Our Marketing Team at PopaDex

How to Save Money from Salary: Practical Guide (how to save money from salary)

To really get a handle on saving money from your salary, you first have to know where it’s all going. The best way I’ve found to do this is to create a simple budget, treat your savings goal like any other non-negotiable bill, and then put the whole system on autopilot. When you do that, saving stops feeling like a chore and just becomes a habit that works for you in the background, quietly building your wealth.

Build Your Foundation with a Simple Budget

Before you can start saving effectively, you need a clear map of your financial landscape. The point isn’t to micromanage every single coffee you buy, but to gain control so you can tell your money where to go with purpose. You can forget about those overwhelming spreadsheets or complicated software for now; the most powerful way to start is with a simple, intuitive framework.

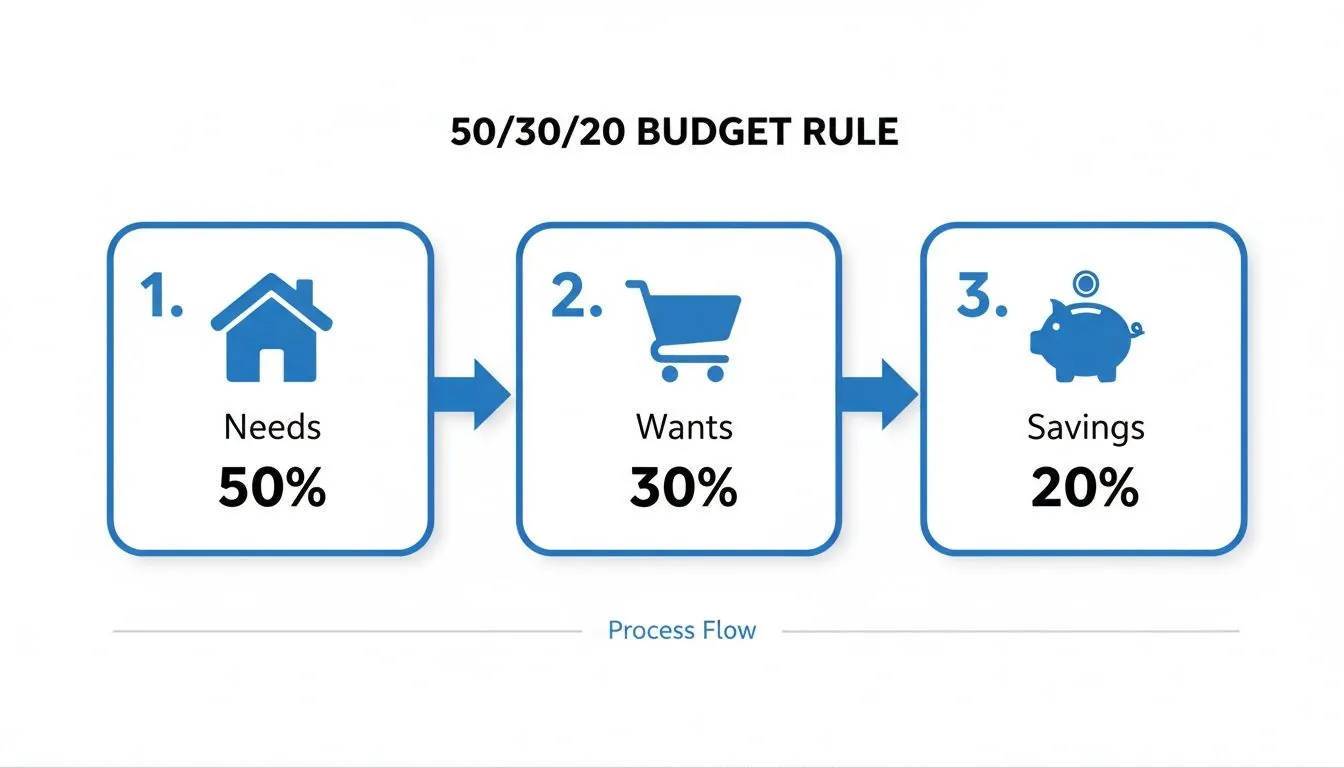

This is where the 50/30/20 rule really shines. It’s a dead-simple method for splitting up your after-tax income—the actual cash that lands in your bank account—into three buckets. This approach takes the guesswork out of budgeting and gives you a clear, actionable plan for every paycheck. If you want to dive deeper into other methods, our detailed guide on https://popadex.com/how-to-budget-money/ is a great place to explore.

The Three Core Categories of Your Budget

Getting a feel for these categories is the first step to mastering your cash flow. Each one plays a specific role in creating a balanced financial life.

-

50% for Needs: This is the biggest slice of the pie, covering all your essential living expenses. These are the things you absolutely have to pay for to live and work: rent or mortgage, utilities, groceries, transportation, and insurance. No fluff here.

-

30% for Wants: This bucket is for all the lifestyle choices that make life more enjoyable but aren’t strictly necessary for survival. Think eating out, streaming services, concert tickets, hobbies, and that vacation you’ve been dreaming about. This is where you have the most wiggle room to make adjustments.

-

20% for Savings and Debt Repayment: This is the most important part. This slice of your income is your ticket to financial freedom. It covers everything from building your emergency fund and investing for retirement to saving for a down payment or knocking out high-interest debt like credit cards.

Treat that 20% savings target like a mandatory bill you pay to your future self first. This one mental shift changes everything. You stop saving what’s left over and start prioritizing your financial security from day one.

Putting the 50/30/20 Rule into Practice

So, what does this look like with real numbers? Let’s take a recent graduate in the US who brings home $3,500 a month after taxes.

- Needs (50%): They’d have a maximum of $1,750 for essentials like rent, utilities, groceries, and a car payment. If those bills are higher than that, it’s a clear sign something needs to be trimmed.

- Wants (30%): That leaves $1,050 for discretionary spending—going out with friends, shopping, subscriptions, you name it.

- Savings (20%): A non-negotiable $700 gets funneled directly into savings or used to attack student loans.

Financial experts love this rule because it’s simple and it just works. With US salary increases projected at 3.8% and India’s at a whopping 9.5%, sticking to this plan can seriously speed up your savings. For example, a professional in the US earning $60,000 a year would see their salary bump to $62,280. By holding firm to a 20% savings rate, their monthly contribution jumps to nearly $1,040. It’s a powerful example of how even small raises can lead to big gains in your net worth.

The 50/30/20 Budget in Action

To make this even clearer, here’s a quick breakdown showing how the 50/30/20 rule applies to different income levels. This helps visualize how your allocations would scale as your take-home pay changes.

| Monthly Take-Home Pay | 50% Needs (Max Allocation) | 30% Wants (Max Allocation) | 20% Savings (Target) |

|---|---|---|---|

| $2,500 | $1,250 | $750 | $500 |

| $3,500 | $1,750 | $1,050 | $700 |

| $5,000 | $2,500 | $1,500 | $1,000 |

| $7,000 | $3,500 | $2,100 | $1,400 |

As you can see, the principle remains the same no matter your income. The goal is to create a predictable structure for your money.

To keep tabs on all of this without driving yourself crazy, you might want to check out some of the best budgeting apps out there. These tools can automatically categorize your spending and show you in real-time if you’re sticking to your 50/30/20 targets, making the whole process much less of a headache.

This first step—creating a simple, clear budget—is the most critical move you can make. It takes the fuzzy idea of “saving money” and turns it into a concrete plan, giving every single dollar from your paycheck a job to do. This is how you set the stage for building real, lasting wealth.

Automate Your Savings and Pay Yourself First

Once your budget is locked in, the next step is to make saving completely effortless. The real secret to consistent saving isn’t superhuman willpower—it’s taking willpower out of the picture entirely. This is the simple but profound idea behind the “pay yourself first” method. You start treating your savings contribution like it’s your most important bill.

Instead of waiting to see what’s left over at the end of the month, you pull money out for your savings and investments the instant your paycheck hits. This one move guarantees you hit your savings goals before a single dollar gets spent on random wants. It flips saving from an afterthought into a deliberate, non-negotiable priority.

Getting this set up is surprisingly simple. Just log into your bank’s online portal and schedule automatic, recurring transfers from your checking account to your savings accounts. Now, on payday, your savings goals are met without you lifting a finger. This is how you build a financial system that works for you, not against you.

Choosing the Right Accounts for Your Goals

Automation is the engine, but where you’re sending the money is just as critical. Different goals need different types of accounts, each with its own job to do. Parking your cash in the right place makes sure it’s working as hard as possible for your specific timeline.

- High-Yield Savings Account (HYSA): This is the perfect spot for your emergency fund and any short-term goals, like saving for a vacation or a down payment. HYSAs pay way more interest than traditional savings accounts, are FDIC-insured, and keep your money liquid for when you need it.

- Brokerage Account: For long-term growth—think retirement or other goals more than five years out—a brokerage account is your go-to. Here, you can invest in stocks, bonds, and ETFs, which have historically delivered much higher returns over time (though they do come with more risk).

- Employer-Sponsored Retirement Plan (e.g., 401(k)): If your job offers a retirement plan, especially one with a company match, this is almost always the first place your long-term savings should go. An employer match is literally free money—an immediate, guaranteed return on your investment.

Key Takeaway: The “pay yourself first” strategy is a game-changer because it forces you to prioritize your future. By automating transfers on payday, you’re not just saving; you’re systematically building wealth without relying on discipline or memory.

Real-World Automation Scenarios

Let’s look at how this plays out. Imagine a young professional just starting their career. They decide to automate 10% of their $3,000 monthly take-home pay. On the 1st and 15th of each month, their bank automatically transfers $150: $50 zips over to an HYSA for their emergency fund, and $100 is invested in a low-cost index fund in their brokerage account. They never see that money in their checking account, so the temptation to spend it disappears.

The 50/30/20 budget framework, shown below, is a great starting point for figuring out what your savings percentage should be.

This visual makes it crystal clear: savings is an intentional slice of your budget, not just the random scraps left at the end.

This strategy even works for a gig worker with a fluctuating income. They can set up their payment app to automatically slice off 20% of every single payment they receive, no matter the size. A $50 payment instantly sends $10 to savings; a $500 payment triggers a $100 transfer. This percentage-based system ensures they’re always saving, adapting on the fly to their income flow. For a deeper dive, check out our guide on how to automate your finances and make this whole process even slicker.

Set Financial Goals You Can Actually Reach

Saving money from your paycheck without a clear purpose is like driving without a destination—you might be moving, but you’re not getting anywhere meaningful. Giving every dollar you save a specific job transforms saving from a chore into a powerful tool for building the life you want. This is where you connect your automated savings plan to tangible, exciting outcomes.

The best way to do this is by breaking down your ambitions into different time horizons. Each timeline needs a different strategy and a different type of savings account to really shine. Think of it as creating separate roadmaps for your money, each leading to a specific destination.

Start with Your Financial Safety Net

Before you even think about saving for a vacation or investing for retirement, your first and most critical goal is building an emergency fund. This isn’t just a suggestion; it’s the bedrock of a stable financial life. Your emergency fund is what protects you from life’s inevitable curveballs without forcing you into high-interest debt.

The gold standard is to save 3 to 6 months’ worth of essential living expenses. To figure out your personal target, add up your non-negotiable monthly costs—rent or mortgage, utilities, food, insurance, and transportation. If your essential expenses are $3,000 a month, you’re aiming for a goal between $9,000 and $18,000.

This financial cushion is a game-changer. The World Bank has noted a significant rise in formal savings, finding that a solid emergency fund helps savers weather downturns 50% better. For a typical young professional in the US with $4,000 in monthly take-home pay, this means aiming for a $12,000-$24,000 buffer in a high-yield savings account. You can dig into this global trend in the Allianz Global Wealth Report 2025.

Define Your Mid-Term Ambitions

Once your emergency fund is fully funded, you can start mapping out your medium-term goals. These are the exciting milestones that usually fall within a one-to-five-year timeframe. Having these defined gives you something concrete and motivating to work toward.

Common mid-term goals include things like:

- A down payment on a house: This is a big one that often requires a dedicated savings plan over several years.

- Buying a new car: Saving for a car in cash can save you thousands in interest payments.

- Funding a dream wedding: Planning ahead lets you pay for your special day without starting your marriage in debt.

- A major vacation: That trip to Europe or Southeast Asia feels much more achievable when you break it down into monthly savings goals.

For these goals, a high-yield savings account is still your best friend. It keeps your money safe and accessible while earning a much better return than a traditional account. I’ve found it helpful to open separate, nicknamed savings accounts for each goal (e.g., “House Fund,” “New Car”) to visually track my progress.

Plan for Your Long-Term Future

Finally, it’s time to focus on the distant horizon—your long-term goals. These are the big-picture items, typically 10 years or more away, with retirement being the most common. It might feel abstract right now, but the magic of compounding interest means the small amounts you save today can grow into massive sums over decades.

Starting to save for long-term goals now, even with small contributions, is far more powerful than waiting to save larger amounts later. Time is your single greatest asset when it comes to investing.

For these ambitions, you need your money to work harder than it can in a savings account. This is where investment accounts come into play.

- Employer-Sponsored Retirement Plans (401k, 403b): If your employer offers a match, contribute enough to get the full amount. It’s an instant, guaranteed return on your money—you can’t beat it.

- Individual Retirement Accounts (IRA): These offer tax advantages and give you more control over your investment choices.

- General Brokerage Accounts: These offer the most flexibility for long-term goals that aren’t specifically for retirement.

By connecting each of your automated transfers to a specific short, medium, or long-term goal, you give your savings a clear mission. This simple act of assigning a job to every dollar is fundamental to mastering how to save money from your salary effectively.

Optimize Your Strategy and Avoid Common Pitfalls

Once you’ve nailed down the habit of saving from every paycheck, it’s time to shift gears. The goal is no longer just about setting money aside—it’s about making that money work as hard as you do. This is where you move from simple saving to strategic wealth-building, sidestepping the common mistakes that trip up so many people.

One of the biggest hurdles? Lifestyle inflation. It’s the natural tendency to spend more as you earn more. That 5% raise you just got doesn’t have to mean a 5% increase in your spending. Think of it as a golden opportunity to boost your savings rate without feeling a pinch in your current lifestyle. By immediately funneling most or all of that new income into savings, you supercharge your progress.

This proactive mindset is what separates casual savers from those who are serious about building long-term wealth.

Supercharge Your Savings with Smart Tools

Your salary is just the starting point. The real magic happens when you use tax-advantaged accounts and strategically wipe out debt. These aren’t complicated Wall Street maneuvers; they’re straightforward moves that give you a huge, often guaranteed, return on your money.

Here are a few high-impact strategies to put on your radar:

- Capture Your Full 401(k) Match: If your job offers a 401(k) match, contributing enough to get the full amount is non-negotiable. It’s an instant 100% return on your money. Not doing this is literally turning down free cash.

- Use an HSA as a Secret Investment Tool: A Health Savings Account (HSA) is a powerhouse with a triple-tax advantage: your contributions are tax-deductible, the money grows tax-free, and withdrawals for medical expenses are also tax-free. What many miss is that after you build a certain balance, you can invest those funds, effectively turning your HSA into a secondary retirement account.

- Attack High-Interest Debt with a Vengeance: High-interest debt, especially from credit cards, is like trying to fill a bucket with a hole in it—it actively cancels out your savings progress. Two popular strategies are the avalanche method (tackling the highest-interest debt first) and the snowball method (clearing the smallest balance first for a quick psychological win). Pick the one that keeps you motivated.

Optimizing your savings goes hand-in-hand with learning how to reduce taxable income. Every dollar you don’t send to the taxman is another dollar you can put to work for your future.

Steer Clear of Common Savings Saboteurs

Knowing what not to do is just as important as knowing what to do. Plenty of well-intentioned savers get quietly derailed by a few common mistakes. The good news is that once you see these traps, they’re easy to avoid.

One of the most common missteps is letting too much cash sit idle in a standard, low-interest savings account. Sure, you need an emergency fund, but any cash beyond that is losing its buying power to inflation. If your savings account is earning 0.1% while inflation is running at 3%, your money is actually shrinking by 2.9% every year.

It’s easy to fall into these patterns without realizing it. Here’s a quick look at some of the most frequent mistakes and, more importantly, how to sidestep them.

Common Savings Pitfalls and How to Avoid Them

| Common Pitfall | Why It Happens | Actionable Solution |

|---|---|---|

| Lifestyle Inflation | The natural tendency to increase spending as income rises, often without conscious thought. | Pre-commit to saving at least half of every raise. Automate the increased savings transfer before the new paycheck even hits your account. |

| Ignoring the 401(k) Match | Not understanding the value of the match or feeling unable to contribute enough. | Start by contributing just enough to get the full match, even if it’s a small percentage. It’s the highest guaranteed return you’ll ever get. |

| Keeping Too Much in Cash | Fear of investing or simply not knowing where else to put the money. | Once your 3-6 month emergency fund is secure in an HYSA, direct new savings toward long-term investment accounts like an IRA or brokerage account. |

| “Mental Accounting” Errors | Treating a tax refund or bonus as “fun money” instead of part of your overall income. | Create a plan for windfalls before you receive them. Decide that 50% will go to savings, 30% to debt, and 20% for a guilt-free splurge. |

By actively managing these smart strategies and dodging these common pitfalls, you graduate from being a passive saver to becoming the active architect of your financial future. That level of intention is what truly accelerates wealth creation.

What If Your Paycheck Is Never the Same? Saving with an Irregular Income

Saving money is one thing when you get a steady, predictable paycheck. But what about when your income is all over the place? For freelancers, commission-based salespeople, and gig workers, standard budgeting rules like the 50/30/20 just don’t work. When your income fluctuates, trying to save a fixed dollar amount each month is a recipe for frustration.

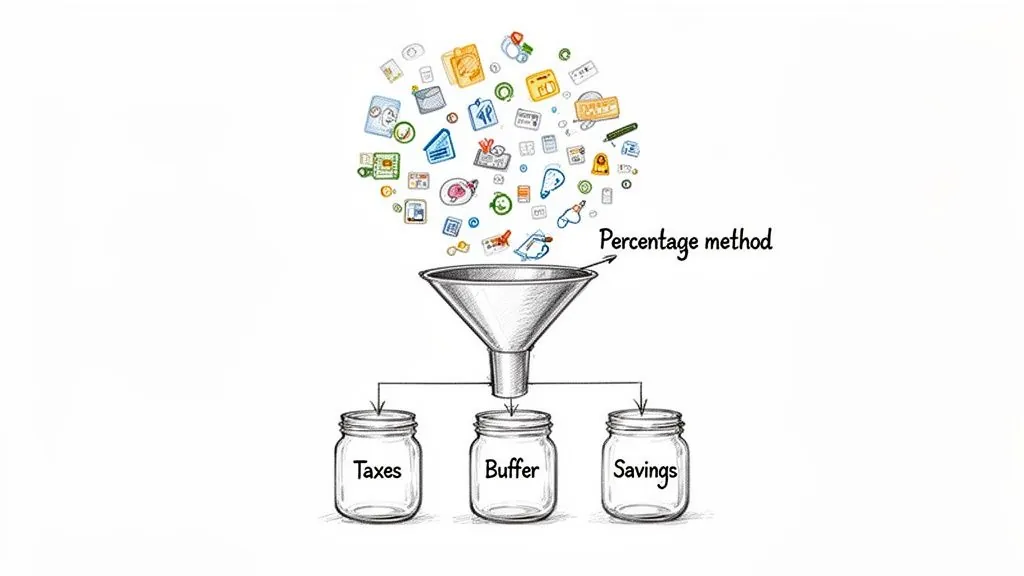

The secret isn’t about hitting a specific number. It’s about building a flexible system that rolls with the punches. The most powerful approach I’ve found is the percentage method. Forget fixed amounts and commit to saving a set percentage of every single dollar that comes in, whether it’s a huge client payment or a small side-hustle deposit. This creates the consistency your finances need, even when your cash flow is chaotic.

Putting the Percentage Method to Work

Let’s say you’re a freelance graphic designer. You decide to split every payment you receive into three buckets using a simple percentage rule. The moment money hits your account, you divide it.

- 30% for Taxes: This is non-negotiable and the first thing you should do. Set this money aside in a separate, untouchable savings account. This one habit alone will save you from the massive headache of a surprise tax bill.

- 20% for Savings: This chunk goes straight toward your goals—your emergency fund, investments, or saving for a down payment. You’re paying your future self first.

- 50% for Living Expenses: This is what you actually live on. It’s the money that covers your rent, groceries, and business expenses until the next check comes in.

If a client pays you $2,000, your system immediately kicks in: $600 zips over to your tax account, $400 heads to your savings, and the remaining $1,000 lands in your checking account for day-to-day life. You’re always covering your obligations before you even see the money to spend.

Build a Buffer to Smooth Out the Bumps

An emergency fund is critical for everyone, but for those with an irregular income, it’s your lifeline. The best way to manage inconsistent pay is by creating a “buffer” account that holds at least one month’s worth of essential living expenses.

Here’s how it works: all your income flows directly into this buffer account first. Then, on the first of every month, you pay yourself a fixed, predictable “salary” from this account into your primary checking account. This simple move creates the stability of a regular paycheck, smoothing out the financial roller coaster and making it infinitely easier to budget for fixed costs like rent. An irregular income budget template can be a game-changer for getting this structure in place.

The goal is to separate your income from your spending. Your monthly budget should be based on a consistent, self-paid salary, not the random timing of client payments. This mental and financial separation is the key to stability.

Why Separate Bank Accounts Are Your Best Friend

To make this system truly work, you need separate bank accounts. This isn’t about making things complicated; it’s about creating absolute clarity. When your tax money is sitting in its own dedicated account, it’s practically impossible to accidentally spend it on a weekend trip.

Here’s the ideal setup:

- Income Account: This is your landing zone. All payments from clients go here before you split them up.

- Tax Savings Account: A high-yield savings account where your tax percentage lives. Do. Not. Touch. This. Money.

- Long-Term Savings/Investment Account: This is your “future self” fund. Your savings percentage goes here to build wealth.

- Operating/Checking Account: This is your main spending account. Your fixed “salary” from your buffer account gets transferred here to cover all your monthly bills and daily spending.

This structure automates good financial habits. By immediately slicing off your tax and savings percentages, you’re only left with what’s truly available to spend. It takes the guesswork and stress out of managing your money, giving you a reliable path to save no matter how much your income fluctuates.

Common Questions About Saving From Your Paycheck

Even the best-laid plans run into real-world questions. Getting tripped up by common hurdles can stall your progress, but knowing the answers ahead of time keeps you moving forward. Let’s tackle some of the most frequent sticking points people face when they start saving from their salary.

What Percentage of My Salary Should I Actually Save?

You’ve probably heard of the 50/30/20 rule, which suggests saving 20% of your income. That’s a great benchmark, but let’s be realistic: the best savings rate is the one you can actually stick with.

Don’t beat yourself up if 20% feels impossible right now. The goal isn’t to hit some perfect number on day one; it’s to build the habit of saving.

Start where you can. If that’s only 5%, that’s a fantastic starting point. Automate that 5% transfer right after your paycheck hits and celebrate the win. Consistency is so much more powerful than the initial amount. You can always nudge that percentage up later as you get a raise or cut back on expenses.

How Can I Save Money if I’m Living Paycheck to Paycheck?

When your budget is stretched to its limit, the idea of saving can feel completely out of reach. The first, most critical step is to track your spending like a hawk for one full month. I mean everything—from your morning coffee to that streaming service you forgot you had.

This exercise is incredibly revealing. It almost always uncovers small, recurring “leaks” in your budget that you can easily plug. Maybe it’s canceling an unused subscription or brown-bagging lunch a couple of times a week. That alone could free up $50 or more a month. That small amount becomes the seed money for your starter emergency fund, giving you the breathing room you need to finally break the cycle.

A small emergency fund—even just $1,000—is the buffer that stops a flat tire from becoming a credit card disaster. It’s your first real step toward financial stability.

Should I Save Money or Pay Off Debt First?

Ah, the classic dilemma. The answer isn’t “one or the other”—it’s a balancing act that requires a specific order of operations. You need to do both.

- First, build a small emergency fund. Aim for $1,000. This safety net is non-negotiable. It stops you from digging a deeper debt hole the next time an unexpected bill pops up.

- Next, attack high-interest debt with a vengeance. Once your buffer is in place, throw every spare dollar you have at debts with interest rates over 7%—think credit cards and personal loans. The interest you save is a guaranteed, tax-free return on your money.

- Then, balance other goals. For lower-interest debt like a mortgage or federal student loans, it’s perfectly fine to make your regular payments while also starting to contribute to long-term retirement investments.

Where’s the Best Place to Keep My Savings?

The right home for your money depends entirely on its purpose. You wouldn’t use a checking account for retirement, and you wouldn’t lock up your emergency cash in the stock market. Think of it as assigning a “job” to every dollar.

- Emergency Fund: This money needs to be safe and liquid. A high-yield savings account is perfect here. It offers much better interest rates than a traditional savings account without tying up your cash when you need it most.

- Medium-Term Goals (1-5 years): For goals like a house down payment or a new car, a high-yield savings account is still a great option. A Certificate of Deposit (CD) can also work well if you’re sure you won’t need the money before it matures.

- Long-Term Goals (5+ years): This is where you put your money to work. For retirement, investing in a diversified portfolio through a tax-advantaged account like a 401(k) or an IRA is the most proven way to build serious wealth over time.

Ready to see your entire financial picture in one place and make smarter decisions? PopaDex provides the clarity you need to track your savings, investments, and net worth with ease. Stop guessing and start building your future with confidence. Get started with PopaDex today.

Now You Know Your Pay — Are You Building Wealth?

Salary is what you earn. Net worth is what you keep. Track whether your income is actually building wealth — connect your accounts in under 2 minutes with PopaDex.

Now You Know Your Pay — Are You Building Wealth?

Salary is what you earn. Net worth is what you keep. Track whether your income is actually building wealth — connect your accounts in under 2 minutes with PopaDex.