Our Marketing Team at PopaDex

10 Actionable Personal Finance Management Tips for 2026

Welcome to your comprehensive guide to financial empowerment. In a world of complex markets, multi-currency challenges, and information overload, achieving financial clarity can feel like an impossible goal. This article is designed to cut through the noise, providing a clear, actionable roadmap to help you take control. We’ve compiled 10 essential personal finance management tips crafted for the modern individual, whether you’re an expat juggling currencies, a freelancer with an irregular income, or a professional aiming to accelerate wealth creation.

This is not a list of vague suggestions. Instead, you’ll find a blueprint for building a robust financial system. We move beyond generic advice to deliver specific strategies you can implement immediately. You will learn how to track your net worth with precision, automate your savings and investments, and strategically eliminate high-interest debt. We will also cover how to diversify your portfolio, set meaningful financial goals, and optimize your tax situation for long-term growth.

Each point is structured for action, showing you how to translate theory into practice. For those using tools like PopaDex, we’ve included specific pointers on leveraging its features to streamline these processes. Prepare to transform your relationship with money by mastering these fundamental principles. By the end of this guide, you will have the knowledge and the tools needed to build a secure, organized, and prosperous financial future. Let’s begin.

1. Track Your Net Worth Regularly

One of the most powerful personal finance management tips is shifting your focus from just income and expenses to your overall net worth. Your net worth, calculated as your total assets minus your total liabilities, offers a comprehensive snapshot of your financial health at a single point in time. Tracking it consistently reveals the true impact of your financial decisions and keeps you motivated toward long-term goals like financial independence.

This practice is essential for anyone, but it becomes critical for those with complex finances, such as an expat in London managing investments in both GBP and USD, or a freelancer balancing fluctuating income against multiple business and personal accounts. Seeing all your accounts in one place clarifies your progress in a way that looking at individual balances cannot.

How to Implement Net Worth Tracking

Getting started is straightforward. The goal is to create a complete and accurate picture of your financial standing.

- Establish a Baseline: Your first calculation is your starting point. Don’t worry if the number is low or negative; its purpose is to serve as a benchmark for future growth.

- Consolidate All Accounts: Manually gathering data is tedious. Use an aggregation tool like PopaDex to automatically sync data from all your accounts, including savings, investments, real estate, and crypto wallets across different countries and currencies.

- Account for Everything: To ensure accuracy, list all assets (cash, stocks, property, vehicles) and all liabilities (mortgages, student loans, credit card debt). An incomplete picture can be misleading.

- Set a Regular Cadence: Track your net worth monthly or quarterly. Monthly tracking helps you stay engaged, while quarterly tracking smooths out short-term market volatility, revealing clearer long-term trends.

By monitoring this single, powerful metric, you can see how paying down debt and increasing investments directly contributes to building wealth. For a more in-depth guide, you can learn more about how to use a net worth tracker to achieve your financial goals.

2. Build an Emergency Fund (3-6 Months Expenses)

One of the most crucial personal finance management tips is establishing a robust emergency fund. This isn’t just another savings account; it’s a dedicated financial safety net containing three to six months of your essential living expenses. Its sole purpose is to cover unexpected financial shocks, like a job loss, urgent medical bill, or critical home repair, preventing you from derailing your long-term goals or accumulating high-interest debt when life happens.

This fund is a non-negotiable for everyone, but its size can vary. A freelancer in Spain with fluctuating income might aim for a €6,000 fund to cover six months of essential €1,000 expenses. In contrast, a salaried professional with a stable job might feel secure with three months’ worth. For those with dependents or highly variable income, aiming for the higher end of the range provides critical peace of mind.

How to Implement an Emergency Fund

Building this buffer is a systematic process that protects your financial future from unforeseen events.

- Calculate Your Target: Tally up only your essential monthly expenses: housing, utilities, food, insurance, and minimum debt payments. Multiply this number by three to six to determine your goal.

- Start Small and Automate: If the final number feels overwhelming, begin by saving for just one month of expenses. Set up an automatic monthly transfer from your primary account to a separate high-yield savings account. This “pay yourself first” approach builds the fund consistently without requiring constant effort.

- Keep it Liquid and Separate: The fund must be easily accessible but not too accessible. A high-yield savings account is ideal as it keeps the money liquid while earning a modest return. Do not invest your emergency fund in the stock market.

- Replenish Immediately: If you use the fund for a true emergency, make replenishing it your top financial priority. Pause other savings goals temporarily until your safety net is fully restored.

An emergency fund is the firewall between you and financial disaster. To create a step-by-step plan, you can learn more about how to build an emergency fund that fits your specific circumstances.

3. Automate Your Savings and Investments

One of the most effective personal finance management tips is to remove willpower from the equation and automate your financial progress. Automating your savings and investments involves setting up recurring, automatic transfers from your checking account to your savings, retirement, and investment accounts. This “pay yourself first” strategy ensures your financial goals are prioritized before you have a chance to spend the money, making consistency effortless.

This approach is a game-changer for busy professionals who lack time for manual transfers, or for anyone who finds it difficult to save consistently. For example, a self-employed consultant can set up quarterly automated transfers to their investment portfolio, while a German employee can schedule an automatic €500 transfer to a savings account on every payday. Automation turns good intentions into reliable habits.

How to Implement Financial Automation

Setting up automation is a powerful step toward building wealth with minimal ongoing effort. The key is to make it a default part of your cash flow.

- Schedule Transfers for Payday: The most effective time to automate is immediately after you receive income. Set up transfers to your savings and investment accounts to occur on the same day you get paid.

- Start Small and Scale Up: If you’re new to this, begin with a small, comfortable amount you won’t miss, like 5% of your income. You can gradually increase the percentage as you adjust to a lower take-home amount.

- Diversify Your Automation: Don’t just save to one account. Create automated transfers for different goals: your emergency fund, specific sinking funds (like a vacation or car down payment), and your retirement or brokerage accounts.

- Review and Adjust Periodically: Check your automated transfers every quarter or after a significant income change. This ensures the amounts still align with your financial goals and you can increase contributions where possible.

By making saving and investing the default action, you build wealth systematically without relying on discipline. This simple yet profound strategy ensures you are consistently working toward your financial future.

4. Pay Off High-Interest Debt Strategically

Among the most impactful personal finance management tips is to aggressively tackle high-interest debt. Consumer debt, especially from credit cards with rates often exceeding 15% APR, acts as a direct anchor on your wealth-building potential. Strategically eliminating it frees up significant cash flow and mental energy, allowing you to redirect funds toward investments and savings.

This strategy is crucial for anyone feeling overwhelmed by monthly payments, but it’s especially vital for individuals trying to gain financial traction. A young professional aggressively paying down €8,000 in credit card debt can save thousands in interest, while a self-employed individual can use peak income months to accelerate their payoff timeline. The key is moving from passively making minimum payments to actively executing a clear plan.

How to Implement a Strategic Debt Payoff Plan

Getting started involves organization and commitment. The goal is to choose a method that aligns with your financial situation and psychological needs to ensure you see it through.

- List and Prioritize Your Debts: First, create a comprehensive list of all your debts. Include the total balance, the interest rate (APR), and the minimum monthly payment for each. This clarity is the foundation of your strategy.

- Choose Your Method: Decide between two popular approaches. The debt avalanche method involves making minimum payments on all debts and directing any extra funds to the one with the highest interest rate. This is the most cost-effective approach. The debt snowball method, popularized by Dave Ramsey, involves paying off the smallest balance first for quick psychological wins, building momentum to tackle larger debts.

- Stop Accumulating New Debt: This step is non-negotiable. Pause the use of credit cards or other high-interest credit lines while you are actively paying down balances. You cannot empty a bucket that you are simultaneously filling.

- Automate and Accelerate: Use any windfalls, like a bonus or tax refund, to make a lump-sum payment on your target debt. Once a debt is paid off, roll its former minimum payment into the payment for the next debt on your list to accelerate the process.

By systematically eliminating these high-interest liabilities, you reclaim your income and empower yourself to build a stronger financial future. The freed-up cash can then be funneled directly into investments or a high-yield savings account, turning a former liability into a wealth-generating asset.

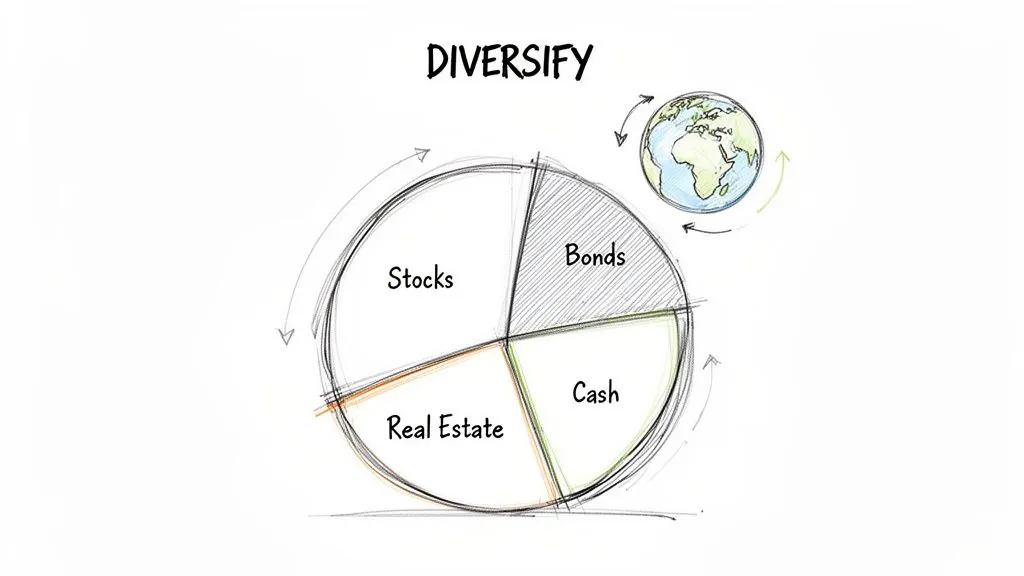

5. Diversify Your Investment Portfolio

A cornerstone of sound personal finance management tips is diversification, the practice of spreading your investments across various asset classes, geographies, and sectors. This strategy, famously summarized as “don’t put all your eggs in one basket,” is designed to reduce your portfolio’s overall risk. By not concentrating your capital in a single area, you protect your wealth from significant losses if one particular investment performs poorly, while still capturing growth potential from others.

This principle is essential for building sustainable wealth and navigating market volatility. For an expat managing investments in both EUR and USD, or a freelancer balancing real estate with stock market holdings, diversification across currencies and asset types is not just a good idea; it’s a critical component of a resilient financial plan. It smooths out returns and provides stability during unpredictable economic cycles.

How to Implement Portfolio Diversification

Building a diversified portfolio is a methodical process that aligns your investments with your risk tolerance and long-term goals.

- Determine Your Asset Allocation: A common starting point is an age-based rule, such as holding your age in bonds and the remainder in stocks. For instance, a 35-year-old might aim for a portfolio of 35% bonds and 65% stocks.

- Diversify Within Asset Classes: Don’t just own stocks; own a mix. Use low-cost index funds or ETFs to gain broad exposure to different sectors (tech, healthcare, energy) and geographies, including both developed and emerging markets.

- Incorporate Multi-Currency Assets: For expats and global citizens, diversification should extend to currencies. Holding assets in different currencies (e.g., a mix of USD-denominated ETFs and EUR-based real estate) can hedge against currency fluctuation risk.

- Rebalance Regularly: Your portfolio’s allocation will drift over time as different assets grow at different rates. Review it annually or when an allocation strays more than 5% from its target, and rebalance by selling overperforming assets and buying underperforming ones.

By systematically diversifying, you create a more robust portfolio capable of weathering market storms. To explore specific strategies in more detail, you can learn more about how to build a diversified investment portfolio.

6. Set Specific, Measurable Financial Goals

Effective personal finance management tips often boil down to one core principle: giving your money a purpose. Vague aspirations like “save more” or “get rich” lack the clarity needed for action. Setting specific, measurable, achievable, relevant, and time-bound (SMART) goals transforms abstract desires into a concrete action plan, providing both a roadmap and the motivation to follow it.

This practice is crucial for maintaining focus over the long term. A self-employed creative needs a clear target, like building a €50,000 emergency fund within two years, to navigate income fluctuations. Similarly, an expat might set a goal to accumulate enough capital in their local currency to purchase a property back home within seven years, guiding their saving and investment decisions across borders. Written goals create accountability and make it easier to say no to short-term temptations.

How to Implement Goal Setting

Turning broad wishes into tangible objectives is a systematic process. The key is to create a framework that guides your daily financial habits.

- Define and Write Down Your Goals: The act of writing down a goal, such as “accumulate a €100,000 net worth by age 35,” significantly increases your chances of achieving it. Be as specific as possible with numbers and deadlines.

- Break Down Large Goals: A goal like saving for a home down payment can feel overwhelming. Break it into smaller annual or monthly milestones, like saving €1,000 per month. This makes the objective more manageable and provides frequent opportunities to celebrate progress.

- Assign Goals to Accounts: Link your goals to specific accounts within a tool like PopaDex. You can create a dedicated savings account for your “Emergency Fund” goal or a specific investment portfolio for your “Retirement” goal, making it easy to track progress visually.

- Review and Adjust Regularly: Life changes, and so should your goals. Set a quarterly or annual review to assess your progress, celebrate achievements, and adjust your targets based on changes in your income, priorities, or market conditions.

By setting clear financial objectives, you shift from passively managing money to actively directing it toward the life you want to build. This strategic approach ensures every financial decision, from daily spending to long-term investing, serves a specific, meaningful purpose.

7. Understand and Optimize Your Tax Situation

A crucial aspect of personal finance management tips often overlooked is proactive tax planning. Tax optimization isn’t about evasion; it’s about legally minimizing your tax liability by understanding your obligations and using available deductions, credits, and tax-advantaged accounts. This strategy moves you from being a passive taxpayer to an active manager of your financial outcomes.

This practice is essential for anyone but becomes a game-changer for those with more complex financial lives. A freelancer, for example, can significantly reduce their taxable income by diligently tracking business expenses. Similarly, an expat living in a new country must navigate two different tax codes to avoid double taxation and make the most of foreign tax credits.

How to Implement Tax Optimization

Getting started involves shifting your mindset from tax preparation (a once-a-year event) to tax planning (an ongoing strategy). The goal is to make tax-aware decisions throughout the year.

- Keep Meticulous Records: Effective tax planning starts with good data. Keep detailed records of all income sources and potential deductions. As you work to optimize your tax situation, it’s important to understand what receipts to keep for taxes to ensure you claim all eligible deductions.

- Maximize Tax-Advantaged Accounts: One of the most powerful tools for building wealth is utilizing accounts like a 401(k), IRA, or Health Savings Account (HSA). Contributions are often tax-deductible, and the investments grow tax-deferred or tax-free.

- Implement Strategic Harvesting: If you have a taxable investment portfolio, consider tax-loss harvesting. This involves selling investments at a loss to offset capital gains taxes from winning investments, effectively lowering your tax bill.

- Seek Professional Guidance: Tax codes are complex, especially for self-employed individuals or those with international ties. Consulting a qualified tax professional can help you develop a personalized strategy and avoid costly mistakes.

By actively managing your tax situation, you ensure that more of your hard-earned money stays in your pocket, ready to be invested or used to achieve your other financial goals.

8. Practice Mindful Spending and Avoid Lifestyle Inflation

One of the most effective personal finance management tips is to focus on your spending habits, specifically by practicing mindful spending and actively avoiding lifestyle inflation. Mindful spending is the art of making conscious, intentional purchasing decisions that align with your values and long-term goals, rather than succumbing to impulse or emotional buying. It’s the antidote to lifestyle inflation, the common tendency to increase spending as your income rises, which is one of the biggest obstacles to building significant wealth.

This principle is crucial for anyone looking to accelerate their financial progress. For instance, a software developer who receives a 15% raise can choose to immediately invest the entire increase rather than upgrading their apartment or car. Similarly, a remote worker moving to a lower cost-of-living area can maintain their previous spending level, creating a substantial savings surplus. By keeping expenses consistent despite income growth, you can dramatically increase your savings rate and compound your wealth faster.

How to Implement Mindful Spending

Adopting a mindful approach to spending requires building new habits and increasing your financial awareness. The goal is to ensure your money is working for your future self, not just your present desires.

- Implement a “Cooling-Off” Period: For any non-essential purchase over a certain amount, enforce a 30-day waiting period. This simple rule helps differentiate a fleeting want from a genuine need, preventing impulse buys.

- Automate Your Savings First: The most effective way to combat lifestyle inflation is to allocate new income before you can spend it. When you get a raise or a bonus, immediately set up an automatic transfer to your investment or savings accounts.

- Distinguish Needs from Wants: Regularly review your spending categories in a tool like PopaDex. Explicitly label each expense as a “need” or a “want.” This awareness is the first step toward consciously cutting back on spending that doesn’t align with your goals.

- Track Your Progress: Instead of finding satisfaction in new purchases, find it in watching your net worth grow. Seeing that number climb provides a powerful, long-lasting motivation that consumption rarely matches. This shift in mindset is a cornerstone of sustainable wealth building.

9. Plan for Retirement and Long-Term Financial Security

Effective personal finance management is incomplete without a clear strategy for long-term financial security. Planning for retirement involves more than just saving money; it’s about building a portfolio that can sustain your desired lifestyle long after you stop earning a regular income. This requires understanding your future needs, setting clear savings goals, and consistently executing a strategy over several decades.

This forward-thinking approach is crucial for everyone, but it takes on added complexity for those with non-traditional financial lives. An expat in Singapore must navigate both local and home-country pension systems, while a freelancer needs to be proactive about creating their own retirement safety net through accounts like a SEP-IRA or Solo 401(k), replacing the employer-sponsored plans they lack.

How to Implement Retirement Planning

Starting your retirement plan involves defining your goals and creating a structured path to reach them. The earlier you begin, the more powerful the effect of compound growth.

- Calculate Your Retirement Number: Use the “4% rule” as a guideline to estimate the portfolio size you’ll need. Multiply your desired annual retirement spending by 25. For example, if you plan to live on €80,000 per year, your target is a €2 million portfolio.

- Maximize Tax-Advantaged Accounts: Prioritize contributions to retirement accounts that offer tax benefits, such as a 401(k), IRA, or their international equivalents. Always contribute enough to get the full employer match in a 401(k) if one is offered, as this is essentially free money.

- Automate Your Contributions: Set up automatic transfers from your checking account to your retirement and investment accounts each payday. This “pay yourself first” strategy ensures consistency and removes the temptation to spend the money elsewhere.

- Reassess and Adjust Regularly: Your life and financial situation will change. Review your retirement plan every few years, or after significant life events like a marriage, a new job, or a change in residency. This ensures your strategy remains aligned with your long-term goals.

By turning retirement into a concrete, calculated goal rather than an abstract concept, you can make informed decisions today that secure your financial freedom tomorrow. For expats, it’s particularly important to research the pension implications and tax treaties between your country of residence and your home country to build an efficient multi-jurisdictional plan.

10. Monitor Credit Score and Manage Debt Responsibly

Responsible debt management and a strong credit score are cornerstones of a healthy financial life. Your credit score, a numerical representation of your creditworthiness (typically 300-850 in the US), directly influences your ability to access loans, the interest rates you’ll pay, and even insurance premiums. Effectively managing debt isn’t just about avoiding late fees; it’s a strategic tool for building wealth and unlocking financial opportunities.

This practice is crucial for anyone looking to make a major purchase, such as a home or car, but it’s especially vital for individuals navigating complex financial landscapes. For instance, an expat moving to the UK must understand how to build a credit history from scratch, which differs significantly from the system they left behind. Similarly, a freelancer needs a strong credit profile to qualify for a mortgage or business loan based on their fluctuating income.

How to Implement Responsible Credit Management

Building and maintaining a good credit score is a long-term habit built on a few key principles. The goal is to demonstrate to lenders that you are a reliable borrower.

- Check Your Reports Regularly: In the US, you can get free annual credit reports from all three major bureaus (Equifax, Experian, and TransUnion) via AnnualCreditReport.com. Review them carefully for any errors, such as incorrect account information or fraudulent activity, and dispute them immediately.

- Prioritize On-Time Payments: Your payment history is the single most important factor in your credit score. Set up automatic payments for all your recurring bills to ensure you never miss a due date.

- Keep Credit Utilization Low: Aim to use less than 30% of your available credit on each card, and ideally less than 10%. For example, if you have a £10,000 credit limit, try to keep your balance below £3,000.

- Maintain a Mix of Credit: Lenders like to see that you can responsibly handle different types of debt, such as credit cards (revolving credit) and installment loans (like a car loan or mortgage).

- Preserve Account History: Avoid closing old credit card accounts, even if you don’t use them often. The length of your credit history positively impacts your score. Making a small, recurring purchase on an old card can keep it active.

10-Point Personal Finance Tips Comparison

| Item | 🔄 Implementation Complexity | ⚡ Resource Requirements | 📊 Expected Outcomes | 💡 Ideal Use Cases | ⭐ Key Advantages |

|---|---|---|---|---|---|

| Track Your Net Worth Regularly | 🔄 Moderate — ongoing data aggregation; easier with automation | ⚡ Aggregation tools, account access, periodic time investment | 📊 Holistic financial clarity; trend detection and better decisions | 💡 Expats, multi-account holders, complex portfolios | ⭐ High accuracy and insight; motivates progress |

| Build an Emergency Fund (3–6 Months) | 🔄 Low — simple calculation and separate savings setup | ⚡ Disciplined cash contributions; high‑yield savings account recommended | 📊 Greater resilience; reduced need for high‑cost borrowing | 💡 Self‑employed, gig workers, anyone facing income risk | ⭐ Strong downside protection; reduces financial stress |

| Automate Your Savings and Investments | 🔄 Low–Medium — one‑time setup, low maintenance | ⚡ Bank/broker automation features, payroll access, small setup time | 📊 Consistent contributions; improved savings rate and DCA benefits | 💡 Busy professionals, those prone to overspending | ⭐ Ensures discipline and reduces decision fatigue |

| Pay Off High‑Interest Debt Strategically | 🔄 Medium — requires prioritization and cash‑flow changes | ⚡ Extra payments, possible consolidation fees, budgeting effort | 📊 Lower interest costs; faster net‑worth improvement | 💡 Credit card holders, high APR borrowers, multi‑debt situations | ⭐ Frees cash flow and improves long‑term wealth trajectory |

| Diversify Your Investment Portfolio | 🔄 Medium — allocation choices and periodic rebalancing | ⚡ Access to funds/ETFs, possible higher fees, monitoring time | 📊 Reduced volatility; more stable long‑term returns | 💡 Long‑term investors, expats with international exposure | ⭐ Risk reduction and broader growth exposure |

| Set Specific, Measurable Financial Goals | 🔄 Low — reflection and periodic review required | ⚡ Time to define goals; tracking tools for measurement | 📊 Clearer priorities and measurable progress toward objectives | 💡 Everyone seeking direction; early‑career and expats | ⭐ Increases focus, motivation, and resource allocation |

| Understand and Optimize Your Tax Situation | 🔄 High — complex rules and cross‑jurisdiction issues | ⚡ Professional advice often needed; detailed record‑keeping | 📊 Lower tax liability and improved after‑tax returns | 💡 Self‑employed, high‑earners, multi‑country taxpayers | ⭐ Significant tax savings and compliance risk reduction |

| Practice Mindful Spending & Avoid Lifestyle Inflation | 🔄 Low–Medium — habit change and tracking required | ⚡ Time for tracking, budgeting tools, behavioral discipline | 📊 Higher savings rate; accelerated wealth accumulation | 💡 Rising earners and those prone to spending more with income | ⭐ Boosts long‑term savings without increasing income |

| Plan for Retirement & Long‑Term Security | 🔄 High — long‑horizon planning and assumptions | ⚡ Retirement accounts, consistent contributions, possible advisors | 📊 Retirement readiness and sustainable long‑term income | 💡 All adults, especially long‑term planners and expats | ⭐ Ensures future income stability and peace of mind |

| Monitor Credit Score & Manage Debt Responsibly | 🔄 Medium — continuous monitoring and corrective actions | ⚡ Credit monitoring tools, timely payments, possible enrollment fees | 📊 Lower borrowing costs; improved access to credit products | 💡 Prospective borrowers, homeowners, expats building local credit | ⭐ Saves on interest and improves financial opportunities |

Your Next Step Towards Financial Freedom

You have now explored ten foundational personal finance management tips designed to transform your relationship with money and build a secure, prosperous future. Navigating the worlds of budgeting, investing, and debt management can feel overwhelming, but the journey toward financial freedom isn’t about mastering everything overnight. It’s about taking consistent, deliberate steps, one at a time.

We’ve moved from the high-level perspective of tracking your net worth to the granular details of mindful spending and tax optimization. Each tip is a powerful lever you can pull to effect real change. Remember, these are not just abstract financial theories; they are practical, actionable strategies that, when combined, create a powerful system for wealth creation and financial well-being.

From Knowledge to Action: Your Personal Roadmap

The true value of this guide lies not in reading it, but in implementing it. Information without action is simply entertainment. To avoid the common pitfall of analysis paralysis, where you feel overwhelmed by the sheer number of options, focus on a single, impactful starting point. Your first step is the most critical one because it builds momentum.

Consider your current financial situation and choose the one area that feels most urgent or most achievable for you right now:

- If you feel lost or uncertain: Start with Tip #1: Track Your Net Worth Regularly. Gaining this clarity is the most powerful first step. It provides the map you need before you can plan your journey.

- If you live paycheck to paycheck: Focus on Tip #2: Build an Emergency Fund. This financial safety net is non-negotiable and provides the peace of mind needed to tackle other goals.

- If you’re burdened by credit cards or loans: Your priority is Tip #4: Pay Off High-Interest Debt Strategically. Use the avalanche or snowball method to begin chipping away at balances that are actively costing you money.

- If you have stable savings but aren’t growing your wealth: It’s time to embrace Tip #3: Automate Your Savings and Investments and Tip #5: Diversify Your Investment Portfolio. Put your money to work for you systematically.

Key Takeaway: Progress over perfection. The goal is not to execute all ten strategies flawlessly from day one. The goal is to start. Choose one tip, implement it this week, and build from that small but significant victory.

The Compounding Power of Good Habits

Mastering these personal finance management tips is about more than just numbers on a spreadsheet; it’s about building a life of intention and choice. When you automate your savings, you are buying future freedom. When you pay down debt, you are breaking chains that limit your opportunities. When you plan for retirement, you are giving your future self the gift of security and dignity.

Each positive financial decision you make, no matter how small, compounds over time. Saving an extra $50 a month, negotiating a bill, or choosing to cook at home instead of dining out are the small hinges that swing big doors. These habits create a positive feedback loop: as you see your net worth grow and your debt shrink, you become more motivated to continue, reinforcing the very behaviors that led to your success. This is the engine of wealth creation.

This comprehensive approach, covering everything from managing multi-currency assets for expats to handling irregular income for freelancers, ensures that no matter your financial complexity, there is a clear path forward. The principles remain the same: understand where you are, define where you want to go, and use the right tools and strategies to bridge that gap. Your financial future is not a matter of chance; it is a matter of choice. The choices you make today will define the life you live tomorrow.

Ready to stop juggling spreadsheets and connect all the pieces of your financial life in one place? PopaDex is the all-in-one wealth dashboard designed to help you implement these exact personal finance management tips, from net worth tracking across 30+ countries to monitoring your investments and liabilities. Turn these powerful insights into action by starting your free trial at PopaDex today.