Our Marketing Team at PopaDex

7 Essential Expense Tracking Categories for 2026

Ever feel like your money vanishes into thin air? The problem isn’t your willpower; it’s your system. Without a clear framework, tracking your spending becomes a guessing game, and your budget never quite sticks. Effective financial management hinges on one crucial element: well-defined expense tracking categories.

This goes beyond listing where your money goes. It’s about creating a roadmap that reveals your actual spending habits, highlights hidden savings opportunities, and empowers you to take decisive control. A generic, messy list of expenses won’t work. To build real wealth and reduce financial stress, you need a structured approach that clearly separates needs from wants and fixed costs from variable ones.

This guide moves beyond generic advice to provide a comprehensive breakdown of the essential categories that form the backbone of any successful financial plan. We will explore a detailed system for organizing your finances, complete with practical examples and actionable insights. You will learn how to transform your budget from a source of anxiety into a powerful tool for achieving your goals, whether you’re a gig worker with irregular income, a young professional building wealth, or an investor optimizing your portfolio.

1. Housing and Utilities

For most households, housing and utilities represent the largest and most significant of all expense tracking categories. This foundational category covers all costs associated with keeping a roof over your head and maintaining a habitable living space. It’s the cornerstone of any budget, often consuming between 25-35% of total income.

This category is a blend of fixed and variable costs. Fixed costs are predictable and consistent, such as your monthly rent or mortgage payment. Variable costs, like electricity or water bills, can fluctuate based on seasonal usage or other factors. Properly tracking these expenses is crucial for financial stability and long-term planning.

What to Include in This Category

To effectively manage this part of your budget, it’s important to capture all related costs. Be sure to include:

- Primary Payments: Rent or mortgage payments.

- Essential Services: Electricity, water, natural gas, and trash collection.

- Connectivity: Internet and home phone services.

- Property Costs: Property taxes and homeowners’ or renters’ insurance.

- Upkeep: Routine maintenance, HOA fees, and unexpected repair costs (e.g., a plumbing emergency or appliance fix).

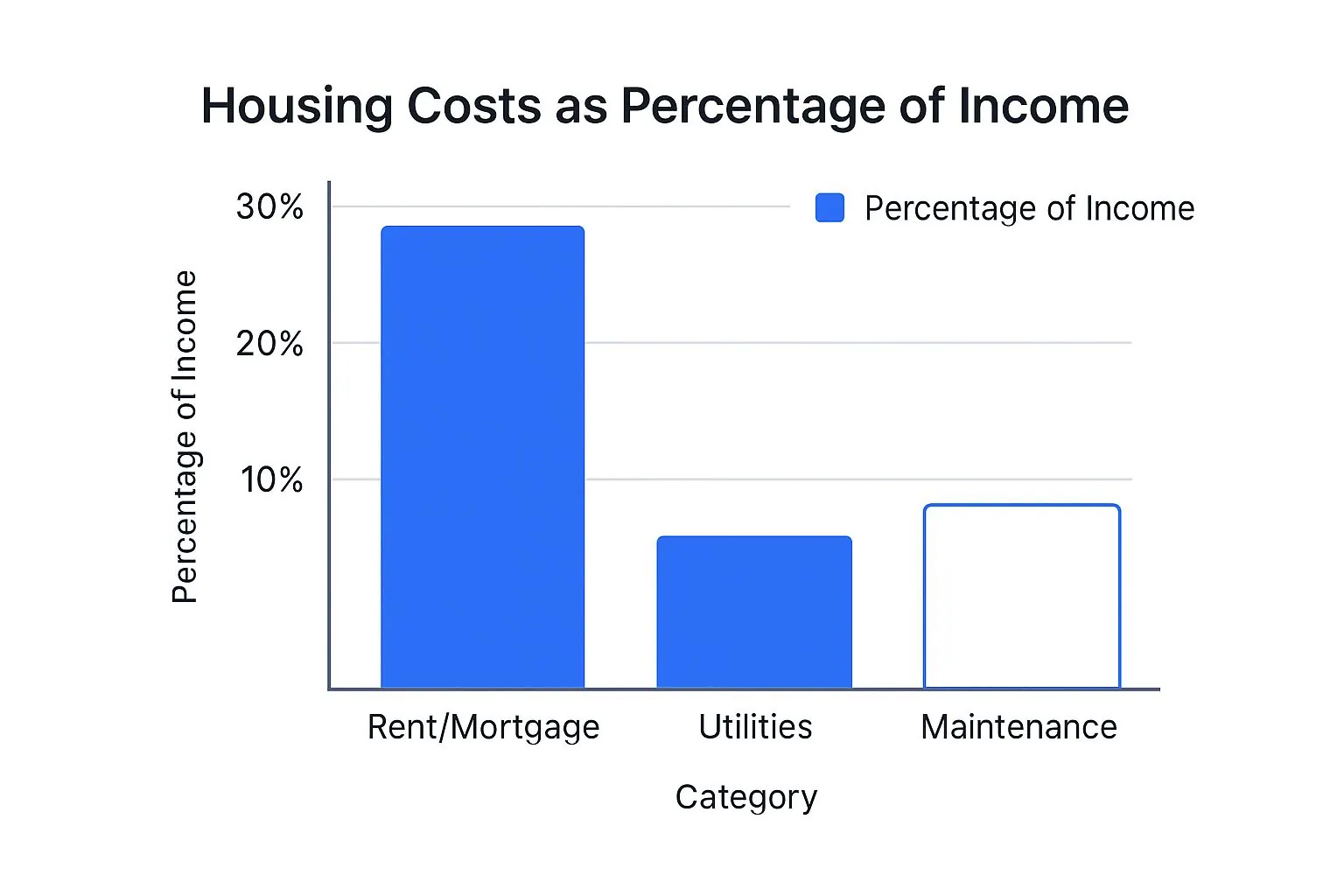

The bar chart below illustrates how these expenses typically break down as a percentage of a household’s income.

As the chart highlights, the primary rent or mortgage payment is by far the largest component, while utilities and maintenance make up smaller but still significant portions of your spending.

Key Insight: The sheer size of this category means that even small savings can have a major impact. Annually reviewing your insurance policies or implementing energy-saving habits can free up a surprising amount of cash over time.

To streamline tracking, consider setting up automatic payments for recurring bills to avoid late fees. For variable costs like utilities, analyze past bills to identify seasonal trends and budget accordingly. Mastering these details is a key step when you learn how to organize your finances. Finally, a dedicated emergency fund specifically for home repairs can prevent unexpected expenses from derailing your entire budget.

2. Transportation and Vehicle Expenses

After housing, transportation often represents the second-largest portion of a household’s budget, making it one of the most vital expense tracking categories. This category encompasses all costs associated with getting from place to place, whether by personal vehicle, public transit, or ridesharing services. For many, a car is a necessity, but its associated costs extend far beyond the monthly payment.

Like housing, this category is a mix of predictable fixed expenses and highly variable costs. A car payment and insurance premium are typically consistent each month, while fuel and maintenance costs can change significantly based on your travel habits, gas prices, and the age of your vehicle. Diligent tracking is essential for avoiding financial surprises and managing your cash flow effectively.

What to Include in This Category

To gain a clear picture of your total transportation spending, you must capture every related expense. Be sure to include:

- Vehicle Payments: Monthly car loan or lease payments.

- Recurring Costs: Car insurance, vehicle registration, and annual license fees.

- Fuel: Gasoline or electric vehicle charging costs.

- Maintenance & Repairs: Oil changes, tire rotations, brake replacements, and unexpected fixes.

- Transit & Other: Public transportation passes (bus, train), rideshare fees (Uber, Lyft), tolls, and parking costs.

The bar chart below illustrates the typical breakdown of transportation costs, showing how fuel and maintenance can add up to nearly as much as the primary vehicle payment itself.

As this breakdown shows, focusing only on your car payment gives you an incomplete picture of the true cost of ownership.

Key Insight: The most significant financial drain in this category often comes from unexpected repairs. Proactive, regular maintenance is the best defense against large, budget-breaking mechanical failures.

To keep these costs under control, shop for car insurance annually to ensure you’re getting the best rate. For vehicle maintenance, sticking to the manufacturer’s recommended service schedule can prevent bigger issues down the line. Beyond the regular costs, managing unexpected vehicle maintenance is crucial. You might find value in exploring smart tips for saving on car repairs to further reduce expenses. Finally, if you drive for work, meticulously track your mileage, as it can lead to valuable tax deductions.

3. Food and Dining

Of all the expense tracking categories, Food and Dining is often the most variable and offers the greatest opportunity for immediate savings. This category encompasses all spending related to nourishment, from essential groceries to discretionary meals out. It’s a critical area to monitor because it’s where small, daily choices can accumulate into significant monthly expenses.

Unlike fixed costs such as rent, food spending can fluctuate dramatically based on lifestyle, planning, and habits. A household might spend a predictable amount on groceries each week while seeing its dining-out budget swing wildly. Separating these two subcategories is a common and highly effective budgeting strategy championed by financial experts like Dave Ramsey and platforms like YNAB. This separation clarifies the difference between needs (groceries) and wants (restaurants, takeout).

What to Include in This Category

To gain full control over your food budget, you need to track every related expense with precision. This includes:

- Groceries: All purchases from supermarkets, farmers’ markets, and specialty food stores.

- Dining Out: Meals at restaurants, cafes, and pubs.

- Takeout and Delivery: Costs for services like Uber Eats, DoorDash, and direct-from-restaurant orders.

- Coffee and Snacks: Daily coffee runs, vending machine purchases, and other convenience buys.

- Work Lunches: Any meals purchased during the workday.

- Special Occasions: Expenses for celebratory dinners or event catering.

The bar chart below shows a sample breakdown of food spending for a typical household, illustrating the significant portion that discretionary dining can occupy.

As shown, while groceries form the foundation, the combined cost of dining out and daily conveniences can easily rival or exceed it, making it a key area for potential budget cuts.

Key Insight: This is one of the few categories where you have daily control. The simple act of meal planning for the week can drastically reduce impulse buys, minimize food waste, and cut your grocery bill by 15-20%.

For effective management, set separate weekly or monthly limits for groceries and dining out. Use a dedicated app to snap photos of receipts immediately, ensuring no purchase is missed. For more ideas on managing these costs, explore some of the best easy expense tracker apps that can automate categorization for you. By actively managing this category, you can find substantial savings without making drastic sacrifices.

4. Healthcare and Medical

Among the most unpredictable yet essential expense tracking categories is Healthcare and Medical. This category encompasses all costs related to maintaining your physical and mental well-being. Unlike more predictable expenses, healthcare spending can fluctuate dramatically based on your age, health status, and the specifics of your insurance coverage, making it a critical area to monitor closely.

This category is a mix of predictable, fixed costs and highly variable, unexpected expenses. Fixed costs include your monthly health insurance premiums, which are consistent. However, variable costs like co-pays for doctor visits, prescription refills, or emergency procedures can arise without warning. Diligent tracking is vital for managing these potentially significant costs and ensuring you are prepared for any health-related financial event.

What to Include in This Category

To gain a clear picture of your total health spending, it’s crucial to track every related expense. Make sure your budget includes:

- Insurance Premiums: Monthly payments for health, dental, and vision insurance.

- Out-of-Pocket Costs: Deductibles, co-pays for doctor and specialist visits, and coinsurance.

- Medications: Prescription drugs, over-the-counter medicines, and vitamins or supplements.

- Professional Services: Costs for dental cleanings, eye exams, physical therapy, and mental health counseling.

- Medical Supplies: Expenses for items like contact lenses, glasses, or medical devices.

The infographic below shows how an average individual’s out-of-pocket medical expenses might be distributed, separate from their fixed insurance premiums.

As illustrated, prescription drugs and professional services often represent the largest portion of variable healthcare spending, highlighting the need for careful financial planning.

Key Insight: Utilizing tax-advantaged accounts like a Health Savings Account (HSA) or Flexible Spending Account (FSA) can significantly reduce your taxable income. By contributing pre-tax dollars to these accounts, you effectively lower the real cost of your medical expenses.

To effectively manage this category, always keep detailed records of medical bills and payments, which can be invaluable for insurance claims or potential tax deductions. For non-emergency procedures, take the time to compare costs between different providers. Most importantly, maintaining a dedicated emergency fund specifically for medical needs can prevent an unexpected health issue from becoming a major financial crisis.

5. Entertainment and Recreation

While not essential for survival, the expense tracking categories for entertainment and recreation are vital for a well-rounded and fulfilling life. This category encompasses all discretionary spending on activities that bring you joy, relaxation, and personal enrichment. It’s often seen as the “fun” part of the budget, but without careful tracking, it can easily spiral out of control.

This category is entirely composed of variable and discretionary costs, making it the most flexible part of your budget. These are often the first expenses to be trimmed when money is tight, but they are also crucial for preventing burnout and maintaining mental well-being. Acknowledging and planning for these costs is a sign of a mature and realistic financial plan.

What to Include in This Category

To get a clear picture of your leisure spending, it’s important to group all related costs. Be sure to track:

- Subscriptions: Streaming services (Netflix, Spotify), gaming memberships, and other recurring digital entertainment.

- Events & Outings: Movie tickets, concerts, sporting events, and social gatherings like dinner with friends.

- Hobbies & Activities: Costs for hobbies like craft supplies or photography equipment, as well as gym memberships and fitness classes.

- Personal Enrichment: Purchases like books, magazines, and online courses.

- Travel: While some create a separate category for major vacations, smaller trips or weekend getaways often fit well here.

Tracking these items reveals how much you spend on personal fulfillment and helps you align your spending with what truly brings you happiness.

Key Insight: This category is a powerful tool for values-based budgeting. By reviewing your entertainment spending, you can see if your money is going toward activities you genuinely enjoy or just mindless consumption, allowing you to reallocate funds for a more satisfying life.

To manage this category effectively, start by auditing all your subscriptions quarterly and canceling any you no longer use. Set a specific monthly “fun money” budget and track it closely to avoid overspending. Also, explore free community events, library resources, and outdoor activities to enjoy recreation without the high cost. Sharing subscription costs with family or friends where permissible is another easy way to save.

6. Debt Payments and Interest

For individuals managing borrowed funds, payments toward debt are one of the most critical expense tracking categories to monitor. This category encompasses all money directed toward paying down balances on credit cards, student loans, personal loans, and other forms of financing. It specifically tracks both the principal reduction and the interest charges, which represent the cost of borrowing.

Actively managing and tracking these payments is vital for improving your financial health. High-interest debt, in particular, can quickly erode your income and hinder your ability to save and invest. By isolating debt payments into their own category, you gain a clear picture of how much of your money is going to lenders versus other financial goals. This clarity is the first step toward creating an effective debt-reduction strategy.

What to Include in This Category

To gain full control over your debt, it’s essential to track every component of your repayment efforts. Make sure to include:

- Credit Card Payments: Both the minimum required payments and any extra amounts you send to pay down the balance faster.

- Student Loan Payments: Monthly payments for federal and private student loans.

- Personal Loan Payments: Regular installments for things like debt consolidation or large purchases.

- Auto Loan Payments: Your monthly car note.

- Other Financing: Payments for any other borrowed money, such as medical debt or “buy now, pay later” plans.

Key Insight: Understanding how your payments are divided is crucial. For a deeper dive into this category, consider understanding principal and interest in a home loan to better plan your repayments, as the same principles apply to other forms of debt.

To accelerate your progress, list all your debts with their balances and interest rates to decide on a payoff strategy. Popular methods include the debt avalanche (tackling the highest-interest debt first) or the debt snowball (paying off the smallest balance first for a motivational win). Automating at least the minimum payments helps avoid costly late fees, while a dedicated tracking system keeps you motivated on your journey to becoming debt-free.

7. Savings and Investments

While most expense tracking categories focus on money going out, this one is about paying your future self. Savings and Investments is a unique but crucial category that treats long-term financial health as a non-negotiable monthly “expense.” It’s the proactive allocation of funds toward building wealth, achieving goals, and creating a safety net.

This category is fundamentally about prioritizing your future. Unlike discretionary spending, these are planned outflows from your income that are set aside before other wants are considered. The core principle is to “pay yourself first,” ensuring that goals like retirement, a down payment, or financial freedom are consistently funded rather than left to whatever is remaining at the end of the month.

What to Include in This Category

To get a clear picture of your wealth-building progress, it’s essential to track every dollar you intentionally set aside. Be sure to include:

- Retirement Contributions: Pre-tax or post-tax contributions to accounts like a 401(k), Roth IRA, or Traditional IRA.

- Emergency Fund: Money transferred to a high-yield savings account to cover 3-6 months of living expenses.

- Taxable Investments: Contributions to brokerage accounts for buying stocks, bonds, ETFs, or index funds.

- Goal-Specific Savings: Funds set aside for specific targets, such as a vacation fund, a new car fund, or a down payment on a home.

- Education Savings: Contributions to plans like a 529 for future education costs for yourself or a dependent.

The contributions you make are the building blocks of your financial future, turning your current income into a source of long-term security and opportunity.

Key Insight: The most powerful lever in this category is automation. Setting up automatic transfers from your checking account to your savings and investment accounts on payday removes the temptation to spend and ensures you consistently hit your goals without relying on willpower.

To maximize your efforts, first focus on capturing any available employer match on your 401(k), as it’s essentially free money. Next, build a robust emergency fund before aggressively pursuing riskier investments. As your income grows, commit to increasing your savings rate by 1-2% each year. This discipline is a core component as you work toward achieving financial independence. Finally, regularly review your allocations to ensure they align with your evolving financial goals and timelines.

Expense Category Comparison Chart

| Category | Implementation Complexity | Resource Requirements | Expected Outcomes | Ideal Use Cases | Key Advantages |

|---|---|---|---|---|---|

| Housing and Utilities | Medium - mix of fixed and variable bills | High - significant portion of income | Stable shelter, essential home services | Essential monthly expense tracking | Predictable bills, tax deductions, savings potential |

| Transportation and Vehicle Expenses | Medium - mix of fixed and variable costs | Medium - varies by lifestyle | Reliable mobility, cost control opportunities | Commuting, travel, and business use | Tax deductions, cost control via habits and alternatives |

| Food and Dining | Medium - highly variable, depends on choices | Medium - can be optimized | Balanced nutrition, budget flexibility | Daily living and discretionary dining | Budget optimization, health benefits, easy tracking |

| Healthcare and Medical | Medium to High - mix of predictable and emergencies | Medium to High - insurance dependent | Health maintenance, financial protection | Managing health expenses and insurance | Tax advantages, preventive care, employer benefits |

| Entertainment and Recreation | Low - fully discretionary | Low to Medium - varies with habits | Personal enjoyment, stress relief | Leisure and social activities | Easily reduced expense, budgeted rewards |

| Debt Payments and Interest | Medium - requires strategic planning | Medium - prioritizing high-interest debt | Reduced debt burden, improved credit | Debt reduction and financial health | Interest savings, tax deductions, improved cash flow |

| Savings and Investments | Medium - requires discipline, automation | Medium to High - consistent contributions | Financial security, wealth building | Long-term financial goals | Employer matching, tax advantages, compound growth |

From Categories to Clarity: Your Next Financial Move

Embarking on the journey of detailed expense tracking can feel like assembling a complex puzzle. You begin with dozens, even hundreds, of individual transactions scattered across various accounts. This article has provided the framework-the seven core expense tracking categories of Housing, Transportation, Food, Healthcare, Entertainment, Debt, and Savings-to help you assemble those pieces into a clear, coherent picture of your financial life.

Moving beyond a simple list of transactions and into a categorized system is the pivotal step from reactive spending to proactive financial management. It’s the difference between wondering where your money went and knowing precisely where it’s going, allowing you to direct it with intention. This structured approach demystifies your cash flow, revealing the true cost of your lifestyle and highlighting opportunities for optimization you might otherwise miss.

Synthesizing Your Spending Story

The power of these categories goes beyond the organization itself, but in the story they tell. By consistently applying this framework, you transform raw data into a narrative about your habits, priorities, and values.

- Revealing Priorities: Does your Entertainment category consistently rival your Savings and Investments? This isn’t inherently good or bad, but it makes your financial priorities explicit, allowing you to assess if your spending truly aligns with your long-term goals.

- Identifying “Silent Drains”: Small, frequent purchases in categories like Food and Dining or Entertainment can accumulate into significant sums. Categorization shines a bright light on these “silent drains,” turning them from invisible leaks into actionable data points.

- Empowering Decisions: When you know exactly how much you spend on Transportation, you can make an informed decision about buying a new car versus using public transit. When your Healthcare costs are clearly defined, you can better plan for future medical needs or choose a more suitable insurance plan.

This clarity is the foundation of financial confidence. It removes the anxiety of the unknown and replaces it with the empowerment of knowledge.

Your Actionable Path to Financial Control

Understanding the theory is complete; now, the real transformation begins with application. Don’t let this newfound knowledge remain passive. Take concrete steps today to translate these concepts into tangible results.

Your immediate next move should be a 30-Day Tracking Challenge. For the next month, commit to categorizing every single expense using the seven core buckets we’ve outlined. Whether you use a simple spreadsheet or a dedicated app, the goal is consistency. This short-term experiment will provide an invaluable, real-world baseline of your financial habits.

At the end of the 30 days, review your findings. You will likely discover surprising patterns and gain immediate insights into your spending. This initial review is your first major victory, providing the momentum needed to build a sustainable budgeting and tracking habit. By mastering these foundational expense tracking categories, you are not just managing money; you are architecting a more secure and intentional financial future, one categorized transaction at a time.

Ready to automate this process and gain deeper insights? PopaDex is designed to make mastering your expense tracking categories effortless by securely aggregating all your financial accounts in one place and automatically categorizing your transactions. Start your journey to financial clarity and build a smarter budget today by visiting PopaDex.