Our Marketing Team at PopaDex

What Is Net Cash Flow A Guide to Your Financial Health

Think of your finances like a heartbeat.Think of net cash flow as your financial heartbeat. It’s the simplest, most honest look you can get at your financial health, showing you exactly how much money is actually moving in and out of your accounts over a specific time.

In short, it’s the difference between all the cash you receive and all the cash you spend.

The True Meaning of Net Cash Flow

Unlike complicated metrics like profit or net worth, net cash flow cuts right to the chase. It answers one simple but critical question: are you bringing in more money than you’re sending out? For day-to-day financial decisions, this single number is often more powerful than any other because it deals with real, spendable cash.

Let’s try an analogy. Picture your bank account as a bathtub. The water flowing in from the faucet is all your income—your salary, any side hustle earnings, or investment dividends. The water going down the drain represents all your expenses, like rent, groceries, and loan payments. Net cash flow is simply whether the water level in the tub is rising or falling each month.

Why This Simple Number Matters

Getting a handle on this concept is the first step toward real financial control. It gives you an immediate, unfiltered look at the impact of your spending habits and income streams. A consistently positive flow is the bedrock for hitting any major financial goal, whether it’s for you personally or for your small business. You can dive deeper into how a healthy surplus works in our guide to what is positive cash flow.

Your net worth tells you where you are today, but your net cash flow tells you where you’re headed. It’s the engine that drives wealth creation, giving you the extra cash needed to save, invest, and crush debt.

This metric is especially vital in certain industries. For instance, understanding what is cash flow in real estate is non-negotiable, as it directly determines whether a property is a smart investment or a financial drain.

Breaking Down Your Cash Inflows and Outflows

Before you can get a handle on your net cash flow, you need to get real about what’s coming in and what’s going out. Think of it as a quick, no-nonsense audit of your financial life. On one side, you have all the money flowing into your accounts—your cash inflows.

This isn’t just about your nine-to-five paycheck. To get the full picture, you need to account for every single dollar coming your way, no matter how small.

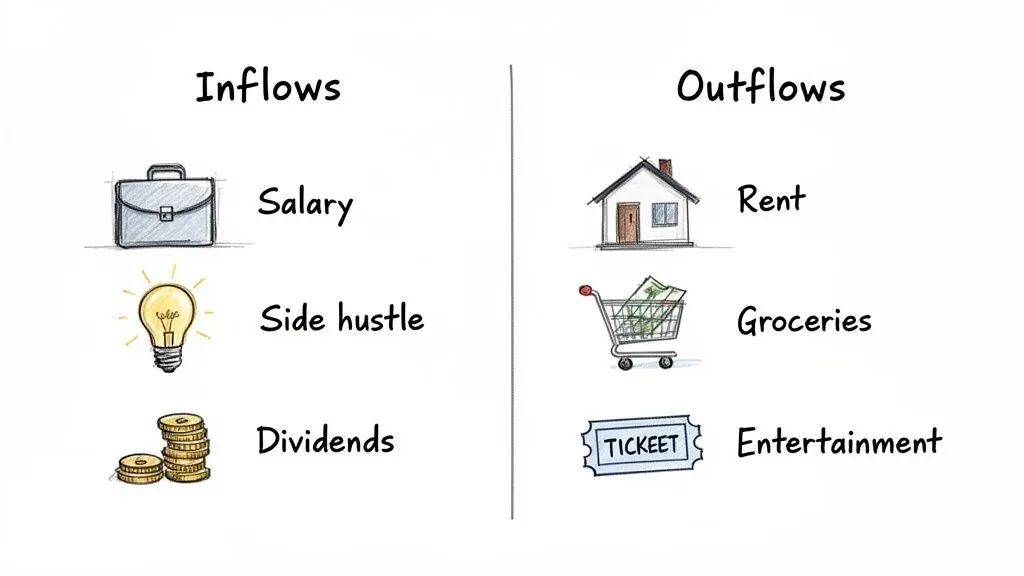

Identifying Your Cash Inflows

Your cash inflows are the engine of your finances. They’re every dollar you receive, and they usually fall into a few key buckets:

- Earned Income: This is the most obvious one. It’s your salary, wages from a part-time gig, or any cash you pull in from a side hustle or freelance work.

- Investment Income: This is your money working for you. Think stock dividends, interest from a high-yield savings account, or rent you collect from a property.

- Other Income: Don’t forget the one-offs. This category covers everything else, like a tax refund, a surprise work bonus, or even cash gifts.

Laying out every source gives you the first half of your net cash flow equation. It’s the essential first step before you can effectively track cash flow and start making real progress.

Pinpointing Your Cash Outflows

On the flip side, you have your cash outflows—every dollar that leaves your pocket. This is where your money actually goes, and expenses tend to fall into two main camps: fixed and variable.

Fixed Costs: These are the predictable bills that hit your account like clockwork every month. We’re talking rent or mortgage payments, your car loan, and insurance premiums.

Variable Costs: These are the expenses that change based on your day-to-day choices. Think groceries, dinners out with friends, concert tickets, and your electricity bill.

Understanding where your money goes is crucial. It shows the direct link between your spending habits and your overall financial health. This isn’t just a personal finance rule; it’s a principle that applies on a massive scale, where U.S. corporate net cash flow can run into the trillions. You can dig into these large-scale financial trends on the St. Louis Fed website if you’re curious.

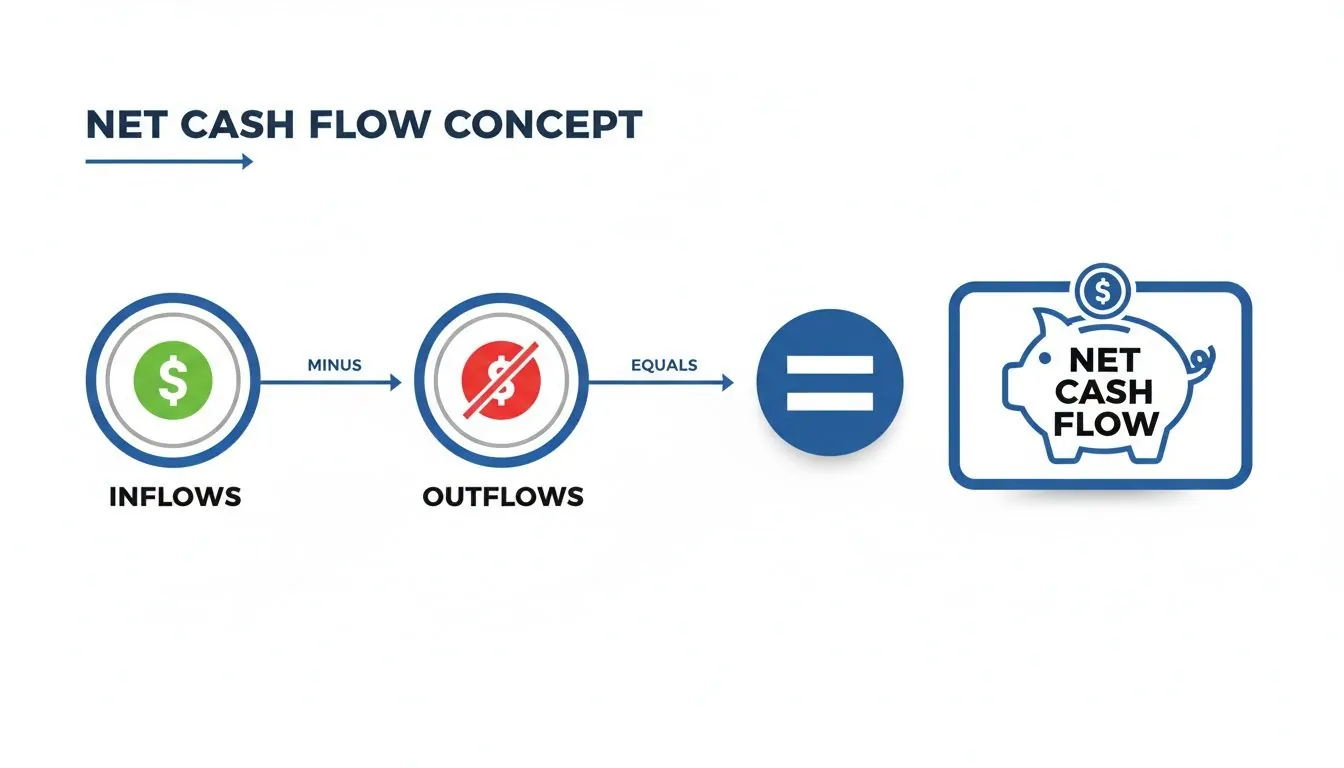

The Simple Formula for Calculating Your Net Cash Flow

You don’t need an accounting degree or fancy software to figure out your net cash flow. The logic behind it is refreshingly simple and boils down to one powerful formula.

Total Cash Inflows - Total Cash Outflows = Net Cash Flow

This single calculation gives you the clearest possible picture of your financial performance over a specific period—whether that’s a week, a month, or a quarter. It cuts straight through the noise and tells you one thing: are you bringing in more cash than you’re spending?

To get your number, you just add up every dollar that came in (inflows) and subtract every dollar that went out (outflows). The result is your net cash flow, a single figure that reveals your financial momentum.

Putting the Formula Into Action

Let’s walk through a couple of real-world scenarios to see how this works. These examples show how anyone can use the net cash flow formula to get immediate financial clarity.

Example 1: A Salaried Professional Meet Alex, a graphic designer with a predictable monthly salary. Here’s a look at their finances for the month:

- Cash Inflows:

- Monthly Salary (after tax): $4,500

- Freelance Project Payment: $500

- Total Inflows = $5,000

- Cash Outflows:

- Rent & Utilities: $1,800

- Groceries & Dining: $700

- Car Payment & Insurance: $450

- Student Loan Payment: $300

- Subscriptions & Entertainment: $250

- Total Outflows = $3,500

Plugging these numbers into the formula, Alex’s calculation is simple:

$5,000 (Inflows) - $3,500 (Outflows) = +$1,500 Net Cash Flow

Alex ended the month with a $1,500 surplus. This is money that can now be put to work—building savings, making investments, or knocking down debt faster. This positive result is the engine that builds wealth.

Net Cash Flow Vs. Profit And Net Worth

It’s easy to lump financial terms together, but net cash flow, profit, and net worth each tell a completely different story about your financial health. Getting them mixed up can lead to a false sense of security or, just as bad, needless panic. Understanding what makes each one unique is the first step toward making smarter money moves.

For instance, profit can be a tricky number. A business might look great on paper, showing a hefty profit, but have zero cash in the bank because its clients are slow to pay their invoices. Profit is an accounting figure that can include money you haven’t received yet. Net cash flow, on the other hand, is the cold, hard truth of what money has actually moved in or out of your accounts.

Your Financial Snapshot Vs. Your Financial Story

The difference between net worth and net cash flow is best captured with an analogy.

Think of your net worth as a single photograph—a static snapshot of your finances on one specific day. It shows what you own (assets) minus what you owe (liabilities). Your net cash flow, however, is the video. It reveals the momentum and direction of your money over time, showing whether you’re moving forward or falling behind.

It really is that simple: cash coming in minus cash going out.

This focus on the actual movement of money is crucial for understanding the real-world health of a business. To dig deeper, it’s worth exploring the Difference Between Cash Flow & Profit.

Putting The Pieces Together

To make sense of these concepts, it helps to see them side-by-side. Each metric provides a different lens through which to view your financial situation, and you need all three for a complete picture.

| Metric | What It Measures | Why It Matters |

|---|---|---|

| Net Cash Flow | The actual cash moving in and out of your accounts over a period. | Shows your ability to cover immediate expenses and stay afloat. It’s about liquidity. |

| Profit | Revenue minus expenses on an accounting basis (can include non-cash items). | Indicates operational efficiency and long-term viability, but not necessarily cash on hand. |

| Net Worth | Your total assets minus your total liabilities at a single point in time. | Provides a “big picture” view of your overall financial position and wealth accumulation. |

Ultimately, a profitable business with negative cash flow is living on borrowed time. And a high net worth doesn’t help pay this month’s bills if all your assets are tied up and your cash flow is negative. They all have to work together.

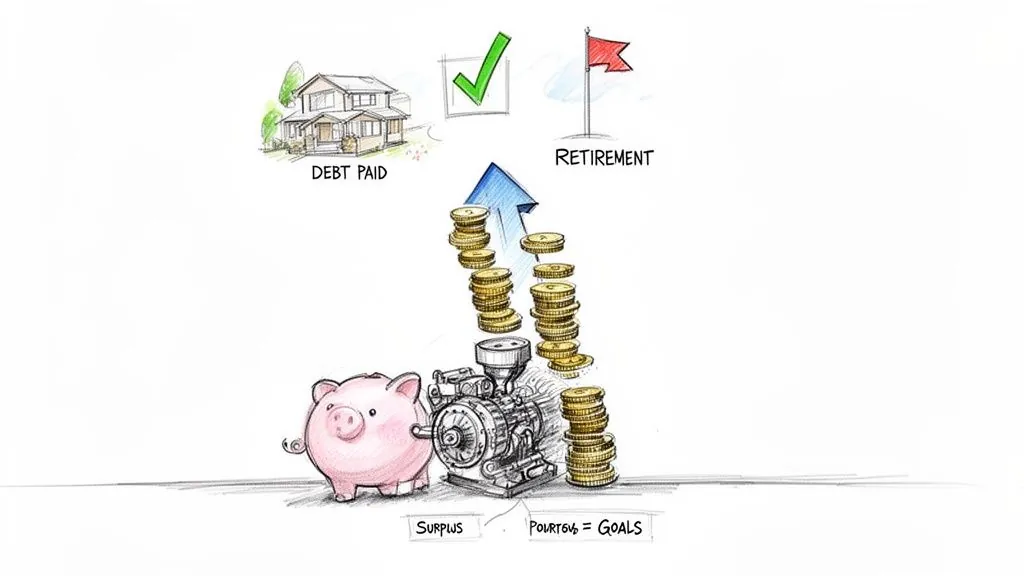

Why Net Cash Flow Drives Your Financial Goals

Want to buy a home, achieve financial independence, or retire early? Your success hinges almost entirely on net cash flow. While your net worth is a snapshot of where you are today, net cash flow is the engine showing you where you’re going—and how fast you’ll get there.

Think of a positive net cash flow as your monthly surplus. This isn’t just some leftover change; it’s the raw material for building serious wealth. It’s the cash that gives you the power to make real moves.

When you consistently bring in more than you spend, you unlock the freedom to:

- Aggressively pay down debt, saving yourself thousands in interest payments.

- Build a robust emergency fund, creating a financial cushion for life’s surprises.

- Make meaningful investments, putting your money to work so it can grow over time.

This surplus is how you shift from just tracking numbers to making them work for you. It’s the difference between financial stagnation and tangible progress.

Turning Your Goals into Reality

Tracking this one metric helps you spot spending leaks, make smarter decisions, and gain true control over your financial destiny. For example, a positive flow of just a few hundred dollars a month can be channeled directly into an investment account, where it immediately starts compounding.

This same principle plays out on a massive scale in the investment world. Net cash flow into Exchange-Traded Funds (ETFs) is a key indicator of investor sentiment and market liquidity. Global ETF assets soared to a record $18.81 trillion by the end of September 2025, powered by $1.54 trillion in net inflows that year alone.

For a savvy individual investor, these massive flows can signal opportune moments to adjust a personal portfolio and ride market momentum. With a platform like PopaDex, you can easily monitor how these large-scale trends affect your own net worth. You can find more insights on these trends by reading about global ETF asset trends at etfgi.com.

Your financial goals are not achieved by your income alone, but by the portion of that income you can direct toward your future. This is the essence of net cash flow.

Ultimately, a consistently positive net cash flow isn’t just a nice-to-have metric. It’s the single most important driver for turning your long-term financial dreams into a concrete, achievable plan.

Put Your Finances on Autopilot with PopaDex

Figuring out your net cash flow is a great start, but the real magic happens when you track it consistently. Let’s be honest—pulling numbers from bank statements, credit card bills, and investment portals every month is a massive headache and an easy way to make mistakes. That’s exactly why we built PopaDex.

PopaDex takes that manual work off your plate and acts as your single financial command center. It doesn’t just give you a static photo of your net worth; it shows you a live video of your money as it moves.

See the Full Financial Story

When you securely link your accounts, you get a single, clear view of every dollar you have. This brings together:

- Bank and savings accounts

- Credit card spending

- Investment portfolio performance

- Outstanding loans and mortgages

This setup makes it incredibly simple to keep an eye on your cash inflows and outflows. PopaDex pieces everything together so you can see your true net cash flow at a glance, updated in real time. This is a game-changer for anyone with complex finances, especially if you’re managing accounts in different currencies from living or working abroad. You can learn more about how PopaDex securely connects your accounts through our financial data aggregation process.

PopaDex turns confusing numbers into clear, actionable insights. Its simple visualizations chart your financial progress, helping you spot trends, tweak your budget, and make smart decisions with total confidence.

With this kind of clarity, you can stop just calculating your net cash flow and start actively managing it. The platform shows you exactly where your money is going, helps you find opportunities to save or invest more, and empowers you to build real, lasting financial stability. When you put your financial data to work, you get the control you need to hit your goals faster.

Common Questions About Net Cash Flow

Even with a clear formula, some practical questions always pop up when you start digging into your finances. Getting the nuances of what is net cash flow right helps you read the numbers correctly and, ultimately, make smarter money moves. Let’s tackle a few common ones.

What Does Negative Net Cash Flow Mean?

Seeing a negative number can feel like a punch to the gut, but it isn’t automatically a red flag. A net cash outflow just means you spent more cash than you brought in during that specific window of time. This is totally normal if you made a big, planned purchase—like paying for a vacation, putting a down payment on a car, or buying new equipment for your business.

The real trouble starts when your cash flow is consistently negative without a good reason. That’s a sign you’re burning through your savings and probably need to take a hard look at your budget.

How Often Should I Calculate It?

Honestly, the right frequency depends on your financial rhythm. For most people with regular paychecks or a stable business, calculating net cash flow monthly is the sweet spot. It lines up perfectly with most bills and income cycles, giving you a reliable snapshot of where you stand.

But if you’re a freelancer with lumpy income or a business in a high-growth (and high-spend) phase, you might want to check it weekly. More frequent check-ins help you spot cash crunches before they turn into full-blown crises.

At the end of the day, the goal is consistency. Pick a schedule you can actually stick to, and you’ll build a clear picture of your financial trends over time.

Ready to stop guessing and start seeing your real financial picture? PopaDex automates the entire process, connecting all your accounts to give you a live, accurate view of your net cash flow. Get started for free today and take control of your money.