Our Marketing Team at PopaDex

Master Your Finances With a Credit Card APR Calculator

A simple credit card purchase feels harmless at first, but a high Annual Percentage Rate (APR) can quickly turn it into a heavy financial burden. A credit card APR calculator is the tool that shines a light on this hidden cost, showing you exactly how much interest you’ll be paying over time. It’s your first step toward real financial clarity.

The Hidden Cost of Your Credit Card Balance

That small charge on your credit card—a new gadget, a nice dinner out—rarely feels like a major financial decision. But when that balance carries over to the next month, its true cost begins to emerge, all thanks to the powerful force of your card’s APR. This is where a manageable debt can spiral, silently eating away at your wealth and pushing your major life goals further into the distance.

Think of APR as the price you pay for borrowing money. The higher that price, the slower you pay down the actual amount you borrowed. A lot of people don’t realize just how fast this adds up, especially with store-specific retail cards, which often carry much higher rates than your typical Visa or Mastercard.

How Interest Piles Up Over Time

The impact of APR becomes crystal clear when you look at the numbers. Let’s say you’re carrying a $1,000 balance on a card with the average general-purpose APR of 21.98%. Over a single year, that balance would rack up about $219.80 in interest alone—and that’s before you even think about minimum payments, which barely chip away at the original debt.

For retail store cards, the situation is even more grim. The average APR skyrockets to a staggering 30.14%, as highlighted in a 2025 Bankrate.com study.

This cycle of paying interest on an ever-present balance is how people stay in debt for years, often paying more in finance charges than the original purchase was even worth.

Understanding this dynamic is urgent. A credit card APR calculator takes those abstract percentages and translates them into tangible dollars and cents. It exposes the true, eye-watering cost of just making minimum payments and completely changes your perspective. Suddenly, it’s not just a tool; it’s an essential weapon in your financial arsenal, empowering you to see the future cost of your debt today and build a plan to wipe it out for good.

What APR Really Means and How It Works

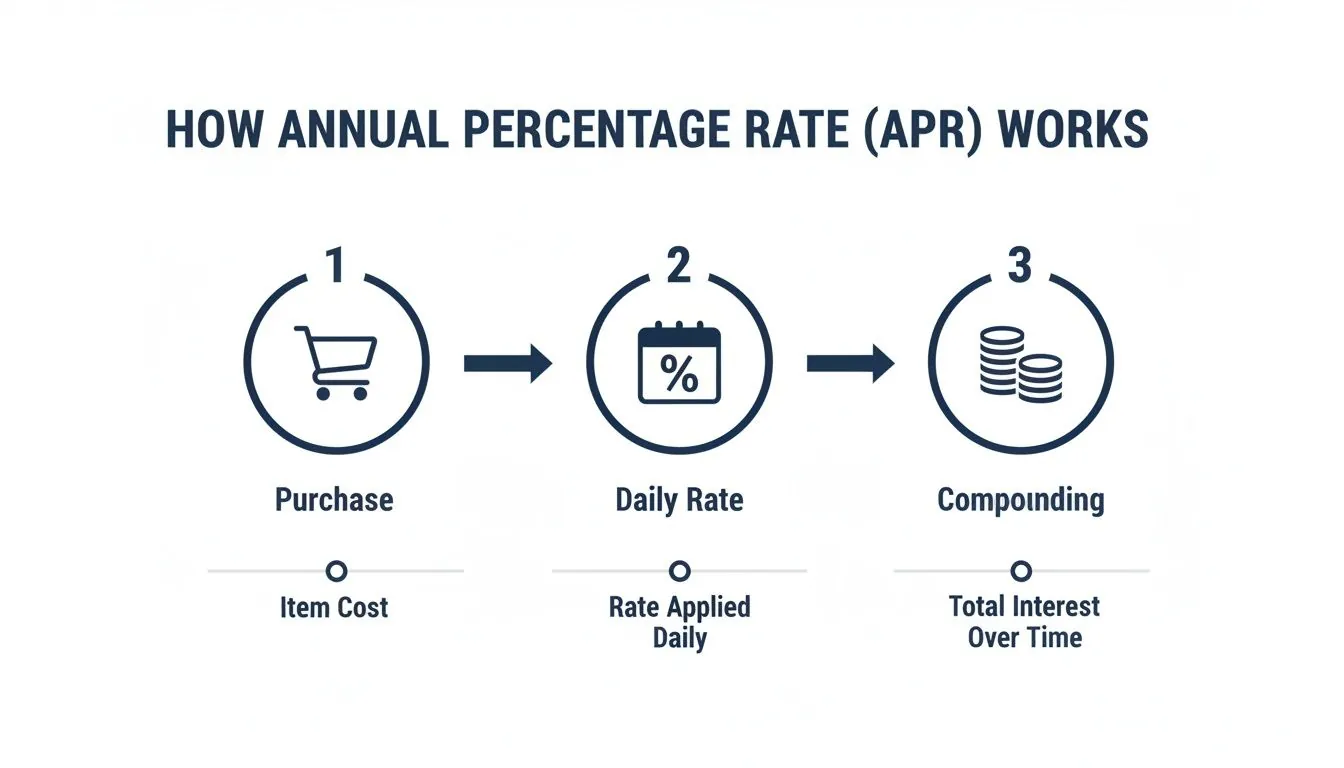

Think of your credit card’s Annual Percentage Rate (APR) as the price tag for borrowing money. While the word “annual” is right there in the name, this cost isn’t a once-a-year thing. It’s the engine that powers the interest charges on your account, and your credit card company calculates it daily.

So, how does that work? Your card issuer takes your yearly APR and chops it up into a daily periodic rate. They just divide your APR by 365 (some use 360, it’s in the fine print). This tiny little percentage gets applied to your outstanding balance every single day you carry one.

But the real kicker is compounding. Each day, the interest calculated is tacked onto your balance. The next day, you’re charged interest not just on what you originally spent, but on yesterday’s interest, too. It’s a financial snowball effect—the longer it rolls, the bigger and faster it gets.

The Different Flavors of APR

Not all APRs are the same. In fact, if you look closely at your credit card statement, you’ll see a few different types listed. Knowing which one applies at any given moment is critical if you want to use a credit card APR calculator and get a number that’s even close to accurate.

Before we get into the nitty-gritty, it helps to see them side-by-side. Each one serves a different purpose and kicks in under different circumstances.

Understanding Different Types of Credit Card APR

| APR Type | What It Is | When It Applies | Typical Rate |

|---|---|---|---|

| Purchase APR | The standard interest rate for things you buy. | Applies to new purchases if you carry a balance past the due date. | 18% - 28% |

| Cash Advance APR | A much higher rate for withdrawing cash. | Kicks in the moment you take cash from an ATM using your card. | 25% - 29.99% |

| Penalty APR | The highest rate your issuer can charge you. | Triggered by late or missed payments. One slip-up can activate it. | 29.99% or higher |

| Introductory 0% APR | A temporary promotional rate. | For a limited time on new purchases or balance transfers. | 0% |

As you can see, the interest rate you pay can vary wildly depending on how you use your card. A single late payment could cause your rate to spike to a punishing 29.99%, which is why staying on top of your due dates is so important.

Understanding these different rates is the foundation of managing your credit. Each one represents a different cost of borrowing, and being aware of them prevents unexpected spikes in your balance. By knowing which APR applies, you can make smarter decisions about how you use your card and avoid costly financial traps.

How a Credit Card APR Calculator Works

A credit card APR calculator seems complicated, but under the hood, it’s running on surprisingly simple math. The whole point is to demystify how interest actually piles up on your balance. It does this by taking that big annual percentage and breaking it down into a tiny daily number that gets applied over and over. Once you see how it works, you’ll trust the results and really feel the cost of carrying debt.

At its core, the calculator just needs three things from you: your current balance, your annual APR, and how much you plan to pay each month. With just those numbers, it can map out the entire life of your debt, giving you a clear finish line.

Let’s pull back the curtain and do the math for the first month ourselves to see exactly what’s happening.

The Math Behind the First Month

Let’s say you’re carrying a $5,000 balance on a card with a 22% APR. The calculator’s first move is to figure out the daily periodic rate.

- Convert APR to a decimal: 22% is just 0.22.

- Get the daily rate: Divide that decimal by 365. So, 0.22 / 365 = 0.0006027. This tiny, seemingly harmless number is the percentage of interest tacked onto your balance every single day.

- Assume an average daily balance: If your balance stays at $5,000 for the whole billing cycle, that’s our number.

- Calculate the monthly interest: Now, multiply that daily rate by the number of days in the cycle (we’ll use 30) and then by your balance. The formula looks like this: (0.0006027 × 30 days) × $5,000 = $90.41.

That $90.41 is what you owe in interest for just one month. An online calculator spits this out instantly, saving you the tedious math.

This daily interest calculation is the engine that drives the compounding cycle, which is how a balance can slowly grow over time if you’re not careful.

As the diagram shows, a single purchase gets pulled into a cycle where the daily interest is calculated and then folded back into the balance, creating a compounding effect.

The Power of Compounding and the Minimum Payment Trap

So, what happens in month two? Imagine you make a $150 payment. After the $90.41 interest charge is paid, only $59.59 of your money actually goes toward chipping away at the original debt. Your new balance becomes $4,940.41. The next month’s interest is then calculated on that new, slightly lower balance. This is compounding working in reverse—but very, very slowly.

This is also where a calculator reveals a brutal financial truth. With total U.S. credit card debt now at $1.18 trillion and more people falling behind on payments, millions are stuck paying only the minimum.

On a $10,000 balance with the average 24.62% APR, making only minimum payments could drag the debt out for over 35 years and cost you more than $25,000 in interest alone. You can find more on these trends in the latest credit card statistics on SellersCommerce.com.

A credit card APR calculator’s greatest strength is its ability to instantly model these long-term scenarios. It transforms abstract percentages into a concrete timeline and a total cost, showing you exactly how much money and time you can save by paying more than the minimum.

Using an APR Calculator for Your Payoff Plan

Okay, you get the math behind APR. Now, let’s put that knowledge to work and build a real debt payoff strategy. This is where an online credit card APR calculator becomes your best friend. It’s the tool that turns all those confusing numbers into a clear, actionable plan. Think of it as your financial co-pilot, ready to map out different routes to get you out of debt.

To get going, you just need three things: your current credit card balance, your APR, and a monthly payment you think you can make. The calculator instantly shows you what your credit card statement never will: the Total Interest Paid and your final Payoff Date. These are the two numbers that really matter for your wallet and your timeline.

Modeling Your Path to Zero Debt

The real magic of a credit card APR calculator is its power to play “what if.” By tweaking just one number—your monthly payment—you can see completely different financial futures unfold. It’s how you find a plan that actually fits your life and your budget.

Of course, to use the calculator effectively, you first need a solid grip on your own money. Getting a handle on understanding your overall cash flow is a great first step, as it helps you see exactly where you can free up extra cash to throw at your debt.

Let’s walk through three powerful scenarios you can model right now:

- The Minimum Payment Trap: First, plug in your balance, your APR, and just the minimum payment. The result is usually pretty shocking—we’re talking a payoff timeline that could stretch for decades and an insane amount of interest paid. It’s a powerful visual of why the minimum is a trap.

- The Snowball Effect: Now for the fun part. Keep everything the same, but add an extra $50 or $100 to your monthly payment. Watch what happens. You’ll likely see years vanish from your payoff date and thousands of dollars in interest savings. It’s proof that even small, steady efforts make a huge difference.

- The Debt-Free Date: Got a goal in mind? Maybe you want to be debt-free in three years. Most calculators let you work backward. You set the target date, and it tells you the exact monthly payment needed to make it happen. This turns a vague wish into a concrete number you can aim for.

Here’s a look at what a typical online credit card APR calculator looks like. Simple, right?

The clean input fields let you quickly test different payment strategies and see the financial impact immediately.

When you start playing with these scenarios, the calculator stops being a simple math tool and becomes a motivational powerhouse. Seeing the real savings in both time and money gives you the fuel you need to stick with the plan. For those who love to track things in detail, you can pair this with a good debt payoff calculator spreadsheet to keep yourself organized and on target.

Actionable Strategies to Lower Your APR

Seeing the damage a high APR can do on a calculator is one thing; doing something about it is another. But a high interest rate isn’t a life sentence. With a few smart moves, you can slash your rate, cut down your interest payments, and get on the fast track to being debt-free.

Believe it or not, one of the easiest and most effective tactics is to simply ask for a lower rate. So many people have no idea this is even on the table. If you have a solid history of paying on time, your credit card company has every reason to keep you as a happy customer.

Negotiate Directly with Your Issuer

A single phone call could literally save you hundreds of dollars. Before you dial, get your facts straight: know your current APR, have your payment history handy, and check what rates competitors are offering to customers like you.

When you get someone on the line, you don’t need a complicated script. Try something like this:

“Hello, I’ve been a loyal customer for [Number] years and have always paid my bill on time. I’m working on lowering my expenses and noticed my current APR is pretty high. I’ve seen other cards offering much lower rates, and I’d really like to know if you can offer me a more competitive APR to keep my business.”

Be polite but firm. If the first person you talk to can’t help, ask if there’s a retention department you can speak with. This costs you nothing but a few minutes, and the potential savings are huge.

Explore Balance Transfer Offers

Another fantastic tool in your arsenal is the balance transfer. This is where you move a high-interest balance to a brand-new card that offers a 0% introductory APR for a limited time—usually 12 to 21 months. This creates a golden opportunity, a window of time where you can attack your principal balance without interest piling up against you.

Of course, you have to read the fine print:

- Transfer Fees: Most cards will charge you a fee to move the balance, typically 3% to 5% of the amount you transfer.

- Post-Introductory APR: That 0% rate won’t last forever. Find out what the APR will jump to once the promotional period is over.

- Credit Requirements: The best balance transfer offers are usually reserved for people with good to excellent credit scores.

Ultimately, improving your credit score is the long-term play that opens doors to better rates on everything. Making consistent, on-time payments and keeping your credit card balances low are the cornerstones of a healthy score. You can dive deeper into creating a solid payoff strategy with our guide on how to pay off debt.

With credit card rates hitting historic highs—the average purchase APR for bank cards is now a staggering 21.98%, while credit unions are significantly lower at 15.90%—every point you can add to your credit score helps you get a better deal. For more on these trends, check out the Philly Fed’s latest report.

Tying It All Back to Your Net Worth

Figuring out your credit card interest with an APR calculator is like a doctor diagnosing a problem. It’s the critical first step. But the real goal is to see how treating that problem—paying down your debt—improves your overall financial health.

Think of high-interest credit card balances as an anchor weighing down your net worth. Every single dollar you pay in interest is a dollar that vanishes instead of building your wealth. It’s a direct drain on your financial progress.

This is where you graduate from a simple calculator to a full-blown financial command center. With a platform like PopaDex, you get a clear dashboard showing your assets and liabilities right next to each other. As you knock down those card balances, you can literally watch your net worth number tick up in real time. Talk about a powerful motivator.

See Your Entire Financial Story

These days, our finances often aren’t limited to just one country. Modern life can mean international assets and debts, so your tracking tools need to keep up with features like multi-currency support. This lets you manage a credit card from another country just as easily as your local one, giving you a truly unified view of where you stand.

Automated tracking brings all your accounts into one place, so you always have an up-to-the-minute picture without the headache of manual spreadsheets. You can see exactly how chipping away at that high-APR card directly lifts your overall wealth.

Your net worth is the most honest report card on your financial health. When you look at debt repayment through this lens, it stops being a stressful chore and becomes a strategic play to build long-term wealth.

Seeing the bigger picture helps you make smarter moves everywhere else. While tackling credit card debt is a fantastic way to boost your personal net worth, savvy investors also use tools like a Rental Property ROI Calculator to weigh other wealth-building opportunities.

Want to get that instant snapshot of where you stand today? You can use PopaDex’s free net worth calculator to find out.

Common Questions About Credit Card APR

Even after crunching the numbers with a credit card APR calculator, you might still have a few nagging questions. It’s totally normal. Let’s tackle the most common points of confusion so you can feel fully in control.

Interest Rate vs. APR: What’s the Real Difference?

One of the biggest mix-ups is between the interest rate and the APR. Think of the interest rate as the base price for borrowing money—the sticker price, if you will.

The APR, or Annual Percentage Rate, is the all-in cost. It rolls up the interest rate plus any mandatory fees (like an annual fee) into a single, standardized number. This makes the APR a much truer measure of what you’re actually paying over a year.

Fixed vs. Variable APR

Next up is the difference between fixed and variable APRs, and this one is crucial. A fixed APR is exactly what it sounds like: it’s set and doesn’t wiggle around with the market. This gives you predictable payments, which is great for budgeting. Just know that “fixed” isn’t forever; card issuers can still change it, but they have to give you a heads-up first.

A variable APR, on the other hand, is tied to a benchmark financial index, like the U.S. Prime Rate. When that index moves, your APR moves with it. Since most credit cards today have variable rates, your interest costs can—and likely will—change over time.

So, which one is better? It really comes down to your comfort with risk. A fixed rate offers stability. A variable rate might be cheaper if interest rates fall, but it could cost you more if they start climbing.

Why Your Credit Score Is King

Finally, let’s talk about the single most important factor that dictates the APR you’ll get: your credit score. Lenders see a high credit score as a sign of a reliable, low-risk borrower. The reward? You get offered their best, lowest interest rates.

If your score is on the lower side, lenders see more risk, so they’ll offer you a higher APR to compensate. This makes paying off your balance quickly even more critical. Understanding this direct link between your score and your rate is the key to unlocking better terms and keeping more of your money in your pocket.

Ready to see your full financial picture? Track your debts and watch your net worth grow with PopaDex. Take control of your finances today at https://popadex.com.