Our Marketing Team at PopaDex

Start Here: roth ira vs traditional ira - A Quick Guide

The whole Roth IRA vs. Traditional IRA debate really comes down to one simple question: Do you want to pay taxes now or later?

Understanding the Core IRA Differences

Picking the right Individual Retirement Account (IRA) is a huge deal for your financial future. It directly impacts how much spending money you’ll actually have when you retire. While both Roth and Traditional IRAs are fantastic for building wealth, they’re built on opposite tax philosophies, creating a clear trade-off you need to understand.

Here’s the main distinction in plain English:

- A Traditional IRA can give you an upfront tax deduction on your contributions, which lowers your taxable income today. The catch? Your withdrawals in retirement are taxed as regular income.

- A Roth IRA gives you zero immediate tax breaks. You put in after-tax money, but in exchange, all your qualified withdrawals in retirement are 100% tax-free.

This fundamental difference sends ripples through your entire financial strategy, affecting everything from your current tax return to how you pass on your wealth.

A Quick Comparison

To see how this plays out in the real world, let’s put the key features side-by-side. Think of this table as your high-level cheat sheet before we dive into the finer details.

Core Feature Comparison Roth IRA vs Traditional IRA

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Contribution Taxes | Made with after-tax dollars (no deduction) | Often made with pre-tax dollars (potential deduction) |

| Withdrawal Taxes | Qualified withdrawals are completely tax-free | Withdrawals are taxed as ordinary income |

| Income Limits | Yes, high earners cannot contribute directly | No, anyone with earned income can contribute |

| Required Minimums | No RMDs for the original account owner | Yes, RMDs typically start at age 73 |

| Early Withdrawals | Contributions (not earnings) can be withdrawn anytime, tax and penalty-free | Generally subject to taxes and a 10% penalty before age 59½ |

As you can see, the “right” choice isn’t universal—it completely depends on your personal financial situation, your income, and what you expect your tax situation to look like down the road.

The Historical Context of IRA Popularity

The sheer amount of money in these accounts also tells a story. The Traditional IRA has been around a lot longer than the Roth, and it shows. By the end of 2015, Traditional IRAs held a staggering $6.4 trillion, completely dwarfing the $625 billion sitting in Roth IRAs.

This massive gap exists mostly because of its head start and its role as the go-to account for rolling over old 401(k)s. If you want to dig into the history and growth of these retirement accounts, Ascensus.com has some great insights.

No matter which IRA you go with, seeing how it fits into your overall financial picture is key. A net worth tool like PopaDex is perfect for this, letting you monitor these tax-advantaged accounts right alongside your other assets. This kind of big-picture view is exactly what you need to make smart retirement decisions.

Tax & Contribution Rules: The Core of the Roth vs. Traditional IRA Debate

The entire Roth vs. Traditional IRA decision boils down to one thing: taxes. When do you want to pay them? The classic “pay now or pay later” summary is a decent starting point, but the devil is in the details. The real choice depends on specific rules about your income, whether you can even deduct contributions, and annual limits. Getting these rules straight is the first and most important step.

A Traditional IRA’s big draw is the immediate tax break. When you contribute, you might be able to deduct that amount from your income for the year, which means a lower tax bill right now. This can be a huge win if you’re in a high tax bracket during your peak earning years.

But here’s the catch: not everyone gets that deduction. Your ability to deduct contributions hinges on two things: your modified adjusted gross income (MAGI) and whether you have a retirement plan like a 401(k) at work. If your income is too high and you’re covered by a workplace plan, that deduction shrinks or disappears completely.

Roth IRA: Tax-Free Growth and Income Limits

The Roth IRA flips the script. You get zero upfront tax deduction because you contribute with after-tax dollars. The tradeoff is massive, though: your investments grow completely tax-free, and every qualified withdrawal you make in retirement is 100% tax-free.

That tax-free withdrawal feature is the Roth’s superpower, especially if you think you’ll be in the same or a higher tax bracket when you retire. It gives you incredible certainty about your retirement income—no need to guess what future tax rates will do to your savings.

The main obstacle with a Roth is the income limit. If your MAGI is above the IRS threshold, your ability to contribute directly gets reduced or even eliminated. These income phase-out ranges are adjusted for inflation each year and are a critical fork in the road for high earners.

It all comes down to a bet. A Traditional IRA offers a potential tax break today, betting your tax rate will be lower in retirement. A Roth IRA gives up that break for the guarantee of tax-free income later, betting that future tax rates might be higher or that tax-free money is simply more valuable to your plan.

Shared Contribution Limits

For all their differences in tax treatment, both Roth and Traditional IRAs share the same annual contribution limits. For 2024, you can contribute a maximum of $7,000 across all of your IRAs. This is a combined limit, not a per-account limit.

This setup allows you to hedge your bets. For instance, you could put $4,000 into a Roth IRA and $3,000 into a Traditional IRA in the same year, as long as the total stays at or below the annual maximum.

Catch-Up Contributions for Savers Over 50

To help people closer to retirement give their savings a final push, the IRS allows for “catch-up” contributions. If you are age 50 or older, you can contribute an extra amount on top of the regular limit.

- Standard Annual Limit: $7,000 for 2024

- Catch-Up Contribution: An additional $1,000 for those age 50+

- Total Possible Contribution: $8,000 for savers 50 and over in 2024

This rule applies equally to both Roth and Traditional IRAs. It’s a valuable way to accelerate your savings in the final stretch before you stop working. Understanding these foundational rules is the bedrock for figuring out which account makes sense for you.

Comparing Withdrawal Rules and Account Flexibility

How and when you can pull money out of your retirement account is a massive factor in the Roth vs. Traditional IRA debate. They’re both built for the long haul, but their withdrawal rules create a night-and-day difference in flexibility, especially before you hit retirement age.

Getting these details right is critical. It determines how easily you can access your cash in an emergency and how you can plan your estate for the long term.

The Big Hurdle: The 59½ Age Rule

For the most part, both accounts play by the same core rule: the 59½ age rule. Try to take money out before you reach this magic age, and you’ll likely get hit with a 10% early withdrawal penalty on top of any income taxes you owe. This is the IRS’s way of making sure your retirement money is actually used for, well, retirement.

But life happens. The IRS knows this, so they’ve carved out a few key exceptions to that painful 10% penalty.

Getting Around Early Withdrawal Penalties

You can sidestep the 10% penalty for both Roth and Traditional IRAs in a few specific situations, including:

- Disability: If you become totally and permanently disabled.

- First-Time Home Purchase: You can withdraw up to $10,000 penalty-free to help buy your first home.

- Higher Education Expenses: Funds can be used for qualified college costs for yourself, a spouse, or your kids/grandkids.

- Medical Expenses: You can use the money to cover unreimbursed medical bills that are more than a certain percentage of your adjusted gross income.

While these exceptions apply to both account types, the tax treatment of the withdrawal is where things get interesting—and where the Roth IRA really starts to shine.

The Roth IRA’s Flexibility Superpower

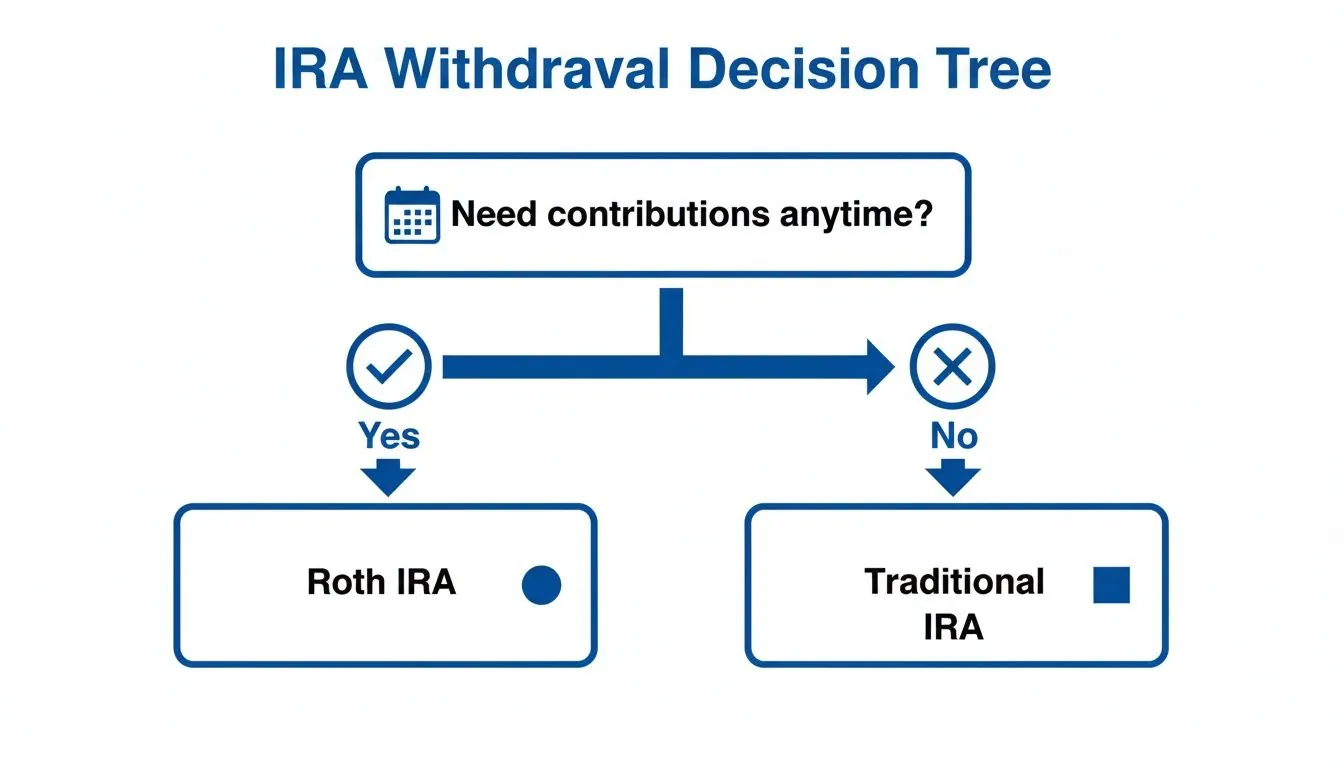

This is where the Roth IRA flexes its muscles. Because you’ve already paid taxes on your contributions, the IRS lets you withdraw those contributions—and only the contributions—whenever you want, for whatever reason you want. No taxes, no penalties.

This is a game-changer. It effectively turns your Roth IRA contributions into a supercharged emergency fund. If a crisis hits, you can tap your own money without getting penalized. A Traditional IRA simply can’t do that.

This unique feature makes the Roth IRA a powerful hybrid tool. It’s a retirement account first, but it also doubles as a highly accessible savings bucket. For younger investors who might need that cash before retirement, this flexibility makes the Roth an incredibly compelling choice.

Just be careful: this special treatment is only for your direct contributions. If you touch any of the investment earnings before age 59½, you’ll still face taxes and that 10% penalty unless you have a qualifying exception.

Required Minimum Distributions (RMDs)

The differences don’t stop at retirement age. They stretch deep into your golden years, especially when it comes to Required Minimum Distributions (RMDs). These are mandatory withdrawals you have to start taking once you hit a certain age, whether you need the money or not.

- Traditional IRA: You must start taking RMDs at age 73. These withdrawals are taxed as ordinary income, forcing you to finally pay the tax bill on all those years of tax-deferred growth.

- Roth IRA: Original account owners are completely exempt from RMDs. You are never, ever forced to take money out of your Roth IRA during your lifetime.

This RMD exemption is a massive win for estate planning. It lets your investments keep growing, completely tax-free, for your entire life. This maximizes what you can pass on to your heirs, who will then inherit the funds tax-free. It’s an incredibly efficient way to transfer wealth.

As you get closer to retirement, thinking through different retirement withdrawal strategies becomes crucial for making the most of these rules.

Real-World Scenarios for Choosing Your IRA

The theory behind Roth vs. Traditional IRAs only really clicks when you apply it to your own life. There’s no universal “best” choice here; the right answer is deeply personal. It all comes down to your financial reality today and your best guess about tomorrow.

Let’s move past the abstract rules and see how these accounts actually play out for different people.

Scenario 1: The Young Professional

Meet Alex, a 25-year-old just kicking off their career. Alex’s income is still on the lower side, landing them in the 12% federal tax bracket. But with a solid career path ahead, Alex is pretty confident they’ll be in a much higher bracket—maybe 24% or more—by the time retirement rolls around.

For Alex, the choice is a no-brainer: the Roth IRA is the better option.

Paying taxes now at a low 12% rate makes way more sense than taking a small deduction today, only to pay taxes on a much larger nest egg at a higher rate later. Over a 40-year career, the power of tax-free growth and tax-free withdrawals is going to be massive.

Scenario 2: The Peak Earner

Now, let’s look at Sarah, a 45-year-old in her peak earning years. Her income puts her squarely in the 32% tax bracket, and she’s actively looking for ways to lower her current tax bill. Sarah expects her income, and thus her tax bracket, to drop once she stops working.

In this situation, the Traditional IRA is likely the superior choice.

By contributing to a Traditional IRA, Sarah gets an immediate and significant tax deduction, saving money at her high 32% marginal rate. When she pulls the money out in retirement, she expects to be in a lower bracket (say, 22%), which means she pays less in taxes over the long haul.

The core decision hinges on your marginal tax rate now versus your expected effective tax rate in retirement. A high-income professional often saves more with an immediate deduction than they would by forgoing it for future tax-free withdrawals.

Scenario 3: The Pre-Retiree Expecting Lower Taxes

Finally, we have David, who is 60 years old. He’s planning to retire in five years and expects his income from pensions and Social Security to be modest, putting him in a lower tax bracket than he’s in now.

For David, the Traditional IRA makes the most sense.

Just like Sarah, David benefits by trimming his taxable income during his last few high-earning years. Since he’s anticipating a lower tax rate in retirement, deferring the tax hit until then is a financially sound move. He gets a valuable break now when he needs it most.

This chart visualizes a key difference in flexibility—the ability to access your contributions penalty-free, which is a major perk of the Roth IRA.

As you can see, if there’s any chance you might need to tap your contributions before retirement, the Roth IRA offers an unmatched level of liquidity.

A Worked Example: The Long-Term Impact

Let’s run the numbers to see how this plays out. Assume you contribute $7,000 annually for 30 years with an average 7% annual return.

- Roth IRA: You contribute a total of $210,000. It grows to approximately $661,000. When you retire, all $661,000 is yours to spend, completely tax-free.

- Traditional IRA: You contribute the same amount, and it also grows to $661,000. But, if you’re in a 22% effective federal tax bracket in retirement, you’ll owe about $145,420 in taxes. That leaves you with $515,580.

Financial models consistently show the Roth IRA coming out ahead for many people, especially younger investors. One study found that a 25-year-old contributing annually until age 65 would end up with nearly 20% more spendable income from a Roth IRA than a Traditional IRA, even after reinvesting the Traditional IRA’s tax deduction. You can learn more about the study’s findings on retirement income yourself.

Ultimately, your assumption about future tax rates is the single most important factor. If you’re confident your retirement tax rate will be much lower than it is today, the Traditional IRA holds its ground. Otherwise, the tax-free certainty of a Roth is tough to beat.

Advanced Strategies: Backdoor and Mega Backdoor Roth IRAs

What happens when you earn too much to contribute to a Roth IRA directly? Don’t worry, the game isn’t over. A couple of clever, and perfectly legal, strategies exist for high earners to get in on the tax-free growth a Roth account provides.

This is where you move beyond the standard Roth vs. Traditional IRA debate and into more advanced territory.

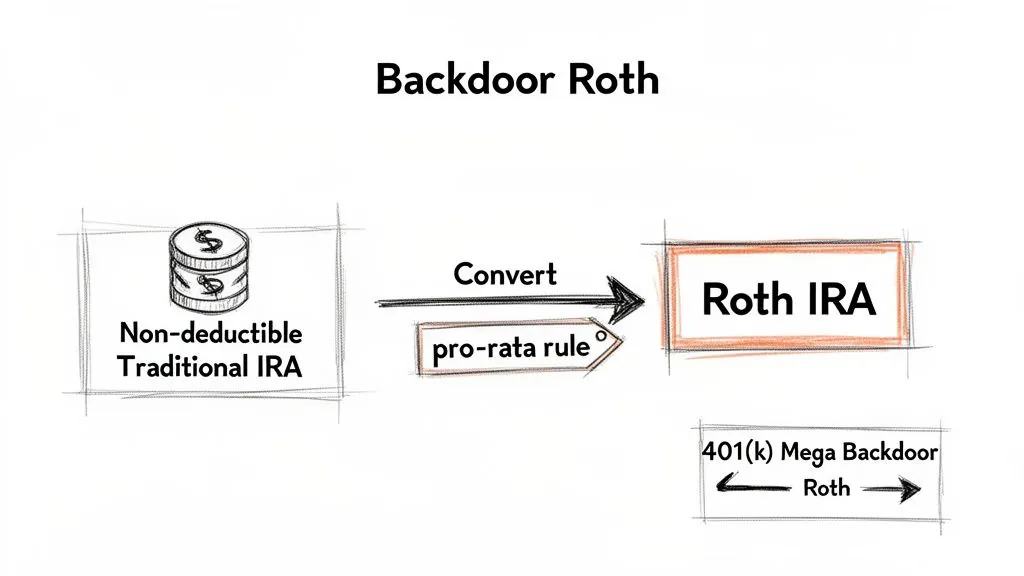

The most popular workaround is the Backdoor Roth IRA. It’s not a special type of account, but a simple two-step process. High-income investors can legally sidestep the Roth income limits by first contributing to a Traditional IRA and then immediately converting those funds into a Roth IRA.

Executing a Backdoor Roth IRA

The process itself is quite simple, but you need to be precise to avoid unexpected tax bills. Here’s the breakdown:

- Contribute to a Traditional IRA: First, you make a non-deductible contribution to a Traditional IRA, up to the annual limit. Since your income is high, you probably couldn’t deduct this contribution from your taxes anyway.

- Convert to a Roth IRA: As soon as the funds clear, you convert the entire balance of that Traditional IRA to a Roth IRA. If you do this quickly, there should be little to no investment gains to get taxed on during the conversion.

This slick maneuver gets your after-tax money into a Roth, where it can grow and eventually be withdrawn completely tax-free in retirement. But there’s one major catch you absolutely have to know about.

The single most important thing to understand with a Backdoor Roth is the pro-rata rule. If you already have pre-tax money sitting in any Traditional, SEP, or SIMPLE IRAs, your conversion will be partially taxable. The IRS views all your Traditional IRAs as one single account for tax purposes.

The Mega Backdoor Roth IRA

For those lucky enough to have a specific type of 401(k) plan at work, an even more powerful strategy exists: the Mega Backdoor Roth IRA. This move lets you funnel way more into a Roth account than the standard IRA limits allow—we’re talking tens of thousands more per year.

This strategy only works if your 401(k) plan allows two things: after-tax contributions (separate from your regular pre-tax or Roth 401(k) deferrals) and in-service withdrawals or conversions of that after-tax money into a Roth account (either a Roth IRA or a Roth 401(k)).

It’s a niche but incredibly valuable option if you have it. You can dive deeper into the mechanics in our guide on the after-tax contribution to a 401(k) to see if you qualify.

Both of these strategies demand careful planning and a solid grasp of the tax rules. For high-income earners who are locked out of direct Roth contributions, they are indispensable tools for building a more tax-efficient retirement portfolio.

Integrating Your IRA Into a Holistic Financial Plan

Picking between a Roth and a Traditional IRA is a fantastic start, but it’s just one move on a much larger chessboard. To truly build wealth, you have to see your IRA not as a standalone account but as a vital piece of your entire financial picture. This big-picture view is what separates good financial decisions from great ones.

Your IRA’s tax treatment and performance ripple across your entire portfolio. For example, the tax break from a Traditional IRA frees up cash today, while a Roth IRA’s tax-free withdrawals reshape how you plan for income in retirement. Without a single dashboard to connect these dots, you’re essentially flying blind.

Visualizing Your Entire Portfolio

This is where a net worth tracker like PopaDex becomes so valuable. Instead of juggling logins for a dozen different accounts, you can see your Roth or Traditional IRA balance right next to your 401(k), brokerage accounts, real estate, and even crypto. This unified view gives you instant clarity on your asset allocation and how you’re tracking toward your goals.

Here’s a quick look at how PopaDex brings all your assets together, giving you a clean, visual summary of your financial health.

A dashboard like this immediately shows how your tax-advantaged accounts are contributing to your overall net worth, keeping you focused and motivated on the road to retirement.

By seeing everything in one place, you can better understand how contributing to your IRA impacts other goals, like saving for a down payment or crushing debt. This holistic perspective is the foundation of a solid strategy, and our guide on creating a financial plan walks through the detailed steps.

Beyond Retirement Accounts

A truly comprehensive plan also thinks about what happens to your hard-earned assets down the road. As you weave your IRA into your financial strategy, it’s just as important to think about how it fits into your broader wealth transfer and legacy goals.

Your IRA isn’t just a retirement fund; it’s a significant asset that plays a role in your overall estate. Understanding how it passes to your heirs—and the tax implications for them—is a crucial part of responsible wealth management.

Features like the Roth IRA’s lack of Required Minimum Distributions (RMDs) make it an incredibly powerful tool for legacy planning. For those thinking ahead, resources on Estate Planning for Retirement offer valuable insights on securing your assets for the next generation. This kind of strategic thinking elevates your IRA from a simple savings account to a cornerstone of your family’s financial future.

Common Questions About Roth vs. Traditional IRAs

Even after a deep dive, a few key questions always pop up when it’s time to make the final call. Let’s tackle some of the most common ones we hear from investors who are mapping out their financial futures.

Can I Contribute to Both a Roth and a Traditional IRA in the Same Year?

Absolutely. Not only can you contribute to both, but it can be a savvy move for tax diversification. This strategy gives you a pool of tax-deferred money and another that’s completely tax-free, offering more flexibility in retirement.

Just remember one critical rule: the annual IRA contribution limit is a total across all your IRA accounts. If the 2024 limit is $7,000, you could put $3,500 in your Roth and $3,500 in your Traditional, or split it $6,000 and $1,000—any combo works as long as you don’t go over the total.

What Happens If My Income Is Too High for a Roth IRA?

Hitting the income ceiling for a Roth IRA doesn’t mean you’re out of the game. High earners often turn to a popular strategy called the Backdoor Roth IRA, which we detailed earlier.

The process is straightforward: you make a non-deductible contribution to a Traditional IRA and then immediately convert it to a Roth. It’s a perfectly legal way to fund a Roth IRA, but be mindful of the pro-rata rule if you already have pre-tax money in other Traditional, SEP, or SIMPLE IRAs.

The Backdoor Roth IRA is a powerful workaround that ensures high-income professionals don’t miss out on decades of tax-free growth. It levels the playing field, giving more people access to one of the best retirement accounts out there.

Which IRA Is Better for Estate Planning Purposes?

When it comes to leaving a financial legacy, the Roth IRA usually has a clear advantage. The game-changer is that Roth IRAs are exempt from Required Minimum Distributions (RMDs) for the original owner. This means your account can keep growing, completely tax-free, for your entire life, maximizing what you pass on.

Your beneficiaries who inherit the Roth IRA can then take distributions tax-free. They’ll have their own withdrawal rules, of course, but giving them a source of tax-free wealth makes the Roth an incredibly powerful tool for many estate plans.

Ready to see how your IRA fits into your complete financial picture? With PopaDex, you can track all your accounts in one simple dashboard to make smarter, more confident decisions. Get a holistic view of your net worth today.