Our Marketing Team at PopaDex

A Modern Playbook for Financial Planning for Young Professionals

Financial planning isn’t just for the wealthy or those nearing retirement. For young professionals, it’s about building a system for your money that values long-term freedom over just a high paycheck. It’s a proactive game plan to tackle debt, build up savings, and start investing early to let the magic of compound interest do the heavy lifting. This is the blueprint for designing the life you actually want to live.

Why Financial Planning Is Critical in Your 20s and 30s

Let’s be real—managing money in your 20s and 30s is a whole different beast than it was for our parents. You’re likely juggling a mountain of student loans, insane living costs, and the subtle pressure of “lifestyle creep” that sneaks in with that first real salary. It’s way too easy to feel like you’re just treading water, let alone planning for a future that feels a lifetime away.

This is exactly why having a financial plan is no longer a “nice-to-have.” It’s essential. And no, this isn’t about creating a miserable budget that cuts out all the fun. It’s about empowerment. It’s about finally telling your money where to go, instead of scratching your head and wondering where it all went.

Shifting from Income to Wealth Building

The single biggest mental shift you can make is moving from an income mindset to a wealth-building mindset. A good salary is great for paying the bills, but real financial freedom comes from what you keep and what you grow. Wealth is your collection of assets—investments, savings, property—that work for you, even when you’re not clocking in.

Think of it this way: your income is the tool, but wealth is the house you build with it. Without a plan, even the best tools just gather dust. With one, you can build something that gives you security and options for decades.

“Building wealth is about making your money work for you, rather than working for money indefinitely.”

Getting this right changes everything. Suddenly, saving and investing aren’t sacrifices. They’re strategic moves to buy back your future time and freedom.

The Core Pillars of Your Financial Strategy

A smart financial plan for a young professional is built on a few non-negotiable pillars. Get these right, and you’ll have a rock-solid foundation for everything else.

- Cash Flow Management: This is more than just budgeting. It’s about knowing exactly where your money is flowing so you can consciously point it toward your goals, whether that’s a down payment on a house or your first big investment.

- Strategic Debt Reduction: Not all debt is the same. A good plan helps you attack high-interest debt (looking at you, credit cards) that’s actively fighting against your efforts to build wealth.

- Early and Consistent Investing: Your biggest financial advantage right now is time. Starting to invest in your 20s, even with small amounts, unleashes the incredible power of compounding and can radically change your long-term net worth.

- Wealth Protection: This is the boring but crucial stuff. It means having the right insurance (like disability and renter’s) and knowing enough about taxes to protect the assets you’re working so hard to build.

You’re not alone in feeling like you need a roadmap. A surprising 55% of Americans believe the ideal time to get professional financial advice is between ages 25 and 39. And with over 80% of Millennials and Gen Z admitting their financial planning could be better, it’s clear that taking control is a top priority. This guide is your first step. Read the full research about these financial planning trends.

Mastering Your Cash Flow Beyond Basic Budgeting

Forget the rigid, guilt-inducing spreadsheets where every coffee purchase feels like a financial sin. Real financial planning for young professionals isn’t about restriction; it’s about direction. We’re moving past basic budgeting to create a wealth-building cash flow plan—a forward-looking system designed for growth, not just tracking what you’ve already spent.

This is about intentionally telling your money where to go to build the future you want. But you can’t redirect a river without knowing its current course, so the first step is always getting a clear picture of where your money is going right now. Once you have that, you can pick a framework that actually fits your life.

Choosing Your Cash Flow Method

There are a couple of popular methods that work great for young professionals, whether you have a steady paycheck or a more variable, freelance income.

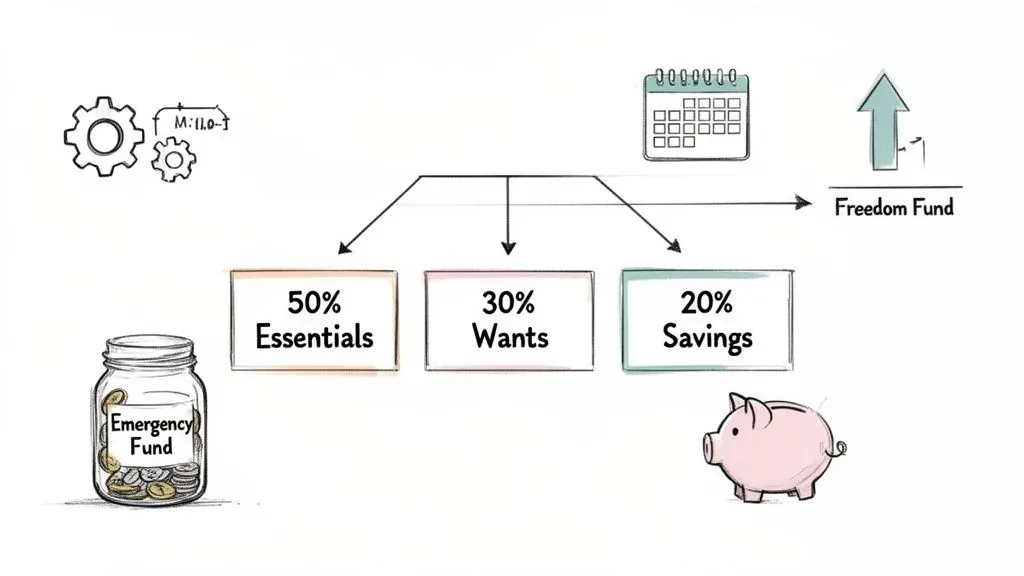

- The 50/30/20 Rule: This is a fantastic, simple guideline. You aim to put 50% of your after-tax income toward “Needs” (rent, utilities, groceries), 30% toward “Wants” (dining out, travel, hobbies), and a crucial 20% toward “Financial Goals” like savings, debt repayment, and investments.

- Zero-Based Budgeting: With this hands-on approach, every single dollar of your income gets a specific job. Your income minus your expenses, savings, and investments equals zero at the end of the month. It’s more detailed, but it gives you maximum control—perfect if your income fluctuates.

Think of it this way: a marketing manager with a predictable salary might love the 50/30/20 rule for its simplicity. But a freelance graphic designer could use a zero-based budget to cover essentials first and then strategically funnel cash from a big project into savings or investments. The goal is to find a system that reduces your stress, not adds to it.

Your cash flow plan is your financial GPS. It doesn’t just show you where you are; it gives you the power to choose your destination and the best route to get there.

Automate Your Way to Wealth

Honestly, the single most powerful habit you can build is automating your financial goals. This is “paying yourself first” in its purest form. Before you even think about paying bills or buying groceries, a slice of your paycheck should be automatically whisked away to where it can grow.

Set up recurring transfers from your checking account to your:

- High-Yield Savings Account (HYSA): The home for your emergency fund.

- Retirement Accounts: Your 401(k), Roth IRA, or similar accounts.

- Brokerage Account: For your longer-term investments outside of retirement.

When you make it automatic, you take willpower and emotion completely out of the picture. Your wealth just builds consistently in the background. It’s the easiest way to make sure you’re always prioritizing your future self.

Building Your Emergency and Freedom Funds

Your cash flow plan needs to build two critical pools of money: an emergency fund and a freedom fund.

An emergency fund is your non-negotiable financial safety net. The classic advice holds true: save three to six months’ worth of essential living expenses. If your absolute must-haves (rent, food, insurance) cost you $3,000 a month, you’re shooting for a target of $9,000 to $18,000. Keep this money in a high-yield savings account—it needs to be accessible, but not so easy to grab that you’d dip into it for non-emergencies. This is the fund that turns a surprise car repair from a crisis into an inconvenience.

Your freedom fund, on the other hand, is what’s left over after all your needs are met and your savings goals are funded. This is your calculated, guilt-free spending money. Knowing this number is empowering. It lets you decide whether to save for a big trip, invest in a new skill, or just enjoy a nice dinner out without a shred of worry. To really nail this down, you need a clear way to track cash flow and determine your disposable income. Gaining that clarity turns budgeting from a chore into a tool that lets you confidently spend on the things that actually matter to you.

Tackling Debt and Building Credit with a Clear Strategy

Debt can feel like a massive weight holding you back, especially when you’re just starting to build momentum in your career. The key is to reframe it. Instead of seeing debt as a permanent anchor, think of it as a temporary—and totally manageable—obstacle you can strategically dismantle. With the right game plan, you can take control and clear the path to building real wealth.

First things first, you need a method of attack. Two of the most effective strategies out there are the Debt Avalanche and the Debt Snowball. Each has its own financial and psychological perks, so the “best” choice really comes down to what motivates you.

Debt Avalanche vs. Debt Snowball

The Debt Avalanche is all about logic. With this method, you throw every extra dollar at the debt with the highest interest rate, regardless of the balance. Mathematically, this is the smartest move because it saves you the most money on interest over the long haul.

On the other hand, the Debt Snowball is built for psychological wins. You focus on paying off your smallest debt first, no matter the interest rate. Every time you wipe a debt off your list, you get a powerful boost of momentum and motivation to keep crushing the next one.

Let’s look at a real-world example. Meet Alex, a young professional juggling two main debts:

- A $5,000 credit card balance with a painful 22% APR.

- A $30,000 student loan at a more manageable 5.8% APR.

Alex has an extra $500 a month to throw at this debt after covering the minimum payments.

| Strategy | Alex’s First Target | Financial Benefit | Psychological Benefit |

|---|---|---|---|

| Debt Avalanche | The $5,000 credit card (22% APR) | Saves the most money on interest. | Tackles the most “expensive” debt first, creating financial breathing room faster. |

| Debt Snowball | The $5,000 credit card (smallest balance) | N/A in this case, as it’s also the highest interest. | Provides a quick win, building confidence to tackle the larger student loan next. |

In Alex’s case, both strategies point to the same starting line. But if Alex had a smaller, lower-interest personal loan, the Snowball would target that first for the quick win, while the Avalanche would stick to the high-interest credit card. For a deeper dive, our guide on how to pay off debt effectively breaks these strategies down even further.

Why Your Credit Score Is a Financial Superpower

While you’re chipping away at existing debt, you absolutely have to focus on building a strong credit history. Your credit score is so much more than a three-digit number; it’s a direct reflection of your financial reliability. A high score can save you tens of thousands of dollars over your lifetime by unlocking lower interest rates on mortgages, auto loans, and everything in between.

Think of it as your financial reputation. Lenders use it to quickly size up how risky it is to lend you money. A score of 740 or higher is generally considered the sweet spot and will open doors to the best rates and terms out there.

This is a critical area where many young people are flying blind. The 2025 TIAA Institute-GFLEC Personal Finance Index found that Gen Z could only answer 38% of financial literacy questions correctly—the lowest of any generation. This points to a huge knowledge gap, especially around concepts like credit and risk. Discover more insights from the personal finance study.

A good credit score is a financial asset. It doesn’t just help you borrow money; it helps you borrow money more cheaply, accelerating your ability to build wealth.

Actionable Steps to Build Excellent Credit

Building good credit doesn’t happen overnight, but a few consistent, responsible habits will get you there faster than you think.

-

Use Credit Cards Responsibly: One of the simplest ways to build credit is to use a credit card for small, regular purchases (like your Netflix subscription or weekly groceries) and pay the balance in full every single month. This shows lenders you can handle credit without racking up high-interest debt.

-

Keep Your Credit Utilization Low: This is a big one. Aim to use less than 30% of your available credit limit on any card. So, if you have a $10,000 limit, try to keep your reported balance under $3,000. Maxing out your cards is a major red flag to lenders.

-

Never Miss a Payment: Your payment history is the single biggest factor in your credit score. Set up automatic payments for at least the minimum amount due to avoid any accidental late fees and dings to your score.

-

Check Your Credit Report Regularly: You’re entitled to a free credit report from each of the three major bureaus (Equifax, Experian, and TransUnion) every year. Pull them. Read them. Look for errors and get a feel for what’s helping or hurting your score.

Investing Early to Build Long-Term Wealth

If you have one financial superpower as a young professional, it’s this: time. Your age isn’t a liability; it’s your single greatest asset. The magic ingredient here is compound interest—where your investment earnings start generating their own earnings. This creates a snowball effect that can turn small, consistent contributions into serious wealth down the road.

Let’s look at two friends, Maya and Ben, to see how this plays out.

- Maya starts investing at 25. She puts away just $200 a month.

- Ben waits until he’s 35. Feeling behind, he invests double Maya’s amount—$400 a month.

Assuming an average annual return of 8%, by the time they both turn 65, Maya will have over $700,000. Ben, despite investing twice as much each month, will have just over $540,000. That $160,000 difference is the incredible power of giving your money an extra decade to grow. The lesson is crystal clear: starting now, even with a little, beats waiting to start with a lot later.

Your First Investment Steps

Getting started with investing feels like a huge hurdle, but it doesn’t have to be complicated. The trick is to start with the most accessible and powerful accounts available to you.

Your first stop should almost always be your employer-sponsored retirement plan, like a 401(k) or 403(b). Why? The company match. Many companies will contribute to your account based on what you put in. This is literally free money.

Capturing your full employer match is the highest guaranteed return you will ever get on an investment. Not doing it is like turning down a pay raise.

For instance, if your company matches 100% of your contributions up to 5% of your salary, you need to contribute at least 5% to get that full match. Anything less, and you’re leaving free money on the table.

Expanding Beyond Your Employer Plan

Once you’re getting that full company match, it’s time to look at other tax-advantaged accounts. A Roth IRA is a fantastic tool for young professionals. You contribute with after-tax dollars, meaning your investments grow completely tax-free, and you won’t owe a dime in taxes on qualified withdrawals when you retire.

After you’ve maxed out your tax-advantaged options, a standard taxable brokerage account is the next logical step. These accounts have no contribution limits and are perfect for goals outside of retirement, like saving for a down payment or another big purchase.

A simple, effective strategy for any of these accounts is to invest in low-cost index funds or ETFs. These funds bundle together hundreds or thousands of stocks (like all the companies in the S&P 500), giving you instant diversification without the headache of picking individual winners. It’s a straightforward, affordable, and historically proven way to build wealth.

This visual breaks down how different debt repayment strategies work—one saves you the most on interest, while the other gives you psychological wins by knocking out small debts first.

Core Principles for Successful Investing

You don’t need to be a Wall Street guru to succeed. Just stick to these foundational principles:

- Consistency is Key: Automate your contributions and invest regularly. This habit is far more important than trying to “time the market.”

- Diversification Reduces Risk: Don’t put all your eggs in one basket. Index funds do this for you automatically. Learning how to diversify your investment portfolio is a cornerstone of managing risk while building wealth.

- Keep Costs Low: Investment fees might seem small, but they can seriously eat into your returns over decades. Always prioritize funds with low expense ratios.

By starting early, grabbing every bit of your employer match, and sticking to simple, proven strategies, you can build a powerful engine for creating long-term wealth. You don’t need a fortune to start—you just need to start.

Don’t Forget to Play Defense: Protecting Your Assets

Building wealth is the fun part, but protecting what you’ve earned is just as critical. A solid financial plan isn’t just about growth; it’s about playing smart defense to safeguard everything you’re working so hard for. This means getting strategic with insurance and proactive about your taxes to avoid nasty surprises down the road.

This isn’t about being paranoid. It’s about building a financial fortress. That way, one of life’s inevitable curveballs—a sudden injury, a stolen laptop—doesn’t completely derail your long-term goals. With the right protection in place, you can keep building your wealth with confidence.

Insurance You Actually Need (Beyond the Obvious)

When you’re young and feel invincible, insurance can seem like a waste of money. But a couple of policies are often overlooked and absolutely essential for protecting your financial future.

-

Disability Insurance: Let’s be real: your ability to earn an income is your most valuable asset. Disability insurance is basically insurance for your paycheck. If you get sick or injured and can’t work, it provides a portion of your income so you can still pay your bills, save, and invest. Without it, a bad accident could bring your entire financial life to a screeching halt.

-

Renter’s or Homeowner’s Insurance: If you’re renting, don’t assume your landlord’s policy covers your stuff—it doesn’t. Renter’s insurance is shockingly affordable, often just a few bucks a month, and protects your valuables from theft, fire, or other damage. Thinking about protecting your home with the right insurance is a core part of being financially responsible.

These aren’t just expenses; they’re high-impact investments in your financial security.

Get Proactive with Taxes to Keep More of Your Money

Taxes are easily one of your biggest expenses, but you have more control over them than you probably think. Getting smart about your tax bill isn’t about finding sketchy loopholes. It’s about using the existing rules to your advantage.

A perfect place to start is understanding the crucial difference between tax deductions and tax credits. A deduction simply lowers your taxable income, while a credit directly reduces the amount of tax you owe, dollar for dollar. Credits are almost always more valuable.

“A proactive tax strategy ensures you’re not leaving money on the table. It’s about legally and ethically minimizing your tax burden so you can redirect those funds toward your wealth-building goals.”

Here’s a simple example: a $1,000 tax credit saves you a full $1,000 on your tax bill. But a $1,000 deduction, if you’re in the 22% tax bracket, only saves you $220. Knowing this difference helps you prioritize financial moves that pack the biggest punch.

Maximize Your Tax-Advantaged Accounts

One of the most powerful ways to get your tax situation in order is by consistently funding your tax-advantaged accounts. These are government-approved plans specifically designed to help you save for retirement and other big goals.

Key Accounts to Focus On:

- 401(k)/403(b): When you contribute to a traditional 401(k), the money comes out of your paycheck before taxes are calculated. This immediately lowers your taxable income for the year, giving you an instant tax deduction. It’s one of the easiest tax wins available.

- Roth IRA: While you don’t get an upfront deduction, the real magic happens later. Your contributions grow completely tax-free, and you won’t pay a dime in taxes on qualified withdrawals in retirement.

- Health Savings Account (HSA): If you have a high-deductible health plan, an HSA is the holy grail of tax savings. It’s a triple threat: your contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

By making these accounts a priority, you’re hitting two birds with one stone: building your nest egg and actively slashing your tax bill, year after year. It’s a cornerstone of any effective financial plan.

How to Track Your Progress with a Net Worth Dashboard

You’ve set up your cash flow system, you have a plan to tackle your debt, and you’re finally starting to invest. So, how do you know if any of it is actually working?

Forget your salary or your checking account balance for a second. The single most important number for measuring your financial health is your net worth.

Think of your net worth as your ultimate financial scorecard. The formula is simple: everything you own (your assets) minus everything you owe (your liabilities). That single number gives you a true, high-level view of your financial journey.

When your net worth is rising, you have concrete proof that your financial plan is working because your assets are growing faster than your debts. Watching that number climb is an incredible motivator and gives you the clarity to make smarter decisions down the road.

Why Net Worth Beats Every Other Metric

Focusing on income alone can be deceptive. You might be pulling in a six-figure salary, but if your spending and debt are just as high, you’re not actually building wealth. You’re just treading water. Net worth cuts through all that noise.

It rolls up all your financial activities—saving, investing, paying off student loans, building home equity—into one clear, meaningful figure. This is exactly why a dedicated dashboard has become a non-negotiable tool for young professionals serious about their finances.

Your net worth is the story of your financial life told in a single number. Tracking it is like having a GPS for your wealth-building journey, showing you exactly where you are and how far you’ve come.

See It All in One Place with a Dashboard

Let’s be real: logging into a dozen different accounts every month to manually calculate your net worth is a massive pain. It’s tedious, you’re bound to make a mistake, and you’ll probably just stop doing it.

This is where a platform like PopaDex completely changes the game. It pulls your entire financial life into one clean, visual dashboard.

It connects to your bank accounts, credit cards, investment portfolios, student loans, and even property values to give you an accurate, real-time snapshot of your net worth. It saves you a ton of time and provides the clarity you need to stay on track.

Here’s a glimpse of what a consolidated dashboard looks like—all the moving parts of your financial life, finally in one spot.

This view instantly shows your total assets, liabilities, and the bottom-line net worth, helping you spot trends and stay fired up about your goals.

This kind of tech is more important than ever. The financial advisory industry is facing a huge supply-demand problem. With nearly 40% of advisors set to retire in the next decade and a staggering 60% drop in advisors under 25 since 2022, getting affordable, personalized guidance is getting tougher. Automated platforms help bridge that gap, putting powerful financial tools directly in your hands. You can read more about the decline of younger financial advisors and its industry impact to understand the shift.

Making Net Worth Tracking Actionable

A dashboard isn’t just about looking at a number; it’s about empowering you to take action. For globally-minded professionals and expats, features like multi-currency support are crucial for tracking assets in different countries without getting bogged down in manual conversions.

By visualizing your financial progress, you can:

- Spot the Trends: See exactly how your investment contributions or extra debt payments are moving the needle on your overall wealth.

- Stay Motivated: There’s nothing like watching your net worth graph tick upward to provide the positive reinforcement you need to stick with your plan.

- Make Smarter Decisions: Thinking about a major purchase or got a salary bump? You can see how that decision would impact your big-picture financial health.

At the end of the day, a clear view of your finances is the bedrock of success. Understanding how a net worth dashboard works is often the final piece of the puzzle, turning your abstract financial goals into something tangible and trackable. It’s the difference between just managing your money and strategically building your wealth.

Answering Your Top Financial Planning Questions

Even with the best plan laid out, real life throws curveballs. Young professionals, in particular, run into unique financial dilemmas that don’t always fit into a neat little box. Let’s tackle some of the most common hurdles you’ll likely face.

How Should I Prioritize My Financial Goals?

This is the classic tug-of-war: attack student loans, save for a down payment, or max out your 401(k)? It’s a paralyzing decision, but the answer isn’t “all or nothing”—it’s about finding the right balance for your situation.

Your first move, no exceptions, is to contribute enough to your 401(k) to get the full employer match. It’s free money, a 100% return on your investment that you simply can’t get anywhere else. Don’t leave it on the table.

After that, let the interest rates be your guide. Any high-interest debt, like credit cards with rates over 15%, is a financial emergency. That debt is actively working against you every single day, so crushing it should be your top priority.

For the middle ground—like student loans around 5-7% versus saving for a home—you can split your focus. It’s perfectly fine to hedge your bets. For instance, you could funnel 60% of your extra monthly cash toward your down payment fund and the other 40% toward extra student loan payments. This way, you’re making real, tangible progress on both goals at the same time.

Is a Financial Advisor Worth It for Me?

Forget the old stereotype that financial advisors are only for the wealthy. That’s ancient history. Getting professional advice can be a game-changer when you’re just starting out, especially if you’re trying to figure out things like company stock options or the tax implications of a side hustle.

Today, many advisors offer project-based fees or hourly rates, which makes their expertise far more accessible. You’re not signing up for a lifelong commitment or handing over a massive portfolio.

A great financial advisor is more like a personal trainer for your money. They act as a coach and accountability partner, helping you sidestep rookie mistakes and stay locked in on what truly matters to you.

Think about a one-time consultation to build a solid financial roadmap. That initial investment can give you a clear, actionable plan that you can then follow on your own, saving you from years of expensive guesswork.

Ready to stop guessing and start tracking? Take control of your financial journey with PopaDex. Consolidate all your accounts into one clear dashboard and watch your net worth grow in real-time. Start your free trial today at popadex.com.