your net worth, watch your investments grow, and get a real-time snapshot of your progress. See what financial clarity feels like by visiting us at https://popadex.com.