Our Marketing Team at PopaDex

How to Find Your Net Worth and Master Your Financial Health

Figuring out your net worth is way simpler than it sounds. At its core, it’s just the total value of your assets minus your total liabilities. This single number is the most honest look you can get at your financial health, cutting through all the noise from income statements and monthly budgets.

Why Net Worth Is Your True Financial Snapshot

It’s incredibly easy to mistake a high salary for actual wealth, but they’re two completely different things. Income is what you earn; net worth is what you own. Think of it as your personal balance sheet—a clear, unfiltered look at exactly where you stand.

Knowing this number gives you a powerful baseline for pretty much every big financial decision you’ll ever make. Whether you’re mapping out retirement, thinking about a major purchase, or building an investment strategy, your net worth provides the context you need to move forward with confidence.

And this isn’t just some exercise for the super-rich. It’s a critical tool for anyone who’s serious about building a secure financial future. It helps you:

- Track your progress over time to see if your financial habits are actually working.

- Spot areas for improvement, like whether you need to tackle debt or beef up your investments.

- Set realistic financial goals that are grounded in your current reality.

- Gain a sense of control over your finances, which is a huge stress-reducer.

To get started, it’s helpful to clearly separate what counts as an asset from what’s considered a liability. Here’s a quick breakdown to guide you.

Quick Guide to Net Worth Components

| Component | What It Is | Common Examples |

|---|---|---|

| Assets | Anything you own that has monetary value. | Cash, bank accounts, stocks, retirement funds, real estate, vehicles, valuable collectibles. |

| Liabilities | Any debt or financial obligation you owe to others. | Mortgages, car loans, student loans, credit card balances, personal loans. |

Having this clear distinction makes the whole process of adding everything up much more straightforward.

The Bigger Picture of Personal Wealth

Tracking your net worth also helps connect your personal finances to what’s happening in the wider economy. For instance, the Allianz Global Wealth Report noted that by the end of a recent year, global net financial assets hit a mind-boggling EUR 210 trillion, with private households’ financial assets jumping 8.7% to EUR 269 trillion.

This kind of growth shows how tracking your own numbers can reveal trends in your portfolio, especially if you have international investments. With North America holding about half of all private financial assets, keeping an eye on regional influences is more important than ever. You can read the full executive summary from Allianz to get a better sense of these global shifts.

The real power of knowing your net worth isn’t about comparing yourself to others; it’s about establishing a benchmark to compete against your past self. Your goal is consistent, steady progress.

The good news is that modern tools have made this whole process incredibly simple. Instead of fighting with spreadsheets, platforms can automatically sync data from all your accounts, giving you a real-time, accurate picture without all the manual work. This turns net worth tracking from a chore into an empowering habit, helping you make smarter decisions and stay on track toward your long-term goals.

Identifying and Valuing Your Assets

Alright, let’s get down to business. The first move in calculating your net worth is to take a complete inventory of everything you own. This is the “assets” side of the equation, and it’s all about creating an honest, methodical financial snapshot of where you are right now.

To make this manageable, I always recommend breaking your assets down into a few key categories. This keeps things tidy and gives you a much clearer picture of where your wealth is actually sitting. The big three are usually cash, investments, and personal property.

Cash and Cash Equivalents

This is the low-hanging fruit—the easiest part to get a handle on. We’re talking about all the highly liquid money you can get your hands on quickly. The value here is crystal clear: it’s just the current balance.

Pull together the numbers from:

- Checking Accounts: Your everyday spending money.

- Savings Accounts: The cash you’ve stashed for goals or emergencies.

- Money Market Accounts: Basically a savings account that often pays a bit more interest.

- Certificates of Deposit (CDs): Savings certificates with fixed maturity dates.

- Physical Cash: Don’t forget the bills you have tucked away.

Just log into your banking apps or pull up your latest statements and write down the exact balances. This number is the bedrock of your asset list and a critical first step if you ever want to figure out your liquid net worth.

Valuing Your Investments

Next, let’s tackle your investments. Unlike your bank account, these can change in value every single day. For an accurate net worth calculation, what you need is their current market value—not what you paid for them. That’s a super important distinction.

For things like a 401(k), 403(b), or a pension plan, your account portal will show you the current vested balance. It’s the same story for your IRAs and brokerage accounts holding stocks, bonds, or mutual funds. Log in and grab the total value as of today.

My Personal Tip: When you’re dealing with volatile stuff like individual stocks or crypto, this number is going to dance around. Don’t sweat it. The goal isn’t to time the market peak; it’s to get an accurate, real-time snapshot for this calculation.

Assessing Real and Personal Property

This is where things can feel a bit more subjective, but we’re still aiming for accuracy. This bucket holds all the tangible, physical stuff you own. The key is to use realistic, current market values—what would someone actually pay you for these items today?

- Real Estate: If you have a recent professional appraisal for your home or investment properties, use that. If not, sites like Zillow or Redfin can give you a decent ballpark figure. Just be realistic, not overly optimistic.

- Vehicles: Cars, boats, and motorcycles almost always go down in value. Use a trusted source like Kelley Blue Book (KBB) or Edmunds to find the current private-party sale value based on its condition.

- Collectibles and Valuables: This covers jewelry, art, antiques, or other valuable collections. This part can be tricky. For anything high-value, a professional appraisal is your best bet. For other items, check out recent sale prices on sites like eBay to land on a conservative estimate.

If you’re an entrepreneur, your business itself is a major asset. Figuring out its value is a complex but absolutely essential step. For anyone in that boat, understanding how to value a business for sale is non-negotiable for an accurate net worth statement. It’s a lot more involved than just looking at profits.

When in doubt, always be conservative with your property estimates. It’s much smarter to slightly undervalue an asset than to inflate it and give yourself a false sense of financial security. This discipline keeps your calculations grounded in reality and sets you up for success as you move on to your liabilities.

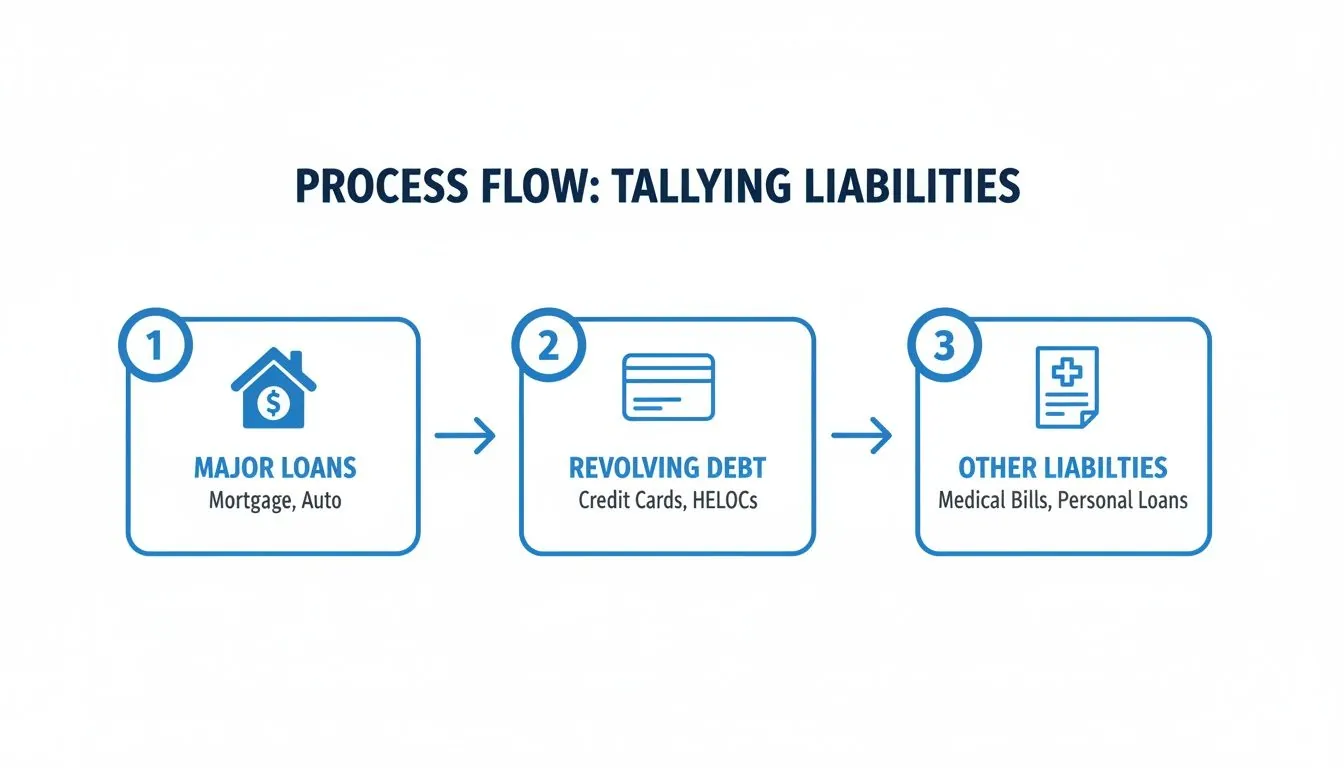

Tallying Up Your Liabilities Accurately

Now for the other side of the balance sheet: what you owe. This part is just as critical as listing your assets, and getting the numbers right is non-negotiable. An honest assessment here keeps you from calculating an inflated net worth and makes sure your financial picture is grounded in reality.

The goal isn’t to feel buried by your debts. It’s about gaining absolute clarity and control. Seeing the full picture is the first and most powerful step toward making a plan to shrink what you owe. The process is simple—list every single debt and its current payoff amount.

Major Loans: Mortgages and Auto

Let’s start with the big ones. These are usually your largest debts and have a massive impact on your net worth calculation. For most people, this means a mortgage and any vehicle loans.

To get the right value, you need the current principal balance, not the original loan amount. The easiest way to find this is by logging into your lender’s online portal or checking your most recent statement. This number is what you’d need to pay today to own the asset free and clear.

- Mortgage: List the remaining principal balance on your home loan.

- Auto Loans: Find the current payoff amount for any car, truck, or motorcycle loans.

- Other Major Loans: Don’t forget any loans for boats, RVs, or other significant assets.

Getting these numbers right is crucial because they’re often the largest liability you carry.

Remember, the value you’re looking for is the “payoff amount,” which might be slightly different from the principal balance because of accrued interest. Always use the most accurate figure you can get from your lender.

Revolving and Installment Debt

Next up are the debts that often have variable balances or fixed repayment schedules. This category covers everything from student loans to the balance sitting on your credit cards. These debts can change monthly, so it’s important to capture a current snapshot.

Compile a list of the following, making sure to grab the current statement balance for each:

- Student Loans: Both federal and private. You’ll need to log into each provider’s portal to get the total current balance.

- Credit Card Balances: Go through every single credit card—even the store cards you barely use—and write down the total amount owed.

- Personal Loans: This includes any unsecured loans from banks, credit unions, or online lenders.

- Lines of Credit: If you have a Home Equity Line of Credit (HELOC) or a personal line of credit, list the amount you’ve actually drawn from it.

Methodically tackling these debts is often a top priority for improving your financial health. As you think about your next steps, our guide on how to pay off debt effectively can be a huge help. Understanding different approaches to managing what you owe, including exploring efficient debt consolidation strategies, can give you a clear path forward.

Often Overlooked Liabilities

Finally, it’s time to dig up the debts that are easy to forget but can seriously skew your net worth if you leave them out. Think of this as a financial deep clean, catching all the miscellaneous obligations that might be hiding in the corners.

These liabilities can be less formal, but they’re just as real. Don’t skip this part; total accuracy depends on being thorough.

Here are a few common ones to look for:

- Medical Bills: Any outstanding payments you owe to hospitals, clinics, or doctors.

- Taxes Owed: This could be income tax you owe the government or outstanding property taxes.

- “Buy Now, Pay Later” Loans: Services like Klarna or Afterpay are short-term loans and absolutely must be included.

- Personal Debts: That money you owe to family or friends? It counts.

By diligently cataloging every single liability—from your mortgage down to the smallest medical bill—you’ve completed the second half of the net worth equation. With this comprehensive and honest list, you’re ready to put it all together.

Putting It All Together to Calculate Your Net Worth

You’ve done the hard work of listing what you own and what you owe. Now it’s time for the moment of truth, where we turn those lists into a single, powerful number. It all boils down to one simple but profound formula: Assets - Liabilities = Your Net Worth.

Let’s make this real. Imagine a professional in her 30s, Alex, who just finished taking stock of her finances.

A Practical Example of the Calculation

First, Alex totals up her assets, making sure to use current market values for everything.

- Cash: $15,000 sitting in her checking and savings accounts.

- Investments: $65,000 in a 401(k) and another $20,000 in a brokerage account.

- Property: Her condo is currently valued at $300,000, and her car’s Kelley Blue Book value is $10,000.

After adding it all up, Alex’s Total Assets come to $410,000.

Next up is the other side of the balance sheet: her liabilities. As you can see from the breakdown below, debts come in all shapes and sizes, from major loans to revolving credit.

For Alex, her liabilities are pretty straightforward.

- Mortgage: $220,000 remaining on her condo.

- Car Loan: $4,000 left to pay off.

- Student Loans: A remaining balance of $25,000.

That brings her Total Liabilities to $249,000.

With both sides tallied, the final calculation is easy: $410,000 (Assets) - $249,000 (Liabilities) = $161,000. So, Alex’s current net worth is $161,000.

To give you a clearer picture, here’s how a detailed net worth statement might look.

Sample Net Worth Calculation

This table breaks down the assets and liabilities for a fictional person, showing how each item contributes to the final number.

| Category | Item | Value | |

|---|---|---|---|

| Assets | Checking Account | $5,000 | |

| High-Yield Savings Account | $20,000 | ||

| 401(k) Retirement Plan | $75,000 | ||

| Brokerage Account (Stocks/ETFs) | $30,000 | ||

| Home (Market Value) | $450,000 | ||

| Car (Resale Value) | $18,000 | ||

| Total Assets | $598,000 | ||

| Liabilities | Mortgage Balance | $350,000 | |

| Student Loan Balance | $22,000 | ||

| Car Loan Balance | $8,000 | ||

| Credit Card Debt | $4,500 | ||

| Total Liabilities | $384,500 | ||

| Net Worth | (Assets - Liabilities) | $213,500 |

By laying everything out this clearly, you can pinpoint exactly where your wealth is concentrated and which debts are holding you back the most.

Interpreting Your Net Worth Number

Getting to your number is one thing; knowing what to do with it is another. A net worth figure is just a snapshot in time, and its real value lies in the story it tells about your financial journey.

First off, don’t be discouraged if your number is negative. This is extremely common for recent grads staring down student loans or new homeowners with a massive mortgage. A negative net worth isn’t failure—it’s your starting line.

The most important comparison you can make is with your past self. Is your net worth trending upward? If so, you’re on the right track, regardless of the absolute number.

It’s easy to fall into the trap of comparing your net worth to friends, influencers, or family members. Resist that urge. Everyone is on a different timeline with different opportunities and challenges. A rising net worth proves your financial habits are paying off. If it’s declining, that’s just a signal to take a closer look at your spending, saving, or investment strategy.

Why Tracking Your Progress Is Essential

In today’s economy, understanding your financial position isn’t just a good idea—it’s critical. Data from the US shows that the wealthiest 10% of households now control nearly 66% of the nation’s wealth, while the bottom 50% hold just 2.5%. This growing gap makes it more important than ever to know where you stand and have a plan to build your own financial security. You can discover more insights about wealth distribution on Statista.com.

This is where dedicated tracking tools like PopaDex make a world of difference. When you consolidate all your accounts, properties, and debts into a single dashboard, you get a clear, unbiased view of your progress. It shows you if your hard work is actually moving the needle.

Think of your net worth not as a grade on a report card, but as a compass. It shows you exactly where you are so you can chart a course to where you want to be. When you update it regularly, it stops being a static number and becomes your most trusted guide.

Ditching the Spreadsheet: Why Modern Tools Are a Game-Changer

While there’s a certain old-school charm to tracking your finances in a spreadsheet, let’s be honest—it’s a massive pain. The process is tedious and, worse, incredibly easy to mess up. A forgotten credit card payment or a miscalculation of your investment portfolio can paint a completely wrong picture of your financial health. This is exactly where modern financial tools have stepped in and changed the game for anyone serious about tracking their net worth.

Platforms built for this job take the manual labor out of the equation, giving you an accurate, real-time look at your financial life without the headache. Instead of logging into a dozen different websites, you connect everything to one central dashboard and let the technology do the heavy lifting.

The Magic of Automated Aggregation

The real power of these tools lies in their ability to plug directly into your financial institutions. Imagine linking all your accounts—checking, savings, retirement funds, credit cards, you name it—and seeing the numbers update on their own.

This completely removes the risk of human error and frees up a ton of time. What used to be a dreaded quarterly chore becomes a seamless, automatic part of your financial routine. This is a powerful shift, no matter where you are on your financial journey.

- For young professionals, it means less time buried in spreadsheets and more time focused on building wealth.

- For those closing in on retirement, it provides a dynamic, up-to-the-minute view to make sure you’re on track.

By connecting all your accounts, you transform net worth tracking from a static, periodic report into a live, interactive dashboard. This continuous insight is key to making timely and strategic financial decisions.

Taming Financial Complexity with Ease

Let’s face it, modern financial lives are messy. Many of us have assets and debts scattered across different banks, brokerage houses, and even countries. This is another area where dedicated tools truly shine, especially for expats and global citizens.

One of the most valuable features is multi-currency support. If you’ve got a savings account in euros, stocks in US dollars, and a property valued in British pounds, trying to calculate your total net worth is a recipe for a headache filled with currency conversions.

A platform like PopaDex handles this automatically. It pulls in all your international accounts and converts them into your main currency, giving you a single, unified snapshot of your global net worth. This feature alone can save hours of frustration and prevent some seriously expensive mistakes.

The screenshot below gives you a sense of what this looks like—a clean dashboard consolidating all your accounts into one clear view.

This kind of visualization gives you instant clarity on your assets, liabilities, and overall financial picture without having to dig through stacks of statements.

Moving from Tracking to Strategy

At the end of the day, calculating your net worth isn’t just about landing on a number. It’s about using that number to make smarter decisions about your future. When your financial data is organized and always current, you can shift your energy from tedious data entry to strategic planning.

You can instantly see how a good week in the market boosted your investments or how paying down a loan bumped up your net worth. This immediate feedback is incredibly motivating and helps reinforce good financial habits. If you’re looking for a solid way to stay on top of your finances, using a specialized net worth tracker provides the clarity and automation you need to take control.

By grabbing a simple tool, you’re not just buying convenience; you’re investing in a clearer understanding of your financial journey, empowering you to build wealth with confidence.

Got Questions About Net Worth? We’ve Got Answers.

Once you start calculating your net worth, a few questions always seem to surface. The formula itself is dead simple, but the real-world application can get a bit tricky. Let’s clear up some of the most common points of confusion.

How Often Should I Calculate My Net Worth?

For most people, a quarterly check-in is the sweet spot. Every three months is often enough to see real progress and spot any worrying trends, but not so often that you get lost in the day-to-day noise of market fluctuations. It lets you see if your savings strategy is working or if that new car loan is weighing you down more than you thought.

That said, if you’re gearing up for a major financial event—like buying a house, selling a business, or entering the final stretch before retirement—switching to a monthly review can give you a much tighter handle on your finances. While automated tools offer a live snapshot anytime, there’s real power in a scheduled, deliberate sit-down to analyze the trends.

What Are the Most Common Mistakes People Make?

Even with a simple Assets - Liabilities formula, it’s surprisingly easy to get a misleading number. The biggest tripwires almost always involve valuing what you own or forgetting what you owe.

Keep an eye out for these classic blunders:

- Using the Purchase Price: Valuing your home or car based on what you paid for it is a huge mistake. You need to use its current market value. For a depreciating asset like a car, this will be much lower than the sticker price.

- Forgetting the “Small” Debts: Your mortgage is hard to forget, but what about that store credit card, the lingering medical bill, or those “buy now, pay later” plans? They all count and can add up to a significant amount, so make sure they’re on your list.

- Inconsistent Valuations: If you use Zillow to value your home one quarter and a formal appraisal the next, you’ll create wild, artificial swings in your net worth. Pick a method for each asset and stick with it for consistency.

By far the biggest mistake is comparing your net worth to someone else’s. Your financial journey is yours alone. The only comparison that matters is you today versus you last year. Focus on your own progress.

Is a Negative Net Worth Always a Bad Thing?

Not at all. In fact, it’s completely normal, especially when you’re younger. Think about a recent medical school graduate with a mountain of student debt or a new homeowner whose mortgage is almost the entire value of their house. Starting with a negative net worth is incredibly common.

It’s not a failing grade; it’s just your starting line.

What really matters is the direction your net worth is moving. If you have a plan to tackle debt and build assets, and that number is becoming less negative each quarter, you’re on the right track. A negative number is just a temporary snapshot on a much longer journey.

How Do I Handle Assets in Different Currencies?

If you’re an expat, a remote worker with international clients, or a global investor, this one’s for you. Juggling assets in different currencies can feel like a headache, but the approach is straightforward: pick one primary currency and convert everything to it.

Typically, you’ll use the currency of the country where you live and spend the most. You’d take the current balance of your foreign accounts and debts and use today’s exchange rate to translate them into your home currency. This gives you a single, unified number that reflects your true global financial picture.

Doing this manually is a pain, which is precisely why a tool built for multi-currency tracking is a game-changer. It automates all the conversions, so you always have an accurate, up-to-the-minute view without wrestling with a calculator.

Ready to stop guessing and start tracking? PopaDex gives you the tools to see your entire financial world in one place, with automatic updates and multi-currency support. Take control of your financial future by signing up for a free account at https://popadex.com.