Our Marketing Team at PopaDex

Master Your Finances with a Future Value of Money Calculator

A future value of money calculator is a surprisingly powerful tool. At its core, it shows you what a chunk of cash invested today could grow into at a specific point down the road. It does this by taking your initial investment, applying an expected interest rate over a set period, and revealing the potential of your money. This calculation isn’t just a party trick for finance nerds; it’s the bedrock of any serious long-term financial plan, from figuring out your retirement number to hitting a savings goal.

What Is the Future Value of Money

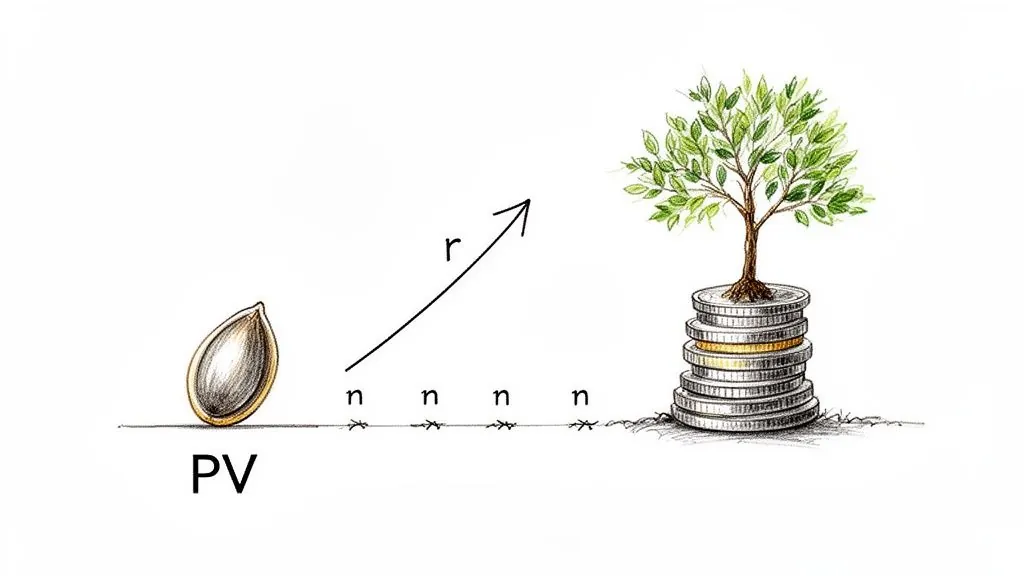

Think of your money as a seed. If you plant it today by investing it, that seed has the potential to grow into a much larger money tree over time. This simple, powerful concept is the whole idea behind the future value of money. It’s the reason a dollar in your hand right now is worth more than the promise of a dollar a year from now.

Why? Because the money you have today can be put to work. It can be invested to earn a return—a fundamental principle often called the time value of money. This growth isn’t magic, though. It relies on three core components working in harmony.

The Core Ingredients of Growth

To really get future value, you just need to understand its three basic building blocks. No finance degree required—each one plays a simple, logical role in how your money can multiply.

- Present Value (PV): This is just the cash you have on hand right now. It’s your starting point, the initial “seed” you’re planting for the future.

- Interest Rate (r): Think of this as the “growth rate” for your money. It’s the percentage return you expect to earn on your investment, usually expressed as an annual figure.

- Time (n): This is how many periods (like years) your money has to grow. Time is arguably the most powerful ingredient of all because it’s what allows your earnings to compound on themselves.

The real magic happens when your money earns interest, and then that interest starts earning its own interest. This snowball effect, known as compounding, is what drives incredible wealth creation over the long haul.

Once you get a handle on these three elements, you can start making some seriously informed projections about where you’re headed financially. A future value of money calculator just takes the manual labor out of it, plugging these variables into a formula to give you a clear picture of what your wealth could look like years from now.

How to Calculate Future Value Step by Step

Let’s be honest, the math behind your money’s growth can sound pretty intimidating. But the good news is, the core ideas are simpler than you think. Once you get a handle on two key formulas, you’ll see exactly what’s happening inside any future value calculator, empowering you to map out your own financial future.

The Power of a Single Investment (Lump Sum)

We’ll start with the most common scenario: figuring out the future value of a single, one-time investment. Think of it as a lump sum.

Imagine you get a $5,000 bonus. Instead of spending it, you decide to invest it for the long haul. Here’s the simple formula that shows you how it can grow.

The formula is: FV = PV * (1 + r)^n

Let’s quickly translate that into plain English.

- PV (Present Value): This is your starting cash. In our example, the PV is $5,000.

- r (Interest Rate): This is your expected annual return on the investment. Let’s say you anticipate an average of 7% per year, which means r = 0.07.

- n (Number of Periods): This is how many years you let your money cook. We’ll plan for 10 years, so n = 10.

When you plug those numbers in, you get: FV = $5,000 * (1 + 0.07)^10.

Without you lifting another finger, that initial $5,000 could grow to roughly $9,835.76 over a decade. That’s the magic of compounding in action.

The Game-Changer: Regular Contributions

But what if you don’t just invest once? What if you’re putting money away consistently, like saving $200 every month for retirement? This is where things get really exciting.

This stream of regular payments is known as an annuity, and it uses a slightly different formula. It has to account for every single new contribution growing over its own unique timeline.

While the math gets a bit more complex, the result is far more powerful. Those steady additions, combined with the compounding returns on your growing balance, create a financial snowball that picks up speed and size dramatically. Thankfully, a good future value calculator does all the heavy lifting for you.

To see what I mean, let’s take that same $5,000 lump sum. Now, let’s add just $100 per month to it for 10 years at that same 7% return. You’ve added an extra $12,000 over the decade, but the total future value skyrockets to over $26,900.

This is why consistent saving is the undisputed champion of wealth-building. It isn’t just about how much you start with; it’s the habit of feeding your investments regularly that truly builds a significant nest egg. Understanding how both a strong start (lump sum) and steady effort (annuity) work together is the key to planning your financial goals.

Unlocking The Power Of Compounding And Time

If you’ve ever heard that time is your greatest ally in building wealth, compounding is the simple reason why. It’s like a snowball rolling downhill—it starts small, but as it rolls, it picks up more snow, getting bigger and moving faster with every rotation.

Your money works the exact same way. It earns returns, and then those returns start earning their own returns. This is the self-fueling cycle that drives long-term growth. At first, the progress feels slow, almost unnoticeable. But give it a few years, and the effect starts to accelerate dramatically. This is how modest, consistent investments eventually transform into substantial wealth and precisely why investing is more powerful than saving.

This diagram breaks down the three core ingredients that work together to grow your money over time.

As the chart shows, it’s the powerful combination of your initial principal, the interest rate you earn, and the amount of time you stay invested that truly drives the results.

How Compounding Frequency Changes Everything

It’s not just about if your money compounds, but how often. The more frequently your investment returns are calculated and added back into the pot, the faster your money grows. We call this the compounding frequency.

Common schedules include:

- Annually: Your interest is calculated just once per year.

- Monthly: Interest is added to your balance 12 times per year.

- Daily: Your earnings are calculated and reinvested 365 times a year.

It might seem like a minor detail, but a higher frequency means your earnings start working for you that much sooner. Over a long timeline, this tiny edge can lead to a much larger outcome. To really get a handle on this, check out our detailed guide on understanding compound interest.

Key Takeaway: The more often your interest compounds, the harder your money works. Even with the same annual interest rate, daily compounding will always beat annual compounding over the same time frame.

Let’s look at a real-world example. Imagine you invest $10,000 for 20 years at a 6% annual interest rate. Here’s how the compounding frequency alone changes the final amount.

Impact of Compounding Frequency on a $10,000 Investment Over 20 Years at 6% APR

This table shows just how much the final value of your investment can change based on how often the interest is calculated and added.

| Compounding Frequency | Future Value (FV) |

|---|---|

| Annually | $32,071.35 |

| Monthly | $33,102.04 |

| Daily | $33,197.94 |

See that? The jump from annual to monthly compounding adds over $1,000 to your final pot without you lifting a finger. While the difference between monthly and daily is less dramatic, it still proves the point: more is better.

A good future value calculator handles all these complex calculations for you, showing exactly how these small details impact your long-term goals.

Factoring in Inflation for a Realistic Financial Picture

Figuring out how much your money could grow is exciting, but it’s only half the story. A silent opponent is always working against your savings, slowly eating away at their value. That opponent is inflation, and if you ignore it, you’re planning with one eye closed.

Simply put, inflation is why a dollar today buys more than a dollar tomorrow. The $100,000 you’re aiming for in 20 years just won’t stretch as far as $100,000 does right now. Overlooking this simple truth can leave you with a retirement fund that looks great on paper but feels disappointingly small when it’s time to actually use it.

Any good future value of money calculator needs to account for this, giving you a much truer sense of where you’ll stand.

Nominal Value vs. Real Value

When you calculate future value without thinking about inflation, you get the nominal value. This is the face value of your money—the straightforward number your investment is projected to hit. It’s a useful starting point, but it isn’t the whole truth.

The number you really need to focus on is the real value. This is your future money adjusted for inflation, showing you its actual purchasing power in today’s dollars. Think of it as the true measure of your future wealth.

Key Insight: Your goal isn’t just to pile up a specific number of dollars. It’s to build enough wealth to afford the life you want. The real value tells you if you’re actually on track to do that.

History shows just how much of a bite inflation can take. Imagine you had $10,000 in the year 2000. By 2020, cumulative inflation in the U.S. was nearly 50%. That means you’d need almost $15,000 in 2020 just to buy the same things you could with your original ten grand—and that’s before any investment growth. You can see more examples of this by exploring how purchasing power has changed over time on in2013dollars.com.

Calculating the Real Rate of Return

To get an inflation-adjusted future value, you first need to find your real rate of return. This simple calculation strips the effect of inflation out of your expected investment returns, giving you a more honest growth rate.

The formula looks more complicated than it is:

- Real Rate of Return = [(1 + Nominal Rate) / (1 + Inflation Rate)] - 1

Let’s run through a quick example. Say you expect your investments to earn 7% a year (your nominal rate), and you assume inflation will average about 3% per year.

- Your real rate of return would be roughly 3.88%.

This is the number you should plug into a future value calculator to project the actual purchasing power of your future savings. By planning with this more conservative, down-to-earth figure, you ensure your financial goals are built on a solid foundation, not just wishful thinking.

Using a Future Value Calculator for Real-Life Goals

Those formulas and compounding tables are great in theory, but where they really shine is when you start plugging in your own numbers. A future value of money calculator is what connects the dots between abstract financial ideas and your actual, real-life goals. It takes a big dream—like a comfortable retirement or a down payment on a house—and boils it down to a set of clear, actionable figures.

This hands-on approach is a game-changer. It shifts your mindset from just hoping you’ll have enough money to actively planning for it. Suddenly, you’re in the driver’s seat, building a financial roadmap and making adjustments as you go.

Planning for Retirement

Let’s walk through a common scenario. Imagine a 25-year-old just starting their career. They’ve set a goal to have a $1.5 million nest egg by the time they hit 65. Right now, they’ve got $10,000 saved in a retirement account.

Here’s how they’d use a future value calculator to see if their current plan cuts it:

- Present Value (PV): They start by plugging in $10,000.

- Number of Periods (n): They have 40 years until retirement, so n = 40.

- Interest Rate (r): They assume a pretty conservative average annual return of 7%, so r = 7.

- Periodic Payment (PMT): They’re committed to contributing $500 every single month.

The calculator crunches the numbers and projects a future value of around $1.48 million. This is fantastic news! It shows them their plan is almost perfectly on track to meet their goal, which provides a massive confidence boost to keep it up. This is a perfect first step before digging deeper with a more detailed retirement nest egg calculator.

Saving for a House Down Payment

Now, picture a couple aiming to buy their first home in five years. They need to save up $60,000 for the down payment and are starting with $5,000 in a high-yield savings account that earns 4% annually.

They can use the calculator to work backward and figure out their required monthly savings:

- Future Value (FV): Their target is $60,000.

- Present Value (PV): They’re starting with $5,000.

- Number of Periods (n): Their timeline is 5 years, which is 60 months.

- Interest Rate (r): Their account earns 4% a year, which works out to roughly 0.33% per month.

The calculator solves for the monthly payment and tells them they need to save about $845 per month. Just like that, a huge, intimidating goal is broken down into a manageable monthly target.

A wise investment of just $100 can grow into a significant sum, but only with precise calculations that account for real-world factors like taxes and inflation. For instance, $100,000 invested in 1990 at a 7% return would have grown to about $379,000 by 2019. However, after accounting for a 97.58% surge in inflation and a 20% tax rate, its real purchasing power shrinks to just $126,500 in 1990 dollars.

This kind of detailed planning is absolutely essential, particularly for entrepreneurs and property investors. For anyone looking to make smarter decisions on different assets, a good guide on using a real estate investment calculator can provide invaluable financial analysis. When you use these tools, you stop guessing and start making strategic moves that build real, lasting wealth.

Turning Future Value Projections Into Action

Okay, so you’ve crunched the numbers. What now? A calculation is only as good as the action it inspires. Using a future value of money calculator isn’t a one-and-done task; think of it as a regular, dynamic part of your financial health check-up. It’s what turns abstract goals into concrete numbers you can actually work toward.

This is the bridge between a simple projection and a robust financial strategy. The figures you get from the calculator become your benchmarks, giving you tangible targets for your net worth and investment goals. This creates a powerful feedback loop where you plan, track your progress, and adapt as you go.

Setting Meaningful Benchmarks

Your future value calculation essentially gives you a destination on your financial map. For example, if you project your retirement fund needs to hit $250,000 in the next ten years, you suddenly have a clear milestone to aim for. That big, intimidating number can now be broken down into smaller, more manageable steps.

To stay organized and focused, it helps to outline these targets in a structured way. Our guide on creating a financial goal setting worksheet gives you a clear framework for turning these projections into a documented plan. This step is what translates numbers on a screen into a real-world strategy you can follow.

The most effective financial plans are living documents, not static reports. Regularly comparing your actual progress to your projections is what keeps you on the path to success, allowing for course corrections before you drift too far off track.

Monitoring Performance and Adapting

Once your benchmarks are set, the real work begins: monitoring how your portfolio is actually performing against your calculated targets. Life happens. Markets fluctuate. Your initial assumptions about interest rates or how much you can contribute might need a second look over time.

This is where a net worth tracker like PopaDex becomes incredibly valuable. It gives you a real-time snapshot of your financial position, which you can then hold up against your future value projections.

Here’s how to make it work:

- Track Your Progress: Check in quarterly or annually. Are your investments growing at the rate you expected?

- Identify Deviations: If your portfolio is lagging, you can dig in and figure out why. Is it just a temporary market dip, or does your investment allocation need a rethink?

- Adjust Your Strategy: Based on what you find, you might decide to increase your monthly contributions, rebalance your assets, or even adjust your timeline.

By regularly reviewing and adapting, you make sure your financial plan stays realistic and aligned with your ultimate goals. This kind of active management is the key to turning a simple calculation into lasting wealth.

Frequently Asked Questions

When you start plugging numbers into a future value of money calculator, a few questions almost always pop up. Let’s clear up some of the common ones so you can build a more solid financial plan.

What Is the Difference Between Present Value and Future Value?

Think of Present Value (PV) and Future Value (FV) as two sides of the same coin, separated only by time and your money’s potential to grow.

- Present Value (PV) tells you what a future chunk of cash is worth right now. It answers, “If I want to have $100,000 in 20 years, how much do I need to invest today to get there?”

- Future Value (FV) is the opposite. It tells you what today’s money will grow into over time. It answers, “If I invest $10,000 today, what will it be worth in 20 years?”

Essentially, PV looks backward from a future goal to find today’s starting point, while FV looks forward from today’s investment to see where you’ll end up.

Can a Future Value Calculator Be Wrong?

The math itself is never wrong—it’s just arithmetic. But the final number is a projection, not a promise. The calculator’s reliability is 100% dependent on the accuracy of the numbers you feed it.

A future value calculation is a planning tool, not a crystal ball. Unexpected changes in interest rates, inflation, or your contribution amounts will alter the actual outcome.

Your result is only as good as your assumptions. If you project a 7% return but your investments only earn 5%, your final balance will naturally be lower than you planned.

How Often Should I Recalculate My Future Value?

Financial planning isn’t a “set it and forget it” task. Life happens, and your plan needs to adapt. It’s smart to revisit and recalculate your future value projections at least once a year.

You should also crunch the numbers again after any significant life event, such as:

- Getting a raise or starting a new job

- Making a big change to your investment strategy

- Adding a new long-term financial goal to your list

This keeps your plan aligned with where you are now and where you want to go.

Does Future Value Account for Taxes?

Most standard future value calculators don’t automatically factor in taxes on your investment gains. For a more grounded, realistic projection, you should plug in an estimated after-tax rate of return. This will give you a much clearer idea of what you’ll actually get to keep.

Ready to turn projections into progress? PopaDex helps you track your entire portfolio in one place, so you can see how your actual performance stacks up against your future value goals. Get clarity on your financial journey today.