Our Marketing Team at PopaDex

Master Your Debt with an Extra Payment Calculator

An extra payment calculator is a fantastic tool that cuts through the noise and shows you exactly how much time and interest you can save by paying a little extra on your loans. You just plug in your loan details, add an extra payment amount, and it instantly spits out a new payoff date and total interest. It’s a simple way to see how even small, consistent extra payments can completely change the game and get you debt-free faster.

How Extra Payments Put You on the Financial Fast Track

Making extra payments on a loan is one of the smartest, most direct ways to build wealth. Here’s why it works so well.

On a standard loan payment, especially in the early years, a huge chunk of your money goes straight to interest. Only a tiny fraction actually reduces what you owe—the principal. This whole process is called amortization, and it’s set up to make the lender the most money over the long haul.

But when you make an extra payment—and this is key—you tell the lender to apply it directly to the principal. This move completely flips the script. That extra cash bypasses the scheduled interest payment and knocks down your outstanding balance.

A smaller principal balance means less interest can build up next month. In turn, more of your next regular payment goes toward the principal, not interest. It creates a powerful snowball effect that builds on itself month after month.

The Real Power of Principal-Only Payments

The magic is in how you disrupt the lender’s amortization schedule. Every single dollar you put toward the principal is a dollar that the lender can no longer charge you interest on for the rest of the loan’s life. It’s a simple action with an absolutely massive impact over time.

You’ll see some very real benefits:

- Shorter Loan Term: You can easily shave months, or even years, off your repayment schedule.

- Huge Interest Savings: We’re talking about potentially thousands of dollars that stay in your pocket instead of going to the bank.

- Faster Net Worth Growth: Every dollar of debt you erase is a dollar added directly to your net worth.

The core idea is to stop “renting” money for longer than you have to. By attacking the principal, you shorten the loan’s life, slash the total cost of borrowing, and free up your cash flow for things that actually matter to you.

A Quick Look At Extra Payment Impact On A $300,000 Mortgage

To see just how powerful this is, let’s look at a typical $300,000, 30-year mortgage with a 6% interest rate. The standard monthly payment would be about $1,798.65.

| Scenario | Total Interest Paid | Loan Paid Off In | Total Savings |

|---|---|---|---|

| Standard Payments | $347,514 | 30 years | $0 |

| Extra $100/month | $299,655 | 26 years, 2 months | $47,859 |

| Extra $200/month | $261,960 | 23 years, 4 months | $85,554 |

| Extra $500/month | $191,858 | 17 years, 11 months | $155,656 |

Even just an extra $100 a month—the cost of a few weekly coffees—saves nearly $48,000 and gets you mortgage-free almost four years sooner. That’s a serious return on a relatively small change.

From “What If” to “Here’s How”

This is exactly where an extra payment calculator becomes your best friend. Instead of guessing, you can run different scenarios and see the real numbers for yourself.

Wondering what an extra $150 a month on your car loan would do? The calculator will show you. Curious about putting your annual bonus toward your student loans? It can model that, too.

It’s no surprise that demand for these tools is exploding. The financial calculators market, valued at $224 million in 2022, is on track to hit $615.8 million by 2032. That tells you people are waking up and taking control of their finances.

By using these calculators, you can stop wondering and start planning. You can build a real strategy for getting out of debt and see exactly how your hard work pays off, which is a huge step as you learn how to increase your net worth.

Navigating the Extra Payment Calculator Like a Pro

Ready to see the numbers for yourself? An extra payment calculator is the best way to turn a vague financial goal into a concrete, actionable plan. It takes the guesswork out of the equation, letting you model different scenarios to find a strategy that actually fits your budget.

Let’s walk through the key inputs so you can start using this tool with total confidence. Most calculators are refreshingly simple, asking for just a few key details you can pull from your latest loan statement. Don’t have it handy? No problem—a quick login to your lender’s online portal will have everything you need.

Gathering Your Loan Details

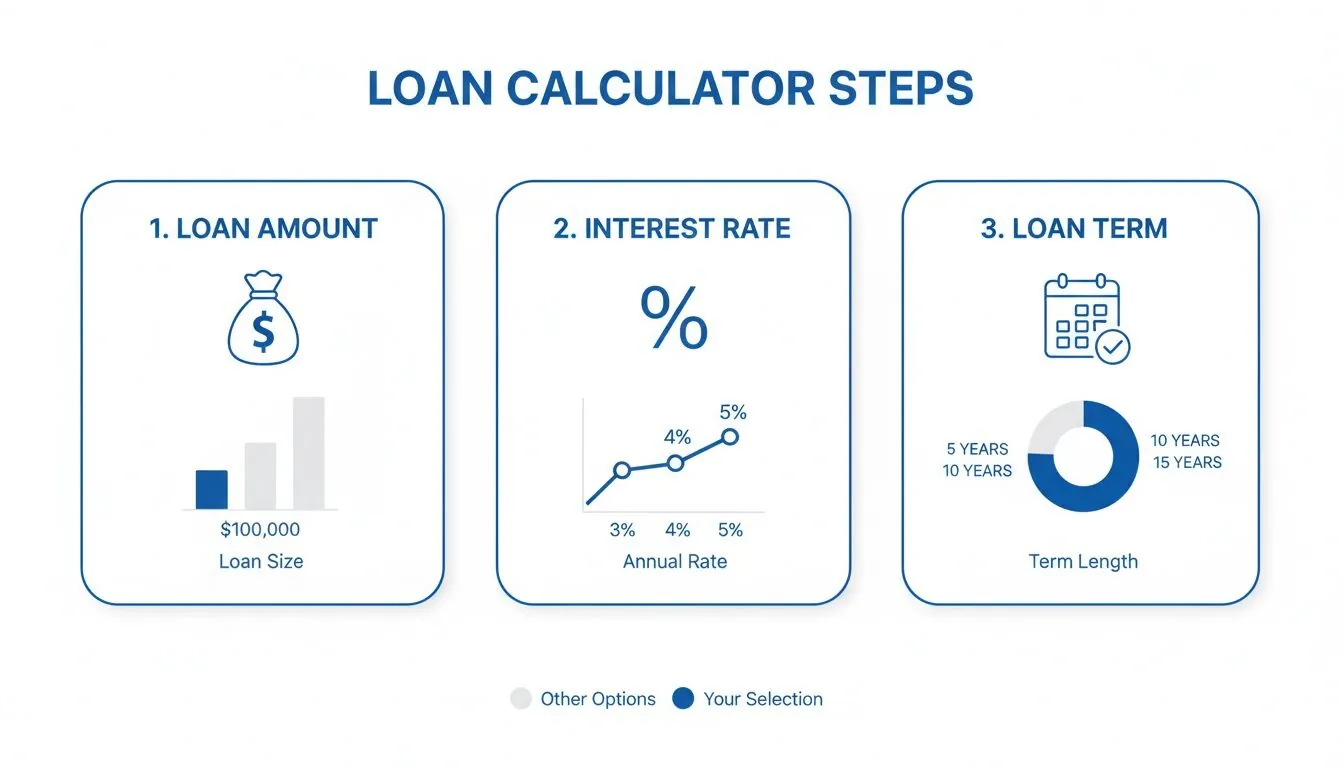

Before you can figure out how much you can save, you need the basic facts about your loan. Think of these as the ingredients for your debt-payoff recipe.

You’ll almost always need to enter these three things:

- Original Loan Amount: This is the total you borrowed at the very beginning. For a mortgage, it’s the home price minus your down payment.

- Interest Rate: Your Annual Percentage Rate (APR). Be precise here—even a fraction of a percent makes a big difference over time.

- Loan Term: The original length of your loan, usually in years (30 years for a mortgage, 5 years for a car loan, etc.).

Here’s a quick look at a typical calculator’s interface. It’s clean, straightforward, and gets right to the point.

As you can see, the layout is designed for clarity, asking for specific inputs like the loan amount, term, and interest rate, along with the extra payment you’re thinking about making.

A Practical Student Loan Example

Let’s put this into practice with a real-world scenario: a student loan. Imagine you’re working with a $30,000 student loan that has a 6.5% interest rate and the standard 10-year repayment term. Your regular monthly payment comes out to about $341.

Now, let’s say you’ve crunched your budget and realized you can comfortably add an extra $100 each month toward that loan. You’d just pop those numbers into the calculator.

This is where the magic happens. The calculator instantly spits out your new, earlier payoff date and—most importantly—the total interest you’ll save. This isn’t just an abstract number; it’s real money that stays in your pocket.

By adding that extra $100 a month, you’d be done with that student loan in just 7 years and 4 months, not the full 10 years. Even better? You’d save $2,965 in interest payments along the way. That’s a huge win for a relatively small monthly change.

This simple exercise turns debt repayment from something passive into an active strategy you control. You’re no longer just sending in payments; you’re actively shortening your loan’s life and cutting its total cost.

For those juggling multiple debts, our guide on using a debt payoff calculator spreadsheet can help you organize and accelerate your entire payoff plan. The calculator shows you the what, and a good strategy tells you the how.

Real-World Scenarios Where Extra Payments Make a Difference

Theory is great, but seeing how these strategies play out in the real world is what really drives the point home. The true power of an extra payment calculator is its ability to turn your abstract financial goals into a concrete, actionable plan. Let’s walk through a few common scenarios to see what I mean.

This is the starting point for any loan calculation—you just need the loan amount, interest rate, and the original term. It’s that simple.

Once you have these three variables plugged in, you can start modeling different scenarios to find the fastest path to being debt-free.

The First-Time Homebuyer’s Mortgage

Picture a couple who just bought their first house with a $350,000, 30-year mortgage at a 6.25% interest rate. Their standard monthly payment comes out to $2,154. After settling in, they figure out they can comfortably add an extra $150 to each payment. It might not seem like much against a loan that size, but the long-term impact is huge.

When you run these numbers, the result is pretty powerful. That small extra payment shaves 4 years and 3 months off their mortgage. Even better, it saves them a staggering $58,110 in total interest. It’s a perfect example of how small, consistent efforts compound into a massive win.

| Scenario | Extra Monthly Payment | Loan Paid Off In | Total Interest Savings |

|---|---|---|---|

| Standard Mortgage | $0 | 30 years | $0 |

| Accelerated Plan | $150 | 25 years, 9 months | $58,110 |

The Everyday Auto Loan

Next up, let’s look at a typical $25,000 car loan. This one has a 5-year term and a 7% interest rate, making the monthly payment $495. The owner decides to simply round this up to an even $550 each month—an extra $55.

This easy “round-up” strategy gets them the car title 6 months earlier. The total interest savings of $462 might feel small compared to a mortgage, but it’s still cash back in their pocket. More importantly, it frees up that $550 payment a half-year sooner, which can then be put toward other financial goals.

The High-Interest Personal Loan

Finally, consider a $10,000 personal loan for a home repair. It comes with a steep 12% interest rate over a 3-year term, and the monthly payment is $332. Six months in, the borrower gets a bonus from work and decides to make a one-time lump-sum payment of $2,000.

This single action has a dramatic effect.

A lump-sum payment applied directly to the principal of a high-interest loan is one of the most effective ways to cut down borrowing costs. It immediately stops that portion of the balance from accruing more interest.

The calculator shows this $2,000 payment saves $670 in interest and knocks 7 months off the loan term. This strategy is incredibly effective for high-interest debt, where every dollar paid toward principal saves you from future interest charges. It’s also a powerful method for other high-interest debts; you can find more information in our guide to student loan payoff strategies.

These examples just scratch the surface, but they show how an extra payment calculator can illuminate the best path forward, no matter what kind of loan you have.

Smart Strategies for Finding Extra Payment Money

Once you’ve plugged numbers into an extra payment calculator, the savings are crystal clear. But then comes the big question: where is this “extra” money supposed to come from?

Finding room in your budget to attack debt isn’t about making drastic, painful sacrifices. It’s about being clever and creating a sustainable plan that works for you. The most effective approach combines small, consistent habits with the smart use of any larger cash windfalls you might receive.

Put Your Payments on Autopilot

One of the easiest ways to guarantee success is to automate your strategy. When it runs in the background, there’s zero temptation to spend that money elsewhere.

-

Switch to Bi-Weekly Payments: Instead of one big payment each month, try splitting it in half and paying that amount every two weeks. There are 26 bi-weekly periods in a year, which means you’ll naturally make 13 full monthly payments instead of 12. It’s a simple but brilliant trick that adds an entire extra payment each year without feeling like a major hit to your budget.

-

Round Up Your Payments: Just like we did in the car loan example, rounding up your payment to the nearest $50 or $100 is an easy win. This “set it and forget it” method can shave months off your loan term and save you hundreds in interest over time.

Capitalize on Financial Windfalls

Another powerful tactic is to earmark any unexpected or non-regular income directly for your debt. These one-off cash infusions can make a serious dent in your principal balance.

Think about dedicating funds from sources like:

- Annual work bonuses

- Tax refunds

- Cash gifts from holidays or birthdays

- Raises or promotions

It’s incredibly tempting to treat windfalls as “fun money.” While you should absolutely celebrate your successes, dedicating even 50% of a bonus to your highest-interest loan can fast-track your payoff timeline. The long-term savings will far outweigh the temporary thrill of spending it all.

Actively Grow Your Income

Beyond trimming your spending, the most direct path to finding more money for debt is to simply earn more. The rise of the gig economy and remote work has opened up a world of opportunities to boost your income on your own terms.

To really ramp up your ability to make extra payments, think about building new skills. You can explore some great ideas in this list of 10 High Income Skills for Side-Hustlers to see what might fit your interests. Even an extra few hundred dollars a month from a side project can have the same impact as years of just rounding up your payments.

One last critical tip: always talk to your lender. When you send an extra payment, make it clear that the money should be applied directly to the principal balance. This ensures your money is working as hard as possible to reduce what you owe, not just covering next month’s interest early. A quick phone call or a note included with your payment can make all the difference.

Connecting Your Payoff Plan to Your Net Worth Growth

An extra payment calculator is fantastic for showing you that glorious debt-free date. But its real magic happens when you zoom out and see how it fits into your entire financial picture. The most powerful motivator I’ve found on my own wealth-building journey is watching how every single extra payment directly pumps up my net worth.

The idea is simple but incredibly effective. Your net worth is just your assets (what you own) minus your liabilities (what you owe). Each time you throw extra cash at a loan, you’re doing a little financial two-step that massively speeds up your progress.

The Double Impact of Each Payment

First, you’re knocking down your liabilities. That extra $100 you just sent to your student loan servicer? It permanently chips away at your total debt. But here’s the cool part: because that $100 is no longer a liability, it also boosts your net worth by the exact same amount.

This creates an amazing positive feedback loop. The more debt you crush, the more solid your financial foundation becomes. You’re shifting from playing defense—paying for the past—to playing offense and building for your future.

Every dollar sent to pay down principal isn’t just a transaction; it’s an investment in your own financial freedom. It reduces the interest you’ll pay tomorrow and frees up capital for growth opportunities down the line.

Tracking Your Progress Visually

Trying to track all this manually is a pain. This is where a good net worth tracker like PopaDex becomes your best friend. Link up your loan accounts, and you can watch your liability balances shrink in near real-time after every payment.

Seeing that visual confirmation is so rewarding. Instead of just watching money leave your bank account, you get to see your net worth chart physically tick upward month after month. It turns debt repayment into a game you’re determined to win.

From Debt Reduction to Wealth Creation

Ultimately, the goal is to flip the switch from paying off debt to actively investing. As soon as a loan is gone, that entire monthly payment—both the principal and all the interest you were paying—is suddenly free.

This newfound cash flow is your new engine for building wealth. That $400 a month that was disappearing into a car loan can now be rerouted into a retirement account, a brokerage fund, or savings for a real estate down payment.

Your debt payoff plan is a critical piece of the puzzle. It’s not just about getting to zero; it’s about building a foundation for lasting prosperity. If you’re thinking bigger, there are many strategies for creating generational wealth that start right here. Using an extra payment calculator helps you map out not just when you’ll be debt-free, but more importantly, when you can truly start making your money work for you.

Got Questions About Extra Payments? We’ve Got Answers.

Even when you’ve run the numbers through an extra payment calculator, a few practical questions always pop up. It’s smart to get these details sorted out before you start sending extra cash to your lender. Making sure your money is working for you—and not against you—is the whole point.

Here are the most common questions we hear from people ready to kick their debt to the curb.

How Do I Make Sure My Extra Payment Hits the Principal?

This is, without a doubt, the most critical piece of the puzzle. If you just send a bigger check, some lenders will simply apply the extra funds toward your next month’s payment. That just means you’re paying future interest early, not actually shrinking the loan balance. You don’t want that.

You have to be explicit.

- Online Payments: Look for a specific field labeled “additional principal,” “principal-only payment,” or something similar. It’s usually right on the payment screen.

- Paper Checks: Write “For Principal Only” and your loan number directly on the memo line. This creates a clear paper trail.

- When in Doubt, Call: A quick phone call to your lender’s customer service can clear up any confusion about their process. It’s five minutes well spent to avoid any headaches later.

Are There Penalties for Paying Off a Loan Early?

Sometimes, yes. Mortgages and auto loans can occasionally come with prepayment penalties, which are exactly what they sound like: a fee for paying off your loan ahead of schedule. They’re less common than they used to be, but you absolutely need to check.

The only way to know for sure is to dig up your original loan agreement and read the fine print.

While federal laws have put some restrictions on prepayment penalties for most mortgages, it’s always best to read your documents or call your lender to be 100% sure. Personal loans and student loans, on the other hand, almost never have them.

Can I Make Extra Payments on Any Type of Loan?

Absolutely. The math behind amortization works the same way for almost any kind of installment debt. You can use this strategy to get ahead on your:

- Mortgage

- Auto Loan

- Student Loans

- Personal Loan

You’ll see the biggest impact on loans with long terms (like a 30-year mortgage) or high interest rates. That’s where shaving off time and interest really adds up. An extra payment calculator will show you exactly where your money can make the most dramatic difference.

Should I Pay Extra on My Debt or Invest the Money?

This is the classic debate in personal finance, and there’s no single right answer for everyone. The standard advice is to compare your loan’s interest rate to what you could reasonably expect to earn from investments. If your student loan is at 5% but you’re confident you can average an 8% return in the stock market over time, investing seems like the better financial move.

But it’s not just about the raw numbers. Paying off debt delivers a guaranteed, risk-free return equal to your interest rate. Knocking out that 5% loan is the same as earning a guaranteed 5% on your money, tax-free. Plus, it frees up your cash flow and provides a huge sense of relief and accomplishment.

Many people find a hybrid approach works best—tackling some debt while still investing for the future.

Ready to see how these strategies could transform your own financial picture? The PopaDex net worth tracker is the perfect place to put this knowledge into action. Connect all your loans and assets in one dashboard and watch your liabilities shrink—and your net worth soar—with every single extra payment you make.