Our Marketing Team at PopaDex

What is Real Estate Equity: A Guide to Growing Your Home's Value

When people talk about building wealth through real estate, what they’re really talking about is building equity. In the simplest terms, equity is the slice of your property that you actually own, free and clear.

Think of it as the difference between what your home is worth today and the amount you still have left on your mortgage. As you pay down your loan and your property’s value (hopefully) goes up, your equity grows right along with it.

Understanding Your Home’s Financial Footprint

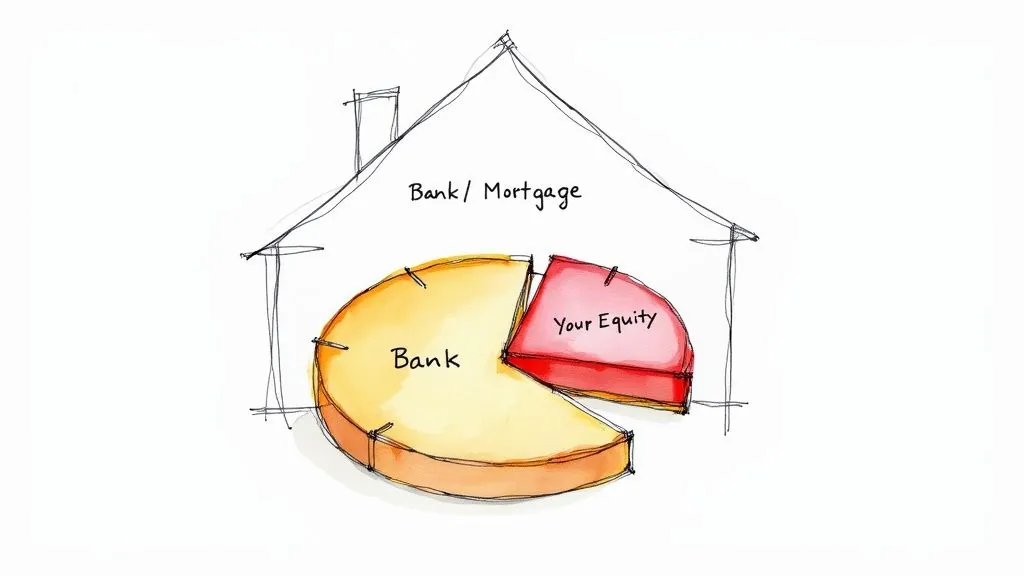

Imagine your home is a pie. When you first buy it, the bank owns almost the entire pie, and your down payment represents your tiny starting slice. That slice is your equity.

But this is more than some abstract number on a spreadsheet; it’s a dynamic and powerful financial tool. Every single mortgage payment you make is like buying a little more of the pie back from the bank. Over time, your slice gets bigger. If the local housing market heats up and your property’s value increases, the entire pie grows, making your slice even more valuable.

The Two Pillars of Equity Growth

So, how does this all happen? Your equity builds up in two main ways, which is why homeownership is such a cornerstone of wealth creation for so many people.

- Paying Down Your Loan: Each month, part of your mortgage payment goes toward interest, and the other part—the principal—pays down your actual loan balance. That principal payment directly increases your equity.

- Market Appreciation: This is the magic that happens without you lifting a finger. As your home’s value increases due to inflation, demand, or neighborhood improvements, your equity gets a passive boost.

For many homeowners, the equity in their home becomes the single largest component of their overall financial picture. To see how it all fits together, check out our guide that explains what net worth means and how to calculate it.

It’s also worth noting that while home equity has historically been a reliable path to financial security, it’s not immune to market cycles. The 2008 financial crisis, for instance, saw U.S. home equity take a massive hit as property values fell. You can dig deeper into real estate trends on Nuveen.com. How that equity is legally divided can also get complicated, especially in states with community property laws, which is another key factor to understand.

How to Calculate Your Real Estate Equity

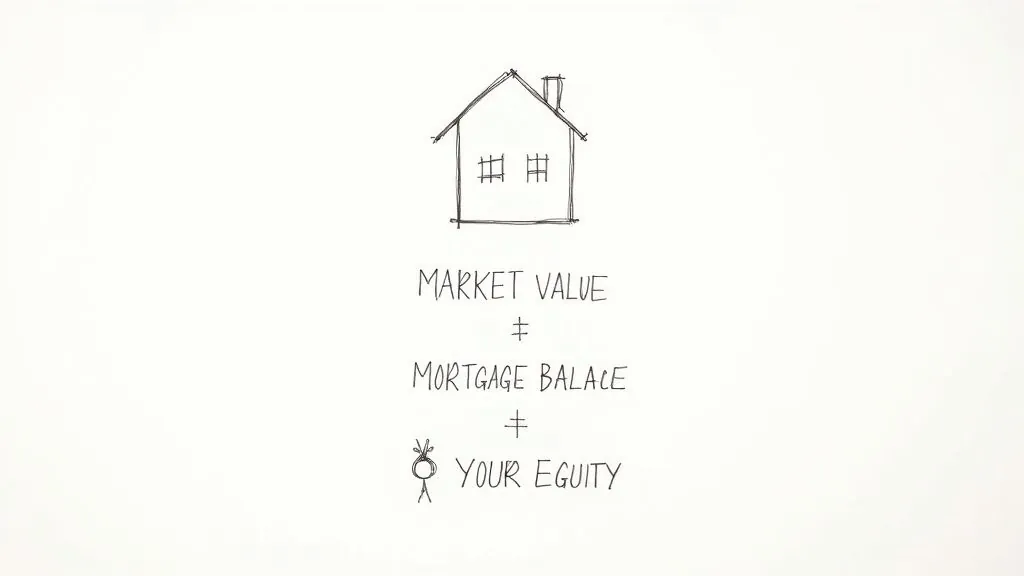

Figuring out your home equity doesn’t require a complicated financial degree. In fact, it’s surprisingly simple. The calculation at its core is just a straightforward formula that reveals how much of your property you actually own, free and clear.

The Equity Formula: Current Market Value – Remaining Mortgage Balance = Your Equity

This simple equation shows that your equity isn’t a fixed number. It’s dynamic, constantly changing as you chip away at your mortgage and as the local real estate market ebbs and flows. To get an accurate snapshot, you just need to find the two key numbers in this formula.

Finding Your Two Key Numbers

First up is your property’s current market value. This isn’t what you paid for the house years ago, but what a buyer would likely pay for it today. The second piece is your remaining mortgage balance—the total principal you still owe the bank.

- Determining Market Value: Getting an accurate value is crucial. You’ve got a few options here. Online valuation tools can give you a quick ballpark figure, but for the most reliable number, a formal appraisal from a licensed professional is the gold standard. A great DIY approach is to check the recent sale prices of similar homes in your neighborhood.

- Finding Your Mortgage Balance: This part is easy. Your lender makes this number readily available on your latest mortgage statement, which you can usually find in your mailbox or on their online portal. Just be sure you’re looking at the outstanding principal, not a figure that includes future interest. For a deep dive into how each payment reduces your principal, check out PopaDex’s guide on using an amortization calculator for your mortgage.

Real Estate Equity Examples in Action

Let’s run the numbers for a couple of common homeowner scenarios to see how this plays out in the real world.

Example 1: The Recent Homebuyer Meet Sarah. She bought her first home two years ago.

- Current Market Value: $350,000

- Remaining Mortgage Balance: $315,000

- Sarah’s Equity: $350,000 - $315,000 = $35,000

Sarah’s equity is just starting out, but it’s a solid foundation that will grow with every single mortgage payment she makes.

Example 2: The Long-Term Homeowner Now let’s look at David. He’s owned his home for 15 years, and his diligence has paid off through both consistent payments and a rising market.

- Current Market Value: $600,000

- Remaining Mortgage Balance: $120,000

- David’s Equity: $600,000 - $120,000 = $480,000

You can see how powerful time and consistency are. David’s steady payments and property appreciation have turned his home into a significant financial asset. By checking your own equity regularly, you get a clear, motivating picture of your financial health and the wealth you’re building over time.

Proven Strategies to Increase Your Home Equity

Building equity in your home isn’t magic—it’s a hands-on process driven by two key engines: paying down what you owe and making your property worth more. One happens slowly over time, but the other puts you firmly in the driver’s seat of your financial future.

Pay Down Your Mortgage Faster

The most direct way to build equity is by shrinking your loan principal. Every mortgage payment you make is a small victory, converting a piece of what you owe the bank into wealth that you own outright.

But you don’t have to stick to the standard schedule. You can put your foot on the gas. Making bi-weekly payments or even just one extra payment a year can carve years off your loan term and save you thousands in interest. The result? You build equity much, much faster.

Boost Your Property’s Value

The second engine is all about increasing your home’s market value. Sometimes, this happens on its own when the market is hot—a rising tide lifts all boats, after all. But you can also take matters into your own hands and actively make your property more desirable.

This is where strategic home improvements come in. To give your equity a real boost, you need to know how to increase home value before selling by focusing on renovations with a high return on investment (ROI).

Here are a few proven winners:

- Kitchen Remodels: A modern, functional kitchen is almost always at the top of a homebuyer’s list. It can dramatically increase your home’s appeal and its final sale price.

- Bathroom Upgrades: You don’t have to gut the whole room. Even small updates like new fixtures, a modern vanity, or fresh tile can deliver a surprisingly high ROI.

- Curb Appeal: First impressions are everything. Simple, cost-effective projects like landscaping, a new front door, or a fresh coat of exterior paint can add serious value.

A strong real estate market can be the most powerful force for passive equity growth. Staying informed about market trends helps you understand the bigger picture influencing your home’s worth.

This is especially true when the market is bouncing back. For example, the global private real estate market has seen values climb for five straight quarters. Transaction volumes hit roughly $739 billion over the last year—a 19% jump from the year before—which signals strong investor confidence and rising equity across the board.

By combining smart, value-adding improvements with a strategy for accelerated mortgage payments, you create a powerful, two-pronged approach. You’re no longer just living in a house; you’re actively turning it into a more valuable financial asset. This proactive mindset means you’re not just waiting for the market to do the work—you’re making your own luck.

The table below breaks down the key strategies you can use, separating the things you can control from the market forces you can’t.

Methods For Building Real Estate Equity

| Strategy Type | Method | Description | Control Level |

|---|---|---|---|

| Active | Accelerated Mortgage Payments | Making extra or bi-weekly payments to reduce the principal faster. | High |

| Active | Strategic Renovations | Making targeted improvements (kitchen, bath, curb appeal) to boost market value. | High |

| Passive | Market Appreciation | General increase in property values due to economic growth and neighborhood demand. | Low |

| Passive | Inflation | Over time, inflation can increase the nominal value of your property while the real value of your fixed-rate mortgage decreases. | Low |

Ultimately, a balanced approach works best. Actively manage what you can—your payments and your property’s condition—while staying aware of the passive market forces that are working in your favor.

Putting Your Equity to Work: Financial Strategies

Once you’ve built a meaningful amount of equity, it stops being just a number on paper. It becomes a powerful and flexible financial tool you can use to achieve other life goals, from funding major projects to consolidating debt.

Tapping into your equity simply means borrowing against the value you’ve built in your home. This strategy essentially transforms your illiquid home value into accessible cash. But make no mistake, it’s a big financial decision that adds to your debt and uses your home as collateral. Understanding the primary methods for accessing it is the first step toward making a smart choice.

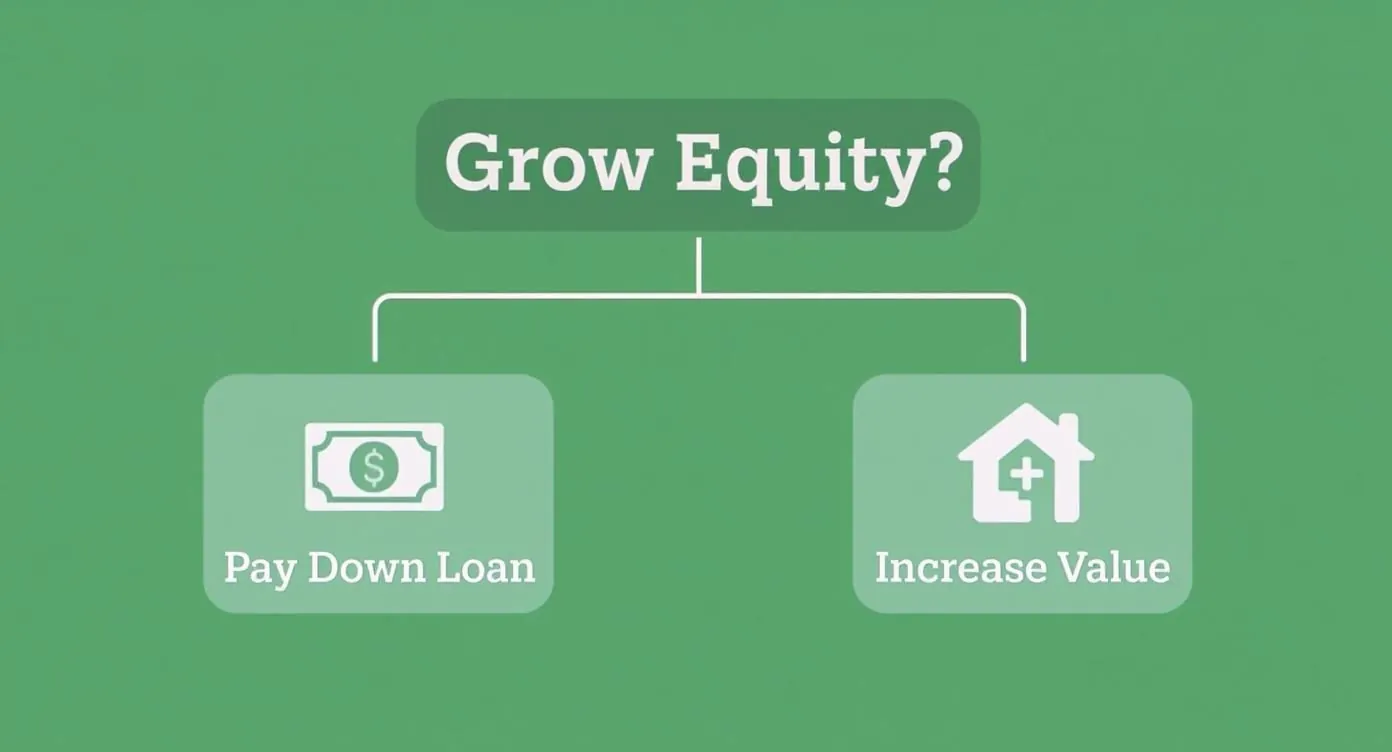

The following visual provides a simple decision tree to show the two core paths to growing the equity you can later use.

This visual boils it down to two fundamental actions: increasing your home’s value or paying down your loan. Both build the foundation for these financial strategies.

Comparing Your Options for Accessing Equity

There are three common financial products designed for homeowners looking to put their equity to use. Each one functions differently and is suited for specific needs. Let’s break them down.

- Home Equity Loan (HEL): Think of this as a traditional second mortgage. You borrow a fixed lump sum of money and pay it back over a set term with a fixed interest rate. This option is ideal for large, one-time expenses where you know the exact cost upfront, like a major home renovation or covering college tuition.

- Home Equity Line of Credit (HELOC): A HELOC works more like a credit card. Instead of a lump sum, you get a revolving line of credit you can draw from as needed during a specific “draw period.” With variable interest rates, it offers great flexibility for ongoing projects or as a ready-to-go emergency fund.

- Cash-Out Refinance: With this option, you replace your current mortgage with a new, larger one. You then receive the difference between the two loan amounts in cash. This is often a smart move when interest rates are low, as it lets you access equity while potentially securing a better rate on your primary mortgage.

Real estate equity is more than just personal wealth; it’s a vital part of the broader economy. The ability of homeowners to refinance or pay down loans is directly linked to their equity stake.

This connection is massive. In a single recent year, nearly $500 billion in loans on real estate assets matured, showing just how intertwined individual equity positions are with large-scale financial markets.

Choosing the right option depends entirely on your financial goals. A HEL is best for predictable, fixed costs, while a HELOC excels with variable expenses. A cash-out refinance makes sense if you can also improve your primary mortgage terms. For those looking to use their equity as a springboard, our guide explains how to start investing money to build wealth beyond just real estate.

Smart Safeguards Before You Tap Your Equity

Accessing your home equity can feel like you’ve unlocked a financial superpower. Suddenly, you have a powerful tool for big projects or investments. But it’s a decision that demands serious thought.

Tapping into your equity isn’t just getting a loan; it’s borrowing against your most significant asset—your home. This means your property is on the line as collateral, securing the new debt.

The biggest risk here is foreclosure. It’s a harsh reality, but if life throws you a curveball—a sudden job loss or a medical emergency—and you can’t make the payments on your home equity loan or HELOC, the lender could take your home. That’s why having a rock-solid repayment plan isn’t just a good idea, it’s essential.

Navigating Market and Financial Risks

Beyond the immediate risk of foreclosure, there are other forces at play that can affect your financial well-being when you borrow against your equity. Getting a handle on these will help you prepare for the unexpected and protect what you’ve built.

Two major factors to keep your eye on are market stability and the true cost of borrowing:

- Housing Market Downturns: Real estate values are not a one-way street. If the market takes a nosedive after you’ve borrowed, you could find yourself with negative equity—more commonly known as being “underwater.” This is a tricky spot where you owe more than your home is worth, making it nearly impossible to sell or refinance.

- Hidden Costs and Fees: Accessing your equity is never free. Be prepared for closing costs, appraisal fees, and of course, the ongoing interest that adds up over the life of the loan. With a variable-rate product like a HELOC, a sudden spike in interest rates can dramatically inflate your monthly payments and put a serious strain on your budget.

Before you sign on the dotted line, make sure you have a clear, realistic plan to pay back every penny. Your home’s value should be a source of security, not a source of stress.

Building a Financial Safety Net

The smartest way to use your real estate equity is to be proactive and strategic. Your best defense is maintaining a healthy financial cushion between what you owe and what your home is actually worth. In lender-speak, this is called the loan-to-value (LTV) ratio.

Most financial experts will tell you to keep your total LTV below 80%. This means that your original mortgage balance plus your new equity loan shouldn’t add up to more than 80% of your home’s current appraised value.

By leaving at least 20% of your equity untouched, you create a buffer. This buffer protects you from market swings and keeps a nice chunk of your hard-earned wealth safe and sound. It’s a disciplined approach that lets you use your equity without gambling with your financial future.

Your Top Equity Questions, Answered

Even after getting the hang of real estate equity, it’s totally normal for a few questions to pop up. Let’s walk through some of the most common ones to make sure you’re feeling confident and clear about your home investment.

How Quickly Will My Equity Grow?

Think of your equity growth like a snowball rolling downhill—it starts slow and picks up speed over time. This is all thanks to mortgage amortization. In the first few years of your loan, it feels like most of your payment is just feeding the bank’s interest pile.

But as you chip away at that principal balance, the tables start to turn. A bigger and bigger slice of your monthly payment goes toward your actual loan, causing your equity to build much faster in the later years of your mortgage. On top of that, market appreciation can give your equity a nice (though unpredictable) boost at any point.

Is My Equity the Same as My Profit When I Sell?

Not quite. While your equity is the starting point, it’s not the final number you’ll walk away with. Before you can count your cash, you have to subtract all the costs that come with selling a house.

These expenses can take a serious bite out of your proceeds. Typically, they include:

- Real estate agent commissions, which usually land somewhere between 5% to 6% of the home’s sale price.

- Closing costs, a mix of things like title insurance, transfer taxes, and attorney fees.

- Staging and repair costs to get your home looking its best for potential buyers.

Whatever is left after you’ve paid off your mortgage and all these selling costs—that’s your actual profit.

Can My Home Equity Be Negative?

Yes, unfortunately, it can. This happens when your mortgage balance is higher than what your home is currently worth on the market. The common term for this is being “underwater” on your mortgage.

Being underwater can make it incredibly difficult to sell or refinance. You’d essentially have to bring your own money to the closing table to cover the difference. It’s a risk that often pops up during sharp downturns in the housing market.

What Is a Good Loan-to-Value Ratio?

Lenders live by the loan-to-value (LTV) ratio; it’s their way of measuring risk. A lower LTV is always better in their eyes because it means you have more “skin in the game.”

Most financial pros suggest keeping your total LTV at 80% or less. This means your total mortgage debt shouldn’t be more than 80% of your home’s value, giving you a healthy 20% equity cushion for peace of mind.

Keeping tabs on your home’s value, mortgage balance, and overall equity is step one toward making smart financial moves. PopaDex makes this effortless by pulling everything into one clear, simple view. You can see your progress at a glance and make informed decisions about your most valuable asset. Get started today at https://popadex.com.