Our Marketing Team at PopaDex

How Much Money to Retire Comfortably Uncovering Your Number

Figuring out how much you really need to retire is a question that stumps almost everyone. The truth is, it all comes down to a surprisingly simple concept: your retirement number is just a reflection of your future spending. While you hear big numbers like $1 million or $1.5 million thrown around, the right answer for you is completely tied to the life you want to live.

What Does a Comfortable Retirement Actually Cost?

Before you can even think about running numbers, you need a vision. My idea of “comfortable”—maybe some gardening and a few road trips—could be worlds apart from your dream of sailing around the world. The goal is to get past those fuzzy daydreams and start putting real dollar signs on your future.

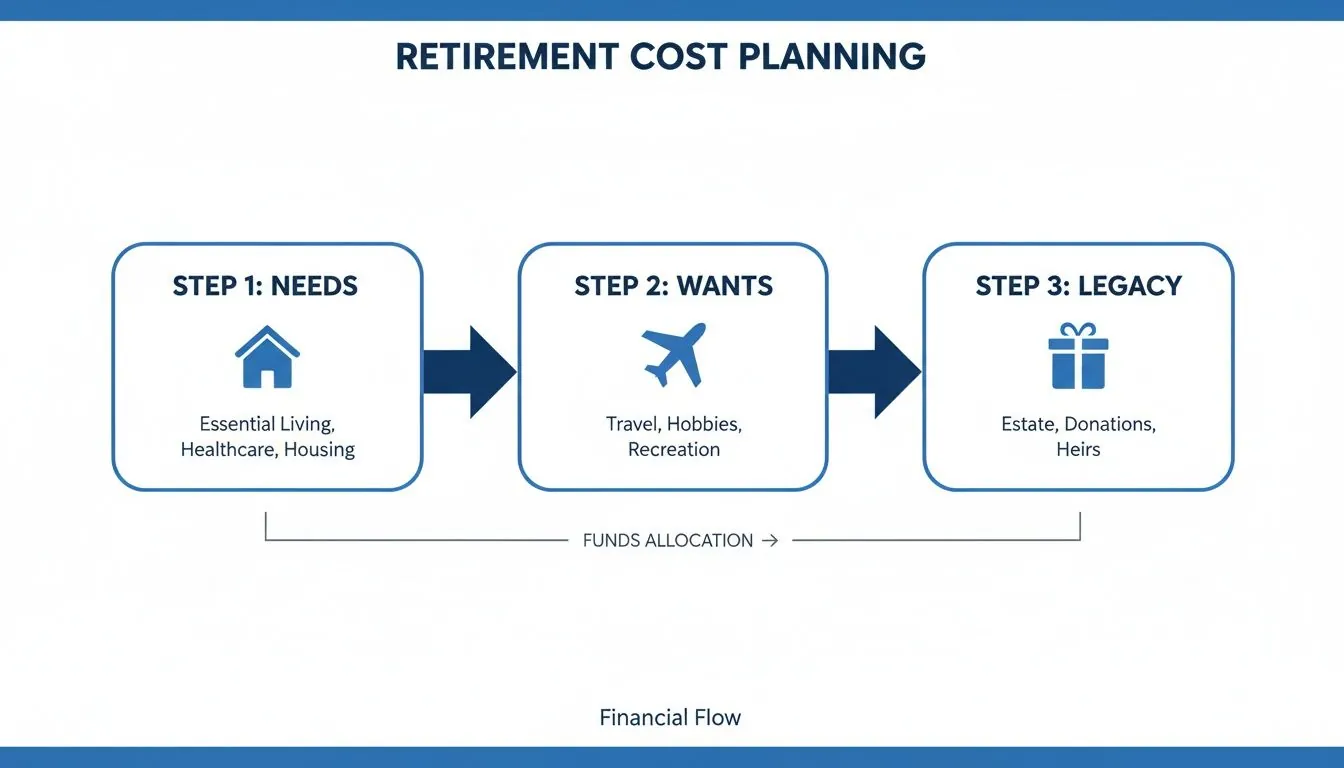

The best way I’ve found to tackle this is by breaking down your future life into three simple spending buckets. It turns an overwhelming question into a much more manageable exercise.

Defining Your Core Needs

This is the bedrock of your budget—the absolute must-pays. These are the bills that will show up every month, no matter what. Getting this number right is the foundation of your entire plan.

- Housing: Will your mortgage be gone? Awesome, but don’t forget property taxes, insurance, HOA fees, and the inevitable roof repair. If you’re planning to rent, what’s a realistic monthly cost for the area you want to live in?

- Healthcare: This is the big one that people consistently underestimate. A 65-year-old couple can expect to spend over $330,000 on healthcare throughout their retirement. You need to account for Medicare premiums, supplemental plans, prescription costs, and the potential for long-term care.

- Utilities & Transportation: The basics still count. Electricity, water, internet, and your phone bill all add up. Same goes for car payments, insurance, gas, and maintenance—or the cost of Ubers and public transit if you go car-free.

Outlining Your Wants and Desires

Okay, this is the fun part. This is where your retirement dream actually starts to take shape. These are the discretionary expenses that make life worth living, and being brutally honest here is what makes or breaks your retirement number.

“Travel,” for instance, is not a budget line item. Is it one huge international trip a year for $10,000? Or is it four long-weekend getaways by car that total maybe $2,000? The difference is massive.

Key Takeaway: Your lifestyle is your retirement number. Someone whose ideal year costs $40,000 has a completely different savings goal than someone whose dream life runs $90,000 a year.

Get specific with your list:

- Travel: How often, where to, and in what style (hostel or hotel)?

- Hobbies: Think golf memberships, art supplies, language classes, or that fancy woodworking equipment you’ve always wanted.

- Entertainment: Dinners out with friends, concert tickets, streaming subscriptions, and social clubs.

- Shopping: A realistic budget for new clothes, the latest tech, or home decor.

Planning Your Legacy Goals

Finally, think beyond yourself. What kind of financial impact do you want to leave behind? For many people, these legacy goals are just as important as their own comfort, and they definitely need to be part of the financial picture.

This could mean a few different things:

- Financial support for family: Maybe helping grandkids with college tuition or giving your kids a hand with a down payment on their first home.

- Inheritance: How much do you hope to pass on to your heirs?

- Charitable giving: Do you want to make regular donations or even set up a small fund for a cause you’re passionate about?

By taking the time to put a realistic annual number on each of these three categories—Needs, Wants, and Legacy—you’ll have a concrete annual spending target. That number is the cornerstone of your entire retirement plan. It transforms the vague, scary question of “how much?” into a real target you can actually aim for.

Calculating the Retirement Number You Can Trust

Alright, you’ve figured out your annual spending target. Now comes the exciting part: turning that dream lifestyle into a real, tangible savings goal. This is where we stop guessing and start calculating what it will actually take to fund your retirement.

The classic starting point for this is a surprisingly simple rule of thumb that’s been a cornerstone of retirement planning for decades: the 4% Rule.

The idea is that you can safely withdraw 4% of your initial retirement portfolio in your first year, then adjust that amount for inflation every year after. Historically, this has given retirees a very high chance of their money lasting for at least 30 years.

To work backward from that, you just flip the math. This gives us the 25x Rule: multiply your desired annual retirement income by 25. This simple multiplication gives you a solid first estimate of the total nest egg you need to build.

The 25x Rule as a Starting Point

Think of the 25x Rule as your baseline—a quick, back-of-the-napkin calculation to understand the scale of what you’re aiming for. It immediately grounds your plan in reality.

For instance:

- If you need $60,000 a year in retirement, your target nest egg is $1.5 million ($60,000 x 25).

- If your ideal lifestyle costs $80,000 annually, you’re aiming for $2.0 million ($80,000 x 25).

Here’s a quick way to see how this plays out for different income levels.

Quick Estimate Your Retirement Nest Egg with the 25x Rule

Use this table for a fast calculation of the savings you’ll need based on your desired annual retirement income, using the classic 4% Rule.

| Desired Annual Retirement Income | Required Nest Egg (Income x 25) |

|---|---|

| $50,000 | $1,250,000 |

| $75,000 | $1,875,000 |

| $100,000 | $2,500,000 |

| $125,000 | $3,125,000 |

| $150,000 | $3,750,000 |

This calculation is a powerful first step. But—and this is a big but—it’s just a start. A rule of thumb developed in the 1990s might not be a perfect fit for a retirement starting in the 2040s. Market returns are never guaranteed, and for early retirees, a 30-year timeline might be cutting it too short.

Before you even get to the math, it helps to frame your spending priorities. This is the foundation of any good calculation.

As you can see, the process starts with defining your core needs, then layering on wants and legacy goals to build a complete financial picture.

Moving Beyond the 4% Rule

Because of all these uncertainties, many financial planners now favor more flexible withdrawal strategies. These modern approaches are designed to adapt to the market’s ups and downs, giving your portfolio a much better chance of lasting longer.

Expert Insight: Instead of being rigid, dynamic withdrawal strategies let you adjust your spending based on your portfolio’s performance. That might mean taking a little less in a down year to preserve your capital and maybe a bit more in a strong year to enjoy the gains.

A couple of popular alternatives include:

- Variable Percentage Withdrawal: This is simple. Instead of a fixed dollar amount, you withdraw a set percentage of your portfolio’s current value each year—say, 4% of whatever the balance is. Your income will fluctuate with the market, so you’ll need a flexible budget.

- The Guardrail Method: This approach sets upper and lower spending limits. You might start with a 4% withdrawal, but if a market dip pushes your withdrawal rate up to 5%, you’d cut back. On the flip side, if a bull market drops your rate to 3%, you could give yourself a raise.

The reality is that having a solid plan is crucial, especially when most people are behind on their savings. The 2025 Natixis Global Retirement Index found that while the average American has saved $1.048 million, they believe they’ll need $1.490 million to retire comfortably. That’s a shortfall of around $442,000.

Putting It All Together: A Couple of Scenarios

Let’s see how this plays out for two different people.

- A 45-Year-Old Planner: She wants to retire in 20 years with $70,000 in today’s dollars for annual expenses. Using the 25x rule, her initial target is $1.75 million. But given her long time horizon, she might use a more conservative 3.5% withdrawal rate, pushing her goal closer to $2 million to build in a bigger safety net.

- A 60-Year-Old Nearing Retirement: He plans to retire in 5 years and needs $90,000 a year. His 25x target is $2.25 million. Since his retirement is much closer and the timeline is shorter, he might feel more comfortable sticking with the standard 4% Rule, but he’ll need to be very diligent about factoring in future inflation.

No matter which approach you choose, it’s absolutely vital to adjust your final number for inflation. A goal of $1.5 million today won’t buy you the same lifestyle in 20 years.

Running these numbers with a good retirement nest egg calculator can show you exactly how different assumptions about inflation, returns, and withdrawal rates will impact your final goal.

Stress-Testing Your Retirement Plan with Real-World Scenarios

A single retirement number is a decent starting point, but let’s be honest—it’s calculated in a perfect world. Reality is messy. A truly solid plan is one that can bend without breaking when life inevitably throws you a curveball. That’s why stress-testing your assumptions is one of the most important steps you can take.

Think of it like a financial fire drill. This process involves running your plan through different scenarios to see how it holds up. By tweaking key variables like your retirement age, expected investment returns, and even your lifespan, you can spot potential weaknesses and build a much more robust strategy. It shows you where the exits are before you ever smell smoke.

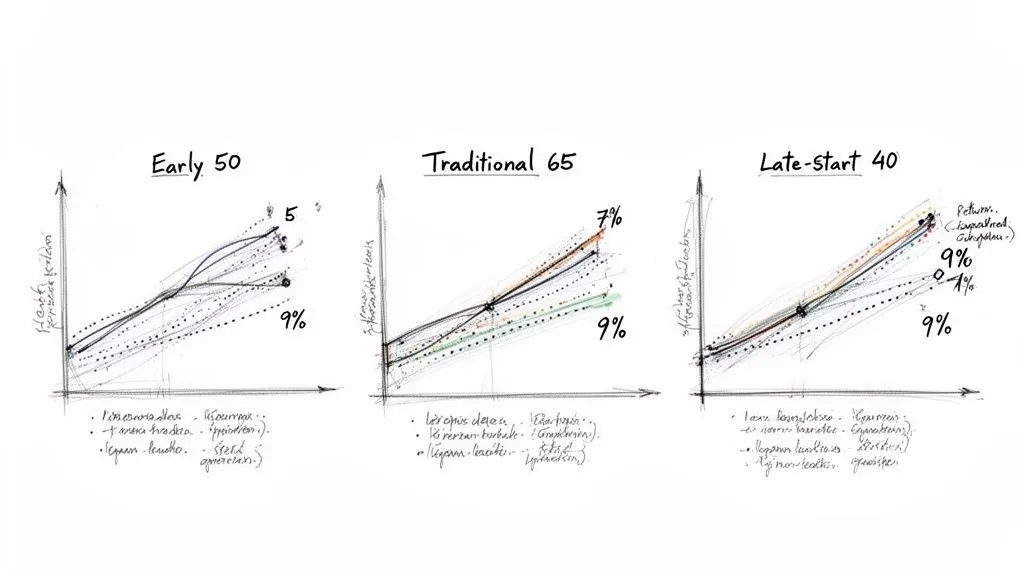

Case Study 1: The Early Retiree at 50

Meet Sarah. She’s gunning to retire at 50 with an annual spending goal of $70,000, which puts her 25x target at $1.75 million. The catch? Her retirement could easily last 40 years or more, a much longer horizon than the 30 years the 4% Rule was designed for.

This extended timeline introduces a monster risk: sequence of returns risk. If a nasty market downturn hits in the first few years of her retirement, it could cripple her portfolio’s ability to recover and last for four long decades.

Let’s run the numbers on her plan with different average annual returns:

- Conservative (5% return): At this rate, her portfolio really struggles to keep up with withdrawals and inflation over 40 years. She’d almost certainly need to slash her spending or work a few more years to build a bigger cushion.

- Moderate (7% return): This looks much more sustainable. Her $1.75 million portfolio has a strong chance of making it, provided she can stay disciplined with her budget during market swings.

- Aggressive (9% return): With these returns, her plan succeeds with flying colors, and her nest egg would likely keep growing. The trade-off is that a consistent 9% average return requires a higher-risk portfolio she might not be comfortable with once she’s no longer earning an income.

Key Insight: For early retirees, a longer timeline magnifies the impact of both market returns and withdrawal rates. A more conservative withdrawal rate, maybe around 3.5%, would be a much safer bet. This bumps her target to $2 million but makes her plan significantly more durable.

Case Study 2: The Traditional Retiree at 65

Now let’s look at David, who’s on track for a traditional retirement at 65. His desired annual income is $90,000, giving him a savings target of $2.25 million. Since his timeline is a more standard 30 years, the 4% Rule is a much better benchmark.

For David, the main variables are investment performance and just how long he lives. What if he makes it to 100? What if his returns are lower than he hopes?

Here’s how his $2.25 million nest egg might fare:

- Living to 85: The plan is very likely to succeed, even with conservative 5% returns. No sweat.

- Living to 95: With moderate 7% returns, his portfolio holds up just fine. But if returns dip into the 5% range, he’s in danger of running out of money in his final years.

- Living to 100+: To fund a 35-year retirement, he’ll need his portfolio to deliver consistent, moderate returns. It’s a powerful reminder not to get overly conservative with investments too early in retirement.

Beyond the markets, a crucial part of stress-testing any plan involves thinking about late-in-life expenses. It’s essential to understand how to protect assets from nursing home costs, as these can completely derail an otherwise solid financial plan.

Case Study 3: The Late Starter at 40

Finally, there’s Maya. She’s 40 and just started saving aggressively. Her goal is to retire by 67 with $60,000 a year, which means she needs to save $1.5 million in just 27 years. For her, everything hinges on her savings rate and the investment returns she earns before she retires.

Her challenge is pure accumulation. Let’s see how different return rates affect her ability to hit her goal, assuming she socks away $2,000 every month:

- Conservative (5% return): After 27 years, she would have around $1.37 million. She’s close, but she’d need to ramp up her savings rate to get over the finish line.

- Moderate (7% return): This is the sweet spot. Her savings would grow to over $1.9 million, comfortably clearing her goal and giving her a fantastic buffer.

- Aggressive (9% return): At this rate, she’d amass over $2.7 million, putting her in an incredible financial position.

These examples make it clear: your retirement “number” isn’t set in stone. It’s a dynamic target that shifts with your timeline, risk tolerance, and all of life’s uncertainties.

For a deeper look, using tools for scenario forecasting and financial planning can give you a much more personalized and detailed picture of your own situation. By running these “what-if” scenarios, you can build a plan that’s not just optimistic, but truly resilient.

Tracking Your Net Worth and Staying on Course

Figuring out your retirement number is like picking a destination on a map. But a map alone won’t get you there; you need to navigate the actual journey. Without a reliable compass, it’s easy to get lost. This is where tracking your progress comes in—it turns a far-off goal into something you can manage today.

Let’s be blunt: you can’t manage what you don’t measure. Trying to keep tabs on your savings, investments, and debts scattered across a dozen different accounts is a logistical nightmare. The only way to get a true picture of where you stand is to pull everything into one place.

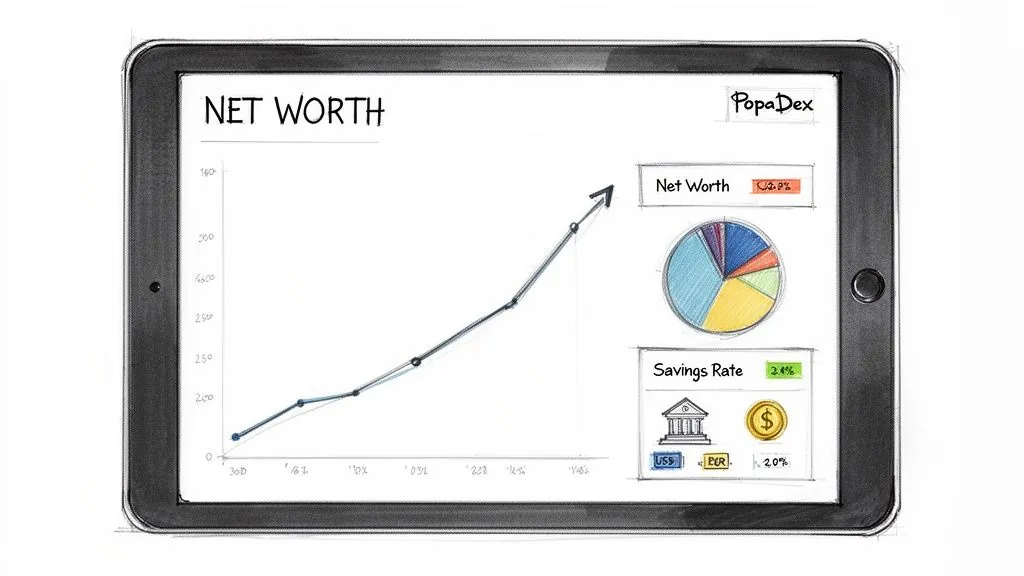

That holistic view all boils down to one critical number: your net worth. This is the single most effective metric for tracking your journey. It’s the value of everything you own minus everything you owe, and watching it grow is how you know you’re on the right track.

Building Your Financial Dashboard

Your first move is to set up a central hub where all your financial data can live. The old-school method is a manual spreadsheet, but let’s be honest—it’s tedious, time-consuming, and easy to mess up. Modern tools are built to do the heavy lifting for you, automating the process and giving you insights in real-time.

A platform like PopaDex streamlines all of this by connecting directly to your bank accounts, investment platforms, and credit cards. It automatically pulls all that data into a single, clean dashboard. It even handles multiple currencies, which is a massive plus for anyone with international assets.

Here’s a glimpse of what a consolidated dashboard looks like, giving you that crucial snapshot of your financial life.

This kind of visual makes it instantly clear how your net worth is trending and how your money is allocated, so you can quickly spot what’s working and what isn’t.

Key Metrics to Keep an Eye On

Once you have your tracking system in place, you don’t need to obsess over every single number. Drowning in data is just as bad as having none. Instead, focus on a few vital signs that directly impact your retirement goals.

Here are the key performance indicators (KPIs) I watch:

- Net Worth Growth: Is your net worth climbing month after month? This is your ultimate report card.

- Savings Rate: What slice of your income are you actually putting away? Boosting this percentage is the most powerful lever you have for speeding up your timeline.

- Investment Performance: Are your investments hitting the return targets you set in your plan? You don’t need to check daily, but a quarterly review is essential.

- Debt-to-Asset Ratio: How much of your financial world is built on debt? Pushing this ratio down over time makes your financial foundation rock-solid.

Monitoring these numbers reveals a fascinating truth about national savings habits. As of Q3 2025, total U.S. retirement assets reached an incredible $48.1 trillion. Yet, the average 401(k) balance was a mere $134,128. That huge gap shows that while the system holds a ton of wealth, individual progress often lags. It’s a stark reminder of why you have to take charge of your own tracking.

Pro Tip: Put a recurring appointment on your calendar—monthly or quarterly—to review your financial dashboard. Treat it like a non-negotiable meeting with your future self. It’s this simple habit that builds momentum.

Ultimately, setting up a system to track net worth effectively is less about being a financial wizard and more about building a sustainable habit. It’s the consistent, disciplined act of checking in that makes sure the small, smart moves you make today add up to the financial freedom you’re aiming for tomorrow.

Common Retirement Planning Mistakes to Avoid

Figuring out your retirement number is a huge step, but it’s only half the battle. The other half is dodging the common traps that can completely sabotage even the most carefully crafted plans.

Many people get so focused on hitting that magic number that they miss the subtle but destructive mistakes lurking in the background. These aren’t just rookie errors; they’re psychological and financial tripwires that can catch anyone off guard. Knowing what they are is the first step to building a truly resilient plan.

Underestimating Inflation and Healthcare

One of the sneakiest threats to your retirement is ignoring the corrosive power of inflation. The money you save today simply won’t buy as much in 20 or 30 years. It’s a slow, quiet drain on your purchasing power. For instance, a $70,000 lifestyle in 2025 could easily demand over $125,000 per year by 2045, assuming a pretty standard inflation rate.

And then there’s healthcare—the other financial juggernaut. A healthy 65-year-old couple can expect to spend over $330,000 on medical costs throughout retirement. That staggering figure doesn’t even touch potential long-term care needs. Ignoring these twin threats is like building your dream house on a foundation of sand.

Here’s how it plays out in the real world: Take Mark, who retired with $1.2 million. He planned for a $48,000 annual withdrawal (4% rule), but he only baked in a tiny adjustment for inflation. A decade later, rising costs for everything from groceries to insurance premiums meant his withdrawal was buying him 20% less. He was forced to make painful cuts to his lifestyle, all because his plan failed to account for the slow, steady erosion of his money.

Investing Too Cautiously or Too Aggressively

Finding the right investment balance is a tightrope walk, and falling off on either side can be disastrous. As you get closer to retirement, the urge to protect your nest egg by shifting into “safer” investments like bonds is completely natural. But going too conservative can starve your portfolio of the growth it needs to outpace inflation. You can end up losing purchasing power even if your account balance stays flat.

The flip side is just as dangerous. Staying hyper-aggressive with an all-stock portfolio deep into your 70s exposes you to what’s known as sequence of returns risk. A nasty market downturn right after you stop working could permanently cripple your portfolio’s ability to recover, leaving you with far less than you planned for.

Ignoring Lifestyle Creep

This is the silent savings killer. As your income grows during your career, it’s incredibly easy to let your spending rise right along with it. A bigger house, a nicer car, more exotic vacations—it all feels earned, but it systematically eats into the money that should be funding your future self.

It’s a common psychological trap. A recent BlackRock study found that while retirement confidence has climbed 23% in the last decade, with 64% of workers feeling on track, employers see a different story. Only 38% of employers believe their people are actually prepared—a record low. That gap is often a direct result of lifestyle creep.

To steer clear of these pitfalls, you need to be proactive:

- Automate Your Savings: The easiest trick in the book. Set up automatic increases to your 401(k) or IRA contributions every time you get a raise. The money is invested before you even have a chance to miss it.

- Conduct Regular Reviews: At least once a year, stress-test your plan. Update your expense projections for inflation and healthcare costs. Rebalance your portfolio to make sure it still aligns with your timeline and risk tolerance.

- Focus on Your Savings Rate: Instead of getting fixated on a dollar amount, lock in on a savings rate. Aim to save a consistent 15% or more of your income. Make it a non-negotiable financial habit.

Answering Your Key Retirement Questions

Once you’ve put a real number on your retirement goal, a whole new set of questions tends to pop up. Suddenly, the plan feels tangible, and that’s when you need to start sweating the details. Getting these follow-up questions answered is what separates a decent plan from a great one.

Let’s dig into some of the most common things people ask once they have a target in sight. This will help you map out your next steps with a lot more confidence.

What If I Want to Retire Abroad?

Dreaming of retiring somewhere sunny and affordable? It’s a fantastic goal, but it means you’ll need to seriously re-evaluate your retirement number. Just converting your nest egg into the local currency won’t cut it.

You need to get granular with your research.

- Cost of Living: Don’t just look at the country; look at the specific city or region. The cost of housing, groceries, and transportation can be wildly different from one town to the next.

- Healthcare Systems: This is a big one. Find out if you’ll qualify for the local public healthcare system. If not, you’ll need to budget for private international health insurance, which can be a massive ongoing expense.

- Exchange Rate Risk: Currencies bounce around. Your $2 million nest egg might feel like a fortune when the dollar is strong, but a sudden shift can put a serious squeeze on your lifestyle. I always suggest building in a 10-15% buffer just to handle these swings.

Is the 4% Rule Still Relevant?

The 4% Rule is a brilliant starting point, but it’s not the final word on withdrawal strategies. For anyone planning a long retirement—say, 30 years or more—a more flexible approach can give you much-needed peace of mind. You want a system that can roll with the punches of the market.

A popular alternative is the guardrail method. It’s pretty straightforward: you set a target withdrawal rate (like 4%) but also establish upper and lower “guardrails,” maybe at 3% and 5%. If a bull market pushes your actual withdrawal rate below 3%, you give yourself a raise. If a market downturn pushes it above 5%, you tighten your belt for a bit to protect your portfolio. This dynamic strategy lets you enjoy the good times while safeguarding your capital when things get rocky.

How Do Taxes Impact My Retirement Number?

Taxes are your silent partner in retirement, and they’ll take a hefty cut if you’re not careful. The source of your retirement income is everything, because not all withdrawals are treated the same by the IRS.

Key Takeaway: The type of account your money comes from dictates how it’s taxed. A $1 million 401(k) and a $1 million Roth IRA are two completely different beasts after taxes are paid. Understanding this is absolutely critical for knowing how much you actually have to spend.

Here’s a quick breakdown of how it works:

- Traditional 401(k)s/IRAs: Every dollar you pull out is taxed as ordinary income. Simple as that.

- Roth 401(k)s/IRAs: All qualified withdrawals are 100% tax-free. This is a huge advantage.

- Brokerage Accounts: You only pay capital gains taxes on the investment growth, not on the original money you put in.

And don’t forget Social Security. A lot of people wrestle with when to start taking benefits. For instance, there are specific implications if you collect Social Security at age 62. By creating a smart withdrawal strategy that pulls from these different account types in a specific order, you can dramatically lower your lifetime tax bill and keep more of your hard-earned money.

Calculating your number is just the beginning. The next step is tracking your progress with a clear, consolidated view of your entire financial picture. PopaDex gives you the tools to see all your accounts in one place, monitor your net worth, and stay on course to your goal. See how it works at https://popadex.com.