Our Marketing Team at PopaDex

What is financial wellness? A quick, actionable guide

Financial wellness isn’t about being rich. It’s about feeling in control. It’s the quiet confidence you have over your day-to-day money and your long-term plans.

Think of it as your financial health. It’s the state where your money actively supports your well-being, letting you handle current needs, absorb surprises, and build toward your future without that constant knot of stress in your stomach.

Understanding Financial Wellness Beyond Your Bank Account

It’s a common mistake to mix up financial wellness with being wealthy. People often picture massive investment portfolios and a garage full of luxury cars. While those things can be a nice bonus, they aren’t the heart of the matter. True financial wellness is an internal feeling, not just an external number.

Let’s paint a picture. Imagine a high-flying executive who pulls in a huge salary but is drowning in stress, living paycheck-to-paycheck to keep up appearances, with nothing set aside for emergencies. Now, picture someone with a modest income who budgets carefully, has a growing emergency fund, and a clear vision for retirement. Who’s really better off? Despite having less on paper, the second person has achieved a far greater degree of financial wellness.

It’s About Control, Not Just Cash

At its core, financial wellness is all about empowerment. It’s knowing you have a plan and can stick to it. It’s the freedom that comes from knowing a surprise car repair won’t throw your entire life into chaos.

This is the kind of control that lets you make choices based on your values, not just what your bank account dictates at that moment. It’s a powerful antidote to money-related anxiety.

Unfortunately, that feeling of control seems to be slipping away for many. Recent global data shows a pretty worrying trend: as of 2025, only 29% of people feel hopeful about their financial future. That’s a massive drop from 60% in 2024. The fallout is real, with 19% of people saying money problems create tension in their relationships and many others linking financial stress to fatigue and poor sleep.

Financial wellness is the ability to live a life you value, without being constantly worried about money. It’s about having the freedom to make choices that allow you to enjoy life today while also building a secure future.

Getting to this state means shifting your mindset. It’s less about chasing a specific dollar amount and more about building smart, sustainable habits that support the life you want. This is exactly why gaining financial clarity is such a critical first step on the journey.

Financial Wellness vs. Being Rich at a Glance

To really drive the point home, let’s break down the difference between genuine financial wellness and the traditional idea of being “rich.” The comparison makes it clear that one is about security and peace of mind, while the other is often just about accumulation.

| Attribute | Financial Wellness | Being Rich |

|---|---|---|

| Primary Focus | Security, control, and peace of mind. | Accumulating a high net worth and assets. |

| Key Metric | Low financial stress and confidence in the future. | The dollar value of your assets. |

| Relationship with Money | Money is a tool to support life goals. | Money is the primary goal itself. |

| Accessibility | Achievable at any income level. | Typically associated with high income. |

As you can see, anyone, regardless of their income, can start working toward financial wellness today. It’s about the systems you build, not just the zeros in your account.

The Core Pillars of a Healthy Financial Life

To really get a handle on financial wellness, it helps to break it down. Think of it like a car—it needs an engine, fuel, and brakes all working together to run smoothly. Your financial life is no different; it relies on several interconnected parts to keep you moving forward. We can call these the seven pillars that hold up your entire financial structure.

When these pillars are strong and in balance, you’ve got a solid foundation for a life with less stress and more security. But if one is shaky, it can put the others at risk. For example, a mountain of debt can suck up all your income, leaving nothing for savings or investments. On the flip side, a healthy savings account can protect your investments when life throws you a curveball.

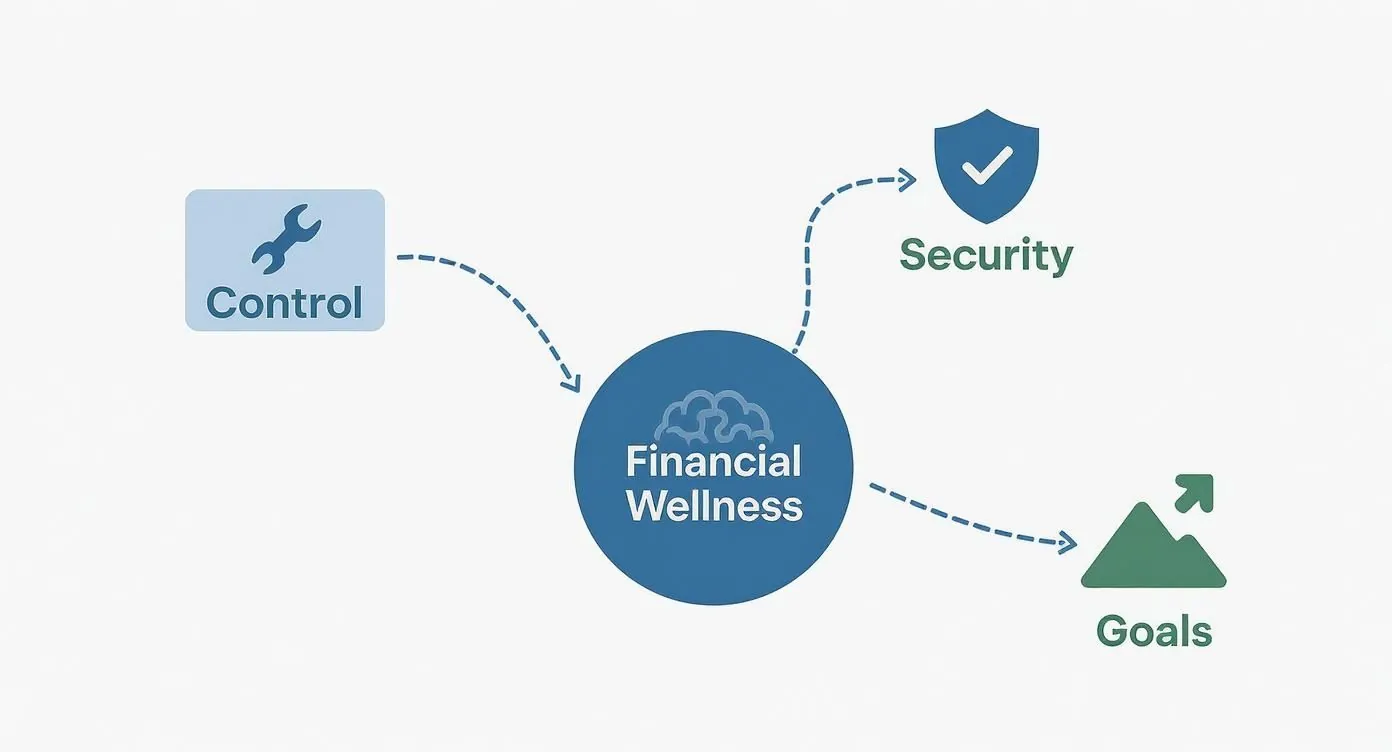

The image below gives you a bird’s-eye view of how these elements all feed into the main goals of financial wellness: getting control, feeling secure, and having the freedom to chase your biggest dreams.

This visual makes it clear that financial wellness is more than one number. It’s a state you achieve by managing all the different parts of your money to gain control today, build security for tomorrow, and ultimately reach your goals.

Income: The Engine of Your Finances

Everything starts with your income. It’s the engine that powers your entire financial life, whether it’s your salary, freelance gigs, side hustle profits, or any other cash flow. A strong engine goes beyond a big paycheck; it’s also about stability and the potential to grow.

But even the most powerful engine is useless if you don’t know how to drive. Plenty of high-earners are still buried in financial stress because they haven’t mastered the other pillars. The trick is to see your income not as a scorecard for your self-worth, but as the primary tool you have to build with.

Spending: Your Fuel Efficiency

If income is your engine, your spending habits are its fuel efficiency. It doesn’t matter how much gas you put in the tank if you’re burning through it wastefully. Mindful spending means pointing your money toward things that actually line up with your values and goals, making sure every dollar takes you further.

This isn’t about pinching pennies or cutting out all the fun. It’s about making conscious choices. A solid spending plan—what most people call a budget—plugs the leaks and frees up cash you can redirect to more powerful pillars, like saving and investing.

Savings: Your Emergency Toolkit

Life is full of surprises, and not all of them are good. Your savings are your emergency toolkit and spare tire. This pillar is your first line of defense against the unexpected, like a layoff, a surprise medical bill, or a leaky roof.

Most financial experts suggest having three to six months’ worth of essential living expenses tucked away in an account you can get to quickly.

An emergency fund is the buffer between you and life’s unexpected crises. Without it, a minor setback can quickly turn into a major financial disaster, forcing you into debt or derailing your long-term goals.

This fund buys you peace of mind. It lets you handle emergencies with a clear head instead of panic. It’s a non-negotiable part of genuine financial wellness.

Debt: Your Financial Brakes

Debt acts like the brakes on your financial journey. Sometimes you need it, but if you lean on it too hard, you’ll bring all your progress to a screeching halt. Not all debt is bad, of course. A mortgage or a student loan can be an investment in your future. High-interest credit card debt, however, can be incredibly destructive.

The goal is to manage debt strategically. That means steering clear of high-interest consumer debt, knowing the terms of any loans you have, and having a clear plan to pay them off. Uncontrolled debt is one of the biggest roadblocks to financial wellness because it eats up the income that should be building your future.

Investing: The Path to Your Destination

Investing is how you put your money to work to build real wealth over the long haul. If savings is your short-term toolkit, investing is the GPS and extra fuel you need to reach your long-term destinations, like retirement or financial independence.

It means taking calculated risks to get returns that beat inflation. The sooner you start, the better, because the power of compounding allows your money to grow exponentially over time. This pillar is what shifts you from just getting by to actively creating a more prosperous future.

Protection: Shielding Your Progress

Protection is all about managing risk and putting a shield around everything you’ve worked so hard to build. This pillar includes things like health, life, disability, home, and auto insurance. It’s the safety net that stops one catastrophic event from wiping you out completely.

Without the right protection, your savings and investments are exposed. Imagine a major illness without health insurance or a house fire without a homeowner’s policy. These events could erase decades of effort in an instant. Proper insurance is a critical, though often overlooked, part of a durable financial plan.

Long-Term Goals: Your Final Destination

Finally, your long-term goals are the “why” behind all this effort. This is your destination—the reason you’re on this financial journey in the first place. Whether you dream of retiring comfortably, paying for your kids’ education, or traveling the world, having clear goals gives you direction and keeps you motivated.

These seven pillars don’t exist in a vacuum. They’re deeply connected, working together as a dynamic system. Your income fuels your spending and saving. Your savings protect you from bad debt. Your investments grow your wealth, and insurance protects it all, giving you the confidence to go after your biggest goals. Understanding how these pieces fit together is the key to building a healthy and resilient financial life.

How to Measure Your Current Financial Health

Knowing the pillars of financial wellness is a great start, but to actually make progress, you have to know where you stand today. Think of it like a doctor checking your vitals before prescribing a treatment plan—you need to measure your financial vitals to build a strategy that works. This isn’t about judging your past decisions; it’s about getting crystal clear so you can move forward with confidence.

The most powerful thing you can do is turn vague feelings into hard numbers. It’s the difference between saying, “I feel like I’m not saving enough,” and knowing, “My savings rate is 8%, and my goal is to get it to 15%.” That simple shift gives you a real target to aim for.

Conducting Your Financial Wellness Checkup

A financial checkup just means looking at a few key numbers that give you a snapshot of your current situation. These are the dashboard lights for your money—they tell you what’s running smoothly and what needs a little attention.

Here are the essential numbers to get a handle on:

-

Net Worth: This is the ultimate scorecard. It’s the total value of everything you own (your assets) minus everything you owe (your liabilities). A positive and growing net worth is one of the strongest signs of financial progress. To get the full picture, you can dig into how to calculate net worth and start tracking this crucial metric.

-

Savings Rate: This tells you exactly what percentage of your after-tax income you’re putting away. The higher the rate, the faster you build your emergency fund and investment portfolio. The formula is simple: (Total Savings / After-Tax Income) x 100.

-

Debt-to-Income (DTI) Ratio: Your DTI compares your monthly debt payments to your gross monthly income. Lenders use it to see how risky it is to lend you money, but it’s an excellent personal gauge, too. A DTI below 36% is generally considered a healthy zone.

Once you have these figures, you’ve established your baseline. This is your “You Are Here” marker on your financial map.

Key Ratios and What They Reveal

Beyond the big three, a few other numbers can give you deeper insights into where your money is really going. These ratios help you diagnose specific areas that might be holding you back.

- Housing Expense Ratio: What slice of your take-home pay goes to your mortgage or rent? Keeping this under 30% is a good rule of thumb that frees up cash for other important goals.

- Emergency Fund Coverage: If you lost your job tomorrow, how many months of essential living expenses could you cover? Aiming for 3 to 6 months gives you a solid safety net.

- Retirement Savings Progress: Are you on track? A quick check is to see if you have at least 1x your annual salary saved by age 30, and 3x by age 40.

Your financial numbers are not a reflection of your self-worth. They are simply data points—neutral information that you can use to build a stronger, more secure future.

Pulling all this information together can feel like a chore, but modern tools make it incredibly simple. Instead of bouncing between spreadsheets and bank logins, a dedicated tracker can give you a single, clear view.

Here’s an example of what a financial dashboard like PopaDex looks like, bringing all your accounts into one easy-to-read overview.

This kind of consolidated view automates the hard part—the measurement—so you can focus your energy on making improvements instead of just collecting data. Once you have this baseline, you’re ready to create a plan that fits your life.

Actionable Financial Plans for Different Lifestyles

Financial wellness isn’t a one-size-fits-all journey. Your life stage, career, and personal circumstances create a unique financial map, and a cookie-cutter plan just won’t cut it. Juggling student loans as a young professional is a world away from managing multiple currencies as an expat or navigating the feast-or-famine cycle of the gig economy.

The real key is building a strategy that fits your reality. When you understand the specific challenges and opportunities your lifestyle presents, you can create an actionable plan that leads to genuine financial control and, more importantly, peace of mind.

It’s also important to acknowledge that everyone starts from a different place. In the United States, for instance, there are significant gaps in financial wellness tied to income and gender. The median financial wellness score for women is 64, while for men, it’s 71. Similarly, employees earning under $40,000 have a median score of 55, compared to 74 for those earning over $100,000. These numbers highlight why personalized financial strategies are so critical.

Plans for Young Professionals

If you’re just starting your career, the financial world can feel like a balancing act. You’re trying to pay off the past (hello, student loans) while building for the future (hello, first investments). The absolute priority is to lay a rock-solid foundation.

Your financial plan should zero in on three core areas:

- Aggressive Debt Repayment: High-interest debt from credit cards or private student loans is like an anchor dragging you down. Make it your mission to pay these off using a method that works for you, like the avalanche (tackling the highest interest rate first) or snowball (clearing the smallest balance first for a quick win).

- Automating Savings and Investments: Put your wealth-building on autopilot. Set up automatic transfers to a high-yield savings account for your emergency fund. And don’t leave free money on the table—contribute to your 401(k), especially if your employer offers a match.

- Building Credit Wisely: Your credit score is one of your most powerful financial tools. Use a credit card for small, planned purchases you can afford, and always pay the balance in full each month. It’s the simplest way to build a positive history.

Strategies for Expats and Global Citizens

Living and working abroad adds a whole new layer of financial complexity. Suddenly, you’re not just managing a budget; you’re navigating international tax laws, currency swings, and banks that don’t talk to each other.

An expat’s financial plan has to be both robust and flexible.

Financial success for an expat means creating a unified strategy from a set of disconnected international accounts. It requires careful planning around taxes, currency risk, and long-term goals that span multiple countries.

Here are the key action items for any expat:

- Consolidate Your Financial View: You can’t manage what you can’t see. Use a multi-currency net worth tracker like PopaDex to get a single, clear picture of all your global assets and liabilities. This clarity is the first step to making smart decisions.

- Understand Your Tax Obligations: You might owe taxes in your home country and your country of residence. This is not a DIY situation. Investing in a consultation with a tax pro who specializes in expat finances can save you massive headaches and money down the road.

- Manage Currency Risk: Don’t underestimate how much exchange rate shifts can affect your savings. Look into hedging strategies or simply hold funds in different currencies to soften the impact of market volatility.

Guidance for Gig Economy Workers

Freelancers, contractors, and other gig workers trade the security of a 9-to-5 for flexibility and freedom. But that freedom comes with big responsibilities: wildly inconsistent income and managing your own benefits.

For a gig worker, a solid financial plan is more than nice to have—it’s your safety net. The first step is to get a handle on your cash flow, which we cover in our guide to financial planning for freelancers.

From there, your strategy needs to include:

- Creating a “Paycheck” System: Tame your variable income by opening separate bank accounts for business income, expenses, taxes, and your personal salary. Then, pay yourself a consistent “salary” from your business account. This brings predictability to an unpredictable world.

- Prioritizing Retirement Savings: Without an employer 401(k), you’re the boss of your retirement. Open a retirement account designed for the self-employed, like a Solo 401(k) or a SEP IRA, and fund it relentlessly.

- Setting Clear Investment Goals: A clear vision keeps you moving forward. To formalize your approach, consider drafting an Investment Policy Statement. Using an Investment Policy Statement template can help you document your goals and risk tolerance, ensuring your strategy always aligns with what you truly want to achieve.

The Money Myths Holding You Back

Your mindset is one of the most powerful tools in your financial toolkit. But it can also be your biggest obstacle.

Certain widely-held beliefs about money act like invisible walls, stopping you from making progress before you even start. Let’s tear those walls down. Dismantling these myths is a critical first step toward real financial wellness.

So many people feel stuck because they’ve internalized ideas that are just plain wrong. These misconceptions create unnecessary fear and paralysis, making money management feel like some exclusive club you weren’t invited to. By calling out these outdated beliefs, you clear the path for confident, proactive decisions.

Myth 1: You Need a High Salary to Be Financially Well

This is probably the most damaging myth out there. It’s easy to look at someone with a big paycheck and assume they have it all figured out. But financial wellness isn’t about how much you earn—it’s about how well you manage what you have.

Someone earning a modest income who budgets wisely, dodges high-interest debt, and consistently saves for the future is in far better financial shape than a high-earner living paycheck-to-paycheck. It’s your habits, not your income bracket, that truly matter. Control and planning are the real drivers of wellness, and anyone can learn those skills.

Financial wellness is about the gap between your income and your expenses, not the size of your paycheck. A small, positive gap managed consistently over time builds more security than a large income with no gap at all.

Myth 2: Investing Is Only for Stock Market Experts

The idea that you need to be some Wall Street wizard to invest is a stubborn and intimidating myth. It conjures images of complex charts and risky bets, scaring countless people away from one of the most powerful wealth-building tools we have.

The truth is much simpler. Today, investing is more accessible than ever before. Here’s why this myth is totally outdated:

- Automation: Tools like robo-advisors and target-date funds do the heavy lifting for you. They build a diversified portfolio based on your goals and risk tolerance—no stock-picking required.

- Low-Cost Options: You don’t need a fortune to start. With low-cost index funds and ETFs, you can own a small piece of the entire market for just a few dollars.

- Simplicity Wins: Honestly, the most effective long-term strategy is often the simplest one: consistently invest in a broad market index fund and let compound growth work its magic.

You don’t need to predict the market’s next move. You just need to show up and participate consistently.

Myth 3: Budgeting Is All About Restriction

Let’s be real, the word “budget” makes most people groan. It sounds like a financial diet where you have to cut out everything fun. This completely misses the point.

A budget isn’t about restriction; it’s about permission.

Think of it this way: a good budget is a plan that gives you the freedom to spend money on the things you actually value, completely guilt-free. It’s a tool for being intentional. By telling your money where to go, you make sure it aligns with your priorities, whether that’s saving for a house, planning an epic vacation, or just enjoying dinner out. It puts you in the driver’s seat, turning chaotic spending into conscious choices that support your life.

Building Your Resilient Financial Future Starting Today

Knowing what financial wellness is gives you the map, but the real adventure begins the moment you take that first step. Think of it less like a finish line you cross and more like a continuous journey of learning, tweaking, and growing. The whole point is to build a financial life that can handle life’s curveballs while still supporting your biggest dreams.

You don’t need to turn your entire financial world upside down overnight. A simple, practical move could be to finally organize business receipts for ultimate peace of mind—it’s a small win that removes a common source of money stress. It’s these small, consistent actions that build incredible momentum over time.

And the good news? Getting your hands on the right tools has never been easier. Financial inclusion has taken massive leaps globally, with 79% of adults expected to have a financial account by 2025. This explosion, fueled by mobile money and digital banking, proves just how powerful accessible tools are in building real security. You can dig into more of these global financial trends from The World Bank.

Your Simple Three-Step Action Plan

Feeling empowered is a great start, but taking action is what really counts. Here’s a straightforward plan to start building that resilient future right now:

-

Assess Your Current Standing: Use the metrics from this guide to get a brutally honest snapshot of where you are today. Know your numbers—your net worth, your savings rate, your debt-to-income ratio. This isn’t about judgment; it’s about drawing a clear “You Are Here” mark on your map.

-

Choose One Pillar to Improve: Don’t try to fix everything at once. You’ll burn out. Instead, pick just one of the seven financial pillars—say, savings or debt—and give it your full attention for the next 90 days. Maybe that means building a one-month emergency fund or laser-focusing on wiping out a high-interest credit card.

-

Track Your Progress: This part is critical. Use a tool like PopaDex to see your progress without having to manually crunch the numbers. Watching your net worth climb or your debt shrink is the fuel you need to stay motivated and turn those small wins into habits that last a lifetime.

You now have the knowledge and a clear path forward. The journey to financial wellness truly starts with a single, deliberate step. Go on, take it.

Got Questions About Financial Wellness? Let’s Talk.

When you’re figuring out your money, questions are a good thing. They mean you’re engaged and ready to make a change. Here are some straightforward answers to the questions we hear most often.

How Long Does It Take to Achieve Financial Wellness?

The honest answer? It’s a journey, not a destination. Think of it less like a race with a finish line and more like keeping up with your physical fitness—it’s an ongoing practice.

You’ll hit some amazing milestones quickly. You might build up a small emergency fund in just a few months, which is a huge win. Other goals, like saving for retirement, are a marathon that will take years. The real progress comes from consistent, positive habits that you build over time.

What’s the Most Important First Step to Take?

Forget everything else for a moment and just track your spending. Seriously. Before you can make a budget that works, save effectively, or start investing, you absolutely have to know where your money is going right now. It’s the bedrock of everything else.

This one habit gives you the clarity you need to make every other decision. It puts you back in the driver’s seat of your cash flow and instantly shows you where you can redirect money toward the things that actually matter to you.

The first step isn’t about some massive, intimidating change. It’s simply about awareness. Once you see your starting point on the map, you can finally figure out how to get where you want to go.

Can I Improve My Financial Wellness on a Low Income?

Absolutely, and don’t let anyone tell you otherwise. Financial wellness is about how well you manage what you have, not how much you have in the first place. It’s a game of strategy, and it’s winnable at any income level.

When your income is tight, you just have to be more strategic. Focus on the moves that give you the biggest bang for your buck. This means attacking high-interest debt with a vengeance, setting up automatic transfers for even small amounts of savings, and soaking up all the free financial knowledge you can find. Every smart little decision you make adds up to huge progress down the road.

Ready to get that clarity and start building real financial wellness? With PopaDex, you can finally see your entire financial world in one place, track your progress without the headache, and make decisions with confidence. Start your free trial today and take control of your financial future.