Our Marketing Team at PopaDex

how much should i have saved for retirement: quick guide

Trying to answer the question, “How much should I have saved for retirement?” can feel like trying to hit a moving target in the dark. It’s a deeply personal number, but there’s a widely accepted rule of thumb that can give you a solid starting point: aim to have 10 times your final salary saved up by the time you’re ready to leave the workforce.

Think of that 10x figure as your destination. It provides a strong financial cushion for a comfortable, worry-free life after your career.

Your Retirement Savings Number at a Glance

Let’s cut through the noise and get straight to some simple benchmarks. While your perfect retirement number is unique to you, seeing how you stack up against common guidelines can be incredibly helpful.

Think of these numbers as a friendly check-in on a long road trip. They’re the major signposts along the highway, letting you know if you’re generally on track. They don’t account for your specific detours or travel style, but they tell you if you’re headed in the right direction.

This is just the beginning. A bit later, we’ll dive into how to fine-tune these numbers to match your specific goals, spending habits, and the lifestyle you actually want to live.

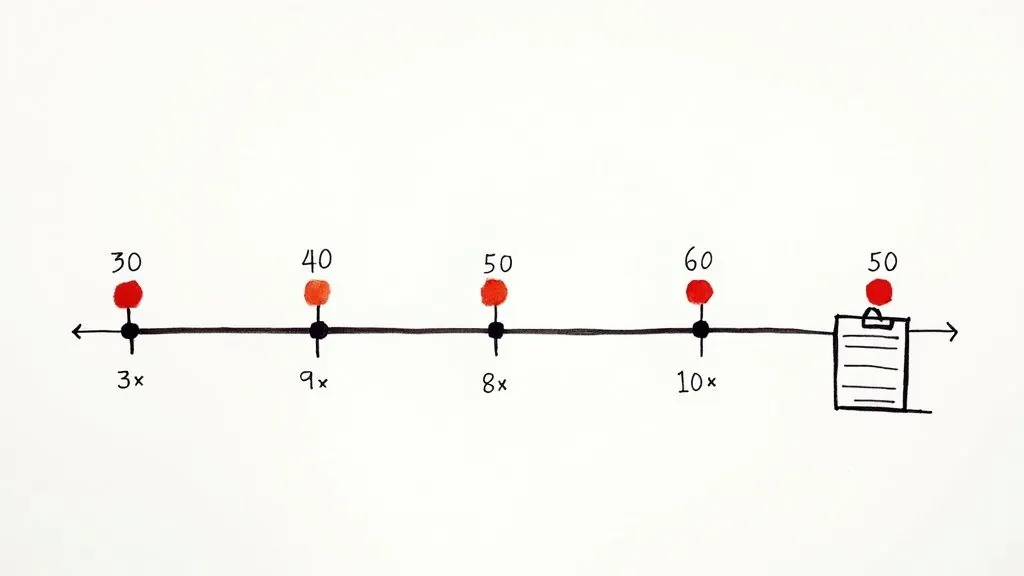

Retirement Savings Benchmarks by Age (Based on Annual Salary)

Here’s a simple table that breaks down common savings targets based on a multiple of your annual salary. It’s a great way to get a quick snapshot of where you stand right now. Remember, these are just guidelines, not hard-and-fast rules.

| Age | Savings Goal (Multiple of Salary) |

|---|---|

| 30 | 1x Your Annual Salary |

| 40 | 3x Your Annual Salary |

| 50 | 6x Your Annual Salary |

| 60 | 8x Your Annual Salary |

| 67 | 10x Your Annual Salary |

Don’t panic if your number doesn’t match up perfectly! The goal here isn’t to cause stress but to give you a clear reference point to start from.

Why Your Personal Savings Matter So Much: A Global Look

It’s also useful to see the bigger picture. How much you need to save personally is heavily influenced by the strength of your country’s retirement system.

The Mercer CFA Institute Global Pension Index 2025 offers a fascinating look at this. Countries like the Netherlands and Denmark get top marks for their robust, well-funded systems. The United States, on the other hand, scored a 61.1, which highlights a much greater need for individuals to build their own wealth through accounts like 401(k)s and IRAs.

This context really underscores why being proactive with your own savings is so critical, especially in the U.S.

Key Takeaway: Benchmarks are fantastic for a quick check-in, but they’re no substitute for a real plan. Your actual savings target will be shaped by your unique life—from your career path to your dreams for retirement.

The purpose of these numbers isn’t to make you feel behind. It’s to give you a tangible starting point so you can begin crafting a personalized strategy that truly works for you.

Understanding the Building Blocks of Your Retirement Number

Figuring out “how much do I need to retire?” isn’t about memorizing some magic formula. It’s really about getting a handle on three core ideas that work together to create a savings target that makes sense for you. Once you see how they connect, that big, scary number suddenly feels a lot more concrete and achievable.

Think of these as the foundation of your retirement plan. Each one supports the others, and getting them right ensures the whole structure is solid enough to see you through decades of life after work. Let’s break them down, one by one.

Your Income Replacement Rate

First up is the Income Replacement Rate. This is just a fancy term for the percentage of your current income you’ll need each year to live comfortably once you stop working. It’s the starting point for everything else.

A lot of people think their expenses will magically plummet in retirement, but that’s not always the case. Sure, you might ditch the daily commute and your work wardrobe, but other costs like healthcare, hobbies, and travel could easily go up. A good rule of thumb is to plan on replacing 70% to 85% of your pre-retirement income.

- Example: If you make $100,000 a year before retiring, an 80% replacement rate means you’d need an annual income of $80,000 in retirement.

Of course, this isn’t set in stone. If your vision for retirement involves downsizing and simple living, you might need less. If you’re dreaming of world travel and new adventures, you might need 90% or even more. The key is to be brutally honest about the lifestyle you actually want.

The Safe Withdrawal Rate

Once you know how much income you’ll need each year, the next building block helps you calculate the total size of the nest egg required to generate it. This is the Safe Withdrawal Rate (SWR), and it’s one of the most powerful concepts in financial planning.

Picture your retirement savings as an apple orchard. Your SWR is the number of apples you can pick each year without ever having to chop down the trees (your principal). It’s the rate you can pull money from your portfolio with a very high chance of it lasting for your entire retirement.

The most famous SWR is the 4% Rule. This guideline suggests you can safely withdraw 4% of your portfolio in your first year of retirement, then adjust that dollar amount for inflation each year after. The math shows this should last for at least 30 years.

Let’s say you need that $80,000 per year. You can use the 4% Rule to work backward and find your target number:

- $80,000 / 0.04 = $2,000,000

Just like that, a fuzzy question about annual income turns into a tangible savings goal. A more conservative rate, like 3.5%, would mean you need a bigger nest egg. A higher rate means a smaller one, but it definitely comes with more risk.

Your Time Horizon and Inflation

The final piece of the puzzle is your Time Horizon. This has two parts: how many years you have left to save, and—just as importantly—how many years your money needs to last in retirement. A longer retirement is like a longer road trip; it just requires more fuel in the tank.

Someone who retires at 60 and lives to 95 needs their money to last for 35 years. Someone who works until 70 and lives to 90 only needs their funds for 20 years. That difference has a massive impact on the total amount you’ll need.

But there’s a quiet thief you have to account for across that timeline: inflation. The cost of everything tends to creep up over time, meaning the $80,000 that sounds great today will buy a lot less 20 or 30 years from now.

Keep these points in mind:

- Long-Term Impact: Even a mild 3% average inflation rate will cut the buying power of your money in half in about 24 years.

- Plan Ahead: Your retirement math has to factor this in. The 4% Rule has inflation adjustments built into its methodology, but it’s critical to remember your future expenses will be higher in dollar terms.

- Growth vs. Inflation: Your investment strategy must aim for returns that consistently outrun inflation. If it doesn’t, your portfolio’s real value is actually shrinking, even if the balance looks like it’s going up.

By understanding these three building blocks—how much you’ll spend, how you’ll draw it down, and how long it needs to last—you stop guessing and start planning. You can finally build a personalized retirement number that actually reflects your life and your goals.

How to Calculate Your Personalized Retirement Target

Generic benchmarks are a decent starting point, but let’s be honest—they’re a bit like a one-size-fits-all t-shirt. They get the job done, but they don’t really fit. Now it’s time to ditch the averages and build a retirement savings target that’s designed just for you.

This isn’t about intimidating financial modeling. It’s about using some simple, powerful math to connect the lifestyle you want with a concrete number you can aim for. We’ll walk through it step-by-step, turning abstract ideas into tangible goals.

The process is pretty straightforward. You start by defining what you want your future to look like, which then helps figure out how much you can spend and how long your money needs to last.

As you can see, everything flows from your desired lifestyle. That’s the foundation for the rest of your plan.

Step 1: Determine Your Desired Annual Retirement Income

The first, most important question to answer is: “How much money do you actually need hitting your bank account each year in retirement?” Forget your current salary for a moment; this is all about your future expenses.

Think through your non-negotiables first—housing, food, and especially healthcare. Then, layer in the fun stuff like travel, hobbies, and dining out. A common rule of thumb is to aim for 80% of your pre-retirement income, but your personal number could easily be higher or lower depending on your plans.

Example Calculation: Annual Income Goal Let’s say you’re currently earning $75,000 a year. Applying the 80% guideline, your target retirement income would look like this: $75,000 x 0.80 = $60,000 per year This $60,000 is the magic number your nest egg needs to generate for you each year.

Step 2: Calculate Your Total Nest Egg with the Safe Withdrawal Rate

Okay, you’ve got your annual income target. Now, how big does your portfolio need to be to produce that income without running out of money? This is where the Safe Withdrawal Rate (SWR) comes in, most famously known as the 4% Rule.

The rule suggests you can withdraw 4% of your portfolio in your first year of retirement, then adjust that amount for inflation each year after. Historically, this has given retirees a very high chance of their money lasting at least 30 years.

To get your target number, you simply divide your annual income goal by your chosen SWR.

Example Calculation: Total Nest Egg Using our $60,000 annual income goal and a 4% SWR: $60,000 / 0.04 = $1,500,000 And there it is. Your personalized retirement savings target is $1.5 million.

This is a powerful moment. You just turned a vague “I need to save for retirement” thought into a specific, tangible goal. If you want to play around with different income levels or withdrawal rates, a good retirement nest egg calculator can do the math for you instantly.

Step 3: Understand the Impact of Small Changes

That final number you calculated is extremely sensitive to the assumptions you make. Your withdrawal rate and your guess at the long-term inflation rate are the two biggest levers. Tweaking either one, even slightly, can dramatically change how much you need to save.

For example, a more conservative planner might choose a 3.5% SWR to build in a bigger safety net. Likewise, if you believe inflation will run higher than its historical average of around 3%, your portfolio has to work that much harder just to maintain your purchasing power.

Let’s see how changing these assumptions affects our $60,000 annual income goal.

Impact of Withdrawal Rate and Inflation on a $60,000 Annual Income Goal

This table shows how small adjustments to your safe withdrawal rate and inflation assumption can significantly alter your total savings target.

| Safe Withdrawal Rate | Assumed Annual Inflation | Total Nest Egg Required |

|---|---|---|

| 4.0% | 3.0% | $1,500,000 |

| 3.5% | 3.0% | $1,714,286 |

| 4.0% | 4.0% | $1,500,000* |

| 3.5% | 4.0% | $1,714,286* |

*Note: The nest egg target is determined by the withdrawal rate, while inflation affects how quickly that nest egg’s purchasing power erodes over time. A higher inflation rate means you’ll need to be more careful with annual withdrawal adjustments.

Look at that difference. Dropping your withdrawal rate by just half a percent adds over $214,000 to your savings goal. This is exactly why personalization matters so much. It’s not just about crunching numbers; it’s about building a plan that truly aligns with your risk tolerance and economic outlook. That’s how you arrive at an answer to “how much should I have saved for retirement” that is truly your own.

Benchmarking Your Progress Against Real-World Data

Once you’ve done the hard work of calculating a retirement number that’s actually built for your life, it’s only human to wonder, “So, how am I actually doing compared to everyone else?” Looking at real-world data isn’t about feeling ahead or behind; it’s about gaining some much-needed perspective.

Seeing where you stand relative to national averages can be a powerful motivator. It gives your own plan context, shines a light on the challenges lots of people are facing, and can even reaffirm that you’re on the right track. Think of it like plotting your own road trip, then looking at a map of the entire country—it helps you understand the bigger picture of the journey ahead.

A Snapshot of Retirement Savings Today

When you ask, “how much should I have saved for retirement?”, it helps to see what others have managed to put away. Recent data shows the average 401(k) balance in 2025 is $134,128. Of course, that number shifts dramatically with age—savers in their 60s hold a much higher average of $239,900.

But those numbers only tell part of the story. Individual Retirement Accounts (IRAs) actually hold the biggest piece of the pie, totaling a massive $14.52 trillion in retirement assets nationwide.

The data also reveals some tough realities. A persistent gender gap means women have roughly 30% less saved for retirement than men. The median savings for women is just $31,291, compared to $45,106 for men, a difference often tied to things like career breaks and pay inequality.

These statistics aren’t meant to be discouraging. Instead, they highlight common hurdles and prove just how important it is for everyone to have a consistent, early plan, no matter your starting point.

Why Averages Don’t Define Your Success

It’s critical to remember that “average” is just a mathematical middle ground, not a measure of what’s right for you. Your personalized retirement target is built on your unique spending habits, lifestyle goals, and timeline. The average saver probably doesn’t share your specific dream of retiring to a beach town or funding a passion project.

A few things make direct comparisons tricky:

- Cost of Living: Someone saving for retirement in San Francisco has a completely different financial mountain to climb than someone in a small Midwest town.

- Access to Pensions: A small but lucky portion of the workforce still gets a traditional pension, which dramatically changes how much they need to save on their own.

- Career Paths: A doctor who starts earning a six-figure salary in their 30s will have a very different savings curve than a teacher who has been steadily contributing since they were 22.

Your Plan, Your Benchmark: The most important number to measure yourself against is your own. The personalized retirement goal you calculated is the only benchmark that truly matters for your financial security.

Use the national data for motivation, not anxiety. If you’re ahead of the curve, great! It’s confirmation your strategy is working. If you’re a bit behind, see it as a signal to revisit your plan, find ways to bump up your savings, and get back on track. For a more detailed breakdown, check out our guide on the average retirement savings by age 65.

Ultimately, these numbers provide context, not a verdict. Your success will be defined by the plan you build and the consistent steps you take to make it a reality.

Actionable Strategies to Bridge Your Retirement Gap

So, you’ve run the numbers and there’s a gap between where you are and where you need to be. First things first: don’t panic. This isn’t a sign of failure; it’s a call to action. This is the moment you shift from planning to doing.

You have two powerful levers at your disposal: how much you save and how you invest it. Think of your savings rate as the engine pushing you toward retirement and your investment strategy as the high-octane fuel. A bigger engine running on better fuel will get you to your destination much, much faster. The best part? You’re in the driver’s seat for both.

Small, consistent adjustments in these two areas can create massive momentum over the long haul, putting you firmly back on track.

Power Up Your Savings Rate

The most direct way to close a retirement gap is simply to save more money. Obvious, right? But the key is to make it systematic and sustainable, not something that relies on sheer willpower at the end of the month.

The goal is to flip the script from saving what’s “left over” to a “pay yourself first” mindset. As a benchmark, Fidelity suggests aiming to save between 13% and 21% of your pre-tax income throughout your career, starting in your 20s.

Here are a few practical ways to make that happen:

- Automate Everything: This is non-negotiable. Set up automatic transfers from your checking to your retirement accounts for the day you get paid. The money is gone before you even have a chance to miss it.

- Escalate Your Contributions: Every time you get a raise or a bonus, immediately bump up your savings rate by 1-2%. You won’t feel the pinch of money you never got used to spending in the first place.

- Find “Hidden” Cash in Your Budget: Take a hard look at your subscriptions, dining habits, and other flexible expenses. Redirecting even $100 a month toward retirement can compound into tens of thousands of dollars over time.

For an even deeper dive, check out our guide on how to catch up on retirement savings, which is packed with more detailed tactics.

Optimize Your Investment Strategy

Saving diligently is half the battle. The other half is ensuring your money is working as hard for you as you did for it. This is where asset allocation comes into play—it’s just the fancy term for the mix of different investments, like stocks and bonds, in your portfolio.

Your ideal mix comes down almost entirely to your time horizon. The further you are from retirement, the more risk you can generally afford to take in the hunt for higher growth.

A younger investor’s portfolio should look very different from that of someone nearing retirement. Time is your greatest asset, allowing you to ride out market volatility for the potential of greater long-term returns.

As you get closer to needing that money, your focus should gradually shift from all-out growth to protecting what you’ve built.

- Early Career (20s-30s): Your portfolio can be heavily weighted toward stocks (80-90%), which historically offer the best potential for long-term growth.

- Mid-Career (40s-50s): You might start shifting to a more balanced mix, maybe 60-70% stocks and 30-40% bonds, to lock in some of your gains and reduce volatility.

- Approaching Retirement (60s+): Now, the focus is on capital preservation. A portfolio of 40-50% stocks and 50-60% bonds is a common approach.

And remember, a well-balanced portfolio goes beyond stocks and bonds. For those looking to diversify, understanding how to calculate cash flow on rental property is a crucial first step for potential real estate investors. It’s all about finding the right mix of assets that fits your timeline and comfort with risk to get you across the finish line.

It’s Time to Own Your Retirement Journey

This whole process is about one thing: swapping financial anxiety for a clear, confident plan. You’re now equipped to move past generic advice and figure out exactly how much you need to have saved for the retirement you want.

We’ve walked through how to find your starting line with age and income benchmarks, grasp the core ideas that drive your final number, and then calculate a savings target that’s truly yours. More importantly, you have real strategies to start closing any gaps you might have uncovered.

Look, the “perfect” retirement plan doesn’t exist. But a well-informed, proactive one absolutely does. Your financial future isn’t built on one big, dramatic decision—it’s built on the small, consistent moves you make every single day.

The most important step is the one you take right now. Use what you’ve learned here to review your savings rate, double-check your investment mix, and start building a future that gives you both freedom and genuine peace of mind. Every dollar you set aside is a vote for the life you want to live down the road.

And as you map out this journey, remember that a solid plan also protects your assets for the long haul. It’s smart to explore resources on Estate Planning for Retirement: Securing Your Golden Years. All these pieces work together to build a truly secure financial foundation.

Common Questions About Your Retirement Number

You’ve got the concepts down and maybe even crunched a few numbers, but let’s be real—retirement planning is never a straight line. Life throws curveballs, and it’s totally normal to have some “what if” questions pop up.

Let’s tackle a few of the most common ones to give you the clarity you need to move forward with confidence.

What if I Started Saving for Retirement Late?

First off, don’t panic. Starting late is incredibly common, but it does mean you need a more focused, aggressive game plan. Your main lever is your savings rate. Forget the standard 15%—you’ll likely need to push that closer to 25% or more of your income.

Your mission is to max out every tax-advantaged account you can get your hands on, like your 401(k) or IRA. And never, ever leave an employer match on the table. It’s the closest thing to free money you’ll ever get. You might also have to get creative by working a few extra years or rethinking what your dream retirement lifestyle looks like. The most important thing? Start now.

How Do I Factor in Healthcare Costs?

Healthcare is the wild card of retirement expenses—it’s one of the biggest and most unpredictable costs you’ll face. We’re not just talking about prescriptions; a healthy 65-year-old couple could need hundreds of thousands of dollars just for medical care throughout their retirement, and that doesn’t even touch long-term care.

A smart move is to plan for this beast separately. If you’re eligible, a Health Savings Account (HSA) is your secret weapon. The HSA has a powerful triple tax advantage that’s hard to beat:

- Your contributions are tax-deductible.

- Your money grows completely tax-free.

- Withdrawals for qualified medical expenses are also tax-free.

Think of it as building a dedicated healthcare fund that won’t force you to raid your primary retirement nest egg when a big medical bill comes due.

Should My Goal Change if I Have a Pension?

Absolutely. Having a pension is a game-changer. It provides a guaranteed stream of income, which means your personal savings don’t have to do as much heavy lifting. This is fantastic news for your target number.

Here’s how to adjust your math. First, find out what your annual pension income will be. Then, subtract that figure from the total annual income you want in retirement. The remainder is the amount you need to generate from your own investments. For example, if you need $70,000 a year to live comfortably and your pension will provide $30,000, your portfolio only needs to cover the remaining $40,000. That dramatically lowers the total nest egg you need to build.

Is the 4% Safe Withdrawal Rule Still Reliable?

The 4% rule is a fantastic starting point, but it’s not gospel. Think of it more as a guideline than a hard-and-fast rule. It was born from historical market data and is based on a traditional 30-year retirement with a specific mix of stocks and bonds.

Today, with people living longer and market forecasts looking different than they did in the ’90s, many financial planners are leaning toward a more conservative rate. A rate of 3% or 3.5% might give your portfolio a better chance of lasting. The best approach is to see 4% as a benchmark, then adjust it based on your personal situation and how much risk you’re comfortable with.

Planning for retirement involves juggling a lot of moving parts. Instead of guessing, what if you could see your entire financial picture in one simple, clear dashboard? PopaDex helps you track your net worth, monitor your investments, and stay on course to hit your goals. Make confident decisions for your future. Take control by visiting https://popadex.com to get started for free.