Our Marketing Team at PopaDex

What Is Financial Independence: what is financial independence for your future?

Financial independence is the point where you no longer have to work for money. It’s when your assets—your investments, properties, and other income streams—generate enough cash to cover all your living expenses for the rest of your life.

This isn’t about being fabulously wealthy. It’s about being fundamentally free.

Understanding What Financial Independence Really Means

At its heart, financial independence means flipping the script on the traditional career path. Instead of relying on a paycheck to live, you build a portfolio of assets that work for you. Think stocks, real estate, or even a side business that runs without your daily involvement. This collection of assets becomes your personal economic engine, giving you total control over your most valuable resource: your time.

Picture your investments like an orchard you’ve spent years planting and tending. Financial independence is the moment that orchard produces enough fruit (your passive income) to feed you year after year. You don’t have to toil in the fields anymore—unless, of course, you want to.

The True Goal: Autonomy and Choice

The journey to FI is less about spreadsheets and more about a deep-seated desire for autonomy. It’s the power to design your days around what truly matters to you, whether that’s traveling the world, launching a passion project, or simply being more present with your family. It fundamentally decouples your survival from your job.

This is why so many people are exploring different ways to stop trading time for money on their path to FI. The ultimate prize is a life where your finances serve your values, not the other way around.

Financial independence is the ultimate form of self-reliance. It grants you the power to design your life based on your own terms, not on economic necessity. It shifts the focus from earning a living to simply living.

Putting a Number on Freedom

While the feeling of freedom is the goal, getting there requires a concrete target. Recent country-level research helps put a real number on it. A 2025 study in the UK, for instance, found that an average household would need around £743,338 in investments to cover their living costs for 25 years. This calculation assumes a 5% annual return that outpaces inflation, showing how much heavy lifting your investment growth can do. You can dig into the full financial independence research for a closer look.

Of course, this number isn’t one-size-fits-all. A high-spending household might need over £1.3 million, while a more frugal one could get there with closer to £706,167. The crucial takeaway is that your personal FI number is tied directly to your annual expenses, making a clear understanding of your spending the very first step on this empowering journey.

How to Calculate Your Financial Independence Number

Financial independence can feel like a fuzzy, far-off dream. But what if you could turn that dream into a hard number? That’s exactly what your Financial Independence (FI) Number does. It transforms a vague goal into a concrete target, showing you exactly how much you need in investments to live off the returns forever.

Forget complex algorithms. The calculation is surprisingly simple, but it’s the most powerful step you can take toward making FI a reality.

The 25x Rule Explained

The go-to method for finding your FI Number is the 25x Rule. It’s a straightforward principle: you are financially independent when you have saved 25 times your expected annual expenses.

Here’s the formula:

Your FI Number = Your Annual Expenses x 25

Let’s say you figure out you need $60,000 a year to live comfortably. Using the 25x Rule, your FI Number is $1,500,000 (that’s $60,000 x 25). Once you have that much invested, it should generate enough passive income to cover your spending year after year.

This is the core idea—building a base of assets that works for you, so you don’t have to.

As the diagram shows, it all starts with your assets. They’re the foundation for creating the passive income that ultimately buys your freedom.

The Power Behind the Math: The 4 Percent Rule

So, where does “25” come from? It is more than a random number. It’s actually the flip side of another crucial concept in the retirement world: the 4% Rule, also known as the Safe Withdrawal Rate (SWR).

This rule suggests you can safely withdraw 4% of your investment portfolio in your first year of retirement, then adjust that amount for inflation every year after, without a high risk of running out of money. Think of your portfolio as a goose that lays golden eggs. The 4% rule tells you how many eggs you can take each year without harming the goose, ensuring it keeps laying them for decades to come.

Getting this right is a cornerstone of long-term planning. You can dig deeper into the details of a safe withdrawal rate for retirement planning to see how it holds up in different market scenarios.

What Flavor of FI Are You?

Financial independence isn’t a single destination; it’s a spectrum. Your target number depends entirely on the lifestyle you want. The FI community has come up with a few handy terms to describe these different paths.

- Lean FI: This is the minimalist’s route. If you’re happy living on a modest budget, you can reach FI much faster. For someone with $30,000 in annual expenses, the FI number is just $750,000.

- Fat FI: This is for those who want a more luxurious retirement filled with travel, hobbies, and a high standard of living. If your dream lifestyle costs $120,000 a year, your target FI number jumps to a cool $3 million.

- Coast FI: This is a fantastic milestone where you’ve invested enough that your portfolio will grow to support a traditional retirement (say, by age 65) without you adding another dime. Once you hit Coast FI, you can “coast”—maybe take a less stressful job or work part-time just to cover your current bills, knowing your retirement is already locked in.

Your FI number isn’t just a financial calculation; it’s a reflection of your values and priorities. It quantifies the cost of the life you want to live, making your abstract goals concrete and actionable.

Modern financial dashboards are built to handle these calculations for you. For instance, a tool like PopaDex lets you track your net worth against your FI number in real-time. This gives you a clear, motivating picture of your progress, turning a long journey into a series of achievable steps.

The Three Pillars of an Effective FI Strategy

Reaching financial independence isn’t about stumbling upon a secret formula or getting lucky with a hot stock tip. It’s a journey, one built on a disciplined and repeatable strategy. This strategy stands on three powerful pillars that work together to build real, lasting wealth and create the freedom you’re after.

By focusing on these core areas, you can turn the abstract goal of FI into a tangible, achievable plan.

Understanding and putting these pillars into action gives you a clear roadmap. Each one tackles a critical part of your financial life, from how you handle your income to how you make your money grow for you.

Pillar 1 Master Your Savings Rate

A lot of people think a high income is the key to getting rich. While it certainly helps, the single most powerful metric on your journey to FI is your savings rate—the percentage of your income you actually keep and put to work. Think about it: someone earning $50,000 and saving 50% will reach financial independence decades before someone earning $200,000 but only saving 10%.

A high savings rate is so effective because it attacks the FI equation from two angles at once:

- You stack up assets way faster. Every dollar saved is a dollar invested, turbocharging the growth of your financial base.

- You learn to live on less. This directly shrinks your target FI number, pulling the finish line much, much closer.

Mastering your savings rate isn’t just about making more money; it’s about optimizing your spending. This isn’t about deprivation, but conscious consumption. Every spending decision becomes an active choice: immediate gratification now, or long-term freedom later?

Pillar 2 Conquer High-Interest Debt

Imagine trying to climb a tall ladder while wearing a heavy backpack full of rocks. With every step you take, that weight is pulling you back down. That’s exactly what high-interest debt—like credit card balances or personal loans—does to your financial progress.

The interest rates on this kind of debt often soar past 20% annually, a return you’re highly unlikely to beat consistently in the stock market. Paying off this debt is a guaranteed, risk-free return on your money. You’re essentially “un-losing” money, which is just as powerful as earning it.

Conquering debt is more than a financial move; it’s a strategic one. It frees up your most powerful wealth-building tool—your income—to work for you instead of against you.

To get rid of this financial drag for good, you can use proven strategies:

- The Debt Snowball: Pay off your smallest debts first. Those quick wins create psychological momentum that keeps you going.

- The Debt Avalanche: Focus on paying off debts with the highest interest rates first. This method saves you the most money over time.

Whichever path you choose, the destination is the same: eliminate the dead weight holding you back so you can climb toward FI faster and more efficiently.

Pillar 3 Invest Intelligently for Growth

Once you’ve cranked up your savings rate and crushed your high-interest debt, it’s time for the third pillar: putting your money to work. This is where you shift from just saving money to actively growing it, letting the incredible power of compound growth become your greatest ally.

Think of your investments like a tiny snowball at the top of a very long, snowy hill. As it starts rolling, it picks up more snow, getting bigger and moving faster. Over many years, that tiny ball can become an unstoppable force. Your money works the same way; the returns your investments generate start earning their own returns, creating exponential growth.

You don’t need to be a Wall Street wizard to do this well. For most people, the simplest approach is the best: consistently investing in low-cost, diversified index funds or ETFs. These funds track broad market indexes (like the S&P 500), giving you instant diversification without the hefty fees of actively managed funds. This pillar is all about consistency over complexity. For a deeper look at how investments generate returns, check out our complete guide on what passive income is and how it works.

Unique Considerations for Global Citizens

For expats and digital nomads, managing finances across different countries adds another layer of complexity to these three pillars. Fluctuating exchange rates can mess with both your savings rate and the value of your investments. Juggling multi-currency accounts, navigating cross-border tax rules, and picking the right investment platforms are all critical hurdles. This is where a tool like PopaDex, built for multi-currency tracking, becomes essential for keeping a clear financial picture.

This global perspective really highlights the value of financial literacy. Recent global policy research found a direct link between a person’s financial capability and their household’s stability. In fact, the analysis showed that just a 1 percentage-point improvement in financial literacy is associated with a 2.8 percentage-point drop in household loan defaults. You can discover more insights about these findings in the Principal 2025 Global Financial Inclusion Index.

How to Track Your Progress Toward Financial Freedom

Setting out on the journey to financial independence without a map is like trying to sail across the ocean without a compass. You can’t improve what you don’t measure, and tracking your progress is what turns a vague dream into a real, achievable project.

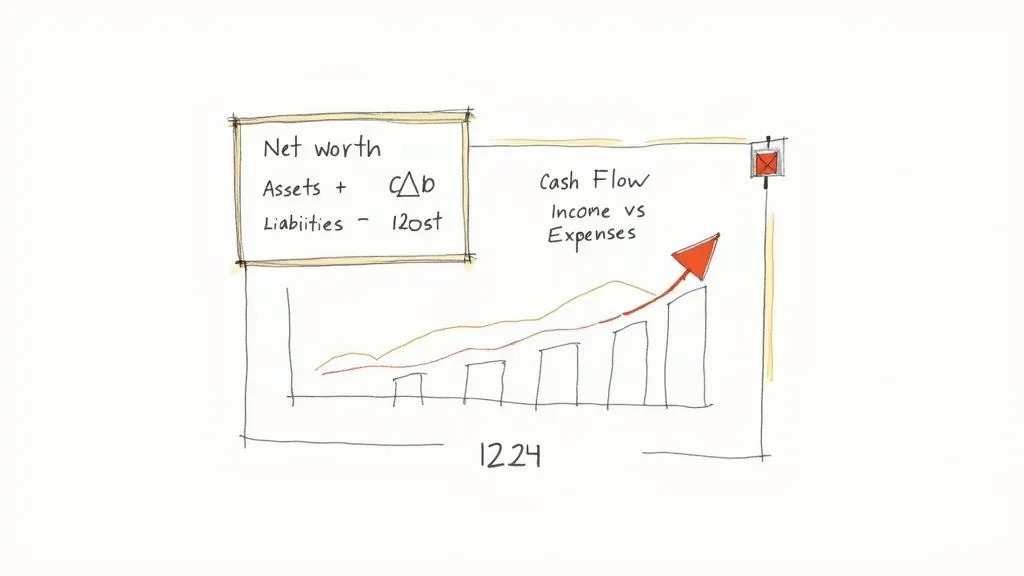

When it comes to your financial health, there are two vital signs that tell you exactly where you stand and how fast you’re moving: Net Worth and Cash Flow. Getting a handle on these two metrics is the first step toward taking full control of your financial future. They work together to give you the complete picture—one shows your current position, and the other shows your momentum.

Net Worth: Your Financial Scorecard

Think of your net worth as the ultimate scorecard on your path to FI. It’s a simple, powerful snapshot of your entire financial position at a single point in time. The calculation couldn’t be easier:

Assets (what you own) - Liabilities (what you owe) = Net Worth

It’s basically your personal balance sheet. The goal is simple: make this number grow, consistently, over time.

To get an accurate number, you’ll need to tally up everything on both sides of that equation.

- Your Assets Include:

- Cash in your checking and savings accounts

- The current value of your investment portfolio (stocks, bonds, retirement funds)

- The market value of any real estate you own

- The value of big-ticket items like your car

- Your Liabilities Include:

- Mortgage balances

- Student loan debt

- Car loans

- Credit card balances

- Any other personal loans you have outstanding

Tracking this number, even just once a quarter, is incredibly motivating. Watching your net worth climb is tangible proof that your hard work and strategy are paying off. If you’re just starting out, our free net worth tracking spreadsheet is a great way to get everything organized and start monitoring your growth.

Cash Flow: The Engine of Your Growth

If net worth is your scorecard, then cash flow is the engine that powers your score higher. It measures the money flowing in and out of your accounts over a period, usually a month. The formula is just as straightforward:

Income (what you earn) - Expenses (what you spend) = Cash Flow

A positive cash flow means you have a surplus. This is the money you can use to pay down debt and invest—the two key actions that boost your net worth. A negative cash flow means you’re spending more than you earn, which actively pushes you further away from financial independence.

The point of tracking your cash flow isn’t to create a restrictive, joyless budget. It’s about achieving financial awareness—making sure your spending actually aligns with your deepest values and long-term goals.

When you see exactly where your money goes, you can start making conscious choices. You might realize you’re spending hundreds on subscriptions you don’t even use—money that could be accelerating your journey to FI. This awareness lets you optimize your spending without feeling deprived, simply by channeling your resources toward what truly matters to you.

Using a Dashboard as Your Co-Pilot

Manually crunching these numbers in spreadsheets works, but let’s be honest—it can be tedious and time-consuming. This is especially true for expats or anyone with assets in multiple currencies or accounts. This is where a dedicated financial dashboard becomes your indispensable co-pilot.

Modern tools like PopaDex are built to automate this entire process. They sync with your various accounts, pulling all your financial data into one clear, visual interface. This lets you:

- Monitor your net worth and cash flow in real-time.

- See exactly how you’re tracking toward your FI number.

- Spot spending patterns and find new opportunities to save.

- Make informed financial decisions quickly and with confidence.

By automating the boring work of tracking, you can free up your energy to focus on the big-picture strategies that will actually get you to financial freedom faster.

Common Pitfalls on the Road to FI and How to Sidestep Them

The journey to financial independence is more of a mental marathon than a mathematical sprint. While the calculations are pretty simple, the path is littered with predictable roadblocks and psychological traps that can derail even the most focused saver. Knowing what these hurdles are ahead of time is the best way to stay resilient and keep moving forward.

Getting to FI is really about sidestepping the common challenges that trip most people up. Let’s break down the most frequent pitfalls and map out a clear plan to navigate them.

Resisting Lifestyle Inflation

One of the sneakiest threats to your FI timeline is lifestyle inflation. It’s that natural urge to spend more as your income grows. You get a promotion, you upgrade the car. You land a bonus, you book a fancier vacation. There’s nothing wrong with enjoying your hard-earned success, but if you’re not careful, you’ll just keep moving the goalposts further and further away.

Remember, your FI number is based on your annual expenses. If those expenses keep creeping up, your target becomes a moving one, and you get stuck on a “hedonic treadmill” where you feel like you’re running hard but never actually getting ahead.

The best defense is a good offense: automate your progress. The moment you get a raise, immediately bump up your automated savings and investment contributions. By paying your future self first, you take the temptation to absorb that new income into your daily spending right off the table. A great rule of thumb is to save at least 50% of every raise. This strategy lets you enjoy some of your success now while seriously accelerating your path to freedom.

Overcoming Analysis Paralysis

The world of investing can feel like a labyrinth. With endless options, conflicting advice, and scary market headlines, it’s incredibly easy to get stuck in analysis paralysis—overthinking things so much that you never actually do anything. You spend months researching the “perfect” fund or waiting for the “perfect” time to invest, all while your money sits in a savings account, quietly losing value to inflation.

Perfection is the enemy of progress on the FI journey. The cost of waiting is almost always higher than the cost of starting with a simple, good-enough plan.

The solution? Keep it simple. Start with a low-cost, broadly diversified index fund or ETF. You don’t need a portfolio worthy of a Wall Street wizard to build wealth; you just need to be consistent. Set up an automatic investment plan and let it run. Starting small is infinitely better than not starting at all.

Navigating Market Volatility

Watching your portfolio value plummet during a market downturn is tough. It’s human nature to panic and feel the urge to sell everything to “stop the bleeding.” But reacting emotionally to market swings is one of the most destructive things an investor can do. History has shown us, time and again, that markets recover. Those who stay the course are rewarded for their patience.

You’re a long-term investor, not a day trader. During a downturn, you haven’t actually lost any money unless you sell. In fact, think of it this way: your regular contributions are now buying you more shares at a discount. Reframe market dips as a sale on your favorite assets, and trust in the long-term growth of the market.

Avoiding the Comparison Trap

In the age of social media, it’s dangerously easy to fall into the comparison trap. You scroll through feeds of friends on lavish vacations or showing off new cars and start questioning your own progress. This is a toxic habit that breeds feelings of inadequacy and can tempt you to abandon your own financial plan just to keep up with appearances. Your FI journey is yours alone—comparing it to someone else’s highlight reel is a recipe for misery.

The desire for financial independence is universal, but how prepared people feel varies wildly. Recent global retirement data found a huge confidence gap: optimism about retirement readiness jumped to 43% for people who invest outside of their workplace plans, compared to just 24% for those who don’t. This shows a direct link between taking action and feeling secure. You can find more on this in the 2025 Global Retirement Reality Report.

So, tune out the noise. Focus on your own progress, celebrate your own milestones, and remember what you’re building: a life of authentic freedom, not just an image of success.

Your Top Financial Independence Questions, Answered

As you start exploring financial independence, you’ll find that some questions pop up again and again. While everyone’s journey is unique, the big curiosities and hurdles are pretty universal. Let’s tackle some of the most common questions to give you a clear path forward.

How Long Does It Realistically Take to Reach FI?

This is the million-dollar question, isn’t it? But the answer has surprisingly little to do with how much you earn. Your timeline to financial independence is almost entirely driven by one thing: your savings rate. The higher the percentage of your income you can sock away and invest, the faster you get there.

Just look at the numbers:

- Saving 10% of your income: You’re looking at about 51 years to reach FI. A traditional retirement path.

- Saving 25% of your income: The timeline shrinks dramatically to roughly 32 years.

- Saving 50% of your income: Now we’re talking. You could hit financial independence in just 17 years.

This powerful math shows that your habits matter far more than your salary. It’s not just about earning more; it’s about keeping more of what you earn.

Is the 4 Percent Safe Withdrawal Rate Still Reliable?

The 4% Rule has been the gold standard in retirement planning for decades, but it’s worth a closer look. It was developed back in the 90s using historical US market data. Today, some experts argue that with potentially lower future stock market returns and people living longer, a more conservative 3% to 3.5% withdrawal rate might be a safer bet.

So, is the 4% Rule dead? Not exactly. It remains a fantastic starting point for your calculations. Many in the FI community still aim for it but build in some wiggle room. This could mean having a flexible withdrawal strategy—pulling out less when the market is down—or planning to earn a little on the side with a passion project in early retirement.

Think of it as a guideline, not a law set in stone.

Financial independence isn’t a rigid formula; it’s a framework for freedom. Your strategy should be adaptable, allowing you to adjust to changing economic conditions and personal circumstances without derailing your long-term security.

Do I Need a High Income to Achieve Financial Independence?

Absolutely not. It’s one of the biggest myths out there. While a big paycheck can definitely accelerate things, your savings habits and discipline are what truly move the needle.

Consider this: someone earning $60,000 and saving 40% ($24,000 a year) will reach FI much faster than a person earning $150,000 who only saves 10% ($15,000 a year).

Why? The lower earner is not only investing more each year, but they’ve also learned to live comfortably on less. This means their target FI number is much lower to begin with, bringing the finish line that much closer. FI is open to almost anyone willing to be intentional with their money.

How Does Having a Family Change My FI Plan?

Starting a family definitely adds new layers to your financial independence plan, but it absolutely doesn’t derail it. Your strategy just needs to evolve to cover your new responsibilities and shared dreams.

Here are a few key adjustments you’ll likely make:

- Increased Expenses: Your FI number will probably need a bump to cover costs for your kids, from diapers to college.

- Risk Management: Things like life and disability insurance suddenly become non-negotiable. They’re there to protect your family’s future if something happens to you.

- Shared Goals: It’s critical to get on the same page with your partner about your financial values and what you’re working toward together.

- Legacy Planning: You might start thinking about goals beyond your own retirement, like helping your kids with their education or leaving an inheritance.

The numbers might get bigger and the stakes a little higher, but the core principles of FI—a high savings rate, smart investing, and mindful spending—are exactly the same.

Ready to stop guessing and start tracking your journey to financial independence? PopaDex gives you a clear, real-time view of your entire financial world, helping you monitor your net worth, track your progress toward your FI number, and make smarter decisions with your money. Take control of your financial future today at https://popadex.com.