Our Marketing Team at PopaDex

Irregular Income Budget Template for Financial Stability (2026)

Why Traditional Budgets Leave Irregular Earners Behind

If you’ve ever tried to force your fluctuating income into a standard monthly budget, you know the frustration all too well. It’s like trying to fit a square peg into a round hole—it just doesn’t work. Most conventional budgeting advice is built on the idea of a steady, predictable paycheck. But for freelancers, gig workers, and contractors, that couldn’t be further from the truth. Your financial life isn’t a calm stream; it’s a series of peaks and valleys.

This fundamental mismatch is exactly why a specialized irregular income budget template is more than a nice-to-have; it is an absolute necessity. Traditional methods fail because they can’t handle the unpredictability you deal with every month. One month, you might land a huge project that floods your bank account. The next could be a scramble just to cover the basics. Trying to set fixed spending categories based on a single month’s income is a recipe for disaster, leading to needless penny-pinching during good months or panic and debt during slow ones.

The Feast-or-Famine Cycle Is Real

The biggest problem is what’s known as the feast-or-famine cycle. A traditional budget might encourage you to ramp up your spending when you have a high-income month, but it has no system for saving that surplus for the lean times that are sure to follow. This creates a stressful financial rollercoaster. For example, a graphic designer might earn $8,000 in October from a major client but only bring in $1,500 in November. A standard budget treats these months as separate events, completely missing the need to smooth that income across both periods.

This cycle is a defining characteristic of the modern workforce. With the rise of flexible work, more people than ever are facing this challenge. In the United States alone, roughly 36% of workers now participate in the gig economy. That’s a huge portion of the population for whom old-school financial planning simply doesn’t cut it. For a deeper look at this trend, you can explore the government’s findings on the freelance economy. This shift highlights the urgent need for a better way to manage money.

Here’s a snapshot of recent data on contingent and alternative employment from the U.S. Bureau of Labor Statistics.

This data shows just how many workers fall outside the typical full-time employee model, reinforcing why rigid budgeting methods are becoming obsolete for a large part of the workforce.

Unique Challenges That Break Old Models

Beyond income volatility, people with irregular incomes face other hurdles that standard budgets completely ignore:

- Quarterly Estimated Taxes: Unlike salaried employees who have taxes withheld automatically, you’re on the hook for setting money aside and paying the IRS four times a year. A regular budget has no built-in spot for this.

- Inconsistent Business Expenses: Your costs for software, marketing, or materials can swing just as much as your income, a variable most personal budgets aren’t designed to handle.

- No Paid Time Off: Planning for vacations or sick days means you have to proactively build your own safety net, a concept that is foreign to traditional budgeting frameworks.

These factors demand a more dynamic and flexible system. If you want to dive deeper into the core principles of money management, it’s worth mastering budgeting as a path to financial freedom. It’s time to ditch the rigid, outdated models and embrace a template built for your reality.

Building Your Financial Foundation That Actually Works

Let’s be real. A budget for an irregular income isn’t some rigid spreadsheet you force yourself to look at once a month. It’s a dynamic, flexible system designed for the chaos of real life, especially when your paycheck changes all the time. The idea is to create a financial bedrock that smooths out the high and low months, giving you a sense of control even when you can’t predict your exact income. This all starts with an honest look at your numbers—no wishful thinking allowed.

Calculate Your Baseline Income

First things first, you need to find your baseline income. This isn’t your best month ever, or the income you hope to make. It’s the absolute lowest amount you brought in during a single month over the past year. Think of this number as your financial safety net; it’s the foundation for a budget that can survive a worst-case scenario. This helps you figure out what you can truly afford every month, no matter what happens.

Once you’ve identified that rock-bottom number, it’s time to list your essential, can’t-live-without expenses. These are often called the “four walls” that you absolutely must keep standing:

- Housing: Your rent or mortgage payment.

- Utilities: The basics like electricity, water, heat, and internet.

- Food: A realistic monthly grocery bill.

- Transportation: What you need for gas, public transit, or essential car repairs.

This list is about survival needs, not wants. When you subtract these essential costs from your baseline income, you get your true “survival” number. Knowing this figure is incredibly powerful because it tells you the bare minimum you need to earn to stay afloat, which cuts through a lot of financial anxiety.

Establish a Smart Buffer System

With your survival budget mapped out, the next step is building a buffer. A classic mistake is to see any income above your baseline as “fun money” for immediate spending. Instead, this surplus is your secret weapon for managing an unpredictable income. Any money you earn that’s over your baseline should be automatically moved into separate savings accounts. I recommend setting up different “pots” for specific goals, like a tax fund, an emergency fund, and a true income buffer to pull from during slower months.

You can see how a simple budgeting tool helps bring these categories to life.

This screenshot shows how modern apps, like the one from Mint, let you categorize your spending. This is essential for seeing exactly where your money is going and figuring out where to direct any surplus. Turning abstract numbers into a visual breakdown makes it much easier to see your progress and stick with your financial plan.

Why Irregular Income Budgeting Became Essential

The idea of an irregular income budget template wasn’t just a random thought; it grew from real-world financial shifts and is now a vital tool for a huge slice of the workforce. For a long time, all financial advice seemed to be for people with a steady 9-to-5 paycheck. But as the economy changed, it became clear that traditional budgeting just didn’t work for anyone whose income went up and down.

From Crisis Comes Innovation

The real wake-up call was the 2008 global financial crisis. As stable jobs became harder to find, millions of people flocked to freelancing and contract work to get by. This created a huge problem: how do you manage your money when you don’t know how much you’ll make next month? These new entrepreneurs were trying to use old, outdated budgeting methods for a completely new financial reality.

It took time, but people adapted. Financial data shows that specialized budgeting methods started gaining serious traction after this disruption. A 2015 survey found that only 10% of freelancers were using a formal budget designed for their income style. Fast forward to 2023, and that number skyrocketed to almost 48%. To see just how much the economy has changed, you can explore more about this economic evolution and its impact and understand the full story.

To better understand why a different approach is necessary, let’s look at a few common methods people with fluctuating incomes use.

| Method | Best For | Complexity Level | Success Rate | Time Investment |

|---|---|---|---|---|

| Pay Yourself a “Salary” | Those who want paycheck-like predictability and can build a buffer. | Medium | High | Moderate setup, low maintenance |

| The 50/30/20 Rule (Modified) | Beginners who need a simple framework to start. | Low | Moderate | Low |

| Zero-Based Budgeting | Detail-oriented individuals who want to account for every dollar each month. | High | Very High | High |

| Envelope System (Digital/Physical) | Visual budgeters who need to physically or digitally separate funds. | Medium | High | Moderate |

Each method has its pros and cons, but they all share a common goal: to bring order to financial chaos. The key is finding the one that fits your personality and financial situation.

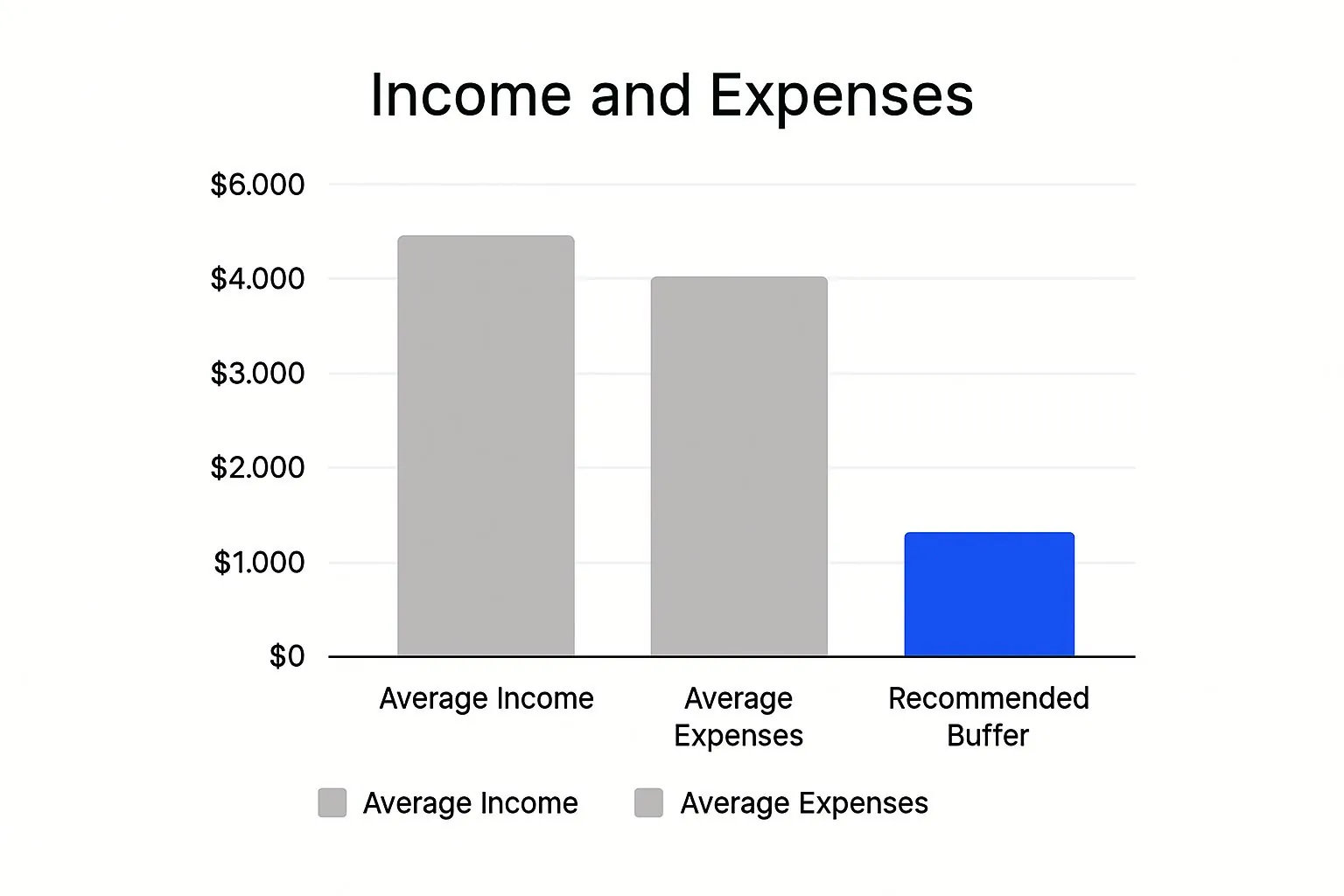

The infographic below really drives home the financial reality for many households, showing the disconnect between income, expenses, and the safety net needed to stay afloat.

This visual shows why just “earning more” often isn’t the answer. Without a proper system to manage the highs and lows, you’re always one slow month away from financial stress.

The Modern Gig Economy Demands a New Approach

Today, what began as a reaction to a crisis has become a smart strategy for anyone in the modern economy. With the explosion of the gig economy and flexible work, income volatility is no longer an exception—it’s the norm for many. Often, the biggest difference between two freelancers earning the same amount annually is their budgeting system.

Those who use a structured template are prepared for lean months, can set aside money for taxes, and save for big goals. Others often get trapped in a stressful cycle of feast or famine. As more people move away from traditional career paths, knowing how to manage money without a predictable paycheck is more important than ever.

Customizing Your Template For Real-World Success

An irregular income budget template is a great starting point, but its real power is unlocked through personalization. Your financial life isn’t a one-size-fits-all situation, so your budget shouldn’t be either. Think of it like a suit: the off-the-rack version works, but a custom fit makes all the difference. This is about turning a basic spreadsheet into a personal financial command center that reflects your unique earning patterns.

The first step is to sync your template with the rhythm of your industry. A wedding photographer’s income, for instance, is heavily seasonal, with most earnings packed between May and October. Their template should feature a dedicated “off-season” fund, where a percentage from every busy summer wedding payment is automatically stashed away. This simple move prevents the panic that can set in during the slower winter months, turning a predictable slowdown into a planned rest period.

Fine-Tuning For Multiple Income Streams

Many people with fluctuating income, from freelance writers to rideshare drivers, are managing money from several sources. A generic template might just lump everything into one big pot, but a customized one creates separate categories for each income stream. This approach delivers critical insights. You might find that one client makes up 60% of your income—a risky position—or that a small side project is surprisingly profitable for the hours you put in.

To get a better handle on this, you’ll want to assign every dollar a specific job, a core principle for managing variable income.

This image, from a budgeting tool like YNAB, illustrates how you can give every dollar a purpose, from covering rent to funding your next vacation. For anyone with an irregular income, this level of detail is crucial. It ensures that extra cash from a good month is deliberately allocated rather than accidentally spent.

Making your template work for you often involves some specific tweaks based on how you earn. The table below outlines some common scenarios and the modifications that can make a big difference.

| Income Type | Key Modifications | Priority Features | Common Challenges | Success Tips |

|---|---|---|---|---|

| Freelancer (Project-Based) | Add categories for individual clients/projects. Include a line for a self-employment tax fund. | Invoice tracking, projected income fields, tax savings bucket. | Unpredictable payment schedules, scope creep affecting profitability. | Set aside 25-30% of every payment for taxes immediately. Use project profitability to guide future rates. |

| Gig Worker (e.g., Rideshare) | Track income by platform. Separate business expenses (gas, maintenance) from personal. | Mileage tracker integration, real-time expense logging, weekly profit calculation. | High variable expenses, inconsistent daily/weekly earnings. | Calculate your net hourly rate after expenses to identify the most profitable times to work. |

| Commission-Based Sales | Create a “base vs. commission” income section. Build a “draw” fund to smooth out low-commission months. | Sales pipeline forecast, commission calculator, savings goals for large purchases. | “Feast or famine” income cycles, long sales cycles with delayed payouts. | Live on your base salary (if you have one) and use commission checks for debt, savings, and investments. |

| Seasonal Worker (e.g., Tourism) | Implement “On-Season” and “Off-Season” views. Automate transfers to a long-term savings fund during peak months. | High-yield savings account integration, automated savings transfers. | Covering expenses during the off-season, managing large lump-sum payments responsibly. | Calculate your total off-season living expenses and divide that by the number of on-season paychecks to know how much to save. |

This table shows there’s no single “right” way to set up your budget. The goal is to create a system that addresses your specific financial pressures and opportunities, giving you a clear path forward no matter what your next paycheck looks like.

Accounting for Business-Specific Expenses

Finally, true customization means building your business finances directly into your budget. A standard personal budget template simply doesn’t have fields for software subscriptions, marketing costs, or client lunches. Yours must.

Create dedicated categories for these variable business expenses. Doing this helps in two major ways:

- Accurate Tax Planning: It lets you meticulously track deductions, which can save you a significant amount of money when you file your taxes.

- Smarter Business Decisions: Seeing your expenses laid out clearly helps you analyze your return on investment. Is that pricey software subscription actually boosting your productivity enough to justify its cost? Your budget will tell you.

By making these kinds of adjustments, you go beyond simple expense tracking. You build a living document that adapts with you, providing clarity and stability in the face of financial uncertainty. For more ideas on getting your finances in order, you can explore our guide on how to organize your finances for clarity and control.

Making Your Budget Work In The Real World

Having a perfectly customized irregular income budget template is a great starting point, but it’s essentially worthless if it just collects digital dust in your downloads folder. The real change happens when you weave your budget into the fabric of your daily financial life. This is where your template shifts from a static document into a dynamic partner for managing your money. The goal is to make it a living tool that guides your decisions, not a chore you dread.

Establish a Realistic Review Cycle

Forget the rigid monthly check-ins that traditional budgets preach. Your income isn’t monthly, so why should your reviews be? A key strategy for success is to set a review cycle that mirrors your actual cash flow. If you get paid after each project, that’s the perfect time to update your budget. If your income arrives in weekly bursts, a Sunday evening review might be your best bet. This frequent, low-effort engagement keeps you connected to your numbers without feeling overwhelming.

This regular interaction turns budgeting from a reactive task into a proactive habit. Instead of scrambling at the end of the month to figure out where your money went, you’re making small, informed adjustments in real-time. This approach also has a significant psychological benefit. Using an irregular income budget template has a direct impact on financial wellness. Studies show that 65% of irregular earners who consistently track their fluctuating incomes report lower financial anxiety compared to just 40% of those who don’t. You can explore the research on financial stability for variable earners to understand these findings more deeply.

Use Your Data to Make Smarter Decisions

Think of your budget as more than just a tracker for expenses; it’s a powerful source of business intelligence. By analyzing your income patterns over time, you can uncover trends you never knew existed. You might discover which types of projects consistently bring in the most money or pinpoint your most profitable months. This insight allows you to plan for slower periods with much more confidence, shifting you from simply surviving your irregular income to actively optimizing it.

A great way to put this into practice is by visualizing how you allocate each payment. When a check comes in, immediately divide it into manageable chunks for your needs, wants, and savings goals.

This visual approach, often recommended by financial platforms like Credit Karma, is a vital practice for anyone with a variable income. It ensures that every dollar has a specific job, whether that’s covering essential bills, paying down debt, or building your savings buffer. By consistently applying this logic, your budget becomes more than just a plan—it transforms into a roadmap that leads to genuine financial peace of mind and growth.

Advanced Strategies For Long-Term Wealth Building

Once you get a good handle on your month-to-month finances, your irregular income budget template stops being just a defensive shield and starts acting as a launchpad for building real wealth. This is where things get exciting. You’re no longer just weathering financial storms; you’re using the nature of your variable income to your advantage and chasing goals that might seem out of reach for someone on a fixed salary.

Tax Strategies For Variable Earners

One of the greatest financial opportunities for anyone with an unpredictable income stream is smart tax planning. Unlike salaried employees with limited options, you have a surprising amount of control. Your budget template should have a specific category for estimated tax payments. A good rule of thumb is to set aside 25-30% of every single check you receive.

By treating taxes like a non-negotiable business expense from the get-go, you avoid that panicked scramble every quarter. Plus, the detailed expense tracking you’re already doing allows you to maximize deductions for your home office, business software, travel, and professional development courses, which could save you thousands each year.

The real takeaway here is making tax savings an automatic, immediate action. This single habit is a cornerstone for financially successful freelancers and business owners, preventing a huge source of future stress.

Investing With Unpredictable Cash Flow

Investing can feel like a tall order when you don’t have a predictable paycheck, but it’s completely doable with the right approach. Instead of trying to invest a fixed amount every month, which can be stressful, switch to a percentage-based strategy.

For instance, you could decide to invest 10% of all income that comes in after your baseline monthly expenses are covered.

- During a fantastic month: You might invest a significant chunk of money.

- During a lean month: You might not invest anything at all, and that’s okay.

This method, sometimes called “drip investing,” lets you consistently grow your portfolio without putting a strain on your essential budget.

You can even automate this process. Many bank accounts allow you to set up “sweep” transfers that automatically move any cash above a certain threshold into your investment accounts. This makes wealth-building feel passive and effortless. These advanced moves are much easier when your household finances are crystal clear, which is especially vital when navigating money management for couples. By using the data from your budget to fuel these strategies, your irregular income transforms into a powerful engine for long-term growth. It’s proof that financial security comes from smart systems, not just a steady paycheck.

Your Roadmap To Financial Confidence And Growth

Mastering an irregular income budget isn’t about hitting every target perfectly from day one. Instead, think of it as building a resilient financial system that can bend and flex with the unpredictable nature of your life and work. True financial confidence is built on small, consistent habits, not on chasing unrealistic numbers. This roadmap is all about creating lasting momentum and turning your irregular income budget template into a core part of how you manage your money for good.

Staying Motivated and Measuring Progress

Let’s be real: some months are going to be tough. You’ll hit a slow period where looking at your expenses feels more discouraging than productive. When this happens, perspective is everything. Instead of fixating on the dollar amounts, start measuring your progress by your actions. Did you track every expense, even when it felt painful? That’s a win. Did you stick to your baseline budget and avoid taking on new debt? That’s a huge win.

To keep the momentum going, especially when life gets busy and tracking can easily slip, try these simple strategies:

- The Five-Minute Check-In: Set aside just five minutes every day to update your template. This small, daily habit is much easier to stick with than a long, overwhelming weekly session and stops the data from piling up.

- Celebrate the Small Victories: When you successfully move money into your tax savings or pay a bill using funds from your income buffer, take a moment to acknowledge it. This kind of positive reinforcement is what builds real, lasting confidence.

- Review Your “Why”: Always keep your long-term goals in sight. Whether you’re saving for a down payment on a house or a completely stress-free vacation, reminding yourself what all this effort is for can be an incredibly powerful motivator.

This approach shifts the focus from simply managing money to building habits that create genuine financial resilience. Your template stops feeling like a restriction and becomes a tool that empowers your choices, guiding you toward greater stability and growth.

Ready to put this into practice? Download our free Irregular Income Budget Template for Excel — it includes income averaging, baseline budgeting, priority-based expense allocation, and a tax reserve calculator all built in. Or take control of your entire financial picture with PopaDex. Our intuitive platform helps you track every asset and liability in one place. Start your free trial today.

You might also find these templates useful:

- Personal Budget Template Excel — Standard monthly budget with 50/30/20 tracking

- Net Worth Tracker Google Sheets — Track your total wealth in the cloud

- Net Worth Statement Template — Formal balance sheet for loan applications