Our Marketing Team at PopaDex

8 Powerful Student Loan Payoff Strategies for 2026

Student loan debt can feel like an anchor holding you back from your financial goals, whether that’s buying a home, investing for retirement, or simply achieving financial peace of mind. With balances often in the tens or even hundreds of thousands, the path forward can seem overwhelming and unclear. The good news is that you have more control than you might think. The key goes beyond making monthly payments; it’s about deploying one of several proven student loan payoff strategies tailored to your specific financial situation, career path, and even your personal psychology.

This guide moves beyond generic advice to provide a detailed, step-by-step breakdown of eight distinct and powerful approaches. We’ll explore everything from mathematically optimal methods designed to save you the most money on interest to motivation-based techniques that build momentum and keep you on track. You will learn how to determine if you qualify for federal forgiveness programs like Public Service Loan Forgiveness (PSLF), how to refinance for a lower interest rate, and how to leverage your employer’s assistance programs to accelerate your progress.

Furthermore, we’ll dive into practical tactics like making bi-weekly payments and strategically allocating extra income from side hustles. Building a debt-free future often involves two core components: reducing your debt and increasing your income. As you explore these strategies, remember that boosting your earning potential is a powerful accelerator; one way to do this is to create an online portfolio that gets you hired and showcases your professional skills. This comprehensive list provides the actionable details you need to build your personalized roadmap and reclaim your financial freedom faster than you thought possible.

1. The Debt Avalanche Method

The debt avalanche is one of the most powerful student loan payoff strategies for borrowers who want to minimize costs and get out of debt as quickly as possible. This approach focuses on paying down your loans in order of interest rate, from highest to lowest, regardless of the balance. It’s the most mathematically efficient way to tackle debt, saving you the most money on interest over time.

You begin by making the minimum required payment on all your student loans. Then, you allocate any extra money you can afford toward the single loan with the highest interest rate. Once that high-interest loan is completely paid off, you “avalanche” that entire payment amount (the original minimum plus the extra you were paying) onto the loan with the next-highest interest rate.

How It Works: A Practical Example

Let’s say you have three student loans:

- Loan A: $25,000 at 6.8% interest

- Loan B: $10,000 at 5.5% interest

- Loan C: $15,000 at 4.2% interest

You would make minimum payments on all three loans. If you have an extra $300 each month to put toward your debt, you would direct that entire $300 to Loan A, because it has the highest interest rate (6.8%). After Loan A is paid off, you’d roll its minimum payment plus your extra $300 into the payments for Loan B (5.5%). This focused approach systematically eliminates your most expensive debt first.

Key Benefits and Actionable Tips

The primary advantage of the debt avalanche method is its cost-effectiveness. By targeting high-interest debt, you reduce the total amount of interest that accrues over the life of your loans, which can save you hundreds or even thousands of dollars.

To implement this strategy effectively:

- List Your Loans: Create a spreadsheet listing all your loans, their balances, minimum payments, and interest rates. This gives you a clear roadmap.

- Automate Extra Payments: Set up automatic payments to ensure your extra funds are consistently applied to the target loan. Be sure to instruct your loan servicer to apply the extra amount to the principal of that specific loan, not as an advance payment for the next month.

- Use a Calculator: Online debt avalanche calculators can help you visualize your progress and calculate your total interest savings, which is a great motivator.

This method is ideal for borrowers who are motivated by numbers and long-term financial optimization. While you may not get the quick psychological wins of paying off smaller loans first, the financial rewards make it a superior strategy for accelerating your journey to being debt-free.

2. The Debt Snowball Method

While the debt avalanche focuses on math, the debt snowball method is one of the most popular student loan payoff strategies because it prioritizes psychology and motivation. This approach, championed by personal finance expert Dave Ramsey, involves paying off your loans in order of balance, from smallest to largest, regardless of the interest rate. The goal is to score quick, motivating wins that build momentum and keep you committed to your debt-free journey.

You start by making the minimum required payments on all your student loans. Then, you throw every extra dollar you have at the loan with the smallest balance. Once that first loan is eliminated, you roll its entire payment amount (the minimum plus the extra you were paying) into the payment for the next-smallest loan, creating a “snowball” effect that grows larger and faster as you knock out each debt.

How It Works: A Practical Example

Let’s use the same three student loans but apply the snowball method:

- Loan A: $25,000 at 6.8% interest

- Loan B: $10,000 at 5.5% interest

- Loan C: $15,000 at 4.2% interest

You would make minimum payments on all three loans. If you have an extra $300 each month, you would direct that entire amount to Loan B, because it has the smallest balance ($10,000). After Loan B is paid off, you’d roll its minimum payment plus your extra $300 into the payments for Loan C ($15,000), the next smallest. This strategy gives you the satisfaction of eliminating an entire loan account much faster.

Key Benefits and Actionable Tips

The primary advantage of the debt snowball is the powerful psychological boost it provides. Seeing a loan balance disappear completely can be the motivation needed to stick with a long-term repayment plan, especially if you’ve struggled with debt before. For more in-depth strategies, you can learn more about how to pay off debt on popadex.com.

To implement this strategy effectively:

- Create a Visual Tracker: Make a chart or spreadsheet listing your loans from smallest to largest balance. Visually crossing off each loan as it’s paid provides a huge sense of accomplishment.

- Celebrate the Wins: When you pay off a loan, celebrate it! This reinforces the positive behavior and makes the process more enjoyable.

- Stay Focused on Behavior: Remember that this method is about changing your behavior with money. The quick wins are designed to build habits that last.

- Share Your Progress: Tell an accountability partner or online community about your progress. Sharing your successes can provide extra encouragement to keep going.

This method is ideal for borrowers who are motivated by progress and quick wins. While you may pay more in total interest compared to the avalanche method, its effectiveness in keeping people engaged often makes it the superior strategy for those who need to build and maintain momentum.

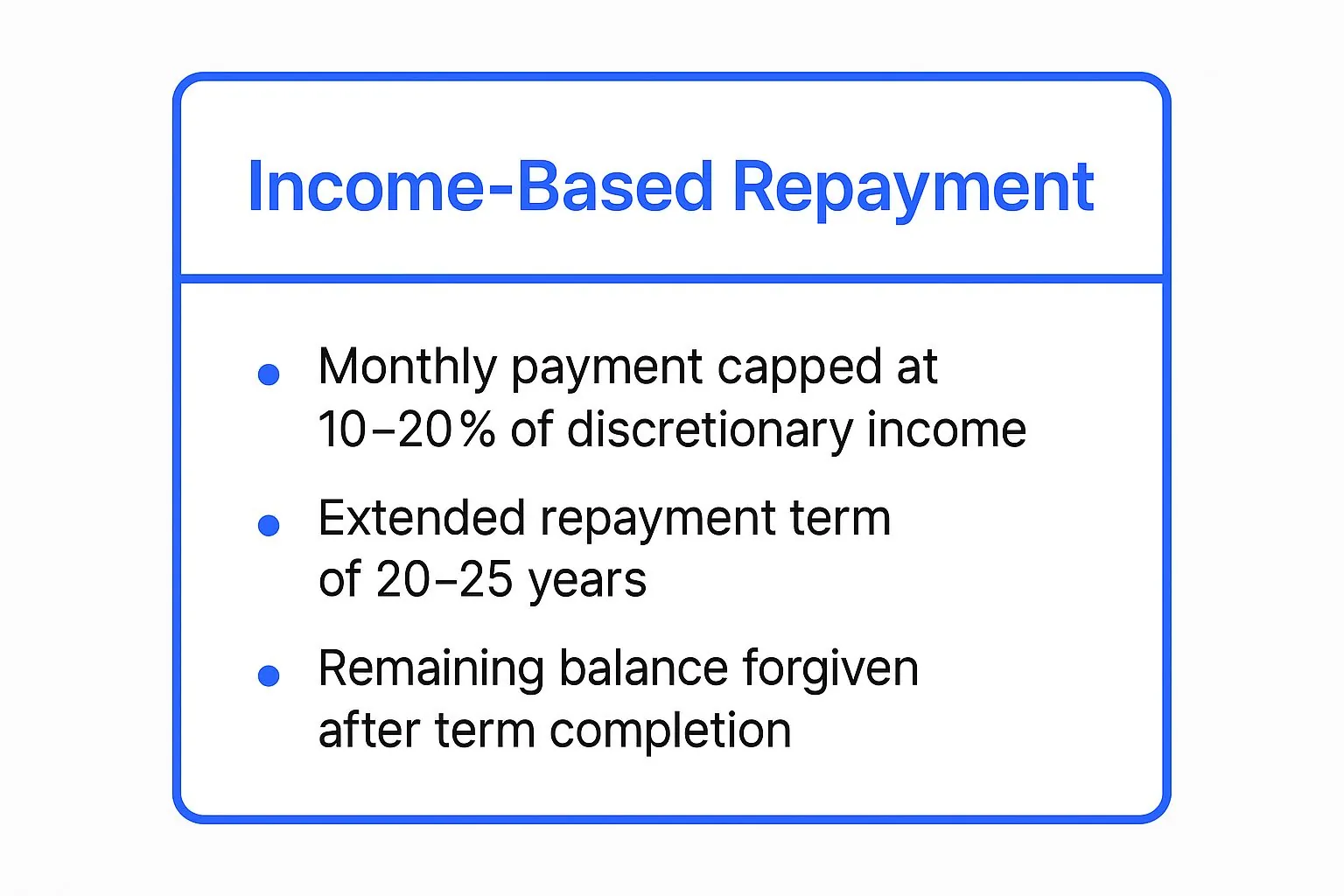

3. Income-Driven Repayment (IDR) Plans with Forgiveness

For federal student loan borrowers, Income-Driven Repayment (IDR) plans can be one of the most essential student loan payoff strategies, especially for those with a high debt-to-income ratio. These plans calculate your monthly payment based on a percentage of your discretionary income, typically 10-15%, rather than your total loan balance. This makes payments more manageable during periods of lower earnings.

The core benefit of an IDR plan is twofold: it provides immediate monthly payment relief and offers a long-term solution through loan forgiveness. After making consistent qualifying payments for a set period, usually 20 or 25 years, the federal government forgives any remaining loan balance. This makes it a powerful tool for individuals who don’t expect their income to rise high enough to pay off their loans in a standard term.

To give a quick reference of their core features, here is a summary of how IDR plans generally work.

These key components work together to make debt manageable in the short term while providing a clear path to forgiveness in the long term.

How It Works: A Practical Example

Let’s consider a teacher with $80,000 in federal student loans who earns an annual salary of $45,000.

- Standard 10-Year Repayment: The monthly payment could be around $900, which would be a significant portion of their take-home pay.

- On an IDR Plan (like SAVE): The payment might be capped at around $200 per month, based on their discretionary income.

By enrolling in an IDR plan, the teacher’s monthly payment becomes affordable, freeing up over $700 per month for other essential expenses. After making payments for 20-25 years, the remaining balance on their loans would be forgiven. This strategy is also crucial for medical residents who have high debt but low income during their training years.

Key Benefits and Actionable Tips

The main advantage of IDR plans is the affordability and the promise of eventual forgiveness. They provide a safety net, ensuring your student loan payments never consume an unmanageable portion of your income.

To implement this strategy effectively:

- Recertify Annually: You must recertify your income and family size each year. Missing the deadline can cause your monthly payment to increase dramatically to the standard repayment amount.

- Compare Plan Options: Use the Federal Student Aid Loan Simulator at StudentAid.gov to compare plans like SAVE, PAYE, and IBR to see which offers the lowest payment and best long-term outcome for you.

- Plan for the “Tax Bomb”: The forgiven loan amount may be treated as taxable income in the year it’s forgiven. It’s wise to set aside money over time to prepare for this potential tax liability.

- Consider PSLF: If you work in public service, you may qualify for Public Service Loan Forgiveness (PSLF), which offers tax-free forgiveness after just 10 years of qualifying payments while on an IDR plan.

This method is ideal for borrowers whose debt is high relative to their income, or for those in public service careers. It transforms an overwhelming debt burden into a manageable, long-term financial plan with a definitive end date.

4. Refinancing to Lower Interest Rates

Refinancing is a powerful student loan payoff strategy that involves replacing one or more existing student loans with a new, single private loan. The goal is to secure a lower interest rate and more favorable terms, which can significantly reduce your monthly payments or shorten your repayment timeline. Private lenders assess your credit score, income, and overall financial health to offer you a competitive rate, potentially saving you thousands over the life of your loan.

This approach is particularly effective for borrowers with stable employment and a good credit history who are paying high interest on their current loans. By consolidating multiple loans into one, you also simplify your finances, making it easier to manage a single monthly payment instead of juggling several. However, it’s crucial to understand that refinancing federal loans with a private lender means permanently giving up federal protections like income-driven repayment plans and forgiveness programs.

How It Works: A Practical Example

Let’s imagine a borrower with a strong financial profile and two student loans:

- Loan A (Federal): $40,000 at 6.8% interest

- Loan B (Private): $20,000 at 8.5% interest

With a good credit score (750+) and a stable income, they shop for refinancing offers and are approved for a new private loan of $60,000 at a 4.5% fixed interest rate on a 10-year term. By refinancing, their new single monthly payment is lower, and more importantly, they are on track to save over $12,000 in total interest compared to their original loans. This is a common scenario for graduates who have improved their financial standing since taking out their initial student loans.

Key Benefits and Actionable Tips

The main benefit of refinancing is the potential for substantial interest savings, which directly accelerates your path out of debt. A lower interest rate means more of your payment goes toward the principal balance each month, helping you pay off your debt faster and for less money. For those looking to manage their cash flow, refinancing can also lower the monthly payment amount.

To implement this strategy effectively:

- Compare Multiple Lenders: Don’t accept the first offer you receive. Use rate comparison tools from lenders like SoFi, Earnest, and Laurel Road to find the best possible terms without impacting your credit score.

- Check Your Credit: Before applying, check your credit score and report. A higher score qualifies you for better rates, so take steps to improve it if necessary.

- Be Strategic with Federal Loans: If you might need federal benefits like Public Service Loan Forgiveness (PSLF) or income-driven repayment, consider only refinancing your high-interest private loans and keeping your federal loans separate.

- Choose the Right Term: Opt for the shortest repayment term you can comfortably afford. A shorter term, like 5 or 7 years, will have a higher monthly payment but will maximize your total interest savings. Strong financial planning is key to making this decision; for more guidance, you can learn more about financial planning for beginners on popadex.com.

This method is ideal for financially stable borrowers who want to optimize their repayment and are not reliant on federal loan protections. It is one of the most effective student loan payoff strategies for cutting long-term costs.

5. Public Service Loan Forgiveness (PSLF)

For borrowers working in government or for a non-profit organization, the Public Service Loan Forgiveness (PSLF) program is one of the most impactful student loan payoff strategies available. This federal program is designed to forgive the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments while working full-time for an eligible employer. It’s a powerful incentive for graduates to enter and remain in public service careers.

The core of the strategy involves enrolling in an Income-Driven Repayment (IDR) plan to keep your monthly payments as low as possible for 10 years. After making 120 on-time payments, the entire remaining loan balance is forgiven, tax-free. This approach is not about aggressive repayment; it’s about strategic patience and maximizing the amount forgiven at the end of the term.

How It Works: A Practical Example

Let’s imagine a public school teacher with federal student loans:

- Total Debt: $90,000 in Direct Loans

- Income: $55,000 per year

- Repayment Plan: Enrolled in the SAVE Plan (formerly REPAYE)

Under the SAVE Plan, their monthly payment might be around $250. Over 10 years (120 payments), they would pay a total of $30,000. Assuming their loan balance grew with interest, they could have over $80,000 forgiven, completely tax-free, for serving their community. This transforms a potentially crippling debt into a manageable expense.

Key Benefits and Actionable Tips

The primary advantage of PSLF is the potential for significant, tax-free loan forgiveness, which can be life-changing for those with high debt-to-income ratios. It allows professionals in vital but often lower-paying fields to manage their educational debt without financial distress.

To implement this strategy effectively:

- Verify Your Employer and Loans: Use the PSLF Help Tool on StudentAid.gov to confirm your employer qualifies and that you have Direct Loans. If you have other federal loan types, consolidate them into a Direct Consolidation Loan immediately to start the clock on qualifying payments.

- Certify Your Employment Annually: Submit the PSLF Certification & Application Form (formerly ECF) every year and whenever you change jobs. This creates an official record of your qualifying payments, preventing surprises down the road.

- Enroll in an IDR Plan: Choose an income-driven repayment plan like SAVE, PAYE, or IBR. This is crucial for minimizing your monthly payments and maximizing the final forgiveness amount.

- Keep Meticulous Records: Save all correspondence from your loan servicer (now MOHELA for PSLF), proof of employment, and payment confirmations in a dedicated folder.

This method is ideal for borrowers committed to a career in public service who have a federal loan balance high enough to benefit from forgiveness after 10 years of payments.

6. Employer Student Loan Repayment Assistance Programs

One of the most impactful student loan payoff strategies involves leveraging a benefit that is rapidly gaining popularity: employer-sponsored repayment assistance. These programs, often called LRAPs (Loan Repayment Assistance Programs), function like a 401(k) match but for your education debt. Your employer makes direct, regular contributions toward your student loan balance, significantly accelerating your payoff timeline without costing you a dime.

This benefit has become a powerful recruitment and retention tool for companies. Thanks to legislation extended through 2025, employers can contribute up to $5,250 per employee annually on a tax-free basis. This means neither you nor your employer pays taxes on that contribution, making it a highly efficient form of compensation dedicated solely to eliminating your student debt.

How It Works: A Practical Example

Imagine you work for a company that offers the maximum tax-free benefit. Let’s look at the impact on a single loan:

- Your Loan: $30,000 at 6.0% interest

- Your Payment: $333 per month (standard 10-year term)

- Employer Contribution: $437.50 per month ($5,250 / 12 months)

With your employer’s contribution, a total of $770.50 is applied to your loan each month. This extra payment turbocharges your progress, allowing you to pay off the loan in just over three years instead of ten, saving you more than $7,000 in interest. Companies like PwC, Fidelity Investments, and Aetna are well-known for offering these valuable benefits to attract and retain talent.

Key Benefits and Actionable Tips

The primary advantage is receiving free money to pay down your debt faster and save thousands on interest. It’s a direct financial boost that reduces your principal balance much more quickly than you could on your own.

To implement this strategy effectively:

- Inquire Early: Ask about student loan repayment assistance during job interviews and salary negotiations. The value of this benefit can be a significant factor when comparing total compensation packages.

- Target High-Interest Loans: If your employer allows it, direct their contributions to your loan with the highest interest rate to maximize your savings, similar to the debt avalanche method.

- Combine with Your Payments: Don’t reduce your own payments. Continue making your regular and any extra payments you can afford to compound the benefit and become debt-free even sooner.

- Verify Application: Log into your loan servicer’s portal to confirm that your employer’s contributions are being applied correctly, ideally as extra payments toward the principal balance.

7. Aggressive Bi-Weekly Payment Strategy

The bi-weekly payment strategy is a clever and largely effortless way to accelerate your student loan repayment. Instead of making one full monthly payment, you make half of your payment every two weeks. This simple shift results in 26 half-payments over the year, which is equivalent to 13 full monthly payments instead of the standard 12. This “extra” payment goes directly toward your principal, helping you pay down your loan faster and save on interest.

This approach works exceptionally well because it aligns with a common bi-weekly pay schedule, making it feel like a normal, manageable expense rather than a major budget adjustment. You are essentially tricking yourself into making an extra payment each year without the financial strain of a large lump-sum contribution. It’s a fantastic, low-impact addition to your student loan payoff strategies.

How It Works: A Practical Example

Let’s say your standard monthly student loan payment is $400. Instead of paying that amount once a month, you would set up a payment of $200 every two weeks.

- Monthly Schedule: $400 x 12 months = $4,800 per year

- Bi-Weekly Schedule: $200 x 26 payments = $5,200 per year

That extra $400 each year is applied directly to your principal balance. For a borrower with a $30,000 loan at 6% interest, this small change could lead to paying off the loan in about 8.5 years instead of 10, saving over $2,100 in total interest payments.

Key Benefits and Actionable Tips

The main benefit of this strategy is that it automates an extra payment each year, reducing your principal and total interest without feeling like a major budget sacrifice. It shortens your loan term and aligns payments with your cash flow, making debt management smoother.

To implement this strategy effectively:

- Talk to Your Servicer: First, contact your loan servicer to confirm they can process bi-weekly payments. Critically, you must instruct them to apply the extra funds directly to the principal balance of your loan, not as a pre-payment for the next month’s bill.

- Automate Everything: Set up automatic transfers from your checking account to align with your paydays. This “set it and forget it” approach ensures consistency.

- Use a Calculator: Online bi-weekly loan payment calculators can show you exactly how much time and money you’ll save, providing powerful motivation to stick with the plan.

- DIY if Necessary: If your servicer doesn’t support bi-weekly payments, you can achieve the same result. Simply divide your monthly payment by 12 and add that amount to each payment you make, or make one extra full payment at the end of the year.

This method is perfect for borrowers who receive bi-weekly paychecks and want an automated, low-effort way to get ahead on their loans without drastically changing their spending habits.

8. Side Hustle Income Allocation Strategy

The side hustle income allocation strategy is a powerful method for supercharging your debt repayment without sacrificing your current lifestyle. This approach involves dedicating 100% of the income from a secondary job or freelance work directly to your student loan debt. By living on your primary income, you create a clear mental and financial separation: your main job covers living expenses, while all extra earnings are channeled exclusively toward debt elimination.

This strategy dramatically accelerates your payoff timeline by applying significant, consistent extra payments to your loan principal. It leverages the growing gig economy, where opportunities for supplemental income are more accessible than ever. It’s one of the most effective student loan payoff strategies for those who want to see rapid progress without cutting back on their core budget.

How It Works: A Practical Example

Imagine you’re a marketing professional with a primary salary. You start a side business managing social media for small businesses, which generates an extra $800 per month. Instead of letting that money blend into your regular spending, you immediately apply the full $800 to your highest-interest student loan each month.

Let’s consider other scenarios:

- A software developer freelancing in the evenings makes an additional $1,500 a month, allowing them to eliminate a $60,000 debt in just over three years.

- A nurse picks up extra hospital shifts and dedicates all overtime pay to their loans, paying off $45,000 in under two years.

- A teacher tutors online for five hours a week, earning an extra $400 monthly. This extra income helps them pay off a $35,000 loan four years ahead of schedule.

Key Benefits and Actionable Tips

The main benefit of this strategy is its ability to aggressively pay down debt without impacting your day-to-day finances, as you maintain your established standard of living. This clear separation makes it easier to stay motivated and track your progress. If you’re looking to boost your income to pay down debt faster, consider exploring guides on finding freelance remote jobs.

To implement this strategy effectively:

- Choose a Skill-Aligned Hustle: Select a side gig that uses your existing skills to minimize the learning curve and maximize your earning potential from day one.

- Separate Your Finances: Open a dedicated bank account for your side hustle income. This creates a psychological barrier and prevents the money from being spent on non-debt expenses.

- Automate Payments: Set up an automatic transfer from your side hustle account directly to your student loan servicer each month. This ensures every dollar earned goes straight to your debt.

- Prevent Burnout: Create a sustainable schedule, such as working a few evenings a week or one day on the weekend, to avoid exhaustion and stay consistent.

- Redirect Future Income: Once your student loans are fully paid off, you can redirect this established income stream toward wealth-building goals like investing or saving for a down payment. You can learn more about how to put this extra cash to work by exploring what passive income is.

Student Loan Payoff Strategies Comparison

| Strategy | Implementation Complexity | Resource Requirements | Expected Outcomes | Ideal Use Cases | Key Advantages |

|---|---|---|---|---|---|

| The Debt Avalanche Method | Moderate - requires discipline | Consistent extra payments needed | Minimizes total interest, faster payoff | Mathematically-minded borrowers motivated by long-term savings | Saves most interest, fastest mathematically |

| The Debt Snowball Method | Easy - simple prioritization | Minimum payments + focus on smallest loan | Quick psychological wins, builds momentum | Borrowers needing motivation and early victories | Boosts motivation with quick wins |

| Income-Driven Repayment (IDR) Plans | Moderate - annual income recert. | Income-based payments, paperwork | Low monthly payments, potential forgiveness after 20-25 years | Borrowers with high debt-to-income, financial hardship | Lowers payments, offers forgiveness path |

| Refinancing to Lower Interest Rates | Moderate - credit check, application | Good credit and income required | Lower interest rates, reduced monthly payments | Borrowers with strong credit and high-interest loans | Significant interest savings, simplifies payments |

| Public Service Loan Forgiveness (PSLF) | High - employment and paperwork compliance | Full-time qualifying public service job | Forgiveness after 10 years, tax-free | Public service workers with long-term commitment | Tax-free forgiveness in 10 years |

| Employer Student Loan Repayment Assistance | Low - passive benefit | Depends on employer offering benefit | Accelerates payoff without personal budget impact | Employees at companies offering repayment benefits | Tax-free employer contributions |

| Aggressive Bi-Weekly Payment Strategy | Easy - setup automatic payments | Frequent payments aligned with paychecks | Shortens loan term by 2-3 years, reduces interest | Borrowers paid bi-weekly wanting extra payment effect | Extra annual payment with minimal budget strain |

| Side Hustle Income Allocation Strategy | High - requires extra work/effort | Time and energy for side income | Dramatically accelerates payoff without lifestyle cuts | Motivated borrowers with skills and time for side income | Speeds payoff while maintaining living standard |

Choosing Your Strategy and Taking Action

Embarking on the journey to become debt-free is a significant step toward achieving true financial independence. Throughout this guide, we’ve navigated a comprehensive map of powerful student loan payoff strategies, each offering a unique path out of debt. The key takeaway is that there is no single “best” method for everyone; the optimal approach is deeply personal and depends entirely on your unique financial landscape, career trajectory, and even your psychological motivation.

Your mission now is to move from passive learning to decisive action. The strategies we’ve detailed, from the mathematically sound Debt Avalanche to the motivation-boosting Debt Snowball, provide the tactical tools. Whether you’re a public servant pursuing PSLF, a high-earner considering refinancing, or a gig worker leveraging a side hustle, the principles remain the same: clarity, commitment, and consistency are your greatest assets.

Synthesizing Your Personal Payoff Plan

The power of these strategies is amplified when they are combined. You don’t have to choose just one. For instance, you could refinance your high-interest private loans to a lower rate and then apply the Debt Avalanche method to the newly consolidated loan to pay it off even faster. Simultaneously, you could be enrolled in an Income-Driven Repayment plan for your federal loans, working toward eventual forgiveness while making manageable monthly payments.

Think of these methods as building blocks for a custom-tailored financial plan.

- For the motivation-seeker: The Debt Snowball method offers quick wins that build momentum. Pairing this with a Side Hustle Income Allocation strategy can supercharge your progress, creating a powerful feedback loop of success.

- For the numbers-driven professional: The Debt Avalanche method is your most efficient path, saving you the most money in interest. Combining this with an aggressive bi-weekly payment schedule will shave years and thousands of dollars off your repayment term.

- For the public service employee: Your strategy is clear: enroll in a qualifying IDR plan and meticulously track your progress toward Public Service Loan Forgiveness (PSLF). Don’t forget to explore employer assistance programs that could supplement your efforts.

Your Immediate Next Steps

Information without implementation is just trivia. To turn this knowledge into tangible results, you must take concrete, actionable steps today. The journey of a thousand miles begins with a single step, and your journey to being debt-free starts with organization.

- Consolidate Your Data: Before you can attack your debt, you need a clear picture of it. Gather all your loan documents. Create a master spreadsheet or use a financial dashboard to list every single loan, including the lender, current balance, and, most importantly, the interest rate.

- Run the Numbers: Use the Federal Student Aid Loan Simulator to model different repayment plans like PAYE or SAVE. Contact multiple lenders to get real refinancing quotes and compare the potential interest savings against the loss of federal protections.

- Automate and Commit: Once you’ve chosen your primary strategy, put it on autopilot. Set up automatic bi-weekly payments. Create an automatic transfer from your checking account to your high-yield savings account dedicated to lump-sum debt payments. Automation removes friction and ensures you stay on track.

Mastering these student loan payoff strategies is about more than just eliminating a line item on your budget. It’s about reclaiming your financial future. It’s about redirecting hundreds, or even thousands, of dollars each month from interest payments toward your own goals: investing for retirement, saving for a down payment, or traveling the world. Each extra payment you make is a direct investment in your own freedom. The path is clear, the tools are in your hands, and the reward is a life unburdened by student debt.

Ready to get a crystal-clear view of your entire financial picture? PopaDex helps you consolidate your student loans alongside all your other accounts, so you can track your payoff progress in real-time and make informed decisions. Start building your personalized debt-free plan today by visiting PopaDex.