Our Marketing Team at PopaDex

Your Net Worth Calculator Guide: Track Wealth Like a Pro

Why Your Net Worth Actually Matters More Than Your Salary

Your salary is that satisfying chunk of change that lands in your bank account every month. It’s tangible, it’s exciting, and let’s be honest, it’s fun to talk about. But here’s the thing: your salary isn’t the whole story. Your net worth is the real MVP of your financial health. It’s the big picture, the difference between what you own (your assets) and what you owe (your liabilities).

Think of it like this: your salary is the water flowing from the faucet into your bathtub, while your net worth is the actual water level. You could have a powerful faucet (amazing salary!), but a leaky drain (big spender!) and never actually fill the tub. That’s why understanding your net worth is so crucial.

This one number—your net worth—can be a real eye-opener. I’ve seen it firsthand with friends and colleagues. People with impressive salaries suddenly realize their net worth isn’t what they expected. It’s human nature to avoid facing our financial reality, especially if we suspect it’s not ideal. It’s like avoiding the scale when you think you’ve gained a few pounds. For veterans looking to secure their financial future, resources like this guide on Financial Planning for Veterans can be incredibly helpful.

The Gap Between High Earners and Low Net Worth

One of the toughest pills to swallow in personal finance is this: high earners can have surprisingly low net worths. How? Lifestyle inflation is often the culprit. A bigger paycheck can easily lead to a bigger house, a nicer car, more lavish vacations—all of which increase your liabilities without necessarily boosting your assets. A net worth calculator can expose this gap, making you confront your spending habits and make necessary changes.

Grasping this dynamic completely changes how you think about money. It shifts the focus from constantly chasing a higher salary to building sustainable wealth.

Comparing Apples to Oranges: Net Worth and Others

Comparing your net worth to others is tricky. It can be motivating to see how you stack up against your peers, but it can also be incredibly misleading. A net worth comparison is only useful in a specific context. For example, in 2023, the average US household net worth was about $1,059,470, while the median was $192,084. Discover more insights. This huge difference shows how wealth is concentrated among a small percentage of the population. Comparing yourself to the average without understanding this distribution can lead to unnecessary discouragement.

Using Net Worth to Your Advantage

The best comparison is to your past self. Are you moving closer to your own financial goals? That’s the real measure of success. Tracking your net worth over time, using a tool like PopaDex, gives you a clear view of your financial trajectory. You can celebrate your wins and tweak your strategy as needed.

The Reality Check: Calculating Your Numbers Honestly

Let’s be real - figuring out your net worth isn’t about creating some crazy spreadsheet. It’s about getting a clear picture of your financial health. Forget the robotic number-crunching; we’ll break this down into manageable steps, just like I did when I first started tracking my own net worth.

Gathering Your Financial Data: No Need for a PhD in Accounting

First, gather your financial statements. Bank statements, investment portfolios, retirement accounts – anything that shows what you own. Don’t stress about being perfect; just grab what’s easily accessible. I remember feeling overwhelmed when I started, but it quickly became much easier. For a deeper dive into what net worth is and how it’s calculated, check out this helpful guide: Net worth: What It Means and How To Calculate It.

Next, let’s look at what you owe. Credit card balances, student loans, your mortgage – list it all out. This part can be a bit tough, but honesty is essential. I’ve known people who initially skipped this step or downplayed their debts. Trust me, facing the full picture, even if it’s uncomfortable, is the only way to get an accurate net worth.

The Tricky Stuff: Valuations and Zillow Dreams

Now for the tricky part: valuations. Take your house, for example. Zillow estimates can be fun to look at, but they’re not always the most accurate. A recent appraisal or an assessment from a local realtor is much more reliable. And your car? Depreciation hits hard the moment you drive it off the lot. Use a reputable used car pricing guide like Kelley Blue Book for a better estimate.

Don’t get stuck trying to be absolutely perfect. A “good enough” estimate is better than getting paralyzed. This is particularly true for investments, which change constantly. Just use the most recent statement values; don’t obsess over daily market swings.

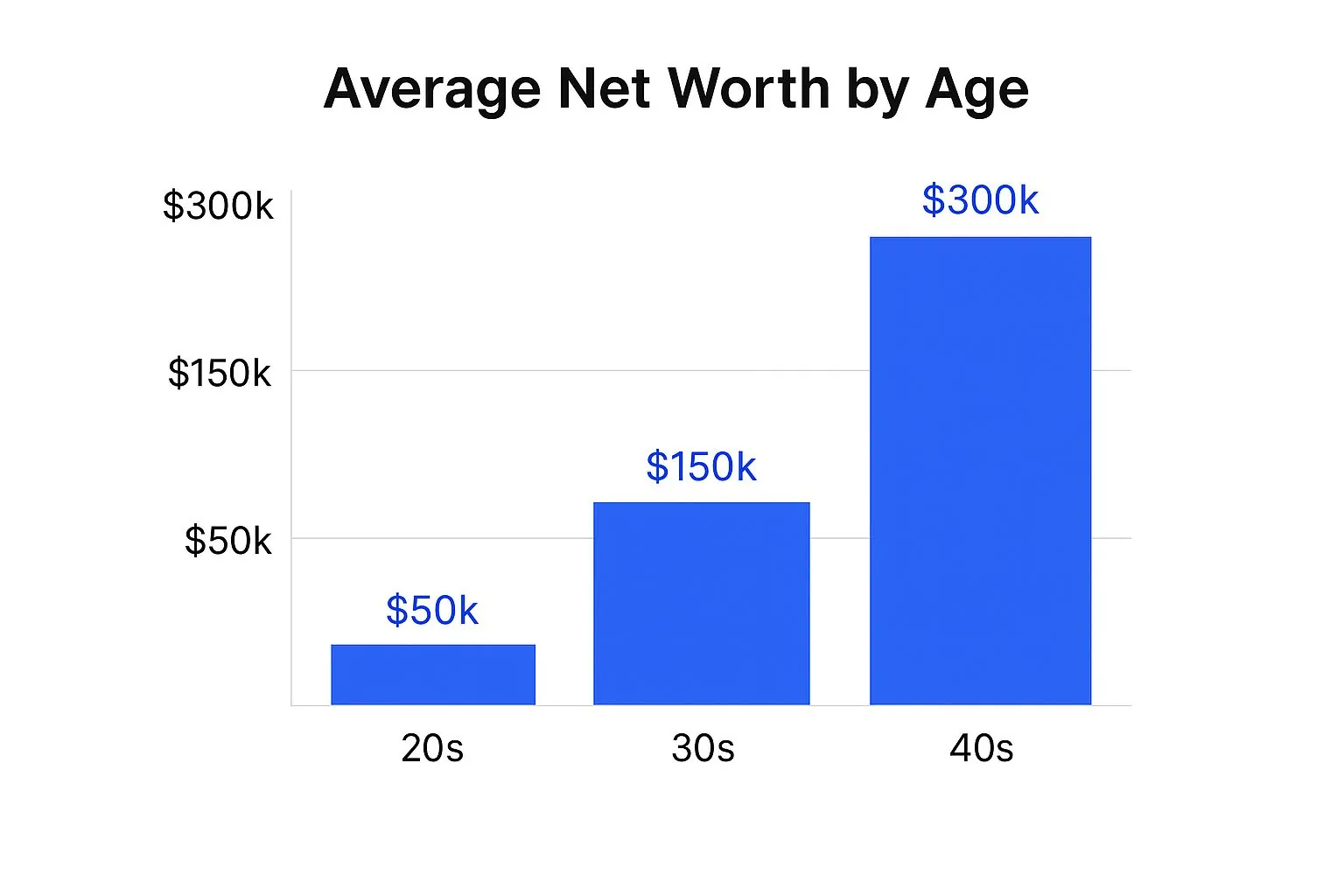

This infographic shows the average net worth across different age groups. Notice how it tends to increase with age, reflecting years of asset accumulation and potentially lower debt. This underscores the importance of long-term financial planning and consistent wealth-building strategies.

To help you categorize everything correctly, let’s look at a breakdown of common assets and liabilities:

This table outlines what to include when calculating your net worth. It’s a handy reference to ensure you’re capturing everything accurately.

| Item | Include as Asset | Include as Liability | Notes |

|---|---|---|---|

| Checking Account | Yes | No | This includes any readily available cash. |

| Savings Account | Yes | No | Include all savings accounts, including money market accounts. |

| Retirement Accounts | Yes | No | 401(k)s, IRAs, etc., should be included at their current value. |

| Investments (Stocks/Bonds) | Yes | No | Use the current market value for your investments. |

| Real Estate | Yes | No | Include the estimated market value of any property you own. |

| Vehicles | Yes | No | Use a reputable source like Kelley Blue Book for accurate valuations. |

| Personal Property | Yes | No | Jewelry, collectibles, etc. – while often overlooked, these can contribute to your net worth. |

| Mortgage | No | Yes | Include the outstanding balance on your mortgage. |

| Car Loan | No | Yes | Include the outstanding balance on any auto loans. |

| Student Loans | No | Yes | Include the outstanding balance on any student loans. |

| Credit Card Debt | No | Yes | Include the current balance on all credit cards. |

| Personal Loans | No | Yes | Include any outstanding personal loans. |

Remembering to include all assets and liabilities is crucial for an accurate net worth calculation. This table helps clarify what falls into each category.

Don’t Forget the Hidden Gems (and Debts)

People often forget about assets like jewelry, collectibles, or even that vintage guitar. While these might not be huge, they still contribute. Conversely, don’t overlook smaller debts: personal loans from family or outstanding medical bills. Every little bit counts.

Remember, this is your financial snapshot. Be honest with yourself, even if the numbers aren’t ideal. The starting point is the most important part of the journey.

Finding Your Perfect Net Worth Calculator Match

So, you’re thinking about diving into the world of net worth calculators. Excellent! But finding the right one can feel a bit like Goldilocks trying out porridge – some are too bare-bones, others too complicated. Trust me, I’ve tried my fair share of clunky calculators that over-promised and under-delivered.

Beyond the Bells and Whistles: What Actually Matters

Some calculators boast a ton of fancy features you’ll probably never use. Honestly, keep it simple. You need a tool that’s accurate and easy to use. Think about whether you prefer manually entering data or connecting directly to your bank accounts.

A simple spreadsheet might do the trick if you’re just starting out. But if you’re juggling a more complex portfolio, a platform like PopaDex, which connects to over 15,000 banks, can be a lifesaver. For a detailed comparison of different net worth applications, check out this helpful guide.

The Security Question: Protecting Your Financial Data

Before you connect any financial tool to your accounts, pause and consider the security implications. Is the connection encrypted? What’s their data privacy policy? A reputable tool will be upfront about its security measures. After all, you’re sharing sensitive information.

Manual Vs. Automated: Finding the Right Balance

Automated tracking sounds fantastic, right? And it can be. But sometimes, manual calculation gives you more control and a deeper understanding of your finances. When I first started tracking my net worth, manual entry forced me to really examine where my money was going. I spotted trends and made adjustments I might have missed otherwise. It also helps you catch potential syncing errors or outdated info.

The Right Tool for the Job

Different financial situations call for different tools. If you’re just beginning your wealth-building journey, a basic spreadsheet or a free tool like Mint might be perfect. As your finances become more complex, consider upgrading to a platform like PopaDex with advanced features like multi-currency support and investment tracking. Start simple and scale up as needed.

Real-World Testing: User Feedback and Experience

Don’t fall for marketing hype. Seek out real user reviews. What are people saying about the ease of use, accuracy, and customer support? I’ve learned the hard way that a shiny interface doesn’t always equal a useful tool. Look for practicality and reliability. These insights can save you a lot of headaches down the road.

What Your Number Really Means (Context Is Everything)

So, you’ve finally calculated your net worth. Great! But now you’re staring at this number, and maybe feeling a bit…underwhelmed? Trust me, I’ve been there. When I first figured out mine, I had that same “Okay, now what?” feeling. Your net worth is a snapshot of your finances at this particular moment, and understanding the context surrounding that snapshot is key.

Benchmarking Your Wealth: The Right Way to Compare

It’s tempting to compare your net worth to others, but honestly, that can be a recipe for disaster. You might end up feeling either totally inadequate or way too proud, neither of which is particularly helpful. The real trick is making sure you’re comparing apples to apples. A $50,000 net worth at 25 is a completely different story than a $50,000 net worth at 45. Think about it: life stage, career progress, where you live – it all makes a huge difference.

Net worth by age is a really important piece of the puzzle. For instance, in 2022, a $100,000 net worth put you around the 38.59th percentile across all age groups. But if you look at specific age brackets, that ranking can shift dramatically. Discover more insights. See? Just looking at the number itself without any context can be seriously misleading.

To give you a better sense of where you could be, I’ve put together a helpful table based on median net worth data. This isn’t about keeping up with the Joneses, but it does give you some general benchmarks to consider.

| Age Range | Median Net Worth | 75th Percentile | Key Milestones |

|---|---|---|---|

| 25-34 | $14,000 | $76,300 | Early career, starting a family, first home |

| 35-44 | $91,300 | $266,400 | Career growth, growing family, larger home |

| 45-54 | $168,600 | $506,400 | Peak earning years, investing for retirement |

| 55-64 | $242,400 | $738,000 | Nearing retirement, downsizing |

| 65-74 | $254,800 | $727,000 | Retirement, estate planning |

Keep in mind these are just median numbers, and your personal situation might look totally different. The real takeaway here is that your net worth journey is a marathon, not a sprint, and everyone runs their own race.

Beyond the Numbers: Life Happens

Here’s the thing: life rarely goes exactly as planned. Marriage, kids, changing careers, a sudden economic downturn – these can all significantly impact your net worth (and your sanity!). Understanding how life events influence your financial trajectory helps you adjust your expectations and strategies. To find the perfect digital tool for your needs, explore the option of using a specialized tool like a Chair Fit Calculator. Sometimes it’s about shifting gears and adapting to new circumstances. Flexibility is key.

Celebrating Wins and Staying Motivated

Don’t let comparing yourself to others steal your joy! Celebrate every milestone, no matter how small it seems. Acknowledge your wins and recognize how far you’ve come. It’s all about finding a balance between pushing yourself to grow and appreciating where you are right now.

Realistic Progress and Course Correction

Looking at wealth patterns and distribution data gives you a realistic benchmark. It helps you understand what “reasonable progress” actually looks like and when you might need to tweak your approach. Don’t be afraid to adjust your strategy based on your unique situation and goals.

The Emotional Side of Wealth: It’s Not Just Math

Calculating your net worth isn’t just a math problem; it’s also about how those numbers make you feel. It’s perfectly normal to feel a mix of emotions, from excited to totally stressed out. Acknowledge those feelings, and don’t let them derail you. Remember, your net worth is a tool, not a judge. Use it to empower yourself and make informed decisions about your financial future.

Tracking Progress That Actually Motivates You

Calculating your net worth once is a bit like stepping on the scale after a week of clean eating. It’s a nice data point, but it doesn’t reveal the bigger picture. Consistently tracking your net worth, however, is where the real magic happens. It’s akin to witnessing your fitness journey unfold over months of dedicated workouts – you see tangible progress, and that fuels your drive. Let’s explore some practical strategies for monitoring your wealth without becoming obsessed with spreadsheets or the stock market ticker.

Finding Your Rhythm: How Often Should You Track?

The ideal tracking frequency is personal. Some folks prefer monthly check-ins, others are comfortable with quarterly or even semi-annual reviews. I started with monthly tracking to get a handle on my financial flows, but I’ve since settled into a quarterly rhythm. It really boils down to your personality and the complexity of your finances. If you’re just beginning, more frequent tracking can help solidify good habits. For a more seasoned investor with an established portfolio, less frequent checks might suffice. Find what keeps you informed without feeling overwhelmed.

Meaningful Changes Vs. Market Noise: Knowing the Difference

Your net worth will ebb and flow – that’s perfectly normal. Markets fluctuate, real estate values shift, and even your car depreciates over time. Don’t get spooked by every dip. The trick is to discern between typical market volatility and significant shifts that warrant your attention. A 10% market correction might feel dramatic, but if you have a long-term investment horizon, it’s likely a temporary blip. A significant change, like paying off a hefty chunk of debt or receiving a large inheritance, is a more meaningful indicator of progress.

This screenshot showcases the clean and user-friendly interface of PopaDex, a net worth tracker. The clear visualization of assets and liabilities provides a quick grasp of your overall financial picture. The platform’s intuitive design simplifies the tracking process, making it accessible for all experience levels.

Setting Realistic Growth Targets: The Motivation Sweet Spot

Unrealistic expectations are motivation killers. I’ve watched friends set themselves up for disappointment by aiming to double their net worth in a year. Ambition is great, but it needs a dose of realism. Look at historical data, consider your income and expenses, and set targets that challenge you without being discouraging. For example, a 5-10% annual increase might be more achievable and sustainable than shooting for 50% growth. Learn more about how PopaDex can support your tracking with their dedicated net worth tracker.

Handling Setbacks: Turning Lemons into Lemonade

Life has a way of throwing curveballs. Market crashes, job losses, unforeseen medical expenses – these things happen. The key is not to let these events derail your entire financial plan. View setbacks as opportunities for learning and growth. A market downturn can be a chance to rebalance your portfolio. A job loss might prompt you to reassess your skills and career trajectory. Resilience is paramount in the long game of wealth building. Use these experiences to refine your strategy and emerge even stronger financially.

Avoiding the Mistakes That Sabotage Your Progress

Let’s be honest, figuring out your net worth can be trickier than it seems. Even with the best intentions, it’s easy to make mistakes. I’ve definitely stumbled a few times myself! So let’s talk about some common pitfalls, from getting a little too optimistic about your assets to conveniently forgetting about those pesky debts.

The Overvaluation Trap: Your Home Isn’t a Lottery Ticket

It’s tempting to overvalue things, especially your home. We’ve all fallen for the allure of Zillow estimates, right? But remember, those are just estimates, not appraisals. I remember once convincing myself my tiny apartment had doubled in value overnight. It hadn’t. A realistic assessment, maybe based on recent sales in your neighborhood or a professional appraisal, is key. Calculating your net worth shouldn’t be a wishful thinking exercise.

The Forgotten Debt: That Lingering Credit Card Balance

On the flip side, it’s surprisingly easy to downplay debts. Especially those smaller, nagging ones. That lingering credit card balance, the loan from a family member – they all add up. The first time I calculated my net worth, I completely spaced on a small student loan. It wasn’t intentional, it just slipped my mind. But even small omissions can skew the big picture. Be honest with yourself. Facing the complete picture, even if it’s a little uncomfortable, is essential for accurate tracking.

The Timing Dilemma: When to Update Your Values

How often should you update your net worth? Daily market fluctuations can be a rollercoaster. I used to obsessively check my investments, riding the emotional highs and lows. Trust me, it’s exhausting. A more practical approach is monthly or quarterly updates. This gives you a good sense of your progress without getting lost in the daily noise. For things like real estate, annual updates are usually fine unless the market goes haywire.

Red Flags: Spotting a Calculation Gone Wrong

If your net worth looks wildly different than you expected, double-check everything. Did you include all your assets and liabilities? Are your valuations realistic? Sometimes a second set of eyes can be helpful. A friend or a financial advisor can offer a fresh perspective and catch errors you might have missed.

Practical Solutions: Navigating Valuation Dilemmas

Valuing certain assets can be a headache. For things like collectibles or jewelry, a professional appraisal is ideal, but can be pricey. Online marketplaces or price guides can give you a decent estimate. For vehicles, use a reliable source like Kelley Blue Book. Remember, the goal is a realistic assessment, not perfect precision. A “good enough” estimate is often better than getting paralyzed by overthinking.

Your Roadmap to Real Financial Clarity

Now that you get how a net worth calculator works, let’s talk about actually using this knowledge to improve your finances. Calculating your net worth isn’t a one-time thing; it’s the first step on a longer journey.

Building Your Personalized Monitoring System

Think of your net worth as your financial dashboard. You wouldn’t drive without glancing at your speedometer or fuel gauge, right? Keeping tabs on your net worth gives you that same crucial insight into your financial health. But it shouldn’t be a drag. Find a system that fits your life. When I started, I just used a simple spreadsheet and updated it monthly. These days, I prefer a platform like PopaDex that syncs with my accounts, giving me a real-time view without all the manual data entry.

From Insights to Action: Making Smarter Financial Decisions

Knowing your net worth is just the beginning. The real magic happens when you use that knowledge to make informed choices. A higher net worth doesn’t just appear out of thin air. It’s built through consistent, strategic moves. For example, if you see your debt starting to climb, tracking your net worth might encourage you to check out strategies like the debt snowball or debt avalanche methods. On the other hand, if you’re consistently crushing your savings goals, you might decide to ramp up your investment contributions to really accelerate your wealth growth.

Realistic Timelines: No Get-Rich-Quick Schemes Here

Building wealth is a marathon, not a sprint. There’s no secret formula or overnight miracle. Your timeline depends on a few key factors: your starting point, your income, your expenses, and your financial goals. A realistic timeline takes all of this into account and focuses on building sustainable habits. Some people might take years to reach a six-figure net worth, while others might hit that milestone much faster. It’s easy to get caught up comparing yourself to others, but remember, your financial journey is unique.

Warning Signs: Knowing When to Pivot

Tracking your net worth also helps you spot potential problems early. If you see your net worth consistently dropping, that’s a clear signal to re-evaluate your strategy. Maybe your spending is outpacing your income, or perhaps your investments aren’t performing as well as you’d hoped. Whatever the reason, catching it early lets you make adjustments before things get out of hand. I remember once noticing my net worth dipping unexpectedly, and realized I’d gotten a little carried away with online shopping. Tracking my net worth was that much-needed wake-up call to get my spending back on track.

Sustainable Habits: Small Changes, Big Impact

Building lasting wealth isn’t about drastic, unsustainable changes. It’s about creating small, consistent habits that build on each other over time. Automating your savings, consistently contributing to your investments, and regularly reviewing your expenses are all examples of habits that, over time, can lead to significant growth. Just like getting in shape, consistency and patience are your best friends when it comes to building wealth.

Celebrate Your Wins: Acknowledge Your Progress

Don’t forget to celebrate your accomplishments! Reaching a savings goal, paying off a loan, or hitting a new net worth milestone – these are all wins worth celebrating. Acknowledging your progress, no matter how small, reinforces positive financial behaviors and keeps you motivated on your journey.