Our Marketing Team at PopaDex

best asset allocation for retirees: 8 proven strategies for secure income

Retirement marks a significant shift not just in lifestyle, but in financial strategy. The primary goal transitions from aggressive wealth accumulation to careful wealth preservation and income distribution. The central question becomes: what is the best asset allocation for retirees to ensure their savings last a lifetime while effectively combating inflation and market volatility? The answer isn’t a single, one-size-fits-all portfolio; it’s about finding the right strategic framework that aligns with your specific financial goals, personal risk tolerance, and retirement timeline.

This comprehensive guide moves beyond generic advice to provide a detailed roundup of proven strategies. We will dissect eight distinct asset allocation models, from time-tested approaches like the Bucket Strategy to more dynamic frameworks like the All-Weather portfolio. For each method, we will explore its core philosophy, ideal use case, and potential drawbacks, giving you a clear picture of how it might function in the real world. Beyond traditional financial instruments, understanding how physical assets like real estate fit into your plan, distinguishing between a vacation home vs. investment property, is also key to a holistic approach.

We’ll equip you with actionable steps and concrete examples to help you construct a resilient portfolio tailored to your needs. You will learn how to balance growth potential with capital protection, manage sequence-of-returns risk, and create a reliable income stream. Our goal is to empower you with the knowledge to build a financial foundation that supports the retirement you have worked so hard to achieve.

1. The 4% Rule (Safe Withdrawal Rate Strategy)

While not an asset allocation model itself, the 4% Rule is a foundational withdrawal strategy that profoundly influences how retirees structure their portfolios. Pioneered by financial planner William Bengen in 1994, it provides a simple yet powerful framework for turning your nest egg into a reliable income stream. This rule is a cornerstone of retirement planning because it directly addresses the central question: “How much can I safely spend each year without running out of money?”

The strategy suggests that you can withdraw 4% of your portfolio’s value in your first year of retirement. In subsequent years, you adjust that initial dollar amount for inflation to maintain your purchasing power. For instance, a retiree with a $1 million portfolio would withdraw $40,000 in their first year. If inflation is 3% that year, the next year’s withdrawal would be $41,200 ($40,000 x 1.03), regardless of the portfolio’s performance.

How It Shapes Asset Allocation

The 4% Rule’s success hinges on a portfolio that can both generate income and grow over the long term, making it a critical component of finding the best asset allocation for retirees. Bengen’s original research was based on a portfolio with a minimum of 50% in stocks, often a 50/50 or 60/40 split between stocks and bonds. This balance is designed to provide enough growth to outpace inflation and withdrawals, while the bond portion offers stability during market downturns.

Key Insight: The 4% Rule goes beyond spending; it’s a mandate for a growth-oriented, yet balanced, portfolio. A portfolio that is too conservative may fail to keep up with inflation-adjusted withdrawals, while one that is too aggressive risks catastrophic losses early in retirement (sequence-of-returns risk).

Practical Implementation Tips

To apply this strategy effectively, consider the following actions:

- Establish a Baseline: Your initial withdrawal sets the stage for all future withdrawals.

- Be Flexible: During severe market downturns, consider forgoing the inflation adjustment or even reducing your withdrawal temporarily to preserve capital.

- Rebalance Annually: Stick to your target asset allocation (e.g., 60% stocks, 40% bonds) by rebalancing at least once a year. This forces you to sell high and buy low.

- Maintain Cash Reserves: Keep one to two years’ worth of living expenses in cash or cash equivalents. This buffer prevents you from having to sell assets at a loss during a market crash.

This time-tested rule provides a disciplined approach, and understanding its mechanics is vital. For a more in-depth analysis, you can learn more about the safe withdrawal rate for retirement on PopaDex.

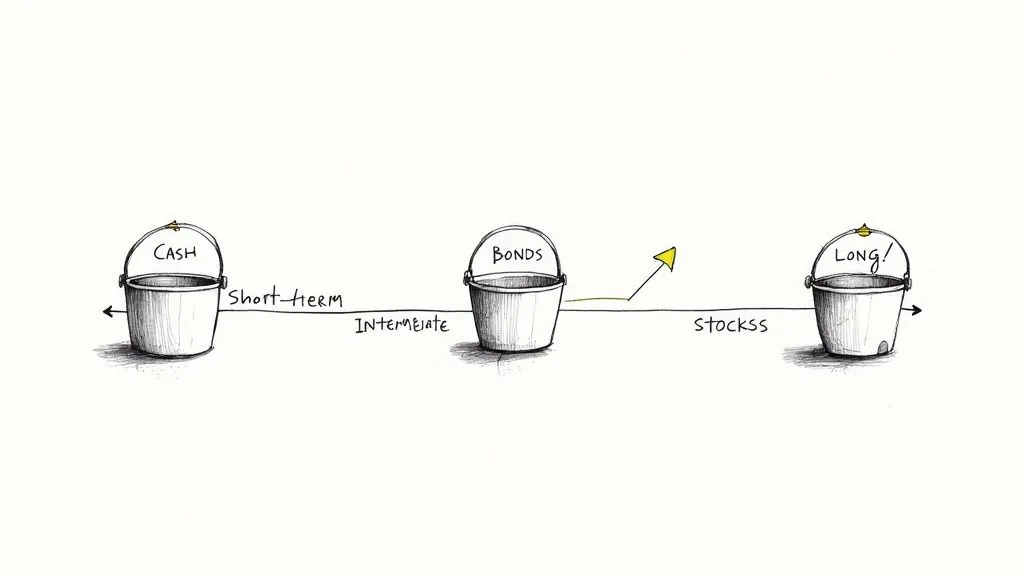

2. The Bucket Strategy (Time-Segmented Approach)

The Bucket Strategy is an intuitive and psychologically powerful method for organizing retirement assets. Popularized by financial planner Harold Evensky, it segments your portfolio into distinct “buckets,” each designed to cover expenses over a specific time horizon. This approach directly tackles a retiree’s greatest fears: running out of money and being forced to sell assets during a market crash. By creating a mental and practical separation, it helps you manage risk and stay invested for long-term growth.

The typical structure involves three buckets: a short-term bucket for immediate needs, an intermediate bucket for midterm expenses, and a long-term bucket for growth. For example, a retiree with a $1 million portfolio might put one to two years of expenses, say $80,000, into a cash bucket (Bucket 1). The next five to seven years of expenses, perhaps $320,000, would go into a conservative mix of bonds and CDs (Bucket 2). The remaining $600,000 would be invested in a diversified stock portfolio for long-term growth (Bucket 3).

How It Shapes Asset Allocation

The Bucket Strategy provides a clear framework for determining the best asset allocation for retirees by linking investments directly to spending needs. Instead of a single, blended portfolio, you create sub-portfolios with distinct risk profiles. The short-term bucket is ultra-conservative, the intermediate bucket is balanced, and the long-term bucket is aggressive. This time-segmented allocation insulates your immediate income needs from market volatility, allowing you to ride out downturns without panic selling.

Key Insight: The primary benefit of the Bucket Strategy is behavioral. Knowing your next few years of expenses are secure in a cash bucket provides the confidence to keep your long-term assets invested for growth, even when markets are turbulent.

Practical Implementation Tips

To effectively implement a bucket system, consider these steps:

- Define Your Buckets: Clearly establish the time horizon and asset allocation for each bucket (e.g., Bucket 1: 1-2 years in cash; Bucket 2: 3-10 years in bonds/balanced funds; Bucket 3: 10+ years in stocks).

- Create Refill Rules: Establish a clear process for refilling Bucket 1. This is typically done by selling appreciated assets from Bucket 2 or Bucket 3 during bull markets.

- Keep Bucket 1 Safe: Hold your short-term funds in high-yield savings accounts, money market funds, or CDs to ensure liquidity and capital preservation.

- Automate When Possible: Set up automatic transfers to move funds from your investment buckets to your cash bucket on a regular schedule, such as annually or semi-annually.

This method transforms a complex portfolio into a manageable system, giving you a clear plan for generating income throughout retirement.

3. Target-Date Fund Strategy

The Target-Date Fund (TDF) strategy offers a “set-it-and-forget-it” approach to asset allocation, making it one of the most popular choices in employer-sponsored retirement plans like 401(k)s. These funds automatically adjust their asset mix over time, becoming more conservative as a specific target retirement year approaches. This automated “glide path” handles the complex rebalancing decisions for you, aligning the portfolio’s risk level with your investment timeline.

Initially, a TDF for a younger investor will be heavily weighted in stocks for maximum growth potential. For example, a Vanguard Target Retirement 2050 Fund might hold over 85% in stocks. As the 2050 target date nears, the fund’s managers systematically sell stocks and buy more bonds and cash equivalents to reduce risk and preserve capital. This hands-off model addresses the core challenge of shifting from an accumulation phase to a preservation phase without requiring active management from the retiree.

How It Shapes Asset Allocation

The core principle of a Target-Date Fund is its professionally managed glide path, which dictates the best asset allocation for retirees based on a pre-set timeline. The allocation is designed to be aggressive early on and gradually de-risk as you get closer to needing the money. For someone in or near retirement, a TDF like a Fidelity Freedom 2025 Fund will already have a conservative allocation, perhaps 55% stocks and 45% bonds and short-term debt, providing a built-in defense against market volatility.

Key Insight: A Target-Date Fund automates the transition from a growth-focused portfolio to an income-focused one. Its primary benefit is removing the guesswork and emotional decision-making from the critical rebalancing process that should occur as retirement approaches.

Practical Implementation Tips

To effectively use a Target-Date Fund strategy, consider the following:

- Review the Glide Path: Not all TDFs are the same. Examine the fund’s glide path to ensure its stock-to-bond ratio at retirement (and after) aligns with your personal risk tolerance.

- Monitor Fees: TDFs can have varying expense ratios. Opt for low-cost, index-based versions whenever possible to maximize your returns.

- Avoid “All-in-One” Misconceptions: While convenient, a single TDF might not cover all your specific financial needs. You may need to supplement it with other investments to fine-tune your overall portfolio.

- Consolidate to Avoid Conflicts: If you hold TDFs in multiple accounts, ensure they have the same target date to avoid holding conflicting asset allocations that work against each other.

This strategy simplifies one of the most crucial aspects of retirement planning. To better understand how these allocations shift over time, you can explore more about retirement portfolio allocation by age on PopaDex.

4. The Total Return / Dynamic Withdrawal Strategy

This flexible approach shifts the focus from generating specific income (like dividends) to maximizing the entire portfolio’s growth, including capital gains, dividends, and interest. Instead of a fixed withdrawal percentage, the amount you take out each year is dynamic, adjusting based on market performance, your portfolio’s value, and your actual spending needs. This strategy offers greater adaptability compared to more rigid rules.

The core idea is to treat all portfolio growth as potential income. When the market performs well, you might withdraw a bit more for discretionary spending or to build up cash reserves. Conversely, during a down year, you would tighten your belt and withdraw less to avoid selling assets at a loss. For example, a retiree might plan for a $50,000 withdrawal but reduce it to $45,000 after a bear market, preserving capital for future growth.

How It Shapes Asset Allocation

A total return strategy frees you from chasing high-yield investments, which can sometimes carry higher risks. Instead, it allows for a diversified portfolio geared toward long-term growth, which is a key component of finding the best asset allocation for retirees. A typical allocation might be a balanced 60/40 or even a 70/30 stock-to-bond mix, as the goal is to generate strong overall returns that can be harvested as needed.

Key Insight: This strategy prioritizes portfolio health over a fixed income stream. By adjusting withdrawals based on performance, you actively mitigate sequence-of-returns risk and give your investments a better chance to recover and grow over a multi-decade retirement.

Practical Implementation Tips

To apply this strategy effectively, consider the following actions:

- Establish Guardrails: Set clear rules for your withdrawals. For instance, define a ceiling (e.g., never increase withdrawals by more than 10% in one year) and a floor (the minimum amount you need to cover essential expenses).

- Use Rolling Averages: Base your withdrawal decisions on your portfolio’s two or three-year average performance rather than a single volatile year. This smooths out market fluctuations.

- Harvest Gains Strategically: During strong years, rebalance your portfolio by selling appreciated assets to generate the cash needed for your annual withdrawal.

- Document Your Plan: Create a written policy outlining how and when you will adjust withdrawals. This prevents emotional decision-making during periods of market stress.

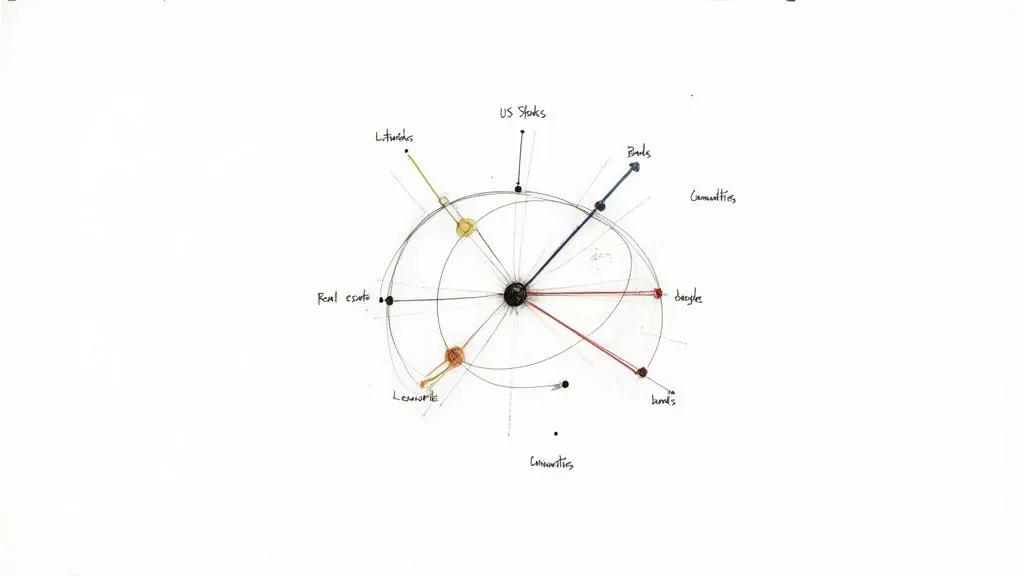

5. The Modern Portfolio Theory (MPT) Approach

Originating from the Nobel Prize-winning work of economist Harry Markowitz, Modern Portfolio Theory (MPT) is a sophisticated framework for building a portfolio that maximizes expected returns for a given level of risk. Rather than picking individual assets based on their standalone potential, MPT focuses on how different asset classes move in relation to one another (their correlation). For retirees, this quantitative approach provides a mathematical foundation for constructing a durable and efficient portfolio.

The core principle is diversification not just for its own sake, but as a scientific method to reduce volatility. By combining assets that are not perfectly correlated (e.g., stocks, bonds, real estate, and commodities), a retiree can create a portfolio where the weakness in one area is offset by strength in another. This creates a smoother overall return profile, which is crucial when you are drawing income.

How It Shapes Asset Allocation

MPT is the intellectual underpinning of finding the best asset allocation for retirees because it shifts the focus from chasing the highest returns to achieving the best risk-adjusted returns. An MPT-optimized retirement portfolio might look more complex than a simple 60/40 model, often including allocations to international stocks, real estate investment trusts (REITs), and alternative assets.

For example, a retiree’s MPT-driven portfolio might be structured as: 30% U.S. Stocks, 20% International Stocks, 25% Bonds, 15% Real Estate, and 10% Commodities. During a crisis like the 2008 financial meltdown, the bond and real estate portions would have provided stability while stocks recovered, demonstrating MPT’s power in action.

Key Insight: MPT teaches that the risk of a portfolio is not the average risk of its components but is driven by their correlations. True diversification means owning assets that behave differently in various market conditions, not just owning a lot of different things.

Practical Implementation Tips

To effectively use MPT principles in your retirement strategy, consider the following steps:

- Diversify Broadly: Move beyond a simple stock/bond mix. Include international equities, real estate, and other uncorrelated assets to build a more resilient portfolio.

- Rebalance Strategically: Monitor your target allocations and rebalance when any single asset class drifts more than 5% from its target. This enforces discipline.

- Stress-Test Your Mix: Use tools like Monte Carlo simulations to model how your proposed allocation would perform under various historical and hypothetical market scenarios.

- Review Assumptions: The correlations between asset classes can change over time. Review and update your assumptions every 3 to 5 years to ensure your allocation remains optimal.

MPT provides a robust, data-driven methodology for constructing a portfolio built to last. For a deeper understanding of its core concepts, you can discover more about diversifying your investment portfolio with PopaDex.

6. The All-Weather / Risk Parity Strategy

Traditional portfolios allocate capital by dollar amount, but the All-Weather, or Risk Parity, strategy takes a radically different approach. It allocates capital based on risk contribution, aiming to build a portfolio that can perform reasonably well across all economic environments: rising growth, falling growth, rising inflation, and falling inflation. This strategy seeks to balance risk, not dollars, to create a truly diversified portfolio.

Developed by Ray Dalio of Bridgewater Associates, this approach sizes each position so that it contributes equally to the overall portfolio volatility. Since stocks are inherently more volatile than bonds, a traditional 60/40 portfolio is overwhelmingly dominated by stock market risk. Risk Parity corrects this by increasing exposure to less volatile assets like long-term bonds and commodities to achieve a more balanced risk profile.

How It Shapes Asset Allocation

The All-Weather strategy fundamentally redefines what makes the best asset allocation for retirees by shifting the focus from potential returns to risk balance. A classic example is Dalio’s All-Weather portfolio: 30% stocks, 40% long-term Treasury bonds, 15% intermediate-term Treasury bonds, 7.5% gold, and 7.5% commodities. The heavy allocation to bonds is designed to balance the high volatility of the smaller stock portion.

Key Insight: Risk Parity’s goal is not to maximize returns in any single year but to generate consistent, steady returns with significantly lower drawdowns across different economic seasons. Its resilience was demonstrated during the 2008 financial crisis, where such portfolios often held up far better than stock-heavy ones.

Practical Implementation Tips

To effectively apply a Risk Parity approach, consider the following actions:

- Use Low-Cost ETFs: Build the portfolio using low-cost index funds or ETFs for each asset class (e.g., total stock market, long-term treasuries, gold, and broad commodities).

- Simplify Without Leverage: While professional Risk Parity funds often use leverage to boost returns from low-volatility assets, individual retirees can implement a simplified, unleveraged version that still captures the core benefit of risk balance.

- Rebalance Strategically: Rebalance at least semi-annually or whenever the risk contributions of the asset classes drift significantly from your target. This ensures the portfolio remains balanced through market shifts.

- Consider Multi-Asset Funds: For a simpler solution, some ETF providers offer “all-weather” or risk-parity-style multi-asset funds that manage the allocations for you.

7. The Income-Focused / Dividend Growth Strategy

Distinct from total-return approaches, the Income-Focused Strategy prioritizes generating a consistent and reliable cash flow directly from portfolio assets. Instead of systematically selling shares to create income, this method aims to cover living expenses using the dividends and interest the portfolio naturally produces. This approach appeals to retirees who value the psychological comfort of a predictable “paycheck” from their investments, mirroring the income they were accustomed to during their working years.

The core idea is to build a portfolio of assets that collectively yields enough to meet spending needs, such as 4% or 5% annually, from organic cash flow alone. This often involves a collection of high-quality, dividend-paying stocks, bond ladders, and other income-producing securities. The goal is to live off the income while allowing the principal investment to remain intact or even grow over time.

How It Shapes Asset Allocation

This strategy directly dictates a tilt towards specific asset classes, making it a powerful tool for finding the best asset allocation for retirees seeking stability. A typical income-focused portfolio might allocate 40-60% to dividend growth stocks and “dividend aristocrats,” which are companies with a long history of increasing their payouts. The remainder is often invested in fixed-income assets like individual bonds structured as a ladder, bond ETFs, and selectively, higher-yielding assets like REITs or preferred stocks.

Key Insight: The primary goal is income sustainability, not just high yield. Chasing the highest-yielding assets can expose a portfolio to significant risk, as an unsustainable dividend is often a sign of a company in distress. The focus should be on quality companies with a proven ability to pay and grow their dividends.

Practical Implementation Tips

To build an effective income-focused portfolio, consider these actions:

- Prioritize Dividend Growth: Focus on companies with a history of increasing their dividends, not just those with a high current yield. This provides a natural, built-in hedge against inflation.

- Diversify Income Sources: Spread your investments across various dividend-paying sectors (e.g., consumer staples, healthcare, utilities) and fixed-income types to avoid over-concentration.

- Monitor Dividend Health: Regularly review the financial health of the companies you own. A company’s ability to maintain and grow its dividend is a key indicator of its stability.

- Combine with Other Strategies: If your portfolio’s natural yield doesn’t cover all expenses, you can supplement it with strategic withdrawals from the growth-oriented portion of your portfolio.

- Consider a Bond Ladder: Build a ladder with individual bonds that mature at different intervals. This provides a predictable stream of principal that can be spent or reinvested.

8. The Guardrails / Corridor Strategy

The Guardrails Strategy, also known as the Corridor Approach, offers a dynamic and efficient alternative to strict calendar-based rebalancing. Instead of adjusting your portfolio on a fixed schedule, you set tolerance bands or “guardrails” around your target asset allocation. You only rebalance when market movements push a specific asset class outside these predefined upper or lower limits. This approach addresses a key challenge for retirees: how to maintain a target risk profile without overtrading and incurring unnecessary costs or taxes.

For example, a retiree with a target 60% stock and 40% bond allocation might set 5% guardrails. This means the stock allocation could drift anywhere between 55% and 65% without triggering a rebalancing event. If a strong bull market pushes stocks to 66% of the portfolio, the retiree would sell stocks to bring the allocation back to the 60% target. Conversely, if a market downturn caused stocks to fall to 54%, they would buy more stocks to return to the 60% mark.

How It Shapes Asset Allocation

This method directly impacts the best asset allocation for retirees by allowing for controlled momentum while enforcing discipline. It lets your winning assets run a bit, potentially capturing more upside than a strict annual rebalancing might. At the same time, it prevents your portfolio’s risk profile from drifting too far from your long-term plan. The guardrails themselves become a critical component of your allocation strategy, defining your tolerance for deviation.

Key Insight: The Guardrails Strategy combines the best of two worlds: the discipline of rebalancing with the cost-efficiency of a more hands-off approach. It forces you to act only when necessary, preventing emotional decisions while minimizing transaction fees and potential tax consequences.

Practical Implementation Tips

To effectively implement a Guardrails Strategy, consider these actions:

- Define Your Corridors: Set tolerance bands based on your risk tolerance and the volatility of the asset classes. A common starting point is a +/- 5% band around your target percentages.

- Document Your Rules: Write down your target allocation and the specific upper and lower guardrails for each asset class. This prevents emotional decision-making when markets are turbulent.

- Monitor Systematically: Check your portfolio’s allocation quarterly or semi-annually. The goal is to monitor, not to trade, unless a guardrail is breached.

- Combine with an Annual Review: Even if no guardrails are breached, review your overall strategy once a year to ensure your target allocation still aligns with your financial goals and life circumstances.

Retirement Asset Allocation — 8-Strategy Comparison

| Strategy | Implementation Complexity | Resource & Monitoring | Expected Outcomes / Effectiveness | Ideal Use Cases | Key Advantages |

|---|---|---|---|---|---|

| The 4% Rule (Safe Withdrawal Rate Strategy) | Low — simple fixed-rule | Low — annual review & rebalance | Predictable income for ~30 yrs; Medium | Hands-off retirees seeking budgeting certainty | Simple, well-researched, predictable withdrawals |

| The Bucket Strategy (Time-Segmented Approach) | Medium — multi-bucket setup | Moderate — active rebalancing across buckets | Reduces sequence-of-returns risk; High | Retirees anxious about short‑term market drops | Protects spending in downturns; matches horizon to risk |

| Target-Date Fund Strategy | Low — automatic glide‑path | Very low — set-and-forget; watch fees | Gradual de‑risking aligned to date; Medium | Beginner investors and 401(k) participants | Auto-rebalancing, broad diversification, minimal decisions |

| Total Return / Dynamic Withdrawal Strategy | High — flexible rules and adjustments | High — ongoing monitoring and possible advisor | Maximizes longevity and flexibility; High | Investors with complex/taxable situations or flexibility needs | Adaptive withdrawals, tax-conscious, longevity-focused |

| Modern Portfolio Theory (MPT) Approach | High — optimization and modeling | Moderate‑High — data, tools, periodic re-optimization | Improved risk‑adjusted returns if assumptions hold; Medium-High | Larger portfolios seeking mathematically driven allocation | Broad diversification, correlation-aware optimization |

| All-Weather / Risk Parity Strategy | High — risk-weighting and possible leverage | High — leverage costs, monitoring, implementation hurdles | Resilient across regimes; lower volatility; High | Institutional or sizable portfolios prioritizing stability | Balanced risk contributions, downside protection |

| Income-Focused / Dividend Growth Strategy | Medium — income security vs selection work | Moderate — monitor dividends, maintain bond ladders | Steady cash flow; yield variability risk; Medium | Retirees who prefer regular income over total-return focus | Predictable payouts, psychological comfort, potential tax benefits |

| Guardrails / Corridor Strategy | Medium — set bands and trigger rules | Low‑Moderate — monitor for breaches, less frequent trades | Disciplined allocation with reduced trading; High | Investors wanting rebalancing discipline with flexibility | Low trading/tax drag, captures momentum, enforces discipline |

Bringing It All Together: Implementing and Monitoring Your Retirement Strategy

Navigating the landscape of retirement finance can feel like charting a course through unpredictable waters. We’ve explored a diverse set of powerful strategies, from the structured simplicity of the Bucket Strategy and Target-Date Funds to the dynamic flexibility of Total Return and Guardrail models. Each approach offers a unique framework for managing your wealth, but the single most important takeaway is this: there is no universal “best asset allocation for retirees.” The optimal strategy is the one that is deeply personalized to your specific risk tolerance, income needs, and long-term goals.

Your journey doesn’t end with selecting a model portfolio. In fact, that’s just the beginning. The true art of a successful retirement plan lies in its implementation and ongoing maintenance. An asset allocation strategy is not a “set-it-and-forget-it” solution; it’s a living plan that requires consistent attention to stay aligned with your objectives as markets fluctuate and your life circumstances evolve.

From Theory to Action: Your Next Steps

Choosing your ideal allocation is the first critical step; putting it into practice is where your financial future is truly forged. Whether you’ve gravitated toward the income-generating focus of a dividend growth strategy or the balanced resilience of an All-Weather portfolio, consistent monitoring and disciplined rebalancing are non-negotiable.

Here are the actionable steps to transform your chosen strategy from a concept into a robust, real-world plan:

-

Codify Your Plan: Don’t leave your strategy to memory. Write down your target allocations for each asset class (e.g., 50% stocks, 40% bonds, 10% alternatives). Define your rebalancing triggers, such as when an asset class drifts more than 5% from its target or on a set quarterly schedule. This document becomes your financial constitution.

-

Consolidate Your View: You cannot manage what you cannot see. The first major hurdle for many retirees is portfolio fragmentation, with assets scattered across 401(k)s, IRAs, brokerage accounts, and perhaps even international holdings. Gaining a single, unified view is essential for accurate allocation tracking.

-

Execute and Automate: Once you have a clear picture, execute the necessary trades to align your current holdings with your target allocation. Consider setting up automatic investments or withdrawals to streamline the process and remove emotion from your day-to-day financial management.

-

Schedule Regular Reviews: Mark your calendar for quarterly or semi-annual portfolio reviews. These are your dedicated times to assess performance, check for allocation drift, and make necessary adjustments. A scheduled review prevents panicked decisions during market volatility and ensures disciplined oversight.

The Power of Vigilant Monitoring and Legal Preparedness

The most meticulously designed asset allocation can fail if it’s not properly maintained. The risk of “portfolio drift” is a constant threat, where outperforming asset classes grow to represent a larger-than-intended share of your portfolio, inadvertently increasing your risk exposure. This is why disciplined rebalancing is the cornerstone of long-term success.

Furthermore, a truly comprehensive retirement strategy extends beyond market returns and withdrawal rates. It’s also crucial to safeguard your assets and ensure your legacy is managed according to your wishes. Beyond asset allocation, a comprehensive retirement plan also includes vital legal considerations like estate planning and asset security to protect your legacy and ensure your wishes are carried out. This legal framework provides peace of mind that complements your financial strategy.

Ultimately, the best asset allocation for retirees is the one you can understand, implement, and stick with through all market cycles. By choosing a strategy that aligns with your financial personality and pairing it with a robust system for monitoring and maintenance, you gain the clarity and confidence needed to enjoy your retirement to the fullest.

Ready to take control of your retirement portfolio with unparalleled clarity? PopaDex is the ultimate net worth tracker designed to consolidate all your accounts into a single, intuitive dashboard, making it effortless to monitor your asset allocation and stay on track. Sign up for a free account today and see your entire financial world in one place with PopaDex.